QSE Falls 1.5% Led by Industrials, Insurance Stocks

•

1 gostou•322 visualizações

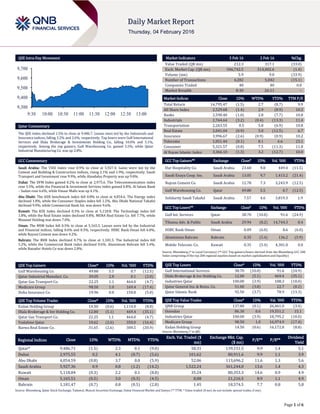

The QSE Index declined 1.5% to close at 9,486.7.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (16)

Semelhante a QSE Falls 1.5% Led by Industrials, Insurance Stocks

Semelhante a QSE Falls 1.5% Led by Industrials, Insurance Stocks (20)

Mais de QNB Group

Mais de QNB Group (20)

Último

Último (20)

QSE Falls 1.5% Led by Industrials, Insurance Stocks

- 1. Page 1 of 6 QSE Intra-Day Movement Qatar Commentary The QSE Index declined 1.5% to close at 9,486.7. Losses were led by the Industrials and Insurance indices, falling 3.2% and 2.6%, respectively. Top losers were Gulf International Services and Dlala Brokerage & Investments Holding Co., falling 10.0% and 5.1%, respectively. Among the top gainers, Gulf Warehousing Co. gained 5.5%, while Qatar Industrial Manufacturing Co. was up 2.8%. GCC Commentary Saudi Arabia: The TASI Index rose 0.9% to close at 5,927.4. Gains were led by the Cement and Building & Construction indices, rising 2.1% and 1.9%, respectively. Saudi Transport and Investment rose 9.9%, while Alandalus Property was up 9.8%. Dubai: The DFM Index gained 0.2% to close at 2,975.6. The Telecommunication index rose 3.5%, while the Financial & Investment Services index gained 0.8%. Al Salam Bank – Sudan rose 6.6%, while Emaar Malls was up 4.1%. Abu Dhabi: The ADX benchmark index fell 0.8% to close at 4,054.6. The Energy index declined 1.8%, while the Consumer Staples index fell 1.2%. Abu Dhabi National Takaful declined 9.9%, while Commercial Bank Int. was down 9.6%. Kuwait: The KSE Index declined 0.3% to close at 5,118.8. The Technology index fell 1.8%, while the Real Estate index declined 0.8%. MENA Real Estate Co. fell 7.7%, while Manazel Holding was down 7.0%. Oman: The MSM Index fell 0.5% to close at 5,165.5. Losses were led by the Industrial and Financial indices, falling 0.6% and 0.5%, respectively. HSBC Bank Oman fell 6.0%, while Raysut Cement was down 4.2%. Bahrain: The BHB Index declined 0.7% to close at 1,181.5. The Industrial index fell 5.2%, while the Commercial Bank index declined 0.6%. Aluminium Bahrain fell 5.4%, while Banader Hotels Co was down 2.8%. QSE Top Gainers Close* 1D% Vol. ‘000 YTD% Gulf Warehousing Co. 49.80 5.5 0.7 (12.5) Qatar Industrial Manufact. Co. 39.05 2.8 0.1 (2.0) Qatar Gas Transport Co. 22.25 1.1 464.0 (4.7) Medicare Group 98.50 1.0 169.4 (17.4) Doha Insurance Co. 19.96 0.8 158.8 (5.0) QSE Top Volume Trades Close* 1D% Vol. ‘000 YTD% Ezdan Holding Group 14.50 (0.6) 1,114.0 (8.8) Dlala Brokerage & Inv Holding Co. 12.00 (5.1) 469.4 (35.1) Qatar Gas Transport Co. 22.25 1.1 464.0 (4.7) Vodafone Qatar 10.62 (2.6) 350.0 (16.4) Barwa Real Estate Co. 31.65 (2.6) 309.5 (20.9) Market Indicators 3 Feb 16 2 Feb 16 %Chg. Value Traded (QR mn) 212.3 317.1 (33.0) Exch. Market Cap. (QR mn) 506,742.5 514,002.6 (1.4) Volume (mn) 5.9 9.0 (33.9) Number of Transactions 4,282 5,042 (15.1) Companies Traded 40 40 0.0 Market Breadth 8:30 26:11 