Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (19)

Semelhante a Basic accounting bca 1

Semelhante a Basic accounting bca 1 (20)

Mais de pcte

Mais de pcte (20)

Basic accounting bca 1

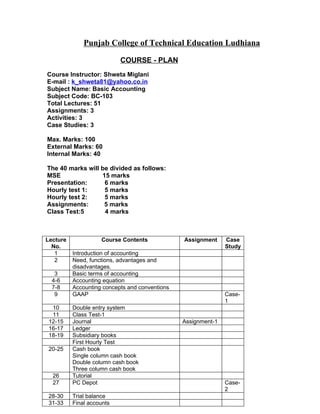

- 1. Punjab College of Technical Education Ludhiana COURSE - PLAN Course Instructor: Shweta Miglani E-mail : k_shweta81@yahoo.co.in Subject Name: Basic Accounting Subject Code: BC-103 Total Lectures: 51 Assignments: 3 Activities: 3 Case Studies: 3 Max. Marks: 100 External Marks: 60 Internal Marks: 40 The 40 marks will be divided as follows: MSE 15 marks Presentation: 6 marks Hourly test 1: 5 marks Hourly test 2: 5 marks Assignments: 5 marks Class Test:5 4 marks Lecture Course Contents Assignment Case No. Study 1 Introduction of accounting 2 Need, functions, advantages and disadvantages. 3 Basic terms of accounting 4-6 Accounting equation 7-8 Accounting concepts and conventions 9 GAAP Case- 1 10 Double entry system 11 Class Test-1 12-15 Journal Assignment-1 16-17 Ledger 18-19 Subsidiary books First Hourly Test 20-25 Cash book Single column cash book Double column cash book Three column cash book 26 Tutorial 27 PC Depot Case- 2 28-30 Trial balance 31-33 Final accounts

- 2. Second Hourly Test 34-37 Final accounts with adjustments Assignment-2 38 Tutorial MSE 39-43 Company accounts- share capital Assignment-3 44 Tutorial 45 Case study based on final accounts Case- 3 46 Management accounting 47 Application of computers in accounting 48 Tutorial 49 Class Test-2 50 Tutorial 51 Tutorial ASSIGNMENT-1 ASSIGNMENT OF JOURNAL ENTRIES 1. Pass the following journal entries: 1. Motilal started business with Rs.10,000 cash and a building worth Rs.50,000. 2. Purchased goods worth Rs.20000 out of which goods worth Rs.12,000 was on credit from shyamlal. 3. Sold goods on credit worth Rs.16,000 to Ramnath. 4. Received Rs.15,900 from Ramnath in full settlement of his account. 5. Paid Rs.11, 800 to shyamlal in full settlement of Rs.12000 due to him. 6. Paid wages Rs.500 and salaries Rs.2,000. 7. Purchased a machinery from Marshal and Sons for Rs.2,000. 8. Machinery depreciated @ 5% p.a. at the year end. 9. Withdrew goods worth Rs.5,000 and cash Rs.1,000 from the business for personal use. 10. A debtor from whom Rs.5,000 were due became insolvent. Only 45% of the amount is realized. 11. Purchased goods worth Rs.10,000 from Sudhir less trade discount 10%. 12. Salary due for the month Rs.1,500. 13. Goods lost by fire Rs.6,500. Stock insured against fire to the extent of 80%. 14. Gave away as charity goods costing Rs.1,500 and cash Rs.500. 15. Rent accrued due on building let-out amounting to Rs.5,000. 2. Enter the following transaction in a three column cash book 2007 Jan1 Cash in hand Rs.5374; Balance at bank Rs.15490 Jan3 Cash sales Rs.6400 Jan5 Paid Rs.7000 into bank Jan6 received a cheque for Rs.700 from Sneh. Jan8 paid into bank Sneh’s cheque. Jan10 Paid to Anurag by cheque Rs.980 and discount allowed by her Rs.20. Jan12 Cash purchases Rs.2500. Jan14 Withdraw from bank for office use Rs.5000.

