Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

Semelhante a Forex market

Semelhante a Forex market (20)

Forex market

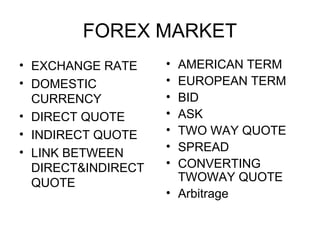

- 1. FOREX MARKET • EXCHANGE RATE • AMERICAN TERM • DOMESTIC • EUROPEAN TERM CURRENCY • BID • DIRECT QUOTE • ASK • INDIRECT QUOTE • TWO WAY QUOTE • LINK BETWEEN • SPREAD DIRECT&INDIRECT • CONVERTING QUOTE TWOWAY QUOTE • Arbitrage

- 2. FOREX MARKET • CROSS RATE • SWAP POINTS • SPOT RATE • FORWARD RATE, • FORWARD RATE PREMIUM AND • APPRECIATION DISCOUNT • DEPRECIATON • COMPUTATION OF APPRECIATION AND DEPRECIATION

- 3. EXCHANGE RATE • THE PRICE OF ONE CURRENCY VIEWED IN RELATION TO ANOTHER CURRENCY IS CALLED EXCHANGE RATE. • EXAMPLE- Re/$ 44.76 means 44.76=1USD

- 4. 3. DIRECT QUOTE • X UNITS OF DOMESTIC CURRENCY EQUAL ONE UNIT OF FOREIGN CURRENCY. • EXAMPLE- Rs44.20 per USD IS A DIRECT QUOTE FOR USD IN INDIA

- 5. 4. INDIRECT QUOTE • THE DOMESTIC CURRENCY IS THE COMMODITY WHICH IS BEING BOUGHT AND SOLD. • COMMODITY COMES FIRST AND PRICE NEXT. • EXAMPLE- Re1=.02 USD

- 6. 5.CONVERTION (D TO I) • RUPEES Rs44.20=1$- DIRECT QUOTE • INDIRECT QUOTE Re1= 1/44.20=.0227 • ? KRONER 0.1481 –KRONERS PER RUPEE • ?SAUDI RIYAL(SAR) .08 –RIYAL PER RUPEE • ? GBP 83.27 RUPEES PER POUND.

- 7. 6. AMERICAN AND EUROPEAN TERMS • AMERICAN TERM IS DIRECT. • EUROPEAN TERM INDIRECT. • EXAMPLE-THE RATE $ 1.5 PER POUND IS AN AMERICAN TERM. • THE QUOTE $1= INR 45 IN EUROPEAN TERM. • ? AMERICA OR EUROPE. • (a) 3.419$ PER QUWAITI DINAR- IN USA IT IS A DIRECT MODE- AMERICAN TERMS. • EUROPEAN TERM- 1/AMRICAN TERM : .2925 KWD PER USD.

- 8. 7. SOLVE • (a) 7.760 HKD PER $ • (b) 7.57 PER DANISH KRONER • Direct quote • American term • 1HKD=.128$ European term • .128Rs=1HKD Indirect quote

- 9. ANSWERS • (a) PERSON IN AMERICA THE QUOTE IS FOREIGN CURRENCY PER UNIT OF HOME CURRENCY. HENSE IT IS INDIRECT MODE- EUROPEAN TERM • THE AMERICAN TERM: 1/EUROPEAN TERM IS 1/7.760= .13 $ PER HKD(HONG-KONG) DOLLAR. • (b)THE QUOTE IS NEITHER EUROPEAN NOR IN AMERICAN TERM SINCE DOLLAR IS NOT ONE OF THE PAIR OF CURRENCIES.

- 10. BID AND ASK • THE BANK’S QUOTE OF BID AND ASK IS FROM THE BANKER’S PERSPECTIVE. • BID= BUY • ASK=SELL • IF THE BID RATE FOR USD IS 40 IT MEANS THAT THE BANK IS READY TO BUY 1$ FOR Rs.40 • IF THE ASK RATE IS FOR USD IS 41, IT MEANS THAT THE BANK IS (ASKING IF SOMEONE WILL BUY) SELLING 1$ FOR Rs.41.