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 14,795.47 (1.5) 2.7 (8.7) 9.9 All Share Index 2,529.68 (1.4) 2.9 (8.9) 10.2 Banks 2,590.40 (1.0) 2.8 (7.7) 10.8 Industrials 2,764.64 (3.2) (0.4) (13.3) 11.4 Transportation 2,263.55 0.5 5.8 (6.9) 10.8 Real Estate 2,041.04 (0.9) 5.0 (12.5) 6.7 Insurance 3,996.67 (2.6) (0.9) (0.9) 10.2 Telecoms 1,051.44 (0.1) 8.1 6.6 23.1 Consumer 5,321.57 (0.8) 7.5 (11.3) 11.8 Al Rayan Islamic Index 3,366.10 (1.3) 3.2 (12.7) 10.0 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Dur Hospitality Co. Saudi Arabia 23.68 9.8 449.4 (11.5) Saudi Enaya Coop. Ins. Saudi Arabia 13.05 9.7 1,413.2 (21.4) Najran Cement Co. Saudi Arabia 12.78 7.3 3,243.9 (12.5) Gulf Warehousing Co. Qatar 49.80 5.5 0.7 (12.5) Solidarity Saudi Takaful Saudi Arabia 7.57 4.6 3,819.3 1.9 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Gulf Int. Services Qatar 38.70 (10.0) 91.6 (24.9) Tihama Adv. & Public Saudi Arabia 29.94 (8.2) 14,744.3 0.4 HSBC Bank Oman Oman 0.09 (6.0) 8.6 (6.0) Aluminium Bahrain Bahrain 0.35 (5.4) 136.2 (5.9) Mobile Telecom. Co. Kuwait 0.35 (5.4) 4,301.0 0.0 Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) QSE Top Losers Close* 1D% Vol. ‘000 YTD% Gulf International Services 38.70 (10.0) 91.6 (24.9) Dlala Brokerage & Inv Holding Co. 12.00 (5.1) 469.4 (35.1) Industries Qatar 100.00 (3.9) 188.3 (10.0) Qatar General Ins. & Reins. Co. 51.00 (3.8) 22.7 (0.2) Qatar Islamic Bank 92.50 (3.7) 78.9 (13.3) QSE Top Value Trades Close* 1D% Val. ‘000 YTD% QNB Group 137.80 (0.1) 26,461.0 (3.4) Ooredoo 86.30 0.6 19,551.2 15.1 Industries Qatar 100.00 (3.9) 18,795.2 (10.0) Medicare Group 98.50 1.0 16,974.9 (17.4) Ezdan Holding Group 14.50 (0.6) 16,172.8 (8.8) Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 9,486.71 (1.5) 2.3 0.1 (9.0) 58.31 139,151.5 9.9 1.4 5.1 Dubai 2,975.55 0.2 4.1 (0.7) (5.6) 101.62 80,911.6 9.9 1.1 3.9 Abu Dhabi 4,054.59 (0.8) 3.7 0.0 (5.9) 52.06 113,696.2 11.6 1.3 5.6 Saudi Arabia 5,927.36 0.9 0.8 (1.2) (14.2) 1,522.24 361,244.0 13.6 1.4 4.3 Kuwait 5,118.84 (0.3) 2.2 0.1 (8.8) 35.24 80,353.3 14.6 0.9 4.9 Oman 5,165.51 (0.5) 3.0 (0.3) (4.5) 8.88 21,216.5 8.9 1.1 4.9 Bahrain 1,181.47 (0.7) 0.8 (0.5) (2.8) 1.45 18,574.5 7.7 0.8 5.8 Source: Bloomberg, Qatar Stock Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 9,300 9,400 9,500 9,600 9,700 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 6 Qatar Market Commentary The QSE Index declined 1.5% to close at 9,486.7. The Industrials and Insurance indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari and GCC shareholders. Gulf International Services and Dlala Brokerage & Investments Holding Co. were the top losers, falling 10.0% and 5.1%, respectively. Among the top gainers, Gulf Warehousing Co. gained 5.5%, while Qatar Industrial Manufacturing Co. was up 2.8%. Volume of shares traded on Wednesday fell by 33.9% to 5.9mn from 9.0mn on Tuesday. Further, as compared to the 30-day moving average of 6.8mn, volume for the day was 12.9% lower. Ezdan Holding Group and Dlala Brokerage & Investments Holding Co. were the most