Example 1

•

4 gostaram•2,733 visualizações

The document provides information about the overhead costs of various production and service departments of ABC Co. Ltd. It allocates the overhead costs of indirect labor, supervision, power, rent, insurance and depreciation to each department. It then reallocates the overhead costs of three service departments S1, S2 and S3 to the four production departments P1, P2, P3 and P4 using different allocation bases. Finally, it calculates the appropriate overhead absorption rate for each production department.

Recomendados

Mais conteúdo relacionado

Mais procurados

Semelhante a Example 1

Semelhante a Example 1 (20)

Mais de Malinga Perera

Mais de Malinga Perera (20)

Último

Último (20)

Example 1

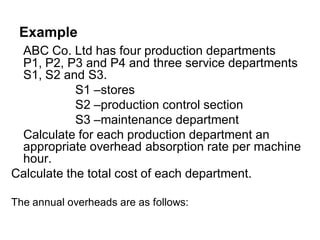

- 1. Example ABC Co. Ltd has four production departments P1, P2, P3 and P4 and three service departments S1, S2 and S3. S1 –stores S2 –production control section S3 –maintenance department Calculate for each production department an appropriate overhead absorption rate per machine hour. Calculate the total cost of each department. The annual overheads are as follows:

- 2. Information Cost Total (Rs.’000) Indirect labour 2,000 Supervision 200 Power 600 Rent 80 Insurance -Building 160 Insurance -Plant 100 Depreciation -Building 240 Depreciation -Plant 120

- 3. Information Indirect Labour Costs Cost centres Actual costs Rs.’000 P1 300 P2 200 P3 500 P4 100 S1 200 S2 300 S3 400

- 4. Information P1 P2 P3 P4 S1 S2 S3 Total No. of employee 400 400 500 600 30 20 50 2,000 Floor Area (Sq.M) 3,000 9,000 8,000 8,000 1,000 1,000 2,000 32,000 Power (KWHrs) 7,000 5,000 3,000 2,000 1,500 500 1,000 20,000 Pro.Cntrl Hours 4,000 5,000 5,000 3,000 - - 1,000 18,000 Stores Requisitions 600 300 250 150 - 400 300 2,000 Maint. Dept Hours 6,000 8,000 5,000 6,000 - - - 25,000 Plant Hrs (‘000) 120 80 200 100 - - - 500 Book value of plant 300 200 100 80 120 50 150 1,000 (Rs.’000)

- 5. Allocation of costs to Production and Service Departments Item Basis Total P1 P2 P3 P4 S1 S2 S3 Ind. Labour Actual 2000 300 200 500 100 200 300 400 Supervision No. of 200 40 40 50 60 3 2 5 employee Power KWHr 600 210 150 90 60 45 15 30 Rent & Floor area 80 7.5 22.5 20 20 2.5 2.5 5 Rates Insurance Floor area 160 15 45 40 40 5 5 10 Building Insurance Book value 100 30 20 10 8 12 2 15 Plant Depreciation Floor area 240 22.5 67.5 60 60 7.5 7.5 15 Building Depreciation Book value 120 36 24 12 9.6 14.4 6 18 Plant Total 3500 661 569 782 357. 289.4 343 498 6

- 6. Calculation Item Basis Total P1 Ind. Labour Actual 2000 300.0 Supervision No. of 200 (200/2,000)*400 = 40.0 Employee Power KWHr 600 (600/20,000)*7000 = 210.0 Rent & rates Floor area 80 (80/32,000)*3000 = 7.5 Insurance -B Floor area 160 (160/32,000)*3000 = 15.0 Insurance-P Book value 100 (100/1,000)*300 = 30.0 Depreciation-B Floor area 240 (240/32,000)*3000 = 22.5 Depreciation-P Book value 120 (120/1,000)*300 = 36.0 Total 3500 661.0

- 7. Reallocation of Service Department Overheads to Production Departments Item Basis Total P1 P2 P3 P4 S1 S2 S3 Total 3500 661.0 569.0 782.0 357.6 289.4 343.0 498.0 costs S1- Store - 86.8 43.4 36.2 21.7 - 57.9 43.4 stores req 289.4 S2-Pro Prodn 3500 748.8 612.4 818.2 379.3 - 400.9 541.4 Control control 89.1 111.35 111.35 66.8 - -400.9 22.3 S3- Main 3500 837.9 723.75 929.55 446.1 - - 563.7 Maint Hrs 135.3 180.4 112.7 135.3 - - - 563.7 Total 3500 973.2 904.15 1042.25 581.4 - - -

- 8. S1- Store - 87.8 43.4 36.2 21.7 (289.4) 57.9 43.4 stores req • S1 P1 (289.4/2000)*600 = 86.82 ≈ 86.8 P2 (289.4/2000)*300 = 43.41 ≈ 43.4 P3 (289.4/2000)*250 = 36.18 ≈ 36.2 P4 (289.4/2000)*150 = 21.71 ≈ 21.7 S2 (289.4/2000)*400 = 57.88 ≈ 57.9 S3 (289.4/2000)*300 = 43.41 ≈ 43.4 Total 289.4