- 11. Three tier architecture • A) bottom tire- Money changers licenced by RBI • B) Second tire-cooperative and Commercial Bank licenced to maintain accounts for NRI • C) TOP TIER- Authoried dealers- Scheduled Banks-full-fledged foreign exchange business.

- 12. Two way quote • BID QUOTE AND ASK QUOTE • Ex: Re/$- 40.42 – 41.63 • Rs.40.42-bid(buying)-( Bank point of view) • Rs.41.63-ask(selling) • Rs.40.42=1$ means the quote is in india • Yen33= Re.1 means the quote is in Japan • If you want to buy, if you have $, you will get Rs.40.42 • If you want to sell Rs. and buy $ you part with Rs.41.63.

- 13. Spread • ASK MINUS BID=SPREAD • EX. 40-41 SPREAD= Rs.41-40=Rs.1 Factors:a) Stability of the exchange rate b) depth of the market-volume of transaction High volume(deep market)-narrow spread Low volume (thin market)-wider spread

- 14. Problem • Indian would like to have travelers cheques: GBP-STERLING 72.70-73.25 • A) explain the quote • B) compute the spread • C) how much would you pay for purchasing 250 pounds in TCS? • D) If you have a balance of pounds 23 in travellers cheques , how many rupees would you receive if the bank in india quotes 73.65-73.92?

- 15. Answer • A)Bank buys at 72.70and Ask rate is 73.25 • B)Spread=.55 • C) 250*73.25=Rs.18312.50 • D)Rs.23*73.65=Rs.1693.95 • Note: in practice all forex transactions are rounded off to a rupee ie Rs.1694

- 16. Converting two way quotes • Formula • Bid(Rs/$)=1/Ask($/Rs)or • Ask(Rs/$)=1/Bid ($/Rs)or • Take the inverse of each rate (bid and ask) and switch them around. • Ex:INR/USD 40.25-41.35 • 1/40.25 1/41.35 • USD/INR =0.0248 =.02418

- 17. PROBLEM • CONSIDER THE FOLLOWING QUOTATIONS IN MUMBAI • Rupee/UAE Dirham(AED)=12.69 • Rupee/Swedish kroner(SEK)=5.49 • Rupee/New Zealand Dollar(NZD)=25.35 • Euro/INR=0.0198 • Compute a)The quote for SEK/AED • b) Euro/NZD

- 18. Solutions • A)SEK/AED=SEK/INR*INR/AED=.18*12.6 9 • =1 AED • B) EURO/NZD=EURO/Re*Re/NZD=.0198*25 .35=.50

- 19. SPOT RATE • RATE OF EXCHANGE FOR IMMEDIATE SETTLEMENT • IT IS SETTLED ON THE SECOND WORKING DAY • SATURDAY AND SUNDAY ARE HOLIDAYS • EX:SPOT RATE:Rs./$40.35-41.36 SUPPOSING YOU HAVE 124000 DOLLAR RECEIVED ON THURSDAY THE BANK WILL SETTLE 124000*40.35=50,03,400 ON THE FOLLOWING MONDAY.

- 20. FORWARD RATE • RATE CONTRACTED TODAY FOR EXCHANGE OF CURRENCIES AT A SPECIFIED FUTURE DATE • THERE IS A FORWARD BID AND FORWARED ASK • CASH DELIVERY-ON THE SAME DAY • TOM DELIVERY-ON WORKING DAY ON THE FOLLOWING DAY