active stocks, contributing 18.8% and 7.9% to the total volume, respectively. Source: Qatar Stock Exchange (* as a % of traded value) Earnings Releases, Global Economic Data and Earnings Calendar Earnings Releases Company Market Currency Revenue (mn) 4Q2015 % Change YoY Operating Profit (mn) 4Q2015 % Change YoY Net Profit (mn) 4Q2015 % Change YoY Aramex Dubai AED 1,003.0 4.8% – – 57.6 -35.6% Nakheel* Dubai AED – – – – 4,380.0 19.0% Source: Company data, DFM, ADX, MSM (*FY2015 results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 02/03 US Mortgage Bankers Association MBA Mortgage Applications 29-January -2.60% – 8.80% 02/03 US Automatic Data Processing, Inc ADP Employment Change January 205k 195k 267k 02/03 US Institute for Supply Managemen ISM Non-Manf. Composite January 53.5 55.1 55.8 02/03 EU Eurostat Retail Sales MoM December 0.30% 0.30% 0.00% 02/03 EU Eurostat Retail Sales YoY December 1.40% 1.50% 1.60% 02/03 UK HM Treasury Official Reserves Changes January $527mn – $527mn 02/03 UK Markit Markit/CIPS UK Services PMI January 55.6 55.4 55.5 02/03 UK Markit Markit/CIPS UK Composite PMI January 56.1 55.0 55.3 02/03 UK The British Retail Consortium BRC Shop Price Index YoY January -1.80% – -2.00% 02/03 Spain Markit Markit Spain Services PMI January 54.6 54.3 55.1 02/03 Spain Markit Markit Spain Composite PMI January 55.3 54.4 55.2 02/03 Italy Markit Markit/ADACI Italy Composite PMI January 53.8 – 56.0 02/03 Italy Markit Markit/ADACI Italy Services PMI January 53.6 54.0 55.3 02/03 Italy ISTAT CPI NIC incl. tobacco MoM January -0.20% -0.20% 0.00% 02/03 Italy ISTAT CPI NIC incl. tobacco YoY January 0.30% 0.30% 0.10% 02/03 Italy ISTAT CPI EU Harmonized MoM January -2.20% -2.30% -0.10% 02/03 Italy ISTAT CPI EU Harmonized YoY January 0.40% 0.30% 0.10% 02/03 China Markit Caixin China PMI Services January 52.4 – 50.2 02/03 China Markit Caixin China PMI Composite January 50.1 – 49.4 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Earnings Calendar Tickers Company Name Date of reporting 4Q2015 results No. of days remaining Status IQCD Industries Qatar 4-Feb-16 0 Due QIMD Qatar Industrial Manufacturing Company 7-Feb-16 3 Due MPHC Mesaieed Petrochemical Holding Company 7-Feb-16 3 Due ERES Ezdan Real Estate Company 7-Feb-16 3 Due QGRI Qatar General Insurance & Reinsurance 10-Feb-16 6 Due WDAM Widam Food Company 11-Feb-16 7 Due SIIS Salam International Investment 14-Feb-16 10 Due MCGS Medicare Group 14-Feb-16 10 Due UDCD United Development Company 14-Feb-16 10 Due DBIS Dlala Brokerage & Investment Holding Company 15-Feb-16 11 Due AKHI Al Khaleej Takaful Insurance 15-Feb-16 11 Due Overall Activity Buy %* Sell %* Net (QR) Qatari Individuals 33.93% 30.33% 7,650,517.24 Qatari Institutions 8.97% 23.42% (30,692,372.69) Qatari 42.90% 53.75% (23,041,855.45) GCC Individuals 2.12% 3.33% (2,574,319.52) GCC Institutions 4.07% 2.39% 3,578,986.91 GCC 6.19% 5.72% 1,004,667.39 Non-Qatari Individuals 16.99% 17.05% (109,789.31) Non-Qatari Institutions 33.91% 23.48% 22,146,977.37 Non-Qatari 50.90% 40.53% 22,037,188.06

