Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (20)

Semelhante a Current Status of Bio-Based Chemicals

Semelhante a Current Status of Bio-Based Chemicals (20)

Último

Último (20)

Current Status of Bio-Based Chemicals

- 1. CURRENT STATUS OF BIO-BASED CHEMICALS (2015) BIOTECH SUPPORT SERVICES (BSS), INDIA S. N. JOGDAND

- 2. 2 CURRENT STATUS OF BIO-BASED CHEMICALS CONTENTS Chapter No. Contents Page No. 1 Bio-based Chemical Industry – Strength of Bio-Economy 03 2 Worldwide Scenario of Bio-based Chemicals 34 3 Biorefinery 63 4 Biotechnological Production of 1,4 -Butanediol 88 5 Biotechnological Production of Acrylamide, Polyacrylic acid 100 6 Bio-Adipic Acid 117 7 Bio-Ethylene 127 8 Bio-Isobutanol 138 9 Bio-Isoprene, Bio-Butadiene 148 10 Bio-Succinic Acid 173 11 Biotechnological Production of Propane 1,3 –diol (PDO) 197 12 Bio-Monoethylene Glycol (Bio-MEG) 211 13 Farnesene 219 14 Epichlorohydrin 224 Summary We have been obtaining chemicals, fuels and products largely from fossil resources. Recently understandings of need, development of bio-processes have enabled us to make the same as bio-based. Thus we have (i) bio-based chemicals (platform chemicals used to obtain range of other chemicals) (ii) bio-based fuels (iii) bio-based products e.g. bio-detergents, bio-lubricants, bio-surfactants etc. which are not further converted into anything but find applications themselves. Many references take account of biofuels and bio-based products but the area of bio-based chemicals (‗platform‘ or ‗Intermediate‘ chemicals) is perhaps still developing and commercial production of them is relatively new. New generation of industrial material, polymers, plastics and many other products in turn will be produced from bio-based chemicals. That makes this era dominated by ‗Bioeconomy‘. So this Report discusses the development of bio-based chemicals. For Soft Copy of the Report write an email to snjogdand@gmail.com or info@biotechsupportbase.com

- 3. 3 Chapter 1 Bio-based Chemical Industry – Strength of Bio-Economy 1.1 What is Bio-based? 1.2 Definition of Bio-based Chemicals 1.3 Historic Biobased Chemistry 1.4 Three Approaches to Bio-based Materials 1.5 Market for Bio-based Products 1.6 Drivers / Factors Affecting Introduction of Bio-based Products 1.7 Hinderances in Introduction of Bio-based Products 1.8 Environmental Benefits of Bioprocesses 1.9 Benefits of Bio-based Chemicals 1.10 Negatives of Bio-based Chemicals 1.11 Chemical Processes Vs Biotransformations 1.12 Impact of Shift to Biobased Chemicals 1.13 Classification of Industrially Produced Chemicals 1.14 Industrial biotechnology and the biobased economy 1.15 Bio-based Chemical Development 1.16 Economics and Prospects of Bio-based Products 1.17 Investments in Bio-based Chemicals and Materials Developers 1.18 Shift towards Biobased Chemicals and Products 1.19 Questions about Biobased Materials 1.20 Recent Large Projects from bio-based feedstocks 1.21 Challenges for Bio-based Chemicals Industry 1.22 Epichlorohydrin What is Bio-based? Bio-based materials are those which are produced using renewable resources of biological origin and / or products produced using biological catalytic agents. Bio-based materials encompass: biofuels (bio-diesel and fuel alcohol) and bio-based chemicals (e.g. succinic acid) obtained from processing of agricultural products, forest biomass and municipal wastes. Bio-based products

- 4. 4 Bio-based chemicals use new carbon instead of old. In normal cycle biomass produced using carbon dioxide over a period of more than 106 years has got converted into fossil fuels which we are using for polymers, chemicals and fuel. Instead, in bio-based approach we are using biomass / organics produced within months. There are some misunderstandings about bio-based materials - Bio-based materials always have a lower carbon footprint Bio-based chemicals and polymers are a recent development Bio-based materials compete with food supply and consume needed resources Bio-based products will require lengthy development Consumers will accept lower performance and significantly higher prices for Bio-based products Source: Tecnon OrbiChem Definition of Bio-based Chemicals Bio-based chemicals can be defined as ‗Platform and Intermediate chemicals‘ derived from biomass feedstocks and used to produce other chemicals. They are base chemicals for industrial manufacturing processes. It is estimated that current global oil reserves will last up to 2030, as projected in 2006-2007 by IEA. Experts predict the end of cheap fossil fuels by 2040-2050. Chemical industries are already witnessing it and are combating with costly oil and natural gas. More than 85 per cent of the chemicals we use today come from fossil-based feedstocks like oil and gas. However, there is growing demand for biobased chemicals. The range of applications for these bio-based chemicals also continues to expand and these sustainable alternatives to fossil-based chemicals are now being used to manufacture a new generation of bio-based plastics, lubricants, paints, cosmetics, pharmaceuticals and other products; in fact, almost all industrial materials made from fossil resources could be substituted by bio-based counterparts. Current global bio-based chemical and polymer production is estimated to be around 50 million tonnes with a market worth of $3.6 billion, but the industry is growing rapidly. Key sectors like bioplastics are showing annual growth rates in excess of 10 per cent and by 2021, the market for bio-based chemicals and polymers is predicted to more than triple in value to around $12.2 billion. The World Wide Fund for Nature reports that by 2030 the use of bio-based chemicals could prevent 660 million tonnes of carbon dioxide reaching the atmosphere each year.

- 5. 5 In 1950s US Chemical industry was leading in the world and was responsible for over 5 million U.S. jobs and a $20 billion positive trade balance for the United States. However, over the last two decades, competitive advantage for chemicals and plastics manufacturing has shifted towards the Middle East and Asia, as has the industry. U.S. employment in the sector has dropped over the last decade and is projected to shrink further as capital investment for the petroleum-based industry has essentially shifted away from the United States. Biobased chemicals and plastics then had an historic opportunity to reverse these trends by creation of new generation of renewable and sustainable products in United States. Biobased chemicals and plastics — often referred to as biobased products — are virtually the same as their petroleum-based counterparts, but are manufactured from renewable resources. Recent advances in biotechnology are now making it possible to manufacture many traditional chemicals — and many promising new alternatives — from renewable biomass instead of petroleum. Historic Biobased Chemistry Biobased chemical technology is seeing resurgence today but it is by no means new. In fermentation era acetone, butanol, acetic acid etc were produced by fermentation while some other bio-based processes / products had made the beginning. Prior to World War II, furfural, furan and tetrahydrofuran were obtained from cellulosic materials (corn cobs). Butanol was produced by acetone/butanol/ethanol fermentation using carbohydrate subtrates. Acetic acid was produced from fermentation of alcohol (which was produced from sugar). Glycerol was dehydrated to allyl alcohol and acrolein, the precursor for acrylic acid, as early as the 1880s. Hydrogenolysis of carbohydrates to produce, 1,2-propylene glycol, ethylene glycol and glycerol, was reported in 1933. Ethanol dehydration to ethylene was documented as early as 1932. Rayon, the first synthetic fabric, and celluloid, the earliest form of film stock, are partially derived from bio-based sources. Whale oil was used as a lamp oil and lubricant before being displaced by petroleum.

