Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (14)

Destaque

Semelhante a T-MobileValuation

Semelhante a T-MobileValuation (20)

T-MobileValuation

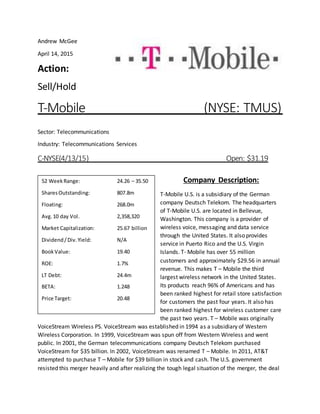

- 1. Andrew McGee April 14, 2015 Action: Sell/Hold T-Mobile (NYSE: TMUS) Sector: Telecommunications Industry: Telecommunications Services C-NYSE(4/13/15) Open: $31.19 Company Description: T-Mobile U.S. is a subsidiary of the German company Deutsch Telekom. The headquarters of T-Mobile U.S. are located in Bellevue, Washington. This company is a provider of wireless voice, messaging and data service through the United States. It also provides service in Puerto Rico and the U.S. Virgin Islands. T- Mobile has over 55 million customers and approximately $29.56 in annual revenue. This makes T – Mobile the third largest wireless network in the United States. Its products reach 96% of Americans and has been ranked highest for retail store satisfaction for customers the past four years. It also has been ranked highest for wireless customer care the past two years. T – Mobile was originally VoiceStream Wireless PS. VoiceStream was established in 1994 as a subsidiary of Western Wireless Corporation. In 1999, VoiceStream was spun off from Western Wireless and went public. In 2001, the German telecommunications company Deutsch Telekom purchased VoiceStream for $35 billion. In 2002, VoiceStream was renamed T – Mobile. In 2011, AT&T attempted to purchase T – Mobile for $39 billion in stock and cash. The U.S. government resisted this merger heavily and after realizing the tough legal situation of the merger, the deal 52 WeekRange: 24.26 – 35.50 SharesOutstanding: 807.8m Floating: 268.0m Avg.10 day Vol. 2,358,320 Market Capitalization: 25.67 billion Dividend/Div.Yield: N/A BookValue: 19.40 ROE: 1.7% LT Debt: 24.4m BETA: 1.248 Price Target: 20.48

- 2. fell through. In 2012, T – Mobile merged with MetroPCS, which was the 6th largest carrier in the United States. This deal increased T – Mobile competitiveness with its competitors. After the merger, the company was renamed T – Mobile US, Inc. In 2013, Sprint began to make a push to take a majority share holder stake in T – Mobile of about $20 billion. This move would be beneficial to T – Mobile because it would drastically increase its market share. Sprint eventually withdrew from the attempted merger for fear that the government would not approve it. There was a lot of anti-trust concern involving this merger. Products: T – Mobile has multiple phone plans and services they provide. T – Mobile focuses on trying to get customer away from the major providers like Verizon and AT&T. In an attempt to do this T – Mobile does a lot of lower prices and deals to help get people out of their long term contracts with other providers. Some examples are: Uncarrier This deal does not require a contract, drops overage fees for data usage and covers any early termination fees. Simple Choice This deal offers unlimited calling and text messagine with 500 mb of data usage for $50 a month. Early Termination Fees T – Mobile is willing to pay off a customer’s early termination fees up to $375 per line when the customer turns in a current device. Test Runs: T – Mobile also tries to get new customers by providing free test runs. In June, 2014 T – Mobile was offering customers a free IPhone 5s to test out T – Mobile’s network for one week. The offer was limited to one per house hold per year. Apple even provided T – Mobile with free IPhones for this promotion. Gogo Inflight Wifi: Enables customers to send text messages and visual voicemails on Gogo equipped U.S. flights. Data Stash: T – Mobile customers have the ability to roll over unused high speed data for up to a year.