- 3. Page 3 of 6 AHCS Aamal Company 15-Feb-16 11 Due QGTS Qatar Gas Transport Company (Nakilat) 17-Feb-16 13 Due BRES Barwa Real Estate Company 21-Feb-16 17 Due MCCS Mannai Corp. 24-Feb-16 20 Due ORDS Ooredoo 1-Mar-16 26 Due Source: QSE News Qatar Tajikistan keen on Islamic banking, seeks investment from Qatar – Republic of Tajikistan Minister of Economic Development & Trade Nematullo Hikmatullozoda has said that Tajikistan is keen to benefit from Islamic banking and utilize the experiences of Islamic banks in his country. During his meeting with Qatar International Islamic Bank (QIIK) CEO Abdulbasit Ahmed al-Shaibei, Hikmatullozoda said, “Tajikistan wholeheartedly welcomes investments, especially in the area of Islamic finance.” Hikmatullozoda, who visited QIIK headquarters, lauded the expertise of QIIK in Islamic banking. He expressed the hope that Tajikistan would be able to attract Islamic banks to his country, where his ministry is making efforts to convince investors about the attractive investment opportunities available. In particular, Tajikistan is keen on expanding and further cementing the relationship with Qatar’s financial and business sectors. Al-Shaibei expressed happiness at the visit of Hikmatullozoda to QIIK and said it reflected his interest in examining “the successful Islamic banks closely.” (Gulf-Times.com) Cabinet okays draft law on economic zones in Qatar – HE the Deputy Prime Minister and Minister of State for Cabinet Affairs Ahmed bin Abdullah al-Mahmoud has said that the cabinet has approved a draft law on economic zones. The cabinet meeting was chaired by HE the Prime Minister Sheikh Abdullah bin Nasser bin Khalifa al-Thani. According to the provisions of the bill and based on a proposal from the board of Economic Zones Company, the law regulates the establishment of an economic zone, specifying its area and borders, the establishment of one or more ports attached to it, whether sea, air or land port. All types of companies, sharing contracts or other legal entities can be created or established at the economic zone. These can be owned by a normal or legal person or more than one person – either citizens or others without adhering to regulating laws in this regard. According to the provisions of the law, a project licensed to work at the zone or through it, is exempted from obtaining another license, approval, permission, or registration to carry out that work. A project underway at the zone enjoys unrestricted transfer of capital, revenues or investments out of the country. The Economic Zones Company is to be granted a 50-year concession from the issuance of the law, during which it solely becomes in-charge of the management, development, operation, and maintenance of the zone and zones associated with projects the state assigns to it. (Gulf-Times.com) Doha tops in real estate deals – Ezdan Holding, in its weekly report, has said that the local real estate market has witnessed an increase in the value of deals, but a drop in their number during January 24- 28, 2016 as compared to the previous week. The report revealed that 40 real estate deals were completed during the week throughout the country, as compared to 57 in the previous week, which shows a drop of 29.8%. The overall value of these deals amounted to around QR418.8mn, as compared to QR387.6mn. This was due to an “exceptional single deal” worth QR100mn. The Doha Municipality topped the real estate deals during the period, with some 15 deals representing 52.8% of the overall deals worth QR221.3mn. This was followed by Al Rayyan Municipality and the Umm Salal Municipality with 10 deals each. Completed buildings represented 76.1% of the real estate deals, while vacant plots of land comprised 22.9%. The highest value of the real estate deal during January 24-28 within the Doha Municipality limits amounted to QR62.6mn for a multiple-purpose vacant plot of land of 2,326 square meters (sq m) in Najma. The rate was QR26,900 per sq m. (Gulf-Times.com) QA begins non-stop Doha-Ras Al Khaimah service – Qatar Airways (QA) has started a non-stop service between Doha and Ras Al Khaimah, its fifth destination in the UAE. QA now offers up to 200 weekly flights from Doha to the UAE, including the new four flights to Ras Al Khaimah, – 105 flights a week to the Dubai International Airport; 28 flights a week to Dubai Al Maktoum International Airport; 42 flights a week to Abu Dhabi; and 21 flights a week to Sharjah. (Gulf-Times.com) Al-Sada: Global arbitration key to resolving energy disputes – Highlighting “Qatar’s successful legal domain,” HE the Minister of Energy and Industry Dr. Mohamed bin Saleh al-Sada has underscored the role of international arbitration in resolving disputes in the energy sector. The minister made the statement before members of the judiciary, private sector officials, and participants of the first “International Arbitration Conference on Energy Disputes” held at the Grand Hyatt Hotel. The conference aims to promote arbitration as a flexible and efficient dispute resolution procedure. Al-Sada admitted that price fluctuations in the energy market have affected commercial transactions and “exchanges between consumers, particularly importers and exporters”, but he also emphasized that “arbitration of commercial disputes plays a very important role in assuring security & peace, and in the prevention of conflicts.” Citing the energy sector as “one of the significant drivers of economic growth,” al-Sada said arbitration plays an important role in preventing disputes “to grow out of proportion.” The minister also commended Qatar’s “experienced judges,” whom, he said, have contributed to Qatar’s “reputable image” and to its “independent and transparent judiciary.” (Gulf-Times.com) Mesaieed solid waste management centre being expanded – A top official at Ministry of Municipality and Environment (MME) said around 3,000 tons of solid domestic waste is collected and disposed of daily across Qatar. Director of General of cleanliness project and mechanical equipment, Safar Mubarak al-Shafi said the figure did not include construction and hazardous waste collected from different industrial and construction locations. According to the official, workers deployed by the ministry also handle street cleaning and transfer of waste to dumping stations, from where it is transported to the domestic solid waste management centre in Mesaieed. “It is the only facility of its kind in the Middle East,” said Al-Shafi, and added the waste management centre has the facility and capacity to recycle green waste and organic materials up to 750 tons a day. However, the centre, which is handling 500 tons daily, will be able to treat more when the ongoing phase of expansion is completed. (Gulf-Times.com) International Trans-Pacific Partnership trade deal signed, but years of negotiations still to come – The Trans-Pacific Partnership (TPP), one of the world's biggest multinational trade deals, was signed by 12 member nations in New Zealand, but the massive trade pact