- 3. Jan15 Received cheque for Rs.950 from lucky’s & Co. allowed him discount Rs. 50. Jan18 Cash sales Rs.7500. Jan19 Paid into bank Luck’s & Co. cheque for Rs.950 and cash Rs.4000. Jan21 Cash paid for stationery Rs.120 sJan23 Paid commission to Rakesh by cheque Rs.500. Jan25 Received cheque for Rs.1000 from Chander Mohan and paid the same into bank. Jan27 Lucky & Co. cheque dishonoured. Jan29 Drew a cheque for Rs.800 for personal use. Jan31 Paid salaries by cheque Rs.1500 and by cash Rs.500. Jan31 Bank charges Rs.20 and insurance premium Rs.520 as shown in pass book. Assignment 2 Assignment (students will know how accounts are to be prepared practically) Practice problem of Financial Accounts 1. From the following ledger balances extracted at the close of trading year ended 31st March 1998 Prepare a trading Account, Profit and Loss Account and balance sheet at that date after giving effect to the undermentioned adjustments. Capital on 1-4-2007 50000 Business Premises 55000 Stock on 1-4-97 8000 Furniture and fixtures 2500 Purchases 20000 Bills Receivables 3500 Sales 80000 Bills Payable 2500 Return Inwards 1500 Sundry Debtors 20000 Returns Outwards 400 Sundry Creditors 15800 Wages 6900 Packing Machinery 4500 Advertisements 5500 Smith’s Loan ( Dr. ) @ Apprenticeship 1200 10% on 1-4-2007 5000 Premium Interest on Smith’s 300 Investment 3000 Loan Proprietor’s 3000 Cash in Hand 250 Withdrawals Office Expenses 8050 Cash at Bank 3500 Adjustments to be Made for the current period are : I) Stock in hand at 31st March 1998 7000.ii) Apprenticeship Premium is for three years, paid in advance on 1st April 1997. iii) Interest on Capital to be allowed at 5% for the year. Iv) Interest on drawings to be charged to him as ascertained for the year Rs.80. v) Rs.5000 out of the advertisement expenses are to be carried forward. Vi) Stock valued at 3000 destroyed by the fire on 25-3-2008 but the insurance Co. admitted a claim of Rs.2000 only and paid it in April 2008. vii) The managers is entitled to a commission of 10% of the Net Profit calculated after charging such commission. viii) Included in sales is an amount of Rs.10000 representing goods on ‘sale or return’ the customer still having the right to return the goods. The goods were invoiced charging a profit of

- 4. 20% on sales. Ix) The stock included material worth Rs.1000 for which bills had not been received and therefore not yet accounted for. Assignment 3 (students will learn how the shares are to be applied for & how the accounting of the same takes place in the books of company’s) 1. DEF Co. Ltd. Issued prospectus inviting applications for 20000 shares of each at a premium of 2 per share payable as follows: On application Rs.2 On allotment Rs.5 (including premium) On first call Rs. 3 On second call Rs. 2 Applications were received for 30000 shares and allotment made pro-rata to the applicants of 24000 shares. Money over paid on application was employed on account of sums due on allotment. Mr. Bhat to whom 400 shares were allotted, failed to pay the alloment money; on his subsequent failure to pay the first call , his shares were forfeited. Mr. Lokesh the holder of 600 shares, failed to pay both calls and his shares were forfeited after the second call. Of the shares forfeited , 800 shares were issued to Mr. Seetharam credited as fully paid, for 9 per share, whole of Mr. Bhat’s shares being included. Pass the necessary journal entries to give effect to the above and prepare Bank Account Forfeited Shares Account and Balance Sheet. PRESENTATION TOPICS: 1.) ATM cards: • procedure of issue • how to use , • problems being faced in using these • How safe is it to use ATM cards 2.) Credit Cards: • procedure of issue • how to use , • problems being faced in using these • How safe is it to use Credit cards 3.) Mutual funds: • Introduction and history • Mutual Fund industry in India • Classification of mutual funds • Advantages of investing in Mutual Funds

- 5. 4.) Different Types of Accounts in Bank • Fixed Deposit Account: Procedure of opening, operating, Rate of interest allowed by different banks on it. • Saving Account: Procedure of opening, operating, Rate of interest allowed by different banks on it. • Recurring Deposit account: Procedure of opening, operating, Rate of interest allowed by different banks on it. • Current Account: Procedure of opening, operating, Rate of interest allowed by different banks on it. 5) Home Loans: Procedure of Applying For it, repayment of amount, Rate of interest being charged by different banks on it, problem faced by banks in recovering these loans, Steps taken by banks in case of default on account of borrower. 6) Educational Loan: Procedure of Applying For it, repayment of amount, Rate of interest being charged by different banks on it problem faced by banks in recovering these loans. Steps taken by banks in case of default on account of borrower. 7) Conveyance Loan : Procedure of Applying For it, repayment of amount, Rate of interest being charged by different banks on it, problem faced by banks in recovering these loans, Steps taken by banks in case of default on account of borrower. 8) Agricultural Loan : Procedure of Applying For it, repayment of amount, Rate of interest being charged by different banks on it, problem faced by banks in recovering these loans, Steps taken by banks in case of default on account of borrower. 9) Personal Loans: Procedure of Applying For it, repayment of amount, Rate of interest being charged by different banks on it, problem faced by banks in recovering these loans, Steps taken by banks in case of default on account of borrower. 10) Equity Shares: procedure of issue, allotment, surrender, forfeiture, and reissue of shares. 11.) Miscellaneous services provided by Mobile Co. in addition to main telecom facilities. 12) Preference shares 13) Debentures