- 6. 6 The reasons these biobased technologies were not successfully commercialized then (or why petrochemical feedstocks dominated chemical industry) and now shift to bio-based are obvious. These are – 1. During the time period of these early developments, between 1920 and 1969, the price of petroleum never exceeded $3.10 per barrel, and it was in abundant supply relative to other feedstocks. 2. Agricultural productivity increased without increase in inputs between 1949 and 2006. 3. Heightened consumer concerns about sustainability. 4. Surprising Innovations in feedstocks and processes to produce bio-based chemicals. 5. Long-term potential of bio- routes to be cost competitive is seen. The application of bioconversion processes has been generally restricted to the production of fine chemicals which are difficult to make by chemical syntheses. In 1979, a novel production process for propene oxide, the 'Cetus Process' was proposed. Thus, for the first time, an enzymatic process was incorporated into a petrochemical process for production of a bulk chemical. In this process, propene halohydrin is synthesized from propene using Caldariornycesfurnago chloroperoxidase in the presence of hydrogen peroxide. Halohydrin is further converted to propene oxide by Flavobucterfurn halohydrin epoxidase. Hydrogen peroxide can be supplied through the oxidation reaction of glucose by glucose-2-oxidase. The arabino-2-hexosulose formed is chemically reduced to D- fructose Next, in 1985, the enzymatic production of acrylamide, a typical commodity chemical, was started on an industrial scale, making microbial transformations in the industrial production of commodity chemicals a rapidly developing fleld. Nitto Chemical Industry started commercial production of acrylamide by enzymatic hydration of acrylonitrile in 1985. Initially in 1990s interest was in biofuels (biodiesel) but it shifted fast to bio-based chemicals (due to the increased value of chemicals relative to fuels). Sustainability concerns and price premium were the reasons again. Due to efficient atom economy carbohydrates are suitable for low-cost production of ethanol, n- and iso-butanol, poly(hydroxyalkanoates), lactic acid, 3-hydroxypropionic acid, diacids such as succinic, fumaric and adipic, diols such as 1,4-butanedioland 1,3-propanediol, isoprene, farnesene and other olefins from alcohol dehydration,ethylene, propylene and butadiene. Carbohydrates are also being chemically transformed to chemicals such as dextrose and

- 7. 7 xylose, and their hydrogenated counterparts, sorbitol and xylitol, isosorbide, glucaric acid, levulinic acid, ethylene and propylene glycol, furfural, hydroxymethylfurfural, furandicarboxylic acid, p-xylene and terephthalic acid, and glycerol derivatives including acrolein, acrylic acid and epichlorohydrin. Most of these chemicals are building blocks. Some are good candidates for platform molecules and high volume commodities. Bio-based polyethylene (PE) and Epichlorohydrin (ECH) are expected to show 10 fold growth in market through the decade. Use of knowledge of molecular biology and impact of genomics and bioinformatics has made it possible to accelerate the efforts of metabolic pathway engineering and to produce desired chemicals commercially. 95% of all chemicals and plastics are produced from non-renewable energy sources, like natural gas, crude oil and coal. Recently there is growing interest in alternative routes to ‗green‘ chemicals. It is expected that bioderived chemicals will come from three sources: (i) Direct production using conventional thermochemical and catalytic process - Direct production is already a reality, as evidenced by the production of propane diol and polylactic acid from corn-derived glucose and others. There has been recent commercialization of bio-derived plasticizers for polyvinyl chloride, polyester resins for coatings and inks, biopolyols for urethane foams and others based on vegetable oil and carbohydrate renewable sources. (ii) Biorefining - Chemical biorefineries, on the other hand, based on various platforms such as carbohydrate/ cellulose, oil, and glycerin, a co-product of biodiesel production, and algae are in the pilot stage. (iii) Expression in plants. Chemicals expressed in genetically enhanced plants to accentuate target functionalities such as primary hydroxyls, oxirane and others are in the discovery phase and still away from commercialization. Enabling technology for this be Industrial Biotechnology in the first place and Synthetic Biology adding to its efficiency. Three Approaches to Bio-based Materials 1. Build on Naturally Occurring Materials • Rayon fibre, Cellophane film – from wood pulp, done for over 100 years. Using eucalyptus trees, the yield per hectare is 10 times that of cotton • Glycerin and fatty acids – from vegetable oils

- 8. 8 • Polylactic acid (PLA) resins from lactic acid • Cellulose acetate, nitrate – from cellulose 2. Develop Bio-Based Routes to Existing Intermediates • Bio-based processes to make MEG, paraxylene, adipic acid, butadiene, caprolactam etc. are being developed; they are in varying stages of advancement - ‗drop in‘ chemicals 3. Develop New Polymers/Fibres • Completely new bio-based polymer products that demonstrate similar or improved properties compared to existing commercial oil-base products. Market for Bio-based Products The market value for biobased chemicals was estimated to be between $130 billion and $180 billion in 2010, and is projected to grow up to 9 percent annually. By 2025, the global market value is projected to reach $483 to $614 billion across a broad range of chemicals as detailed by the USDA. This represents more than 20% share of global chemical industry. In 2007-2017, while chemicals‘ market is projected to grow 60%, bio-based chemicals‘ market will grow at 600%. The market potential for microbes and microbial products has been estimated by BCC Research market forcasting firm in 2011. The global market value for microbial products in bulk chemical production is about $156 billion in 2011and will be $259 billion in 2016 with annual growth rate of 10.7%. The market for bio-based chemicals is comparatively small, 50–75 Bn EUR or 3–4% of global chemical industry sales. Future growth is strongly determined by a number of high-uncertainty developments including technology breakthroughs and government policy. Bio-based chemicals sales will continue to grow and outpace general chemical industry growth. The dedicated production of chemicals through biocatalysis and fermentation is expected to exhibit strong growth in all scenarios. However, a wholesale transformation of the industry is not expected, with bio-based chemicals constituting another option in the chemical industry toolkit, causing a more or less gradual shift from a petroleum-based industry towards one with additional feedstock options. According to Germany‘s Nova Institute market study, production capacity of bio-based polymers will triple from 3.5 million tones in 2011 to nearly 12 million tonnes in 2020. Bio-based drop-in PET and PE/PP polymers and the new polymers PLA and PHA show the fastest rates of market growth. Europe‘s share will decrease from 20% to 14% and North America‘s share from 15% to

- 9. 9 13%, whereas Asia‘s will increase from 52% to 55% and South America‘s from 13% to 18%. Major capital investment is expected to take place in Asia and South America. Drivers / Factors Affecting Introduction of Bio-based Products The fossil resources are finite in stock but the demand for them is continuously increasing. 80% of available raw materials and energy are consumed by affluent 20% in the developed world. Also India and China who have huge human population and rapid economic growth have growing demand for energy and material resources. These are the main driving forces in search for bio-based energy and materials. The global markets for Biobased products are expected to grow rapidly over the next few years. Biobased materials are displacing the petrochemical based materials. Drivers may differ from region to region and country to country depending on issues like their strengths, weaknesses, choices and compulsions. Main drivers for bio-based products are – 1. society's need to reduce its dependence on fossil-based products, 2. the rapid demographic growth of developing countries with their increased fuel demand, and 3. the growing global concern for the future sustainability of our environment. 4. Demand for safer materials that are regulatory compliant, 5. Unfavorable petroleum price dynamics, 6. Materials shortages resulting from shifts in the chemical manufacturing industry, and 7. Increasing consumer demand for green products (environmental considerations). 8. Voluntary corporate environmental initiatives 9. GreenHouse Gas (GHG) emission Regulations 10. Changing consumer behavior with respect to purchasing decisions which have ethical, moral considerations 11. Availability of cost effective technology to produce bio-based products 12. Availability of novel functional building blocks and improved processes Traditionally biobased chemicals are used in niche applications such as personal care and food additives. New applications of biobased chemicals are emerging which are – bio-surfactants, bio-lubricants, bio-polymers. Respective chemical companies are now diversifying their products based on use of bio-based chemicals. The advantage of this to company is that it can significantly lower their portfolio risk and their carbon footprint.