- 4. Page 4 of 6 will still require years of tough negotiations before it becomes a reality. The TPP, a deal which will cover 40% of the world economy, has already taken five years of negotiations to reach the signing stage. New Zealand Prime Minister John Key said the signing is "an important step" but the agreement "is still just a piece of paper, or rather over 16,000 pieces of paper until it actually comes into force". The TPP will now undergo a two-year ratification period in which at least six countries - that account for 85% of the combined GDP of the 12 TPP nations - must approve the final text for the deal to be implemented. The 12 nations include Australia, Brunei, Canada, Chile, Japan, Malaysia, Mexico, New Zealand, Peru, Singapore, the US and Vietnam. (Reuters) US services sector cooling; jobs market resilient – Activity in the vast US services sector slowed to a near two-year low in January, suggesting that economic growth weakened further at the start of the first quarter even as the labor market remains resilient. The economy has been undermined by a strong dollar, softening global demand and an inventory destocking, which have pressured manufacturing and export industries. Spending cuts by energy firms, reeling from a collapse in oil prices, have also dragged on growth. Until recently, services sector strength had offered hope that the economy would weather both the domestic and global headwinds, which held GDP growth to a 0.7% annual rate in 4Q2015. Meanwhile, the Institute for Supply Management (ISM) said its index of non-manufacturing activity fell to 53.5 from 55.8 the month before. The reading was below Reuters expectations of 55.1. The business activity index fell to 53.9 from 59.5 the month before. That was below expectations of 58.5. The employment index fell to 52.1 from 56.3 a month earlier. New orders dropped to 56.5 from 58.9. The prices paid index fell to 46.4 from 51.0. According to an earlier ISM report the US economy's manufacturing sector contracted in January but was slightly improved from December. (Reuters) US Treasury Secretary urges China to communicate FX policy clearly – US Treasury Secretary Jack Lew reiterated to China the importance of transitioning to a market-determined exchange rate in an orderly and transparent way. The Treasury said in a statement that during a phone call with Chinese Vice Premier Wang Yang, Lew also urged Beijing to clearly communicate its exchange rate policies and actions to financial markets. The Chinese official Xinhua news agency reported, Wang said in the call that China remained capable of keeping the exchange rate of China's currency, the renminbi, "basically stable at a reasonable and balanced level". Xinhua added Wang and Lew also discussed how to push forward a bilateral investment treaty, under discussion for much of 2015, to help improve business ties between the two countries. (Reuters) Eurozone sales rebounds in December driven by Christmas shopping – The European Union statistics office Eurostat estimated that Eurozone retail trade increased in December mostly thanks to Christmas shopping of food, drinks and tobacco. Sales in the 19 countries sharing the euro grew on average 0.3% in December on a monthly basis, as expected by economists polled by Reuters. Retail trade increased 1.4% YoY, slightly less than the forecast 1.5%. Eurostat revised upwards both monthly and yearly estimates for the month of November. On a MoM basis, Eurozone sales have been flat in November, contrary to previous estimates of a 0.3% drop. YoY sales recorded in November a 1.6% rise, more than the previously estimated 1.4%. In December, sales increased mostly for food, drinks and tobacco products, which recorded a 0.6% monthly rise. (Reuters) China targets 6.5-7% growth – National Development and Reform Commission (NDRC) Chairman Xu Shaoshi said China has set its economic growth projection range at 6.5 to 7% in 2016, but efforts to curb overcapacity is expected to raise unemployment in some provinces. Xu Shaoshi said downward pressure on the world's second-largest economy would remain in 2016. China's investments were now focused on fixing weak points and structural adjustments, including infrastructure in the central and western regions, education and healthcare sectors. Xu also said that China's basic infrastructure investment growth increased 15% in 2015. Xu further added that China will be affected by the unstable global economic conditions in 2016 but will have the ability to cope with the challenges. The official Purchasing Managers' Index (PMI) for manufacturing stood at 49.4 in January, the lowest reading since August 2012. (Reuters) Regional Barclays to restructure its Middle East corporate banking business – According to sources, Barclays Plc will lay off around 150 staff in Dubai as it restructures its Middle East corporate banking business. The bank will also close its offices at Emaar Square and relocate bankers and support staff to its office at the Dubai International Financial Centre. It would retain its corporate branch in Abu Dhabi and wholesale banking license with the UAE Central Bank. Barclays CEO Jes Staley said the company is planning to cut 1,200 jobs worldwide and shut securities operations across Asia. (Bloomberg) Terrapinn Middle East: Railway projects worth $352bn underway in the MENA region – According to Terrapinn Middle East, the Middle Eastern and North African (MENA) countries are forging ahead with plans to establish a strong passenger and freight transport network, with 16 major railway projects worth $352bn currently underway in the region. According to ICAEW Economic Insight Middle East report, Kuwait, Saudi Arabia, the UAE and Oman are likely to net the biggest windfalls, with logistics forecast to contribute 13.6%, 12.1%, 11.7% and 11.7%, to their respective economies by 2018. (GulfBase.com) Saudi Aramco not to cut upstream investment – Saudi Arabian Oil Company (Saudi Aramco) Senior Vice President Ahmed Al-Sa’adi has said that the company will not cut its upstream investment despite the collapse in oil price. (GulfBase.com) NCB: KSA budget allocations to SCIs moderated significantly – National Commercial Bank (NCB), in its latest monthly Saudi Economic Review report, has said that the Saudi Arabian government’s 2016 budget allocations to specialized credit institutions (SCIs) have moderated significantly, yet their continuation reflects support for the economy. According to the budget announcement, SR49.9bn will be allocated to SCIs, namely the Public Investment Fund (PIF), Saudi Industrial Development fund (SIDF), Saudi Credit & Saving Bank (SCSB) and the Real Estate Development Fund (REDF). The latest data released by the NCB reflect the central role played by SCIs as a catalyst in the domestic economy. As expected, the REDF was the largest among these institutions in terms of the outstanding loans that registered SR141.bn. NCB believes that this figure might have crossed the SR150bn threshold as would be shown in the coming data releases. It is not a surprise that REDF will maintain its status as the largest lender among SCIs with the government trying to mitigate the housing market imbalances, especially on the demand side. The PIF and SCSB had also maintained the second and third ranks given their participation in project finance across different sectors that enhance the Kingdom’s absorptive capacity, with the outstanding loans to both standing at SR96.4bn and SR44.4bn, respectively. The collapse in oil prices has been a focal point for the global economy, leading to an oversupply theme that coincided with waning demand, expected to stretch into 2016. (GulfBase.com) Jadwa Investment: KSA fiscal reserves slide to 4-year low on weak oil – Jadwa Investment, in its economic report, has said that Saudi