- 6. CASE STUDIES: Case Study 1 - Generally Accepted Accounting Principles On auditing the accounts of AB Ltd. Certain mistakes were being found and due to which correct financial position of the concern couldn’t be ascertained. The concern was started on 1st April 05 and is dealing in the trading of readymade garments. The financial accounts are closed on 31st march every year. For the current year the accounts were closed on 31st Dec 07. Machinery was purchased on 1st July 05 for Rs.100, 000 from Mumbai. The transportation cost incurred on it was Rs.15, 000, and the wages paid on the installation of the machinery were Rs.10, 000.This machinery is recorded in the books at Rs.100, 000.Depreciation @10%p.a is being charged on this value. For the first two years the concern was charging depreciation @10%p.a on diminishing balance method, but in year 2008 the depreciation is charged at 5%p.a on straight line method. The trader withdrew an amount of Rs.10, 000 from the business for buying a bicycle for his son and the same amount is included in the purchases of the financial year and the amt. of sales include a amt. of Rs.5,000 taken by the trader for his personal use. The advertisement expenses shown in the P&L A/c are of Rs.15, 000, out of which an amount of Rs.5, 000 is being paid for the next year. There was an amt. of Rs.3, 000 paid last year in advance for the current year the same has not been adjusted in Advertising expenses in P & L A/ C. The salaries shown in P&L A/C are Rs.50, 000 which does not include the amount of Rs.4, 000 which is outstanding for the financial year. The amount of sales includes an item of Rs.2, 000 for which only order has been placed and it is to be delivered on 10th April 09. The closing stock at cost is of Rs.8, 000 but its market value is Rs.10, 000. It has been shown in the balance sheet at market value. You are required to:- 1. Find out the problem and correct it. 2. Name the concept or convention to be applied to correct each problem. Case Study-2 PC Depot PC Depot was a retail store for personal computers and hand held calculators, selling several national brands in each product line. The store was opened in early Sept. by Jenia, a young woman previously employed in direct computer sales for a national firm specializing in business computers. Zenia knew the importance of adequate records. One of her first decisions, therefore, was to hire Ramesh a local accountant, to set up her bookkeeping system. Ramesh wrote up the store’s pre opening financial transactions in journal form to serve as an example. Zenia agreed to write up the remainder of the store’s Sept. financial transactions for Ramesh’s later review. At the end of Sept. Zenia had the following items to record: Entry Dr.(Amt.) Cr. (Amt.)

- 7. No. account 1 Cash 1,65,000 To Bank Loan payable (15%) 100,000 To Proprietor’s Capital 65,000 2 Rent Expense (Sept) 1,485 To cash 1,485 3 Merchandise inventory 137,500 To Accounts payable 137,500 4 Furniture and fixture(10yrs life) 15,500 To cash 15,500 5 Advertising expenses 1,320 To cash 1,320 6 Wages expenses 935 To Cash 935 7 Office supplies expenses 1,100 To cash 1,100 8 Utilities expenses 275 To cash 275 9 Cash sales for Sept. 38,000 10 Credit sales for Sept. 14,850 11 Cash received from credit customers 3,614 12 Bills paid to merchandise suppliers 96195 13 New merchandise received on credit from 49,940 suppliers 14 Ms. Zenia ascertained the cost of merchandise 38,140 sold was 15 Wages paid to assistant 688 16 Wages earned but un paid at the end of Sept. 440 17 Rent paid for Oct. 1,485 18 Insurance bill paid for one year (Sept. 1- 2,310 Aug.31) 19 Bills received, but unpaid from electric Co. 226 20 Purchased typewriter, Paying Rs.660 cash and 1,760 agreeing to pay the Rs.1,100 balance by Dec 31 a. Explain the events that probably gave rise to journal entries 1 through 8 b. Set upto a ledger account for each account. Post entries 1 through 8 to these accounts. c. Analyze the facts listed as 9 through 20, resolving them into debit and credit elements. Prepare journal entries and post to ledger accounts. d. Consider any other transaction that should be recorded. Why are these adjusting entries required? Prepare journal entries for them and post to ledger accounts.

- 8. CLASS ACTIVITIES: 1 This activity will make the students to take interest in stock market which will encourage and help them for investment in future Every student will be given a Co. & he will have to keep a watch on the share price of that Co. for one month and apply trend analysis on it to study the status of the Co. 2 Students will collect transactions from their business of 1 month and they will prepare journal, ledger, trial balance and final accounts. 3 There will be bank visit to know about how to open a saving account, current account and fixed account.