- 21. APPRICIATION AND DEPRECIATION • IF F>S IN A DIRECT QUOTE THE FOREIGN CURRENCY IS APPRECIATING • Home depreciate • Indirect quote: Foreign depreciates and HOME APPRECIATES • Ex: 1. SPOT: SGD .O370=Re 1 • IN SINGAPORE ; FORWARD RATE THREE MONTHS HENCE 0.0360 • SGD APPRECIATES OR DEPRECIATES? • SPOT USD 1.5865= 1 POUND IN UK. FORWARD 1 MONTH 1.5833 . • ?DEPRECIATE OR APPRICIATE

- 22. SWAP POINTS • DIFFRENCE BETWEEN SPOT BID AND FORWARD BID OR SPOT ASK AND FORWARD ASK • ?DIFFRENCE BETWEEN SPREAD AND SWAP POINTS

- 23. FORWARD RATE, PREMIUM AND DISCOUNT • IF SWAP ASK> SWAP BID-FOREIGN CURRENCY IS APPRECIATING HENCE ADD SWAP POINTS • IF SWAP ASK <SWAP BID FOREIGN CURRENCY IS DEPRECIATING. HENCE DEDUCT THE SWAP POINTS.

- 24. Arbitrage • Act of buying currency in one market at lower prices and selling it in another at higher price. • It helps the arbitrageurs in the market to earn profit without risk • It is a balancing operations that do not allow the same currency to have varying rates in different forex markets.

- 25. Types of arbitrage • Geographical • Triangular arbitrage

- 26. Geographical arbitrage • Different prices quoted in two geographical markets for the same currency • Tokyo and London • 1.Observe the following: • Rs/US $ • London Rs.: 42.5730--42.61 • Tokyo $: 42.6750 -- 42.6675 • Can make money out of it?

- 27. • Buy at London market at 42.6100 and sell the same at Tokyo market for Rs.42.6350. • Suppose you buy from London for 100 million Rupees you can get 100 million / 42.61=$2,346,866.932 • Sell $ 2,346,866.932 in Tokyo market at Rs. 42.6350 gives Rs.100,058,671.16 • There are transaction costs involved. • Note: selling price of one market should be higher than buying price of another market.

- 28. Exercise-2 • The following are three quotes in three forex markets 1$=Rs.48.3011 in Mumboi 1pound=Rs.77.1125 in London 1Pound=$1.6231 in Newyork. Are there any arbitrage gains possible? Assume there are no transaction costs and the arbitrageaur has $1,000,000.

- 29. Answer-2 • The cross rate between Mumboi and London with respect to$/pound=77.1125/48.3011 • =$1.5965/pound • But in newyork the price is quoted $1.6231 • There is an opportunity to earn by buing indian rupee in in Mumboi market and convert them into pounds in London Market • Then convert pounds into dollors in NewYork market.

- 30. Answer-2 continues • Rs.48.3011X 1 million dollor=Rs.48,301,100 • Pounds=48,301,100/77.1125=626,371.85 92 • Dollors=626,371.8592X1.6231 =$1,016,664.164. The gain=$16,664.164.

- 31. Exercise-3: arbitrage in forward market • Determine arbitrage gain from the following data: • Spot rate Rs.78.10/pound • 3 month forward rate Rs.78.60/pound • 3 month interest rates: Rupees: 5%; British pound :9% Assume Rs10 million borrowings or pound 200,000 as the case may be.

- 32. Answer-3 • Since forward rate is higher than the spot rate pound is at a premium. • Percentage premium = (78.60- 78.10)X12X100/(78.10X3)=2.56% • Interest rate differential =9%-5%=4% • This helps to borrow from Indian market and invest today in pounds in the spot market

- 33. Method -2 • 1.Borrow in Uk and invest such pounds after converting them into rupees in India • 2.After three months re convert the rupees including the interest into pounds at forward rate • 3.Deduct the loan including interest from step –2 • If step-2 is more than step-3 there is a gain.

- 34. Exercise-4 • Spot rate=78.10; interest rates India-5%; interest rate in UK-9% (pounds); At what forward rate the arbitrage is not possible?

- 35. Answer-4 • Spot rate =78.10 • Add: 4% premium for three month period(78.10 X 4/100) X3/12=0.781 • Forward rate= 78.10-0.781=77.319 • What is the principle used?