- 5. Page 5 of 6 Arabia’s fiscal reserves dropped to a four-year low in 2015 as the government sought to finance a budget deficit caused by plunging oil revenues. The reserves of the world’s largest crude exporter dropped to $611.9bn by 2015-end, down from $732bn a year before. Jadwa said it expected reserves to fall to around $500bn by 2016-end, after oil prices fell by three quarters since mid-2014. To help finance the budget deficit, the Kingdom, in December, introduced a series of austerity measures raising fuel prices by up to 80% and increasing the prices of electricity, water, natural gas etc. Jadwa expects inflation to soar in 2016 to 3.9% from 2.2% in 2015, as a result of the price hikes. (GulfBase.com) J.P. Morgan Saudi Arabia joins Tadawul as member – The Saudi Stock Exchange (Tadawul) has announced that J.P. Morgan Saudi Arabia Limited Company has fulfilled all technical and legal requirements needed to be recognized as Tadawul member. (Tadawul) Saudi CMA approves public offering of Jadwa Saudi IPO Fund – The Saudi Capital Market Authority’s (CMA) board of commissioners issued its resolution approving the public offer made by Jadwa Investment Company of Jadwa Saudi IPO Fund. (Tadawul) Bank AlJazira updates on sale of land – Bank Al Jazira has made an announcement regarding the signing of a MoU with Mr. Fahad Bin Abdul Rahman Bin Sulaiman Al Thunayan to sell the land located in Al Jubail Province - Eastern Region at a total value of SR217.56mn. The bank said that the title deed was discharged through the competent Notary Public, thereby attaining a capital gain of SR208.56mn, while the book value of the land was SR9mn. This capital gain will appear in the 1Q2016 financial statements. (Tadawul) Emirates NBD: KSA non-oil growth slows to record low – Emirates NBD, in its research note, has stated that the Emirates NBD UAE Purchasing Managers’ Index (PMI) showed a loss in growth momentum in January 2016, slipping to 52.7, a 46-month low. The decline points to the weakest improvement in business conditions since March 2012. While the PMI was still above the neutral 50.0 level that separates expansion from contraction, the data points to slow growth in the UAE non-oil private sector in January 2016, in line with the trend seen in 4Q2015. However, Emirates NBD expects the non-oil sectors to contribute positively to overall growth in the UAE in 2016. Meanwhile, a measure of growth in Saudi Arabia’s non-oil economy fell to a record low as cheap crude weighs on the world’s largest oil exporter. The Emirates NBD PMI for Saudi Arabia dropped to 53.9 in January 2016, the lowest in the six-and-a- half year history of the survey, driven by slower expansion in new business. (Bloomberg) RAK TDA: Ras Al Khaimah tourism revenue up 12.4% YoY in 2015 – The Ras Al Khaimah Tourism Development Authority (RAK TDA) said that Ras Al Khaimah’s tourism revenue rose 12.4% YoY in 2015 over 2014, the highest increase in five years. The growth in revenue was driven by a 6% YoY increase in the number of visitors to 740,383 in 2015. Hotel occupancy in the Emirate grew 9.7% to 64.7% in 2015. Average daily rate and food & beverage revenues rose 7% and 14.4%, respectively, during the same period. Revenue per available room (RevPAR) increased 10% YoY to AED355.93 in 2015, while hotel room revenue was up 12.1%. (GulfBase.com) Gulf Finance: UAE SMEs struggling to get paid or secure loans as confidence slides – According to a survey conducted by Gulf Finance, Small and medium-sized enterprises (SMEs) in the UAE struggled to get loans after confidence slipped to a new low in 4Q2015, when the fall in the price of oil was most fierce. As a result, these businesses, typically the