Crowdinvest : All About Crowdfunding in UK

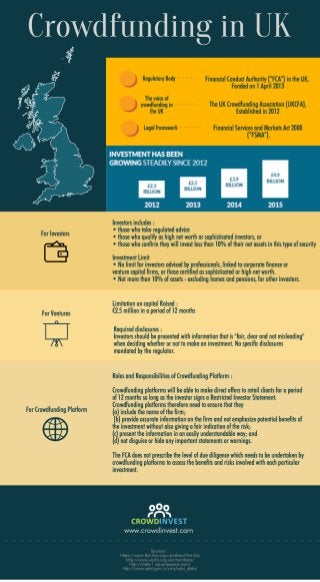

All About Crowdfunding in UK - Regulatory Body - Financial Conduct Authority (“FCA”) in the UK, Fonded on 1 April 2013 The voice of crowdfunding in the UK - The UK Crowdfunding Association (UKCFA), Established in 2012 Legal framework - Financial Services and Markets Act 2000 (“FSMA”). For Investors - Investors includes : • those who take regulated advice • those who qualify as high net worth or sophisticated investors, or • those who confirm they will invest less than 10% of their net assets in this type of security Investment Limit • No limit for investors advised by professionals, linked to corporate finance or venture capital firms, or those certified as sophisticated or high net worth. • Not more than 10% of assets - excluding homes and pensions, for other investors. For Ventures - Limitation on capital Raised : €2.5 million in a period of 12 months Required disclosures : Investors should be presented with information that is "fair, clear and not misleading" when deciding whether or not to make an investment. No specific disclosures mandated by the regulator. For Crowdfunding Platform - Roles and Responsibilities of Crowdfunding Platform : Crowdfunding platforms will be able to make direct offers to retail clients for a period of 12 months so long as the investor signs a Restricted Investor Statement. Crowdfunding platforms therefore need to ensure that they (a) include the name of the firm; (b) provide accurate information on the firm and not emphasize potential benefits of the investment without also giving a fair indication of the risk; (c) present the information in an easily understandable way; and (d) not disguise or hide any important statements or warnings. The FCA does not prescribe the level of due diligence which needs to be undertaken by crowdfunding platforms to assess the benefits and risks involved with each particular investment.