Understanding Valuation for Equity Compensation and Avoiding the Perils of 409A

409 A White Paper If you are a CEO or a CFO of a high growth startup, it is vital to understand how to value your company correctly. Here is a quick list of questions this lunch will help you answer: Do you offer or are you planning to offer your employees stock options? Do you know the difference between ISOs and non-ISOs? Do you understand the general valuation concepts and approaches that the IRS has outlined, especially as they apply to early-stage companies? Did you know that if you run afoul of the 409A rules, your employees could have an unpleasant tax surprise and that some of that responsibility could revert back to you as the employer? Do you know if and when you need to engage an outside expert to assist with a valuation? www.thecapitalnetwork.org

Recomendados

Recomendados

Mais conteúdo relacionado

Mais de The Capital Network

Mais de The Capital Network (20)

Understanding Valuation for Equity Compensation and Avoiding the Perils of 409A

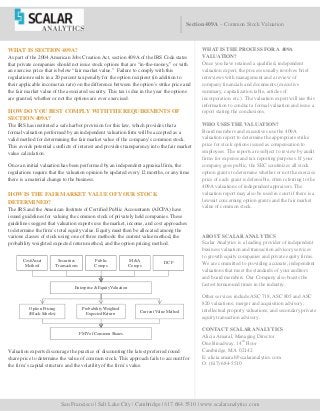

- 1. San Francisco | Salt Lake City | Cambridge | 617.684.5510 | www.scalaranalytics.com Section 409A – Common Stock Valuation WHAT IS SECTION 409A? As part of the 2004 American Jobs Creation Act, section 409A of the IRS Code states that private companies should not issue stock options that are “in-the-money,” or with an exercise price that is below “fair market value.” Failure to comply with this regulation results in a 20 percent tax penalty for the option recipient (in addition to their applicable income tax rate) on the difference between the option’s strike price and the fair market value of the associated security. This tax is due in the year the options are granted, whether or not the options are ever exercised. HOW DO YOU BEST COMPLY WITH THE REQUIREMENTS OF SECTION 409A? The IRS has instituted a safe harbor provision for this law, which provides that a formal valuation performed by an independent valuation firm will be accepted as a valid method for determining the fair market value of the company’s common stock. This avoids potential conflicts of interest and provides transparency into the fair market value calculation. Once an initial valuation has been performed by an independent appraisal firm, the regulations require that the valuation opinion be updated every 12 months, or any time there is a material change to the business. HOW IS THE FAIR MARKET VALUE OF YOUR STOCK DETERMINED? The IRS and the American Institute of Certified Public Accountants (AICPA) have issued guidelines for valuing the common stock of privately held companies. These guidelines suggest that valuation experts use the market, income, and cost approaches to determine the firm’s total equity value. Equity must then be allocated among the various classes of stock using one of three methods: the current value method, the probability weighted expected return method, and the option pricing method. Valuation experts discourage the practice of discounting the latest preferred round share price to determine the value of common stock. This approach fails to account for the firm’s capital structure and the volatility of the firm’s value. Cost/Asset Method Securities Transactions Public Comps M&A Comps DCF Enterprise& EquityValuation Option Pricing (Black-Scholes) ProbabilityWeighted Expected Return Current ValueMethod FMVofCommon Shares ABOUT SCALAR ANALYTICS Scalar Analytics is a leading provider of independent business valuation and transaction advisory services to growth equity companies and private equity firms. We are committed to providing accurate, independent valuations that meet the standards of your auditors and board members. Our Company also boasts the fastest turnaround times in the industry. Other services include ASC 718, ASC 805 and ASC 820 valuations; merger and acquisition advisory; intellectual property valuations; and secondary private equity transaction advisory. CONTACT SCALAR ANALYTICS Alicia Amaral, Managing Director One Broadway, 14th Floor Cambridge, MA 02142 E: alicia.amaral@scalaranalytics.com O: (617) 684-5510 WHAT IS THE PROCESS FOR A 409A VALUATION? Once you have retained a qualified, independent valuation expert, the process usually involves brief interviews with management and a review of company financials and documents (executive summary, capitalization table, articles of incorporation, etc.). The valuation expert will use this information to conduct a formal valuation and issue a report stating the conclusions. WHO USES THE VALUATION? Board members and executives use the 409A valuation report to determine the appropriate strike price for stock options issued as compensation to employees. The reports are subject to review by audit firms for expense and tax reporting purposes. If your company goes public, the SEC scrutinizes all stock option grants to determine whether or not the exercise price of each grant is defensible, often referring to the 409A valuations of independent appraisers. The valuation report may also be used in court if there is a lawsuit concerning option grants and the fair market value of common stock.