- 10. 10 Hinderances in Introduction of Bio-based Products Key factors hindering successful introduction of chemicals and plastics from agricultural feedstock are: 1. Cost of production in comparison to petroleum based processes 2. Product functionality limitation, 3. Size. 4. Investment required for infrastructure and distribution 5. No incentive for adopting of bio-route 6. Downstream users of chemicals reluctant to change supply chain if bio route products are little costlier Environmental Benefits of Bioprocesses The shift to bioprocessing for production of vitamin B2 resulted in a 40% cost reduction and only 5% of the previous level of waste. A similar change to a biological production process for antibiotics combined the original ten-stage process into a single step, giving a 65% reduction in waste, using 50% less energy and halving the cost. Use of enzymes for textile processing reduced energy needs by 25% and gave 60% less effluent. Production of bioplastics derived from cornstarch reduced the inputs of fossil fuels by 17- 55% compared to the conventional alternatives. The use of biofuels and conversion of chemical processes to use agricultural feedstocks gives significant reductions in net carbon emissions. Benefits of Bio-based Chemicals For both companies and consumers there are new and different functionalities of bio- based chemicals. They can offer innovative and better products, Reduce environmental impacts, IB advocates lower net carbon emissions (since growing the feedstock would subtract carbon dioxide from the atmosphere) On the political-economic side, a bio-economy would rely less on oil imports from parts of the world deemed less stable.

- 11. 11 Negatives of Bio-based Chemicals But there are critics too, who state that the expectations are exaggerated. IB remains of little importance for chemical production overall, especially where IB products are more expensive than alternatives, Industry should not exploit valuable farmland that can be used to grow food and feed The petrochemical industry is not a key contributor to climate change; of all crude oil that is produced, only about 5 per cent is used by the petrochemical industry. It does so very efficiently, converting it into useful products first and eventually into energy when it is burned in incinerators, thus providing double use. Chemical Processes Vs Biotransformations Sr. No. Chemical Processes Biotransformations 1 Productivity is low. High productivity 2 Chemical catalyst Repeated use of biocatalyst 3 Relatively harsh / hazardous reaction conditions Carried out in mild reaction conditions 4 Energy intensive Less energy required for biocatalysis 5 Reactions not specific Highly specific reactions with respect to structure and stereo chemistry 6 Generally highly pure substrate required to get pure product of specific chemistry Biocatalyst is highly specific so substrate need not be of high purity 7 More environmental pollution Less environmental pollution 8 Conservation of resources 9 So far generally used for synthesis of ‗fine chemicals‘ but now applications for ‗commodity chemicals‘ synthesis is growing. Impact of Shift to Biobased Chemicals World Market penetration expected from biobased products is as follows – Chemical Industry Sector 2010 2025 Commodity Chemicals 1-2% 6-10% Specialty Chemicals 20-25% 45-50% Fine Chemicals 20-25% 45-50% Polymers 5-10% 10-20% Source: USDA, U.S. Biobased Products Market Potential and Projections Through 2025 Biobased American chemical industry employed 5700 Americans at 159 facilities in 2007. Every new job in the chemical industry creates 5.5 additional jobs elsewhere in the economy. Recent bio-refinery openings are likely to be responsible for 40,000 jobs. Less than 4% of U.S chemical

- 12. 12 sales are bio-based, recent USDA analysis puts the potential market share in excess of 20% by 2025 with adequate Federal policy support. This growth could save tens of thousands of additional jobs in the next five years. US is well positioned to capture share in biobased chemicals market due to its leading biotechnology status, strong agricultural sector with largest arable land, and good downstream infrastructure (warehouses, manufacturing etc.). The growth trend of industrial biotechnology is forcasted at 15-20% per year for 2010- 2020. Classification of Industrially Produced Chemicals Chemical industry is large. The world‘s chemicals production in 2002 was in excess of 1.3 trillion. This industry consists of four major subsectors: basic chemicals, specialty chemicals, consumer care products, and life science products. Biotechnology impacts all these sectors, but to different degrees. Demarcation between sectors is not distinct. No. Category of Chemical Features Examples 1 Bulk Chemical (Commodity Chemicals) Single pure chemical substance. Produced in specialized plant. High volume / low price chemicals. Account for 95% of total chemicals produced. High volume production. Used in processing applications (e.g. pulp and paper, oil refining, metals recovery) and Used as raw materials for producing other basic chemicals, specialty chemicals, and consumer products, including manufactured goods (textiles,automobiles, etc.) 2 Specialty Chemical These are generally mixtures. Derived from basic chemicals but are more technologically advanced and used in lesser volumes than the basic chemicals. Specialty chemicals have a higher value-added component because they are not easily duplicated by other producers or are protected from competition by patents. These chemicals are sold on performance. – on What they can do? Adhesives and sealants, catalysts, coatings, and plastic additives. 3 Consumer care products Products in this category are high-tech in nature and developing them demands expensive research. Soaps, detergents, bleaches, laundry aids, hair care products, skin care products, fragrances, etc., 4 Life science products Pharmaceuticals, products of crop protection and products of modern biotechnology 5 Fine Chemicals Single pure chemical substance. Produced in multi-purpose plant. Low volume / high price 6-aminopenicillanic acid Flavours, fragrance, tobacco,

- 13. 13 chemicals. Few applications. Sold on specifications – what they are? Starting materials for specialty chemicals (pharmaceuticals, biopharmaceuticals, agrochemicals) Global production value - $85 billion foundry, agrochemical and pharmaceutical and other Industrial applications. Commodity chemicals are characterized by relatively high raw material costs as compared to to the cost of production. In contrast to fine chemicals, the commodity chemicals are inexpensive, have larger demand and are produced and sold in bulk quantity. Most of the commodity chemicals are intermediates for further synthesis. Bulk Chemicals Fine Chemicals 1 Produced in large quantities using standardised procedures in continuous set-ups High quality chemicals often made in batch, multipurpose equipment 2 Annual Production >10ktonnes Annual Production <10ktonnes 3 Price Levels 800-2500 Euro/tonne Price Levels >3000 Euro/tonne 4 Examples of Petrochemical products – Ethylene, Propylene, Aromatics Flavours, fragrance, tobacco, foundry, agrochemical and pharmaceutical and other industrial applications Industrial biotechnology and the biobased economy According to a report from Smithers Rapra (www.rapra.net or www.smithersrapra.com), Industrial Biotechnology is currently worth €23 billion representing just 6% in sales of the overall worldwide chemicals market. However, it is significantly out-performing the overall chemicals market at an impressive 20% annual growth rate and has the potential to become the dominant technology of tomorrow's chemicals industry and estimates from different sources consider that: The global revenue potential of the entire biomass value chain for biorefineries could exceed € 200 billion by 2020 (WEF (2010) The future of Industrial Biorefineries) The share of bio-based processes in all chemical production is likely to increase from less than 2% in 2005 to 25% in 2025 (OECD (2009) The bioeconomy to 2030: Designing a Policy Agenda ), and could reach 30% in Europe by 2030 (>50% for high added value chemicals and polymers, less than 10% of bulk commodity chemicals) (Star-COLIBRI (2011) Joint European Biorefinery Vision for 2030) Up to 75 billion litres of bioethanol could be sustainably produced at a competitive cost by 2020, which would represent about €15 billion in additional revenue for the agricultural sector; (Bloomberg New Energy Finance (2010) Next-generation ethanol and biochemicals: What's in it for Europe)