- 36. Principle • The arbitrageur earns 4% extra interest to pay 4% forward premium yielding him no gain.

- 37. Exercise-5 • Spot rate-78.10; forward rate for three months-Rs.77.50; rate of interest for pounds-6% for three months.Rate of interest in India-5%. Is there any arbitrage ?

- 38. Answer-5 • The British pound is at a forward discount of 3.073% ie.(78.10-77.50)x 100/78.10x (12/3)100 • Interest rate differential is 6%-5%=1% • There are arbitrage gain possibilities. • Borrow in UK 2,00,000 pounds at 6% and convert them into Indian currency and invest them in India at rate of 5% • The total amount is converted into pounds at the forward rate • Net gain =1067.7419 pounds.

- 39. Exercise-6 • A Ltd is planning to import a multipurpose machine from Japan at a cost of 3400 lakh Yen.The company can borrow at the rate of 18% per annum with quarterly rests.However there is an offer from Tokyo bran of Indian Bank extending credit of 180 days at 2% per annum against the opening of an irrevocable letter of credit. Other information is as follows: • Spot rate for Rs.100=340 yen; 180 days forward rate for Rs.100=345 yen; commission charges for letters of credit are at 2% for 12 months. • Advise the company which mode of purchase is better?

- 40. Answer-6 • Borrowing 3400 lakhs yen • Borrowing in Indian rupee=Rs.1000 lakhs • Interest for the first 3 months= 45 • Interest for the second quarter=47.025 • Total cash outflow at the end of 6 months equals to Rs.1092.025 lakhs. • If letter of credit is followed: Borrowings 3400 lakhs yen Interest for 6 months 34 yen Commission charges 3400 x .02 x6/12=34

- 41. Answer-6 continues • Total payments =3468 lakhs yen • Conversion into indian rupees=1005.217 • Conclusion:- Avail overseas offer

- 42. Exercise-7 • Spot Rs.48/$ ;6 month interest rate: India- 7.5%Per annum; US interest rate-2% per annum.what forward rate will no arbitrage gain be possible?

- 43. Answer-7 • Difference in rate-7.5%- 2%=5.5%p.a. • Spot rate $48 • Add: 5.5% premium for three months (48x (5.5/100) x 3/12) =0.66 Forward rate = 48.66/$

- 44. Exercise-8 • Spot rate- Rs.48.5/$ ; 6 month forward rate-Rs.48.90/$ ; Annualised interest on US 6 month treasury bill –2.5%; annualised interest on Indian 6-month treasury bill-6.0%; what are the transactions the trader will execute to receive arbitrage gain?

- 45. Answer-8 • Interest rate differential=6%-2.5%=3.5%pa • Premium of forward rate=(48.90- 48.5)/48.5x100 x(12/6)=1.65% • Since interest diferential is more than premium forward arbitrage gain is possible.

- 46. Exercise-9 • Calculate cross currency rate between Euro/pound(bid as well as ask) Rs/Us $ Rs 48.35-48.90 Rs/Euro Rs.51.90-52.30 $/ Pound $ 1.49-1.50

- 47. Answer-9 • Euro/Pound(bid)=Rs/Us $ x $/Pound x Euro/Rs=48.35 x1.49 x 1/51.90 • Euro/Pound(ask)=48.90 x 1.50 x1/52.30

- 48. Exercise-10 • You are required to fill in the missing figures and complete the table US Poun Cana Yen Euro dolla d dian r 1USD 1.0 o.616 1.525 ------ 0.928 1 - 1 9 - 7 pound - 1.0 - - - 1Cana - - 1.0 1.0 - di - - - - - 1 Yen - - 1.0

- 49. Answer-10 US Poun Canadi Yen Euro dollar d an 1USD 1.0 o.616 1.5259 118.08 0.9287 1 pound 1.623 1 2.4767 191.655 1.5074 1Canadi 0.655 1.0 1.0 77.3838 0.6086 1 Yen 30.00 .4037 0.0129 1.0 0.0078 1 Euro 85 .0052 1.6430 127.145 1.0 1.076 .6634 7

- 50. Exercise-11 • The following quotations are available to you: by a bank in New York $ 1.6012/Pound By a bank in Paris FFr4.9800/$ By a a bank in London Pound 0.1350/FFr Is any triangular arbitrage possible?