- 3. Competitive Analysis: T-Mobile is considered one of the four major wireless providers in the United States. Its major competitors are Verizon, AT&T and Sprint. T-Mobile is trying to gain market share against these major competitors by offering low prices for their services, paying off termination fees and high demand products. T-Mobile recently started offering high demand products such as the Iphone 6 & 6+ ad the Samsung Galaxy, along with other high demand smart phones. This will cause people to consider T-Mobile when they are choosing a provider or switching providers. T- Mobile likes to try to take customers away from the other three major providers. AT&T is one customer base it targets specifically because about 20% of AT&T customers do not have contracts. Revenue Growth: For the past 6 years, T-Mobile has demonstrated consistent growth in its revenue. From 2008 through 2011, it had consistent revenue growth of approximately 20%. In 2012, the growth slowed to about 5%. This may have been cause by the merger with MetroPCS and finalizing the transition. After the merger with MetroPCS, the revenue jumped up a large amount. In 2012, the revenue was $5,000. In 2013, after the merger the revenue was $24,000. This is clearly more because of the merger instead of a massive increase in sales. However, in 2014 there was still consistent growth of 21%. Analysts are anticipating growth to slow down in the next couple of years though. In 2015 growth is expected to slow to 9% and in 6% in 2016. In Millions of USD except Per Share FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 12 Months Ending 2008-12- 31 2009-12- 31 2010-12- 31 2011-12- 31 2012-12- 31 2013-12- 31 2014-12- 31 Revenue 2,751.5 3,480.5 4,069.4 4,847.4 5,101.3 24,420.0 29,564.0 Growth (YOY) 26.5% 16.9% 19.1% 5.2% 378.7% 21.1%

- 4. Earnings: Ann Date Per Per End C Reported Comp Estimate 02/19/2015 Q4 14 12/14 0.198 0.12 0.073 10/27/2014 Q3 14 09/14 -0.051 -0.12 0.035 07/31/2014 Q2 14 06/14 0.498 0.48 0.093 05/01/2014 Q1 14 03/14 -0.18 -0.18 -0.105 In the past four quarters, T-Mobile has had some interesting earnings. In the first quarter of 2014, analysts expected a loss of earnings but T-Mobile lost more than anticipated. Then in quarter 2, T-Mobile’s earnings out performed analysts’ expectations by more than 5 times. Following this strong earning quarter, analysts were anticipating small earnings in quarter 3 but T-Mobile ended up having negative earnings. Finally, in quarter 4 the earnings outperformed expectations by more than double. It appears as if T-Mobile has a cyclical earnings pattern. Following a quarter with a negatives earning, the company posts a strong earning period which is then followed by a negative earning period in the next quarter. Analysts anticipate the first quarter of 2015 to have negative earnings which would follow this cycle. However, I have not found any reason or explanation as to why their earnings have this cyclical approach. Valuation: EquityValue 16,547.71 SharesOutstanding 807.8 Value perShare 20.48 Cost of Equity Beta 1.248 Rm 11.7% Rf 3.8% Ke 13.7% Gn 4.0%

- 5. Based on the discounted cash flow method for valuation, I have concluded that T-Mobile US, Inc. is over valued trading at $31.77. Based on my valuation, I believe that the stock should be trading at approximately $20.48. Based on how the revenue growth is anticipated to slow within the next couple of years, I do not see establishing a position in this company being profitable. I believe that the stock price has been inflated in the past couple of years because of excitement from the merger with MetroPCS and an anticipated growth in market shares based on new products and marketing approaches. T-Mobile has a lot of debt on its books as well. Its total liabilities in 2014 were approximately $41 billion. Its long term debt in 2014 was $24 billion. The revenue in 2014 was $29 billion. Therefore, although T-Mobile is producing a higher revenue than its long term debt, the amount of debt is still too high for me to see a strong growth in their stock price. In the past 7 years, TMUS has had an extremely volatile pattern. It has had multiple major fall offs, one in 2009 and one in 2011. Since 2013, the stock has settled around the $25 - $30 range. Based on the slowing of growth and massive amounts of debt, I cannot foresee a major growth in the stock price. Action: Sell

- 6. Based on my valuation, I would not recommend establishing a position in T-Mobile US, Inc. Due to the large amounts of debt, high chance of default and slowing revenue growth I do not see a position in T-Mobile being profitable. Although T-Mobile is considered one of the four major wireless providers in the United States, this company still has a lot of growth potential. However, the risk involved in taking a position in this company does not have an equivalent potential return. Therefore, my recommendation is to avoid a position in T-Mobile.