- 14. 14 The same report predicts development for 2nd generation bioethanol in the EU by 2020 could lead to almost 950 biorefineries generating more than € 32 billion in annual revenue and 933 000 jobs (total man years from 2010 to 2020). Therefore, the biobased economy represents a huge future opportunity, and, in Europe, by 2020 it is estimated that the biobased chemicals market will be worth €40 billion and will have generated 90,000 jobs within the bio-chemical industry alone. Delivering on this opportunity will require significant investment, innovation and value chain development and most importantly new collaborations across the sector. Important challenges will be posed by high energy prices, the impact of the shale gas boom on the development of biobased chemicals markets and the ongoing need for predictable, coherent and supportive policy in the EU. In order to economically and technically compete with petroleum based products it is essential to develop robust microorganisms and efficient processing techniques that are capable of producing biochemicals with high performance and low production cost. Strategies of developing microbial strains using metabolic engineering have been successfully applied to industrial production of several value-added chemicals. The market for microbes and microbial products is forcasted by BCC research in 2011. The global market for microbial products in bulk chemicals production is $156 billion in 2011 and will reach $259 billion in 2016 with annual growth rate of 10.7%. Market for microbes is $4.9 billion in 2011 and will be $6.8 billion in 2016. Bio-based Chemical Development Biobased chemicals are expected to gain 1.5m tonnes production each year upto 2015, from its base figure of 500,000 tonnes per year. By 2015, biobased chemicals capacity will be 6m tonnes per year out of total 400m tonnes of chemicals conventionally produced per year. In 1990s, renewable technology innovators focused on creating biofuels − primarily ethanol and biodiesel. Then in next decade, interest shifted towards bio-based chemicals production. Sustainability, affordable feedstock and price premium were the drivers. Share of biotechnological processes in production of chemicals was 3% in 2004, but is expected to reach upto 15% by 2015. Many bulk chemicals like lactic acid, 1,3-propanediol, succinic acid and 1,4-butanediol, etc. can be produced by fermentation using microorganisms. In late 2006 and early 2007, US-based Dow Chemical and Belgium-based Solvay began the process of

- 15. 15 converting their traditional epichlorohydrin (ECH) production processes into ones that use bio- based glycerol as feedstock. Now they have begun large-scale production. Major chemical companies and consumer product firms are committed to the development and use of bio-based chemicals. Chemical companies such as DuPont, BASF and DSM are rolling out visible corporate strategies with clear messaging around intent to develop bio-based chemicals. Others that are not as vocal are also clearly interested. Consumer momentum also continues to grow in areas such as bottles, apparel and packaging. Genomatica is currently focused on two product platforms – biobutanediol (bio-BDO) and biobutadiene (bio-BD), but continues its interests in other intermediates as well. Germany-based BASF agreed to license Genomatica's technology to build a bio-based BDO plant with a capacity of around 50,000 tonnes / year at a site yet to be determined. Genomatica also has an agreement with Italy-based Novamont to retrofit a plant in Italy to produce bio-BDO. The plant will have a capacity of 20,000 tonnes / year. Genomatica has also made announcements with Japan-based Toray, Germany-based LANXESS and Taiwanbased Far Eastern New Century demonstrating the use of its bioBDO for use in polymer resins and fibre applications. In bio-BD, Genomatica has a venture with Italy-based Versalis to jointly develop and license bioBD technology. Biofuels In the case of biofuels, global production is projected to reach about 135 billion litres by 2020. Brazil is the world's leading producer and primary user of fuel ethanol, and has been for over 25 years. It accounts for slightly less than half the world's total production, with the US coming in second place. With regard to biodiesel, the European Union is currently the world's leading producer: biodiesel production in the region reached 10,187 million liters in 2009, constituting 55-60 percent of world production. One key objective for the world's growing number of biorefineries is to enhance the overall profitability and competitiveness of biofuels. This can be achieved by optimizing their production and driving efficiency. The production path of a bio-based material encompasses the handling and processing of biomass, its fermentation, chemical processing, final recovery, storage and transportation. The production of biofuels is becoming increasingly important for Europe for sustainable future. Rotterdam in Holland is the leader in Europe in facilitating the biobased industry and enabling it to utilize the advantages of the existing (petro-) chemical cluster.

- 16. 16 Economics and Prospects of Bio-based Products No. Shale Gas (SynGas) source Biomass Feedstack source 1 dispersed over vast areas dispersed over vast areas 2 face logistics challenges face logistics challenges 3 require highly capital intensive processing require highly capital intensive processing 4 Provide opportunity to reduce oil dependence Provide opportunity to reduce oil dependence 5 Reduces CO2 emissions Reduces CO2 emissions 6 Development of chemicals by large companies which plan for decades in advance Development of chemicals by large companies which plan for decades in advance If shale gas is used as competitively priced feedstock for certain chemicals it gives opportunity for biomass feedstock in other areas. Shale gas will have positive impact on bio-based chemicals like n-butanol, Isobutanol, paraxylene, Adipic acid, Butadiene, Isoprene, 2,5 - Furandicarboxylic acid, Farnesene while it will have negative impact on ethylene, propylene, Monoethylene glycol. Bio-based chemical investments are driven by raw material availability, price and cost of production, but other factors such as political and financial support play an important role when the first large-scale facility is decided. China, Brazil, Thailand and the US are clear winners in the game. Europe has less bio-based chemicals‘ plants though they have many pilot plants. One of the important factors affecting development of bio-based commodity chemicals is market pull. Global brand owners such as US-based Coca-Cola and France-based Danone and leading retailers such as UK-based Marks & Spencer and France-based Carrefour are large end-users in the commodity chemicals value chain. They all have dedicated programs pursuing environmental sustainability throughout the supply chain. In the case of MEG, Japan-based Toyota Tsusho has taken a different approach. The bio-based value chain is in fact one step longer than the conventional route, but it offers Toyota full control of the value chain from plantations to end-use applications. Large chemical and consumer brand giants who ultimately decide which bio-based chemicals are the first to break ground. All top 20 chemical companies have announced being active in either biofuels or bio-based chemicals. The change in the value chain has called for unconventional partnership networks. Agricultural giants such as US-based firms Cargill, ADM and Bunge have all entered the bio-based chemical business through joint ventures.

- 17. 17 Shale Gas and Biomass feedstock share many features with Coal to olefin as source except CO2 emissions. According to the US Energy Information Administration (EIA) and the Food and Agriculture Organization of the United Nations (FAO), the US has the second largest technically recoverable shale gas reserves identified in the world. China holds 13% of global coal reserves, and Brazil accounts for 40% of global sugarcane production. Impact of coal as source on the global commodity chemicals market has been limited to China. Investment in both shale gas-based and bio-based commodity chemicals is just taking off. Recent investment history shows that global regions are quite differently positioned. North America has significant activity in shale gas whereas Australia is only initiating activities, and in Europe the debate is only starting. Even small reserves on a global scale can have major local effects. European shale gas investments have faced strong resistance from both policymakers and environmental lobbyists. In an EIA study of technically recoverable shale gas in 32 countries, the UK represented only 0.3% of the total resources. The global demand for biodiesel is expected to top 10 billion gallons per year by 2015. Currently 30 countries have implemented biofuel targets and are blending biodiesel with regular fuel. Europe is moving towards 7 percent mix, while Brazil and Indonesia are targeting 10 percent. The developing countries supply 50 percent of the global demand for biofuels, and their commitment to renewable fuel long term is demonstrated by the fact that already 17 percent of the world's biodiesel demand is concentrated in the South. The European Union is the largest consumer of biodiesel with 44 percent of demand, closely followed by Asia-Pacific Region with 39 percent, well ahead of the United States. Investments in Bio-based Chemicals and Materials Developers Capitalists (VCs) invested $3.1 billion in bio-based chemicals and materials developers since 2004. As many of those start-ups reach megaton scales and launch IPOs, Lux Research analysts sought to find which technologies venture investors favored. Analysts tracked 177 venture transactions involving 79 companies operating in five technology categories – biocomposites, bioprocessing, thermochemical processes, crop modification, and algae. In short, they found: Bioprocessing developers infused up $1.89 billion in 96 deals. Bioprocessing developers – especially synthetic biology companies – landed more than half the total venture capital invested since 2004. Encompassing technologies like fermentation, phage display, natural breeding and synthetic biology, all bioprocessing platforms employ some sort of organism as a ―factory‖ for creating products as diverse as sweeteners and catalyst supports. These platforms