- 9. S2-Pro Prodn 3500 748.8 612.4 818.2 379.3 - 400.9 541.4 Control control 89.1 111.35 111.35 66.8 - (400.9) 22.3 • S2 P1 (400.9/18,000)* 4000= 89.08 ≈ 89.1 P2 (400.9/18,000)* 5000=111.35 P3 (400.9/18,000)* 5000=111.35 P4 (400.9/18,000)* 3000=66.81 ≈ 66.8 S3 (400.9/18,000)* 1000=22.27 ≈ 22.3

- 10. S3- Plant 3500 837.9 723.75 929.55 446.1 - - 563.7 Maint Hrs 135.3 180.4 112.7 135.3 - - (563.7) S3 P1 (563.7/25,000)*6000 =135.288 ≈ 135.3 P2(563.7/25,000)*8000 =180.384 ≈ 180.4 P3(563.7/25,000)*5000 =112.74 ≈ 112.7 P4 (563.7/25,000)*6000 =135.288 ≈ 135.3 Total 563.7

- 11. Calculation of appropriate departmental overhead rates • Based on machine hours P1 = 973.3/120 = 8.11 per M/C hour P2 = 904.15/80 = 11.30 per M/C hour P3 =1042.25/200 = 5.21 per M/C hour P4 = 581.4/100 = 5.81 per M/C hour

- 12. Charging Overhead Rates to Products Overhead costs in each cost centre should be absorbed by the products, at an absorption rate of each product. Pro.Dep. Job1(hours) Job2(hours) Job3(hours) P1 3 12 1.5 P2 2.5 0 4 P3 0 5 10 P4 5 0 3

- 13. • Then, based on the production hours the overhead costs chargeable are as follows: • Job 1 = 3*8.11+2.5*11.3+5*5.81 = 81.63 • Job 2 = 12*8.11+5*5.21 = 123.37 • Job 3 = 1.5*8.11+4*11.3+10*5.21+3*5.81 =

- 14. Allocation service department costs Example A manufacturing firm has three production departments, P1, P2 and P3, and two service departments, S1and S2. the following costs are shown in the overhead distribution sheet. production dep. P1 = Rs. 5000 production dep. P2 = Rs. 8000 production dep. P3 = Rs. 6000 service dep. S1 = Rs. 1280 service dep. S2 = Rs. 3000 Total = Rs.23,280

- 15. • The costs of the two service departments S1 and S2 are to be re-apportioned to production departments using the following basis. S1 S2 P1 20% 30% P2 40% 30% P3 10% 20% S1 - 20% S2 30% - Total 100% 100%

- 16. • There are 3 basic methods of allocating service department costs. 1. Continuous Allotment 2. Simultaneous Equation method 3. Specified order of Re-Allocation

- 17. Continuous Allotment Costs of service departments are re-allocated to other departments repeatedly until the amount remaining is too insignificant. s1 s2 P1 20% 30% P2 40% 30% P3 10% 20% S1 - 20% S2 30% - Total 100% 100%

- 18. Total P1 P2 P3 S1 S2 Cost before 23280 5000 8000 6000 1280 3000 re-allocation Dept S1 256 512 128 (1280) 384 Dept. S2 1015 1015 677 677 (3384) 135 271 68 (677) 203 61 62 40 40 (203) 8 16 4 (40) 12 3.6 3.6 2.4 2.4 (12) 4 4 3 - - Total 2380 6479 9880 6920

- 19. Simultaneous equation method X=total cost of S1 after receiving 20% cost of S2 Y=total cost of S2 after receiving 30% cost of S1 X=1280+0.2Y Y=3000+0.3X By solving two equation above, X=2000 and Y=3600

- 20. As above Total P1 P2 P3 Cost before 19000 5000 8000 6000 re-allocation Dept S1 2000 1400* 400* 800* 200* Dept S2 3600 2880 1080 1080 720 Total 23280 6480 9880 6920 (2000/100)*70 (1400/70)*20 (1400/70)*40 (1400/70)*10 =1400 =400 =800 =200

- 21. Specified order of Re-allocation • Assume that service dept. costs are first allocated to S1 and then to S2. S1 S2 30*(100/80) P1 20% 37.5% P2 40% 37.5% 30*(100/80) P3 10% 25.0% 20*(100/80) S1 - - S2 30% - Total 100% 100%

- 22. Total P1 P2 P3 S1 S2 Cost before 23280 5000 8000 6000 1280 3000 re-allocation Dept S1 256 512 128 (1280) 384 Dept. S2 1269 1269 846 - (3384) Total 2380 6525 9781 6974 - - (1280/100)*20 (1280/100)*40 (1280/100)*10 (1280) (1280/100)*30 =256 =512 =128 =384