lifeblood of an economy, reported in the survey that they are finding it more difficult to secure financing and to get paid. They are also suspending plans for expansion and have stopped hiring. Small businesses and individuals have been shying away from borrowing in recent quarters and banks have also become more reluctant to lend at a time when bank deposits are dwindling amid low government revenues from the sale of crude oil. (GulfBase.com) RAKBAK reports AED1.4bn net profit in 2015, recommends 50% cash dividend – The National Bank of Ras Al Khaimah (RAKBAK) reported net profit of AED1.4bn in 2015 as compared to AED1.45bn in 2015. Net operating profit reached AED2.46bn in 2015 as compared to AED2.05bn in 2014. RAKBAK recorded revenues of AED3.93bn in 2015 as compared to AED3.55bn in 2014. The bank’s total assets stood at AED40.55bn at the end of December 31, 2015 as compared to AED34.83bn in the year-ago period. Gross customer’s loans grew 10.6% to reach AED28.5bn, while customer deposits were up 12.9% to stand at AED27.8bn. Meanwhile, the bank’s board of directors (BoD) has recommended 50% cash dividend. This recommendation is subject to approval of the Central Bank of the UAE and shareholders. (ADX) CBO issues bonds worth OMR100mn – Central Bank of Oman (CBO) has announced the new issue of government development bonds (GDB). The size of the new issue is fixed at OMR100mn with a maturity period of five years and will carry a coupon rate of 3.5% per annum. The issue will be open for subscription from February 7 to February 14, 2016, while the auction will be held on February 16, 2016. The issue settlement date will be February 22, 2016. Interest on the new bonds will be paid semiannually on August 22 and February 22 every year until the maturity date, February 22, 2021. Investors may apply for these bonds through the competitive bidding process only. Investors may submit bids through commercial licensed banks operating in Oman. Investors with applications of OMR1mn and above can submit their bids directly to CBO after getting them endorsed from their banks. The bonds are direct and unconditional obligations of the government of Oman. They can be used as collateral to obtain loans from any local commercial licensed bank. The bonds can also be traded at prevailing market rates through the Muscat Securities Market (MSM). GulfBase.com) Oman seeks consultant to forecast power demand – Oman floated a tender on Tuesday, seeking proposals from international consultants to provide technical advisory services for competitive tendering to secure an economic expansion of power capacity to meet future demand in 2021 and beyond. The consultant is expected to advice the Oman Power and Water Procurement Company (OPWP) on how to expand capacity within the main interconnected area (MIS), which serves over 736,000 electricity customers. This procurement will be by using the current established process and contract structure. OPWP, a member of Electricity Holding Company, is responsible for procuring new electricity generation capacity and water in Oman. (GulfBase.com) GCC to invest around $900bn in 1,600 new projects over next decade – Central Bank of Bahrain (CBB) Executive Director of financial institutions supervision Abdul Rahman Al Baker has said that a surge in insurance activity with a growth in gross premiums is expected to unfold across the GCC over the next 5-10 years. He said the sector’s growth will continue to be supported by increasing investment in the GCC in construction, infrastructure and petroleum industry-related projects. He added that the GCC is set to invest around $900bn in almost 1,600 new projects over the next decade. (GulfBase.com)