- 18. 18 enable the likes of Amyris, Codexis, LS9, and Solazyme to produce multiple products from multiple feedstocks, thus ensuring a relatively low-cost route to high-value compounds and providing a hedge against feedstock and product price volatility. Algae developers saw $190.5 million in 13 deals. This only encompasses start-ups developing algae strains, cultivation systems, and processing equipment for creating industrial chemicals. Representative developers include Bio Architecture Lab, a macroalgae developer, and Israel‘s Rosetta Green, which had raised $1.5 million in venture funds, but more recently brought in almost $6 million in an IPO on the Tel Aviv TASE. It excluded, companies primarily developing fuels, and companies like Solazyme and Green Pacific Biologicals that use algae for fermentation (and, thus, are categorized in bioprocessing, above). Biocomposites developers brought in $108.9 million in a mere nine transactions. This category includes bioplastic blends, some starch plastics, and bio-based foams, from the likes of Cereplast, EcoSynthetix, Ecovative Design, and Entropy Resins. Because of the relatively simple nature of these technologies, VCs often don‘t see them as investment opportunities – forcing companies like SoyWorks and Biop Biopolymer to find other sources of funding. Industry giants Coca-Cola, Ford Motor, Heinz, Nike, and Proctor & Gamble formed a partnership agreement designed to integrate 100% plant-based polyethylene terepthalate (PET) into their product lines at commercial scale. Coca-Cola will partner with Virent, Gevo, and Avantium to accelerate development of their current 30% plant-based monoethylene glycol (MEG) PlantBottle. To date, purely bio-based PET technologies exist. In fact, there are many plant-based routes to terepthalic acid (TPA), which can then be converted to PET. These include both fermentation and catalytic processes that are currently too expensive at commercial scale. Coca-Cola’s goal is to convert all petroleum-based PET products to plant-based PET, which represents 52% of the total packaging within the company. Heinz licensed the MEG PlantBottle technology from Coca-Cola, and hopes to achieve similar goals. Furthermore, Ford shifted from using petroleum-based PET to currently use 25% soy-based polyols for seat cushions, recycled resins for underbody systems, post-industrial recycled yarns for seat fabrics, and repurposed nylon to make cylinder head covers in its bio-based portfolio. Considered a drop-in solution, bio-based PET replicates the mechanical and chemical properties of petroleum-based PET. Therefore, the 100% plant-based PET can potentially be used for all of these end products. This consortium acts as a catalyst to grow the bio-based PET industry to produce plastic bottles, clothing, shoes, automotive carpets, and other furnishings, and essentially any product

- 19. 19 made from traditional PET. These industries will inevitably commercialize the technology due to their current R&D partnerships, access to suppliers, collaborations with universities, and extensive monetary resources. Furthermore, this will enhance the strength of the bio-based materials and chemicals industry by promoting collaboration along the entire supply chain, especially as the rate of forged partnerships is expected to slow in 2012. In Brazil, Coca-Cola contracted JBF Industries to produce ethylene glycol in Araraquara, Sao Paulo, for partially bio-based PlantBottle PET. JBF will build a new plant starting at the end of 2012 and will produce 500,000 metric tons/year; it will take two years to complete. But aside from the feedstock and materials developments, Brazilian national development bank, BNDES, and research-financing agency, Finep, have earmarked $988 million for bio-based chemicals and biofuels investment to be placed in 2012 ($148 million), 2013 ($345 million), and 2014 ($493 million). They emphasize only ―several projects‖ will be pursued. Dow Chemical, Braskem, and DuPont each passed the initial selection phase for their proposals to build projects collectively worth more than $1.5 billion. DSM has already been approved to receive funding for succinic acid from sugarcane. Previously, the two organizations contributed $493 million to research on cellulosic ethanol production, gasification, and other value-added derivatives of sugarcane. Brazil‘s sugarcane continues to put it on the map of bio-based chemicals and biofuels production hotspots. Brazilian government support for sugarcane production and downstream conversion activities is strong, and the Brazilian bio-chemical industry has a reputation for translating technology into commercial successes well. Also existing polymers can become “bio” by using bio-based monomers or intermediates. Sr. No. Polymer Billion USD Bio- Route 1 Polyurethane ~27 Soy-based Polyols 2 Unsaturated Polyster Resins ~13 Maleic anhydride from succinic acid 3 Nylon6 ~13 Caprolactam from fermentation 4 ABS ~11 Butadiene from succinic acid 5 Polyacrylamide ~07 Acrylonitrile from 3HP 6 Polybutadiene ~06 Adipic acid from fermented succinic acid 7 Acrylic fibers ~05 Acrylamide from 3HP 8 Nylon 6.6 ~05 Butadiene from succinic acid 9 Polyethylene Bio-ethylene

- 20. 20 Bio-based Chemicals No. Chemical Routes Players 1 Acrylic Acid Fermentation, Glycerine to Acrolein OPXBio, Dow, Nippon Shokubai, Arkema, BASF, Cargill, Novazymes 2 Alpha Olefins Metathesis Elevance 3 Ethylene, EO, EG Ethanol Dehydration Braskem, India Glycols, Greencol Taiwan (Toyota Tsusho) 4 Isoprene Fermentation Amryis, Michelin, Goodyear, Genencor 5 Butadiene Fermentation, Conversion of bioBDO Genomatica, Global Bioenergies, BASF, Invista 6 Isobutylene Fermentation, Isobutanol Dehydration Global Bioenergies, Gevo, Lanxess 7 BTX APR, Pyrolysis Virent, Anellotech, Cool Planet 8 Propylene Glycol Glycerine Conversion ADM, Cargill, Huntsman, Ashland 9 PX Fermentation, Catalysis Gevo, Micromidas 10 BDO Fermentation, Succinic Acid Hydrogenation Genomatica, Lanzatech, BioAmber 11 PDO Fermentation Dupont, Tate & Lyle 12 Butanols Fermentation Gevo, Butamax, Green Biologics, Cobalt, Butalco 13 Succinic Acid Fermentation BioAmber, Reverdia, PTT, Mitsubishi 14 Adipic Acid Fermentation, Glucose Catalysis Verdezyne, Rennovia 15 ECH Glycerine Conversion Dow, Solvay 16 Ammonia Biomass Gasification BioNitrogen, Syngest 17 Methanol/DME Glycerine Gasification, Biogas Conversion BioMCN, Oberon 18 Lactic Acid Fermentation Nature Works, BASF, Purac, Cargill 19 Polycarbonate Isosorbide Based Mitsubishi Chemical Bio-Processes for Chemicals No. Product Process 1 Bio- 1,4 –Butanediol (BDO) Sucrose to BDO by genetically engineered E.coli. Genomatica has developed the technology 2 Bio- Acrylamide, Polyacrylic acid Acrylic acid, the monomer for PAA, can be produced by means of various processes: 1. Fermentation of sugars to 3-HPA (3-hydroxypropionic acid), followed by dehydration into acrylic acid 2. Catalytic dehydration of lactic acid 3. Conversion of glycerol (via acrolein) to acrylic acid 4. Oxidation of biobased propylene 3 Bio-Adipic Acid Verdezyne‘s novel combinatorial approach to pathway engineering rapidly creates and harnesses genetic diversity to optimize a metabolic pathway. Rather than manipulating one pathway gene at a time, the company uses synthetic gene libraries to introduce diversity into a metabolic pathway. The company‘s unique computational and synthetic biology toolbox allows

