Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (19)

Destaque

Semelhante a Set The Wheel Of Controls In Motion

Semelhante a Set The Wheel Of Controls In Motion (20)

Set The Wheel Of Controls In Motion

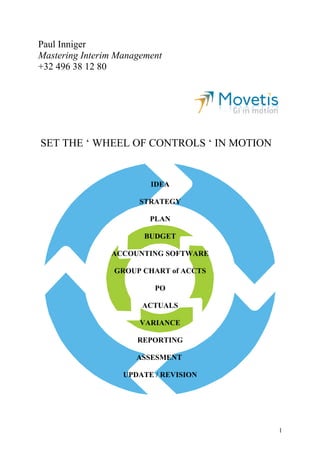

- 1. Paul Inniger Mastering Interim Management +32 496 38 12 80 SET THE ‘ WHEEL OF CONTROLS ‘ IN MOTION IDEA STRATEGY PLAN BUDGET ACCOUNTING SOFTWARE GROUP CHART of ACCTS PO ACTUALS VARIANCE REPORTING ASSESMENT UPDATE / REVISION 1

- 2. IDEA : With each Business Idea, the start is set to implement a Strategy, and to create a Plan. STRATEGY : The Strategy, which is a high level direction from the Board and Sr Management, is immediately translated into a plan, which may, for example, be a 3-year plan. The Strategy of Movetis might be to become a Leading Global Player in the GI Specialty Pharma Business. Or as the Corporate Vision Statement sets : PLAN : The plan, which is drawn by Sr and Middle Management is reviewed each year. The plan is the first level detailed translation of the strategy strategy, containing assumptions, milestones, and detailed financials covering the full period of the plan. The plan will cover numerous consecutive periods. 2

- 3. BUDGET : The first part of the 3 year plan is supported through the yearly budget. This budget is reviewed 2 or 3 times per year, depending on the needs, and the possible changes in the strategy and/or business needs. The budget is built up starting from Sales, COGS, Gross Margin to lower down over Overhead per department, coming to a Gross Profit, Financial Income and Expense, coming to a Pre-Tax Profit. The budget will be the detailed financial guideline to guide the business. ACCOUNTING SYSTEM : So far, all figures supporting the strategy, the 3-year plan and the yearly budget, may, in a start-up situation be drawn based on assumptions, and do not have to be supported by actuals managed and monitored through an accounting system. But the moment Movetis, as a lot of logical steps, have already been executed so far, the need of an Accounting System increases heavily. The current Accounting System sufficiently supports the actual and immediate volume of the Movetis Business GROUP CHART of ACCTS : Without a proper and comprehensive set-up of a Group Chart of Accts, any further step may be jeopardized, unnecessarily slowing down the review of financial data, and moreover being very time consuming and costly. The existing Group Chart of Accts has now been translated into English, and implemented info the three operational countries, Belgium, UK and Germany. The Accounting software Axapta has now been set-up to make sure that the Group Chart of Accts remains same in all three countries. PO : To follow the information trail, each cost (except minors) are initiated through the creation of a PO, which in Axapta is using a : GL acct, belonging to the Group Chart of Accts Product Code Cost Centre This is point of improvement, where currently : Each budgetholder, through it’s assistant(s) are proposing GL accts on the PO, without making ( and being able to make) a link to the budget, and without receiving confirmation from Finance that they understand the content of the GL account tused ACTUALS : Each business action has a financial impact. It’s up to Finance to make sure that all actuals reported at each period-end, completely and truthfully reflect the sales and cost-side of all transactions related to those periods. 3

- 4. Finance has a number of tools available within Axapta, and through manual reporting tools, such as Excel, to capture, maintain and manage a complete cut-off of all costs and revenues. Finance will follow the guidelines and rules set-out by management, such as, for example the rule for Revenue Recognition. Each member of the Movetis Group needs to work together with Finance, allowing Finance to master the Financials, enabling a complete, correct, and in-time reporting of the financials. VARIANCE : Variance reporting should be built in several phases : a/ Post Transaction Follow-Up and Control : Finance reports the actuals compared to budget. Preferably, the analysis is performed each month, and is discussed during a management meeting with all relevant department heads, each explaining the variances between actuals and budget, the trends, etc. In this phase, Finance prepares the reports, and distributes them to a designated list, after which the results are discussed in detail during a management and control meeting. b/ Pre Transaction Follow-UP and Control : In this pro-active phase, Finance is working very intensely together with the Business. The Business looks at Finance as a Day-to-Day internal Business Partner, which is supporting the Business. During this phase, each new Business Transaction is examined, taking into account numerous base Financials, such as : - link with the existing Budget : o Timing, Overruns, Shifts within the Budget, etc - Cash Flow and Working Capital : o Eg : Payment terms for a nex customer o Eg : Cash-Flow forecasting During the period, Finance supports the Business with dynamic reporting and simulations. At period-end, Finance reports the actuals compared to budget, equally indicating a trend, showing the time-impact of budget over runs and under runs. Preferably, the analysis is performed each month, and is discussed during a management meeting with all relevant department heads, each explaining the variances between actuals and budget, the trends, etc. In this phase, Finance prepares the reports, and distributes them to a designated list, after which the results are discussed in detail during a management and control meeting. In a Business which is investing heavily in fixed assets, a specific part of the Budget should be aimed to a dynamic follow-up of the Capital Budget, with strict authorisation levels, and day-to-day control, where as this task typically should be delegated to a Controller within Finance. The second phase will not be created overnight, and will require a full Business and Financial mind-set from all employees. 4

- 5. REPORTING : To support dynamic reporting, Axapta and the supporting reporting tools will need to be reviewed and strengthened. One of the important steps, already initiated through Finance, is to create a dynamic follow-up and reporting tool from within Axapta enabling reporting for status and follow-up on all Purchase Orders (PO’s), enabling each budget holder and finance to receive the following data : PO initial total PO pipe ( already committed for, but no actuals yet) PO actuals ( actuals posted till a certain date) PO horizon ( initial total minus pipe minus actuals ) This will allow the budget holder to stear it’s projects and PO’s more actively. ASSEMMENT / UPDATE & REVISION : During this phase, cost, actuals, pipe, forecast, are all assessed and reviewed. Finance is feeding the information to management captured from and through the Business, through a well defined format. NEXT STEPS ? ? 5

- 6. SET THE ‘ WHEEL OF CONTROLS ‘ IN MOTION 6