- 6. Contacts Saugata Sarkar Shahan Keushgerian Zaid al-Nafoosi, CMT, CFTe Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6509 Tel: (+974) 4476 6535 saugata.sarkar@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa zaid.alnafoosi@qnbfs.com.qa ` QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar Disclaimer and Copyright Notice: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of QNB SAQ (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange QNB SAQ is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. QNBFS accepts no liability whatsoever for any direct or indirect losses arising from use of this report. Any investment decision should depend on the individual circumstances of the investor and be based on specifically engaged investment advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. For reports dealing with Technical Analysis, expressed opinions and/or recommendations may be different or contrary to the opinions/recommendations of QNBFS Fundamental Research as a result of depending solely on the historical technical data (price and volume). QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. This report may not be reproduced in whole or in part without permission from QNBFS COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg (*$ adjusted returns) 80.0 100.0 120.0 140.0 160.0 180.0 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 QSEIndex S&P Pan Ar ab S&P GCC 0.9% (1.5%) (0.3%) (0.7%) (0.5%) (0.8%) 0.2% (2.4%) (1.6%) (0.8%) 0.0% 0.8% 1.6% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D%* WTD%* YTD%* Gold/Ounce 1,142.65 1.2 2.2 7.7 MSCI World Index 1,540.87 0.1 (1.4) (7.3) Silver/Ounce 14.69 2.7 3.0 6.0 DJ Industrial 16,336.66 1.1 (0.8) (6.2) Crude Oil (Brent)/Barrel (FM Future) 35.04 7.1 0.9 (6.0) S&P 500 1,912.53 0.5 (1.4) (6.4) Crude Oil (WTI)/Barrel (FM Future) 32.28 8.0 (4.0) (12.9) NASDAQ 100 4,504.24 (0.3) (2.4) (10.0) Natural Gas (Henry Hub)/MMBtu 2.06 1.2 (8.6) (11.0) STOXX 600 329.43 (0.1) (1.8) (8.3) LPG Propane (Arab Gulf)/Ton 36.00 6.3 0.7 (8.0) DAX 9,434.82 (0.1) (1.7) (10.9) LPG Butane (Arab Gulf)/Ton 53.00 5.0 (1.9) (7.8) FTSE 100 5,837.14 (0.3) (1.7) (7.5) Euro 1.11 1.7 2.5 2.2 CAC 40 4,226.96 0.1 (2.3) (7.2) Yen 117.90 (1.7) (2.7) (1.9) Nikkei 17,191.25 (1.2) 0.8 (7.5) GBP 1.46 1.3 2.5 (0.9) MSCI EM 721.65 (1.0) (2.8) (9.1) CHF 1.00 1.4 1.9 (0.2) SHANGHAI SE Composite 2,739.25 (0.4) 0.0 (23.6) AUD 0.72 1.8 1.2 (1.6) HANG SENG 18,991.59 (2.3) (3.7) (13.9) USD Index 97.29 (1.6) (2.3) (1.4) BSE SENSEX 24,223.32 (1.2) (2.6) (9.5) RUB 76.80 (3.8) 1.7 5.9 Bovespa 39,588.82 4.5 (0.1) (7.9) BRL 0.26 2.4 2.7 1.7 RTS 696.96 (0.6) (6.5) (7.9) 108.1 93.0 92.6