- 21. 21 effective design, synthesis and expression of synthesized genes in a heterologous recombinant yeast microorganism. 4 Bio-Ethylene Braskem - Sugar to bio-ethanol to bio-ethylene. 5 Bio-Isobutanol Genetically engineered Yeast to produce Isobutanol instead of ethanol. Gevo has developed the technology 6 Bio-Isoprene, Bio-Butadiene Genetically modified E. coli to produce an isoprene synthase enzyme, and ferments bioisoprene from a variety of biomass feedstocks. Bio- isoprene is harvested in gas phase (at low temperature). Carbohydrates are stripped of oxygens, leading to a 3,3-dimethylallyl pyrophosphate (a/k/a/ DMAPP). Thence, the enzyme isoprene synthase catalyzes the production of BioIsoprene. Genencor has developed the technology. Genetically engineered E.coli to convert glycerine or low-grade free fatty acids into acetone, technical-grade ethanol and bioisoprene. High-yields of isoprene from low-cost feedstocks such as crude glycerol are obtained. GlycosBio has developed the technology Fermentation process to convert CO (carbon monoxide) to ethanol, and then to 2,3-butanediol. Then to dehydrate 2,3-butanediol to 1,3-butadiene. LanzaTech has developed technology for bio-butadiene. 7 Bio-Succinic Acid BioAmber - Gen. Eng. E.coli converts glucose to succinic acid Myriant - Gen. Eng. E.coli converts glucose to succinic acid Reverdia - Saccharomyces cerevisiae converts glucose to succinic acid BASF/Purac - B. succiniciproducens converts glycerol to succinic acid 8 Bio-Propane 1,3 –diol (PDO) Genetically modified Escherichia coli, which ferments the glucose into PDO. Biosynthetic genes from Klebsiella pneumoniae and Saccharomyces cerevisiae are transferred to production strain. DuPont Tate & Lyle BioProducts has developed this process 9 Bio-Monoethylene Glycol (Bio-MEG) Canesugar to bio-ethanol to bio-ethylene to Bio-MEG. Greencol Taiwan Corp, a joint venture between Taiwan‘s China Man-Made Fiber Corp (CMMFC) and Japan‘s Toyota Tsusho 10 Farnesene Amyris has successfully integrated the enzyme xylose isomerase into its existing Biofene producing strains of yeasts, thereby allowing for the simultaneous fermentation of glucose and xylose to farnesene. Amyris has developed the technology. 11 Bio-Methyl Isobutyl Ketone (MIBK) The process utilizes a modified microbe that converts glucose into isovaleric acid and isocaproate. These intermediate chemicals can then be converted to MIBK, diisobutyl ketone or methyl isoamyl ketone. This technology for producing methyl isobutyl ketone has been exclusively licensed to Ascenix Biotechnologies. University of Minnesota's Office can be contacted for Technology Commercialization. 12 Bio route to p-xylene Examples of Recently Realized and Announced Investments in Biobased Chemicals No. Location Company Product Capacity 1 Thailand Purac Lactic Acid 100.000 2 Thailand Purac Lactide 75.000 3 Spain Purac / BASF Succinic acid industrial 4 Louisiana Myrianth / Uhde Succinic acid 14.000* 5 France Bioamber Succinic acid 2.000*

- 22. 22 6 Japan Mitsubishi Succinic acid Pilot 7 France DSM / Roquette Succinic acid Pilot 8 Tennessee DuPont / Tate&Lyle 1,3-PDO 60.000* 9 Illinois ADM PG 100.000* 10 Brazil Braskem Ethene 200.000* 11 Thailand Solvay Epichlorohydrin 100.000* 12 France Roquette Isosorbide Pilot 13 Illinois ADM Isosorbide Pilot t* Announced / under constructionpacity The European Commission (EC) has announced the start of the Biobased Industries Public Private Partnership (PPP), which will see €3.8 billion spent - €1 billion by the EC, the rest by industry, via the Biobased Industries Consortium (BIC) - from 2014 to 2020, to boost market uptake of new biobased products made in Europe. This should begin in early 2014, subject to approval by EU Member States (MSs). Status of Bio-based Chemicals No. Biobased Chemical Laboratory, Pilot, Demonstration Unit Commercial-Scale Production 1 Ethylene Dow Chemical/Mitsui1 Braskem: from sugarcane ethanol, 200,000 m.t./year PE; Lanxess has capacity of 10,000 m.t./year of EPDM rubber, Brazil 2 Ethylene glycol Greencol Taiwan: 100,000-m.t./year bioMEG plant, 2012 India Glycols: from sugarcane ethanol, 175,000 m.t./year 3 Glycolic acid (hydroxyacetic acid) Metabolic Explorer/ Roquette 4 Acetic acid Wacker, 500-m.t./year pilot plant 5 Propylene Braskem, Dow, Global Bioenergies Braskem, considering a 30,000–50,000- m.t./year PP plant 6 Propylene glycol Senergy Chemical, from glycerin Archer Daniels Midland, 100,000 m.t./year 7 1,3-Propanediol Metabolic Explorer, 8,000 m.t./year DuPont Tate & Lyle Bio Products, 45,000 m.t./year 8 1,3-Propanediol Metabolic Explorer, 8,000 m.t./year DuPont Tate & Lyle Bio Products, 45,000 m.t./year 9 Epichlorohydrin Dow Solvay: 10,000-m.t./year plant, France; 100,000-m.t./year plant, Thailand; plant announced for China, 2014, with 100,000-m.t./year capacity, Spolchemie, 15,000-m.t./year plant 10 Lactic acid Cargill: increasing polylactic acid capacity to over 150,000 m.t./year, Galactic, Purac 11 Acetone TetraVitae Bioscience: acquired by Eastman Renewable Cathay Industrial Biotech; Jiangsu Lianhai Biological Technology Co.

- 23. 23 Materials, Nov 2011 12 Acrylic acid Arkema: glycerin-based; BASF, Cargill, Metabolix, Myriant, OPX Biotechnologies/Dow: fermentation-based; SGA Polymers: from lactic acid 13 3-Hydroxy acrylic acid BASF/Cargill/Novozymes jv, kilogram scale 14 Isobutene Gevo/Lanxess; Global Bioenergies Lanxess has 10,000 m.t./year of biobased EPDM rubber, Brazil 15 Butadiene Global Bioenergies; Genomatica 16 Succinic acid BASF/Purac jv (Purac belongs to CSM, now Corbion), BioAmber, Myriant, and Reverdia (DSM, Roquette Freres jv) BASF/Purac, Succinity: Barcelona plant, 10,000 m.t./year, late 2013; plans for a 50,000-m.t./year plant, BioAmber: 350,000-liter fermenter; demo plant, 2,000 m.t. in France; building a 30,000- m.t./year plant, Sarnia, ON (due 2014), with plans to add 20,000 m.t./year; planning plant in Thailand with capacity about 100,000 m.t./year BDO and biosuccinic acid; Reverdia: Dec 2012, 10,000 m.t./y commercial plant 17 1,4-Butanediol BioAmber, Genomatica/Chemtex, Genomatica/Tate & Lyle, Metabolix (from poly-3- hydroxybutyrate (PHB), 8,000 m.t./y SE Asia, Myriant/DPT Lanxess, Genomatica: trial run June 2013 of 20 m.t. PBT using Genomatica‘s bioBDO. Genomatica did five-week BDO run, 2,000 m.t., Toray Apr 2013, BASF and Geonomatica, May 2013, Novamont (Genomatica), 2013 18 Isoprene Amyris, Genencor/Goodyear, Glycos Biotechnologies due to start BioSIM (biobased Synthetic Isoprene Monomer) production 2014 19 2,5- Furandicarboxylic acid (FDCA) Avantium, 20-m.t./year pilot plant; partnership with Solvay for nylon, engineering,thermoplastics Avantium at engineering stage for a 50,000-m.t./year plant 20 Glucaric acid Rivertop Renewables 21 Adipic acid and other nylon precursors BioAmber/Celexion, Draths (now Amyris), Genomatica, Rennovia, and Verdezyne 22 Hexamethylenediam ine (HMDA) Rennovia, Draths (now Amyris) 23 Aromatics Virent (BTX); 10,000-gal/year pilot plant, Annellotech 24 para-Xylene (PX) Gevo2: from bioisobutanol, Virent Energy Systems, Toray: from biobutanol, Anellotech 25 Sebacic acid (decanoic acid), dodecanoic acid Verdezyne Cathay Industrial Biotech

