8447779800, Low rate Call girls in Saket Delhi NCR

EIAA Media Multi-tasking Report

1. EIAA Media Multi-tasking Report

Executive Summary

Media Multi-tasking Report

The first ‘EIAA Media Multi-tasking Report’ is the latest in the EIAA Mediascope

Europe series. This research reveals a marked increase in the number of people

choosing to consume TV and internet simultaneously (+38% since 2006 to 22%),

heralding the emergence of the engaged ‘Media Multi-Tasker’ and highlighting how

consumers are entering a new phase of communications and commerce online.

Summary

MEDIA MULTI-TASKERS: MORE ENGAGED & ENTERTAINED ONLINE

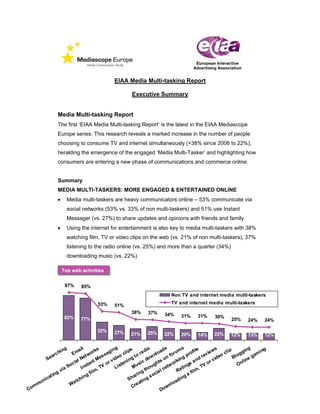

• Media multi-taskers are heavy communicators online – 53% communicate via

social networks (53% vs. 33% of non multi-taskers) and 51% use Instant

Messager (vs. 27%) to share updates and opinions with friends and family

• Using the internet for entertainment is also key to media multi-taskers with 38%

watching film, TV or video clips on the web (vs. 21% of non multi-taskers), 37%

listening to the radio online (vs. 25%) and more than a quarter (34%)

downloading music (vs. 22%)

Top web activities

87% 85%

Non TV and internet media multi-taskers

53% TV and internet media multi-taskers

51%

38% 37% 34%

82% 31% 31% 30%

77% 25% 24% 24%

33% 27% 25%

21% 22% 20% 14% 22% 12% 13% 12%

i ng a il ks gi n

g s io ad

s

um

s

file

s p gin

g

ing

rc h Em t wor sa lip ra d nlo for g pro ie w o cli

ea e es eo c g to w r ev e l og g am

S lN tM v id in do on in nd v id

B

ne

c ia stan or ten sic hts w ork sa or nl i

So In V Li s Mu ug t tin

g

,T

V O

ia ,T ho ne Ra

gv fi lm n gt c ia l film

at i

n

i ng ari so ga

ni c tch Sh ti ng adi n

u

mm Wa Cr

ea nl o

Co D ow

2. • Almost a third (29%) of media multi-taskers use their mobile to communicate

without talking (e.g. via email, IM, communicating via social networking)

suggesting they are both technologically sophisticated and more deeply engaged

as a target market

WORD OF INTERNET

• Media multi-taskers are more inclined to take onboard information from the

websites of well known brands (57% vs. 46% of non multi-taskers), price

comparison websites (57% vs. 47%) and customer website reviews (54% vs.

41%) when researching or considering a product or service:

Important sources of information when researching or considering a product or service

TV and internet media multi-taskers

67% Non TV and internet media multi-taskers

62%

57% 57%

54%

46% 47%

41%

Personal Websites of well Price comparison Customer website

recommendations known brands websites reviews

• Almost half of TV and internet multi-taskers (48%) also admit to actively changing

their mind about a brand compared to 36% of non multi-taskers

• The above implies that ‘word of mouth’ is fast developing into ‘word of web’ and

for marketers, demonstrates how consumers are becoming more empowered to

formulate and communicate thoughts and opinions of brands online. It also

highlights the need to effectively engage with audiences online to build and

safeguard brand reputation.

E-COMMERCE

• The research shows that TV and internet multi-taskers buy almost twice as many

items online than those that do not mix their media (12 items vs. 7) and spend

26% more money on these items (€798 vs. €632 on average).

3. Average number of online purchases per person in 6 months and spend (€)

Online Spend (€)

15 Number of Items Bought Online 1000€

12.0

750€

10

7.0

500€

5

250€

798€ 632€

0 0€

TV and internet media multi-Non TV and internet media multi-

taskers taskers

• The types of popular products bought are not limited to low ticket items and

media multi-taskers also seem especially keen on entertainment, FMCG and

technology products:

Products/services bought online

Top 10 products/services TV and internet multi- Non TV and internet multi-

bought online taskers taskers

Travel tickets 57% 45%

Books 41% 36%

Electrical Goods 41% 27%

Clothes 41% 27%

Concert/theatre/festival 41% 30%

tickets

Holidays 40% 32%

Cinema tickets

31% 18%

CDs

29% 19%

DVDs

28% 16%

Music Downloads

24% 15%

4. IMPACT ON LIFESTYLE

• As a result of the internet, 60% of media multi-taskers believe they are able to

buy better products and services, compared to just 46% of non multi-taskers, in

addition:

o Eight out of ten (80%) multi-taskers state that they are staying in touch

with friends and relatives more (vs. 69% of non multi-taskers)

o More than half (54%) are better able to manage their finances online

(vs. 42%)

Activities done more as a result of the internet

80% 60% 58% 54% 45%

Keep in touch Choose better Book travel / Manage finances Access health

with friends products holidays Non multi-taskers information

Non multi-taskers Non multi- Non multi-taskers = 42% Non multi-taskers

= 69% taskers = 46% = 51% = 41%

• With 88% of media multi-taskers stating they cannot live without at least one web

activity (compared to 79% of non multi-taskers), it seems the empowering effect

the internet is having on lifestyle options and choices is far greater overall than

amongst those who do not mix their media.

PROFILE OF THE MEDIA MULTI-TASKER

• The majority of European media multi-taskers are aged under 35.

o One quarter (25%) of those who mix their media regularly fall within

the digital youth category (16-24 year olds)

o 29% are part of our ‘Golden Youth’ ( 24-35 year olds) – a group

already identified as heavy and engaged users of the internet.

o In comparison, only 13% of media multi-taskers are aged between 45

and 54 years old.

• It seems that Silver Surfers (55+) are also a demographic that is increasingly

meshing their media. With a 75% rise in media multi-tasking since 2006, Silver

Surfers are moving towards being an effective demographic for marketers to tailor

their multi-media campaigns towards in the future

5. Profile of the media multi-taskers vs. non multi-taskers

55+

11%

23%

13%

45-54

% of total number

22% 21%

35-44

24%

29%

18% 25-34

25%

14%

16-24

TV and internet multi-taskers Non TV and internet multi-

taskers

MOVING INTO THE MAINSTREAM

• The rapid growth in the media multi-tasker is expected to be further propelled by

the development of technology and accessibility of the internet.

• Twice as many media multi-taskers access the internet via mobile phone or Wi-Fi

compared to non multi-taskers

• Media multi-taskers are also more likely to have access to wireless technology

(57% vs. 43%) as well as own a laptop (69% vs. 54%)

• This suggests that media multi-taskers will continue to deepen their engagement

with the internet whilst watching TV and that as the numbers of multi-taskers

overall rise, media-meshing will move towards the mainstream.

Products in household

TV and internet media multi-taskers Non TV and internet media multi-taskers

97%98%

87%87%

79%82%

69% 71% 72%74%

54% 59% 56% 55%

41% 40%37% 40%

PC p d r io TV le VR

pto iPo de ad so ca

m

La e r/ or er n /D eb

y rec n co P VR W

pl a er/ alo es

P3 p lay nd Ga

m

M D Sta

DV

6. KEY FINDINGS

• Europeans that use TV and internet simultaneously represent a rapidly growing

group of ‘media multi-taskers’ as media convergence moves mainstream

• Digital youth are the heaviest media multi-taskers while Silver Surfers are also

increasingly multi-tasking their media

• Media multi-taskers are more likely to change their mind about a brand and make

more purchases following web research compared to non multi-taskers

• The need for marketers to manage and build their brand reputation online is

growing rapidly with the emergence of the ‘Word of Web’ as the internet

continues to empower consumers

FOR FURTHER INFORMATION PLEASE CONTACT:

Alison Fennah

Executive Director

EIAA

Tel: +44 (0)1536 712710

Email: afennah@eiaa.net

7. ABOUT THE EUROPEAN INTERACTIVE ADVERTISING ASSOCIATION

(EIAA)

The European Interactive Advertising Association (www.eiaa.net) is a unique pan-

European trade organisation for sellers of interactive media and technology providers.

The primary objectives of the EIAA are to champion and to improve the

understanding of the value of online advertising as a medium, to grow the European

interactive advertising market by proving its effectiveness, thus increasing its share of

total advertising investment. Since its founding in 2002 the EIAA has invested

substantially in multimedia research, marketing, standardisation activities and

education, of both the market and government, on the role of interactive advertising.

With this wide-ranging programme the EIAA has grown quickly to command a solid

reputation and influential position within the European online market.

EIAA members are currently:

With these member networks reaching the majority of the European online audience,

the EIAA is in a unique position to work with advertisers and agencies to realise the

full potential of interactive media in any marketing strategy.