McKinsey Survey: Polish consumer sentiment during the coronavirus crisis

•

3 gostaram•5,646 visualizações

The prevailing sentiment among Polish consumers is similar to those in other European countries, with uncertainty about health and the economy as the biggest concerns. With over half of Poles expecting their income to decrease, we observe a sharp decline in consumers’ intentions to purchase discretionary products, especially in-store. It is also important to note that the majority of Poles expect their finances and personal routines to be impacted for more than four months. These exhibits are based on survey data collected in Poland from April 2–5, 2020. Check back for regular updates on Polish consumer sentiments, behaviors, income, spending, and expectations.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a McKinsey Survey: Polish consumer sentiment during the coronavirus crisis

Semelhante a McKinsey Survey: Polish consumer sentiment during the coronavirus crisis (19)

Mais de McKinsey on Marketing & Sales

Mais de McKinsey on Marketing & Sales (20)

Último

Último (20)

McKinsey Survey: Polish consumer sentiment during the coronavirus crisis

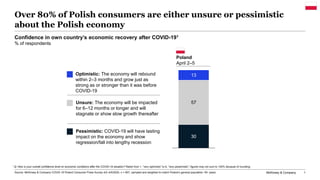

- 1. McKinsey & Company 1 Over 80% of Polish consumers are either unsure or pessimistic about the Polish economy 30 57 13 Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years April 2–5 Poland Unsure: The economy will be impacted for 6–12 months or longer and will stagnate or show slow growth thereafter Pessimistic: COVID-19 will have lasting impact on the economy and show regression/fall into lengthy recession Optimistic: The economy will rebound within 2–3 months and grow just as strong as or stronger than it was before COVID-19 Confidence in own country’s economic recovery after COVID-191 % of respondents 1 Q: How is your overall confidence level on economic conditions after the COVID-19 situation? Rated from 1, “very optimistic” to 6, “very pessimistic”; figures may not sum to 100% because of rounding.

- 2. McKinsey & Company 2 More than half of Poles are being careful about how they spend their money 43% 21% 23% 14% 7% 44% 48% 45% 54% 49% 43% 41% 13% 31% 31% 32% 47% 50% 53% 4% 6% Strongly disagree / disagree Somewhat disagree / agree Strongly agree / agree My family/friends’ health has been negatively affected by coronavirus or COVID-19 My ability to make financial ends meet has been negatively impacted by the coronavirus or COVID-19 My ability to work has been reduced by the coronavirus or COVID-19 Uncertainty about the economy is preventing me from making purchases or investments that I would otherwise make I am cutting back on my spending Given the economy and my personal finances, I have to be very careful how I spend my money My income has been negatively impacted by the coronavirus or COVID-19 Overall sentiment in the general population in Poland1 % of respondents Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years 1 Q: Please indicate how strongly you agree or disagree with each of the following statements. Please select only one response for each statement. Figures may not sum to 100% because of rounding.

- 3. McKinsey & Company 3 Reduce slightly / reduce a lot About the same Increase slightly / increase a lot 2% 51% 40% 57% Past 2 weeks 4% Next 2 weeks 44% Though most Poles expect their income and savings to decrease in the next two weeks, one third expect to increase spending 31%34% 40%37% 29% 29% Past 2 weeks Next 2 weeks Household income1,2 % of respondents Household spending1,2 % of respondents Household savings1,2 % of respondents 58% 5%5% 50% 45% Next 2 weeks 37% Past 2 weeks April 2–5 April 2–5 April 2–5 Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years 1 Q: How has the COVID-19 situation affected your (family’s) overall available income, spending, and savings in the past two weeks? Figures may not sum to 100% because of rounding. 2 Q: How do you think your overall available income, spending, and savings may change in the next two weeks? Figures may not sum to 100% because of rounding.

- 4. McKinsey & Company 4 Spending expectations have declined across categories, though Poles expect to spend more on personal care products 13 46 32 52 48 80 87 61 64 80 79 20 15 9 51 71 27 9 15 5 9 20 26 Groceries 2 Snacks 4Tobacco products 4 Food takeout & delivery Restaurant Quick-service restaurant Non-food child products Alcohol Skin care & makeup 2 3Footwear 2Apparel Household supplies 2Jewelry Accessories Personal-care products 3 2Furnishing & appliances Decrease Stay the same Increase 17 43 66 91 43 81 82 55 76 86 74 88 89 90 86 29 9 5 Out-of-home entertainment Entertainment at home Books/magazines/newspapers 1 2 2Consumer electronics Personal-care services Fitness & wellness Petcare services 1 1 Gasoline Vehicle purchases 1Short-term home rentals 3Travel by car 2Adventures & tours 1International flights 2Hotel/resort stays 2Domestic flights Net intent2 +12 -34 -64 -91 -42 -79 -81 -50 -75 -85 -71 -86 -88 -88 -84 Net intent2 +14 -11 +5 -69 -35 -28 -37 -43 -76 -85 -58 -62 -78 -77 +17 -48 Expected spending per category over the next 2 weeks compared to usual1 % of respondents NA3 Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years 1 Q: Over the next two weeks, do you expect that you will spend more, about the same, or less money on these categories than usual? Figures may not sum to 100% because of rounding. 2 Net intent is calculated by subtracting the % of respondents stating they expect to decrease spending from the % of respondents stating they expect to increase spending.