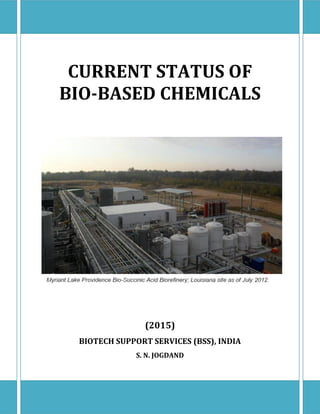

- 24. 24 Bio-based polymers, producing companies in Europe and production capacities (t/a) Production Capacities (Tonnes / Annum) Bio-based Polymers Number of Producing Companies 2013 2020 PLA 07 8.230 226.730 Starch Blends 07 279.000 539.000 PHA 07 10.050 10.090 PA 07 16.000 31.000 PBAT 01 74.000 74.000 Polyolefins (PE, PP, PVC, EPDM) 00 0.000 - PET 00 0.000 300.000 PBT 01 <50 80.000 PUR 03 39.450 39.450 Total 426.780 1,300.270 Source: Report Market Study on Bio-based Polymers in the World, 2013-3 ** Source: Bio-based Polymers Producer Database, 2013-07 Bio-Propylene Glycol No. Company Based In Capacity Started In 1 ADM (Decatur, Ireland) North America, USA 100,000 t/a 2010 Hydrogenolysis of glycerol and sugar alcohols 2 Cargill / Ashland North America, USA 65,000 t/a 2008 3 Dow Chemicals North America, USA 1000 t/a 4 Senergy North America, USA 30,000 t/a 2008 5 Global Biochem China Hydrogenolysis of sorbitol. Biobased propylene glycol has achieved the same product specifications as petrochemical propylene glycol. Life cycle assessment of biobased propylene glycol estimates greenhouse gas impacts for production of bio-based propylene glycol from soybean derived glycerol are approximately 80% that of petro-PG Bio-Succinic Acid No. Company Based In Capacity Started In 1 BioAmber North America, USA 23,000 t/a 2014 2 BioAmber (DNP/ard) North America, USA 3000 t/a 2009 3 CSM / BASF Europe DE 15,000 t/a 2011 4 Lanxess Europe DE 20,000 t/a 2012 5 Myriant North America, USA 15,000 t/a 2013 6 Myriant Technologies, Davy Process Technology North America, USA 15,000 t/a 2013 7 Roquette/DSM Europe/FRA 10,000 t/a 2012 8 Roquette/DSM Europe/ITA 10,000 t/a 2012 9 BASF-Purac JV 50,000 t/a 10 BASF-Purac JV Barcelona, Spain 25,000 t/a 2013 11 BioAmber-ARD Pomacle, France 3000 t/a 2012 12 BioAmber-Mitsui JV US or Brazil 65,000 t/a 13 BioAmber-Mitsui JV Sarnia, Ontario, Canada 17,000 Initially 34,000 finally 2013 14 BioAmber-Mitsui JV Thailand 65,000 t/a 2014

- 25. 25 15 Myriant Lake Providance, Louisiana 13,600 t/a 2013 16 Myriant-China National BlueStar Nanjing, China 1,10,000 t/a 17 Myriant Lake Providence, Louisiana 77,110 t/a 2014 18 Myriant-Uhde (owner and operator) Infraleuna site, Germany 500 t/a 2012 19 Reverdia (DSM-Roquette) Cassano Spinola, Italy 10,000 t/a 2012 Ref. ICIS, Company Reports Epichlorohydrin No. Company Based In Capacity Started In Investment 1 Dow Chemicals North America, USA 1000 t/a 2011 2 Solvay Europe FRA 100,000 t/a 2014 Asia China 3 Solvay Europe FRA 10,000 t/a 2010 Europe FRA 4 Solvay Europe FRA 100,000 t/a 2012 Asia THA 5 Yangnong Asia China 150,000 t/a 2011 Asia China Green Chemistry principles Principle 4 - Use renewable (biobased) feedstocks: Use raw materials and feedstocks that are renewable rather than depleting. Renewable feedstocks are often made from agricultural products or are the wastes of other processes; depleting feedstocks are made from fossil fuels (petroleum, natural gas, or coal) or are mined. Principle 12 - Design chemicals and products to degrade after use: Design chemical products to break down to innocuous substances after use so that they do not accumulate in the environment. Shift towards Biobased Chemicals and Products ―The Sustainable Biomaterials Collaborative‖ is a network of organizations working together to spur the introduction and use of biomaterials that are sustainable from cradle to cradle. The Collaborative seeks to advance the development and diffusion of sustainable biomaterials by creating sustainability guidelines, engaging markets, and promoting policy initiatives. The European Union has set a goal of agrofuels providing 5.75 percent of Europe's transport power by 2010 and 10 percent by 2020. US production of ethanol from corn and other crops continues to increase resulting in rising commodity prices. The International Food Policy Research Institute has estimated that the price of basic staples will increase 20 to 33 percent by 2010 and 26 to 135 percent by 2020. The demand for agricultural based energy supplies has resulted in the expansion of agrofuel monocultures. Agrofuels refer to large-scale industrial monoculture production of crops such as soy, oil palm, sugar cane, jatropha, canola etc. for fuels and do not include small scale,

- 26. 26 sustainably grown fuel crops that benefit local communities, do not employ genetically engineered (GE) varieties, and can be accurately referred to as "biofuels." Questions about Biobased Materials 1. Is the product useful to begin with? Is it needed? 2. Is the source of the biobased material sustainably grown, i.e., the biobased material was not treated with pesticides? 3. Is the land used for growing the biobased material needed for other uses, such as food production? 4. Is the manufacturing process clean and adaptable to local manufacturing expertise? 5. Are genetically engineered organisms used in the manufacturing process? 6. What additives are used in the final product? 7. Is there a composting component to the product development? What happens to the product after its use? Biobased Chemicals, Products and Producers Sr. No. Chemical End Product Key Companies 1 Butanol Solvents, Paints, Butyl rubber, PET, Fuels Gevo, Butamax (isobut), Cathay, MetEx, Cobalt (n-but) 2 Adipic acid Nylons, resins, Polyurethanes Verdezyne, Rennovia, BioAmber, Inventure, Genomatica 3 Succinic Acid C4 molecules, PBS, PBT, Solvents, de- icers BioAmber, Myriant, DSM/Roquette, BASF/Purrac 4 Butanediol (BDO) C4 molecules, PBS, PBT Genomatica, LanzaTech (2,3-BD), BioAmber 5 Butadiene Rubber, ABS Genomatica, Amyris, Global Bioenergies 6 Isoprene Rubber GlycosBio, AE Biofuels/Zymetis, Amyris, Genencor, Global Bioenergies 7 Propanediol (PDO) Fibers, Cosmetics, Polyurethanes, PBT DuPont, GlycosBio, Inventure, MetEx 8 Acrylic acid Coatings, Adhesives, Plastics OPX Biotechnologies, Itaconix, Novomer 9 Furans Polysters, Polyurethane, Fuels Avantium, Pennakem 10 Teraphtalic acid PET, Plasticizers Draths, Aventium, Gevo Bio-lubricants Petroleum based lubricants have been leading the industry since decades. However, these do not readily degrade and, therefore, pose an environmental hazard. Once used, their disposal becomes a challenge, the cost of properly disposing such material is high and improper disposal