- 51. Answer-11 • From a direct quote of New York and Paris, the cross rate for Pound/FFr is Pound/FFr= Pound/$ x $/FFr= 1/1.6012 x1/4.9800 • Or Pound/FFr =0.1254 • Since in the direct quote the FFr in London is pound 0.1350/FFr(different from 0.1254), triangular arbitrage is possible.

- 52. Answer-11 • 1/1.6012 x 1/ 4.9800=0.1254=Pound/FFr • Since in the direct quote the FFr in London is 0.1350/FFr different from 0.1254, triangular arbitrage is possible.

- 53. • Borrow in the country where the rate of interest is low and invest in the country where interest rate is high.

- 54. Exercise-12 • On 1st April 3 months interest rate in the US $ and Germany are 6.5% and 4.5% per annum respectively.The USD/DM spot rate is 0.6560. What would be the forward rate for DM, for delivery on 30 th June?

- 55. Answer-12 • Spot rate is US $ 0.6560/DM • Interest rate parity relationship S0=[1+imA]/ [1+inB • S0= Spot rate; S1= Future exchange rate • inA=Nominal interest in country A(USA) • inB= Nominal interest in country B(Germany) • S1=0.6560{1+(0.065 x3/12)/1 +(0.045 x 3/12)} = 0.6560 x (1.01625/1.01125) = USD 0.6592 $/DM

- 56. Exercise-13 • Spot rate 47.88/$ • 3 month forward rate 48.28/$ • 3 month interest rates Re.7% $ 11% Is there any arbitrage gain?

- 57. Answer-13 3 month forward rate of dollar is higher than spot rate implies that the dollar is at premium. • Premium(percentage)= (48.28-47.88) / 47.88x(12/3) x 100=3.34% per annum. • Interest rate differential=11%-7%=4% • Since interest rate differential is more than premium percentage there are arbitrage gain possible.

- 58. Exercise-14 • On 1st April, 3 months interest rate in the US and Germany are 4.5% and 6.5 % per annum respectively. The $/DM spot rate is 0.6560. What would be the forward rate for DM for delivery on 30th June?

- 59. • S1=0.6560{1+(0.045 x3/12)/1 +(0.065 x 3/12)} = 0.6560 x ( 1.01125/1.01625) = USD 0.652772 $/DM

- 60. Exercise-15 • In International Monetary Market an international forward bid for December, 15 on pound sterling is $ 1.2816 at the same time that the price of IMM sterling future for delivery on December,15 is $1.2806. The contract size of pound sterling is 62,500. How could the dealer use arbitrage in profit from this situation and how much profit is earned?

- 61. Exercise-16 • ABC Co. have taken 6-month loan from their foreign collaborators for US Dollars 2 millions. Interest payable on maturity is at LIBOR plus 1.0%. Current 6-month LIBOR is 2%. Enquiries regarding exchange rates with their bank elicit the following information: Spot USD 1 Rs. 48.5275 6 months forward Rs.48.4575 1.What would be their total commitment in rupees, if they enter into a forward contract? 2. Will you advise them to do so? Explain giving reasons.

- 62. Exercise-17 • The United States Dollar is selling in India at Rs.45.50. If the interest rate for 6 month borrowing in India is 8% per annum and the corresponding rate in USA is 2%. 1.Do you expect US dollar to be at premium or at discount in the Indian forward market? 2.What is expected 6 month forward rate for United States Dollar in India? 3. What is the rate of forward premium or discount?

