Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

Semelhante a Ias 38 case studies 3 nos

Mais de Hyderabad Chapter of ICWAI

Mais de Hyderabad Chapter of ICWAI (13)

Último

Último (20)

Ias 38 case studies 3 nos

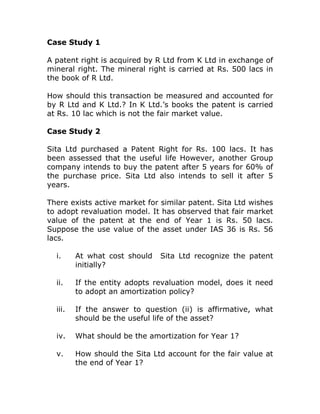

- 1. Case Study 1 A patent right is acquired by R Ltd from K Ltd in exchange of mineral right. The mineral right is carried at Rs. 500 lacs in the book of R Ltd. How should this transaction be measured and accounted for by R Ltd and K Ltd.? In K Ltd.’s books the patent is carried at Rs. 10 lac which is not the fair market value. Case Study 2 Sita Ltd purchased a Patent Right for Rs. 100 lacs. It has been assessed that the useful life However, another Group company intends to buy the patent after 5 years for 60% of the purchase price. Sita Ltd also intends to sell it after 5 years. There exists active market for similar patent. Sita Ltd wishes to adopt revaluation model. It has observed that fair market value of the patent at the end of Year 1 is Rs. 50 lacs. Suppose the use value of the asset under IAS 36 is Rs. 56 lacs. i. At what cost should Sita Ltd recognize the patent initially? ii. If the entity adopts revaluation model, does it need to adopt an amortization policy? iii. If the answer to question (ii) is affirmative, what should be the useful life of the asset? iv. What should be the amortization for Year 1? v. How should the Sita Ltd account for the fair value at the end of Year 1?

- 2. Case Study 3 Ramanuja Ltd is developing production process. During 2007, expenditure incurred was Rs.100 million, of which Rs. 70 million was incurred before 1 December 2007 and balance Rs.30 million was incurred between 1 December 2007 and 31 December 2007. The company demonstrated on 1 December 2007 that the production process met the criteria for recognition as an intangible asset in accordance with Para 57, IAS 38. The recoverable amount of know-how embodied in the process ( including future cash flows to complete the process before it is available for use) is estimated at Rs. 34 million. During 2008, Ramanuja Ltd incurred further expenditure of Rs.50 million. At the end of 2008, the recoverable amount of know-how embodied in the process ( including future cash flows to complete the process before it is available for use) is estimated at Rs.70 million. 1. What should be recognized as Intangible Asset? 2. How much should be expensed off? 3. What is the impairment Loss?