- 5. McKinsey & Company 5 Consumers expect to shift to online shopping for household & child essentials, personal care, groceries, and entertainment at home -45 -70 15 20 -60 -30 -50 -35-40 -25 -20 -40 -15 -10 -5 -30 0 -20 -10 0 255 10 10 Alcohol Accessories Tobacco Non-food child products (e.g., diapers) Consumer electronics Books/ magazines/ newspapers Footwear Snacks Groceries Household supplies (e.g., cleaning, laundry) Food takeout & deliveryFurnishing & appliances Personal-care products (e.g., soap, shampoo) Skincare & makeup Fitness & wellness Apparel Jewelry Entertainment at home (e.g., Netflix) Household essentials Discretionary Entertainment at home In-store Online Expected change in shopping channel per category over the next 2 weeks1 Axes show net intent,2 bubble size is relative to share of respondents that have purchased category in last 6 months Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years 1 Q: And where do you expect you’ll buy these categories? Tell us if you will shop in the following places more, about the same, or less in the next two weeks; please note, if you don’t buy in one of these places today and won’t in next two weeks, please select “N/A”; did not ask this question for categories not shown. 2 Net intent is calculated by subtracting the % of respondents stating they expect to decrease shopping frequency from the % of respondents stating they expect to increase shopping frequency.

- 6. McKinsey & Company 6 Poles expect to spend more time consuming news, video content, and social media 7% 9% 11% 8% 14% 8% 20% 24% 30% 36% 45% 42% 42% 47% 52% 52% 59% 52% 49% 56% 53% 52% 52% 48% 42% 39% 34% 33% 28% 27% 14% 12% Reading news online Live news Movies or shows Social media Texting, chatting, messaging Video content TV Reading for personal interest Video games Working Reading print news 3% Stay the sameDecrease Increase Net intent2 +49 +45 +39 +31 +31 +20 +25 +8 +3 +37 +34 +33 +30 +26 +25 +14 -1 -16 -24 -18 -25 1 Q: Over the next two weeks, how much time do you expect to spend on these activities compared to how much time you normally spend on them? Figures may not sum to 100% because of rounding. 2 Net intent is calculated by subtracting the % of respondents stating they expect to decrease time spent from the % of respondents stating they expect to increase time spent. Expected change to time allocation over the next 2 weeks1 % of respondents -1 Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland ‘s general population 18+ years

- 7. McKinsey & Company 7 Poles increasingly believe that the personal and financial impacts of COVID-19 will last well beyond two months 4% 9% 46% More than one year 34% 7% 0 – 1 month 2 – 3 months 4 – 6 months 7 – 12 months 12% 27% 29% 14% 16%More than one year No impact 7 – 12 months 0 – 1 month 2 – 3 months 4 – 6 months 3% Adjustments to routines1 % of respondents Impact to personal / household finances2 % of respondents ~96% believe it will take 2+ months before routines can return to normal ~85% believe their finances will be impacted for 2+ months by the COVID-19 situation Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years 1 Q: How long do you believe you will need to adjust your routines, given the current COVID-19 situation, before things return back to normal in Poland (e.g., government lifts restrictions on events/travel)? Figures may not sum to 100% because of rounding. 2 Q: How long do you believe your personal/household finances will be impacted by the COVID-19 situation? Figures may not sum to 100% because of rounding.

- 8. McKinsey & Company 8 Uncertainty about family health and safety, the duration of the situation, and the economy are top concerns for Poles 84% 82% 81% 80% 74% 72% 72% 69% 66% 53% 48% 44% 37% Contributing to spread of virus Impact on upcoming events Health of my relatives that are in vulnerable populations The Polish economy Safety of me or my family Not knowing how long it will last Overall public health My personal health Taking care of my family Negative impact on my job or income Not being able to make ends meet Not being able to get the supplies I need Impact on upcoming travel plans 1 Q: What concerns you most about the coronavirus or COVID-19 situation? (not a concern; minimally concerned; somewhat concerned; very concerned; extremely concerned) Very concerned / extremely concerned 84% of Poles are very/extremely concerned about the health of vulnerable relatives during COVID-19 Largest concerns of the Polish population related to COVID-191 % of respondents who are very concerned or extremely concerned Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years

- 9. McKinsey & Company 9 Polish consumers have adopted new digital activities since the start of COVID-19, including remote learning, VC, and telemedicine 15% 7% 10% 2% 3% 2% 7% 7% 14% 3% 5% 6% 1% 14% 16% 2% 25% 9% 6% 6% 10% 10% 27% 5% 4% 8% 3% 4% 2% 5% 5% 5% 9% 15% 1% 4% 3% 1% 3% 2% 5% 78% 96% 1% Restaurant delivery Remote learning for my children 82% 83% 68% Video conferencing for professional use Virtual/video chat for personal use 1% 72%Grocery delivery 1%Meal-kit delivery Remote learning for me 82%Playing online video games 82%Watching online video gaming 55% Telemedicine for physical health 60% Wellness app (e.g., meditation) 90% 95% 90% 83% 95% Telemedicine for mental health TikTok 1% 89% 1% 1% Digital workout bike or machine Online personal training/fitness Online media streaming 2% Source: McKinsey & Company COVID-19 Poland Consumer Pulse Survey 4/2–4/5/2020, n = 607, sampled and weighted to match Poland’s general population 18+ years Have you used or done any of the following since COVID-19 started?1 % of respondents 1 Q: Have you used or done any of the following since the COVID-19 situation started? If yes, Q: Which best describes when you have done or used each of these items? Possible answers: “just started using since COVID-19 started”; “using more since COVID-19 started”; “using about the same since COVID-19 started”; “using less since COVID-19 started.” Just started usingNot using Using less/the same Using more

- 10. McKinsey & Company 10 Disclaimer McKinsey does not provide legal, medical or other regulated advice or guarantee results. These materials reflect general insight and best practice based on information currently available and do not contain all of the information needed to determine a future course of action. Such information has not been generated or independently verified by McKinsey and is inherently uncertain and subject to change. McKinsey has no obligation to update these materials and makes no representation or warranty and expressly disclaims any liability with respect thereto.