- 63. Answer • Borrow in US at 2% and invest in India • Differential interest rate =8%-2%=6% • Since US interest rate is low dollar is at premium. • Forward rate=45.50(1+[.04 x6/12)]=Rs.46.41

- 64. Exercise-18 • A company operation in Japan has today effected sales to an Indian company, the payment being due 3 months from the date of invoice. The invoice amount is 108 lakhs yen. At today’s spot rate, it is equivalent to $30 lakhs. It is anticipated that the exchange will decline by 10% over 3 months period and in order to protect the Yen payments, the importer proposes to take appropriate action in the foreign exchange market. The 3-months forward rate is presently quoted as 3.3 Yen per rupee. You are required to calculate the expected loss and to show how it can be hedged by a forward

- 65. Exercise-19 • The following table shows interest rates for the United States dollar and French francs. The spot exchange rate is 7.05 franks per dollar. Complete the missing entries: 3 months 6 months 1 year Dollar interest rate (annually compounded 11 ½% 12 ¼% ? Frank interest rate 19 ½% ? 20% (annually compounded) Forward franc per dollar ? ? 7.5200 Forward discount on franc per cent per year ? 6.3% ?

- 66. Exercise-20 • In march 2008, the multinational Industries makes the following assessment of dollar rates per British pound to prevail as on 1.9.08. 1) What is the expected spot rate for 1.9.2008? 2) If , as of March,2003, the 6 month forward rate is $1.80, should the firm sell forward its pound receivables due in $/pound Probability September, 2008? 1.6 0.15 1.7 0.20 1.8 0.25 1.9 0.20 2.0 0.20

- 67. Exercise-21 • X Ltd. an Indian company has an export exposure of 10 million(100 lacs) Yen, value September end. Yen is not directly quoted against Rupee. The current spot rates are-USD/INR=41.79 and USD/JPY=129.75. • It is estimated that Yen will depreciate to 144 level and rupee to depreciate against dollar to 43 • Forward rate for September, 2008 USD/Yen =137.35 and USD/INR=42.89. You are required i) To calculate the expected loss if hedging is not done. How the position will change with company taking forward cover? ii) If the spot rate on 30th September, 1998 was eventually USD/Yen=137.85 and USD/INR=42.78, is the decision to take forward cover justified?

- 68. Exercise-22 • A company operating in a country having the dollar as its unit of currency has today invoiced sales to an Indian company, the payment being due three months from the date of invoice.The invoice amount is $13,750 and at today spot rate of $0.0275 per Re.1, is equivalent to Rs.5,00,000. • It is anticipated that the exchange rate will decline by 5% over the three month period and in order to protect the dollar proceeds, the importer proposes to take appropriate action through foreign exchange market. • The three month forward rate is quoted as $0.0273 per Re.1 • You are required to calculate the expected loss and to show, how it can be hedged by forward contract.

- 69. Exercise-23 • Shoe Company sells to a wholesaler in Germany. The purchases price of a shipment is 50,000 deutsche marks with term of 90 days. Upon payment, Shoe Company will convert the DM to dollars. The present spot rate for DM per dollar is 1.71, whereas the 90-day forward rate is 1.70. • You are required to calculate and explain: 1) If Shoe Company were to hedge its foreign –exchange risk, what would it do? What transactions are necessary? 2) Is the deutsche mark at a forward premium or at a forward discont? 3) What is implied differential in interest rates between the two countries? (Use interest rate parity assumption)

- 70. Answer-23 • Spot rate DM/US $ =1.71 • If company receive payment then • 50,000 x 1.71=

- 71. Exercise-24 • A customer with whom the Bank had entered into 3 months forward purchase contract for Swiss Francs 10,000 at the rate of Rs.27.25 comes to the bank after 2 months and requests cancellation of the contract. On this date, the rates prevailing are: • Spot CHF 1=27.30 27.35 • One month forward Rs.27.45 27.52 • What is the loss/gain to the customer on cancellation? • (loss to the customer $2700 due to exchange difference)

- 72. Thank you for watching