- 27. 27 can create several health and environmental hazards. This creates need for biodegradable lubricants. Bio-lubricants are produced from natural oils and fats. In 2012, lubricants market is estimated at 38 million tonne (mt) out of which biolubricants account for approximately 3% share (1.2 mt). Conservative estimates reveal that the global lubricant market is expected to reach approximately 45 mt by 2020 out of which bio-lubricant will account for about 9% (4 mt) of the market. Some companies have already spotted this opportunity and working towards building a bio-lubricant based product portfolio, for example Cargill has developed an electrical insulation fluid based fully on soybean oil. Biopolymers Like bio-lubricants, biopolymers are substituting traditional petrochemicals based polymers due to their better bio-degradability. The market for bio-polymers is in its infancy and estimated at approximately 1.3 mt globally in 2012 as compared to the global polymer demand of 180 mt. It is expected to grow at a rate of 40% annually to reach about 20 mt by 2020 accounting for 7% of the global polymer market. This rapid penetration of biopolymers offers growth opportunity for companies. MNC‘s such as BASF, Solvay, DuPont, DSM and Lanxess as well as few small companies like EarthSoul and Harita have spotted this opportunity and are working towards building polymers based on vegetable oils or various cellulosic materials. Bio-based Surfactants Bio-based surfactants (surface-active molecules) are produced by microbial fermentation or enzyme-catalyzed reactions. Surfactants normally contain both hydrophobic and hydrophilic groups. In the case of bio-based surfactants, at least one of these groups is made from renewable resources. The bio-based hydrophobic group is usually made from coconut oil or palm kernel oil. A hydrophilic group is normally made from carbohydrates such as sorbitol, sucrose or glucose. The use of animal fat has significantly decreased. In contrast, the market for bio-based surfactants is expanding. Due to their good biodegradability and low to zero toxicity, they are used in specific applications by the paint, cosmetic, textile, agricultural, food and pharmaceutical industries. The mining and ore

- 28. 28 processing industry uses them as an emulsifier to facilitate oil production and for biological cleanup of contaminated sites. New age surfactants Methyl ether sulfonate (MES) is a biochemical based substitute for linear alkyl benzene sulfonate (LABS). Till now, the development of MES has been hindered by the lack of installed production capacity. MES has many benefits over LABS. MES has excellent characteristics such as high purity and active level, and is devoid of any volatile organic compound (VOC). It is also gentle on the skin, has low percent of di-salt, is white/near white in colour, and is suitable for both liquid and powder detergents. In 2011, Jiangsu Haiqing Biotechnology setup a 100,000 tonnes per year MES plant in China which is the largest plant of MES to go on stream. Such activities are further expected to drive growth of MES and it will potentially start replacing LABS at a rapid pace. The current LABS global market is estimated at about 3 mt and MES constitutes less than 1% of the same. It is expected that by 2020, MES will replace one third of LABS demand to reach 1.2 mt. Bio-based Solvents In a study carried out on behalf of the German Ministry of Economics and Technology (BMWi), the Fraunhofer Institute for Systems and Innovation Research (ISI) estimated that the global solvents market is in the region of 19.7 million MT per annum. At least 12.5 % of the total market volume could be produced from biomass, but the current figure is only 1.5 %. Solvents belong to the aromatic and aliphatic hydrocarbon, alcohol, ketone, ester, ether, glycol ether and halogenated hydrocarbon groups. Production of most solvents is based largely on fossil feedstock. Due to sustainability and environmental protection considerations, the spectrum is expected to shift towards bio-based solvents. The list of new bio-based solvents includes things like fatty acid methyl esters, which are also used in biodiesel, and esters of lactic acid with methanol (methyl lactate) or ethanol (ethyl lactate) as well as natural substances such as D-limonene which is obtained from the rind of citrus fruits. Another trend is to replace conventional organic solvents with biogenic solvents. Conversion of bio-based succinic acid or furfural (a byproduct of the cellulose industry) to tetrahydrofuran (THF) is one example.

- 29. 29 Biodiesel Biodiesel (methyl esters of various chain lengths) is one of the uses of bio based chemicals. Any change in government regulations and blending norms for biodiesel can significantly impact economics of bio based products. Increased requirement from biodiesel could push prices of oils higher thereby making them less attractive vis-à-vis petroleum feedstocks. However, this risk is largely mitigated due to a significant shift worldwide towards shale gas as the new and economically viable energy source. Continuous availability of feedstocks is a concern which remains at the top of the mind of companies operating in bio based chemicals. Historically, about 12% to 14% of the world‘s vegetable oil production has been used for bio based chemicals production. The emerging applications would require an additional approximately 8 mt of vegetable oil by 2020. Estimates show that this can be met with the increasing global vegetable oil production which is projected to increase from 150 mt in 2012 to 185 mt by 2020. Besides the above, companies are fast realising that there are other geographies around the world which offer climatic conditions suitable for palm oil plantations. Sierra Leone and Liberia form a major part of what is called the new frontier for palm oil production in West Africa. For example, Golden Veroleum plans to invest up to $1.6 billion in Sierra Leone and is eyeing over half a million hectares of land for palm plantations. Bio based chemicals offer a significant diversification opportunity for chemical companies. Asia is the preferred geography with a growing market and availability of feedstock. To capitalize on this opportunity, companies can explore partnerships/mergers with other companies which are integrated in related feedstocks or think about integrating forward/backward themselves. Companies can also plan to establish their footprint in new geographies which could provide them a first mover advantage and position them as a strong integrated player. Purac produces - via its fermentation processes - a wide range of products which are mostly 100% biobased. These products can be used in many different applications, such as home & personal care, animal health, coatings and inks, (agro)chemicals and offer the opportunity to improve the carbon footprint of industrial and consumer products to consequently obtain more sustainable products. Purac is also actively working on the the development of processes to replace agricultural feedstocks with cellulosic feedstocks, so called 2nd generation biomass, in order to not interfere with the food value chain.

- 30. 30 Stage of Bio-based Chemicals Commercial Success (Intermediates) Coming Soon (Drop-In Intermediates) Under Development (New Feedstock) 1,3 PDO DuPont Tate & Lyle ferments corn sugar to produce 1,3 PDO in Loudon, Tenn. Reports of glycerol- based PDO in China BENZENE, TOLUENE, XYLENE (BTX) Anellotech‘s Bio-BTX, Virent‘s BioFormPX Paraxylene from Gevo‘s isobutanol 2,5 FDCA (Furan Dicarboxylic Acid) FDCA + MEG = Polyethylene Furanoate (PEF) as alternative to PET Nylons and Aramids using adipic acid can be reformulated with FDCA BUTANOL Corn-based n-butanol already produced in China - Cathay Industrial Biotech, Laihe Rockley, small firms Gevo started corn-based isobutanol shipments this year ADIPIC ACID Verdezyne, Rennovia, DSM, Genomatica, BioAmber Carbon Monoxide / Carbon Dioxide CO2 + Propylene Oxide = Polypropylene carbonate (PPC) CO2 + Ethylene Oxide = Polyethylene carbonate (PEC) CO2 Polyether Polycarbonate Polyols (PPP) CO + Ethylene Oxide = Propiolactone CO/CO2 C2-C5 products (via GTL and fermentation) SUCCINIC ACID Reverdia and Myriant plants running, BioAmber and Succinity to follow early 2014 ACRYLIC ACID OPX Biotechnologies/Dow Chemical, Myriant, Novozyme/Cargill/BASF, ADM, Novomer, Metabolix Levulinic Acid LA β-acetacrylic acid = New acrylate polymers LA Diphenolic acid = Replacement for Bisphenol-A LA 1,4-pentanediol = New polyesters LA–derived lactones for solvents application GLYCOLS ADM, Oleon producing PG using glycerol (and sorbitol for ADM) as feedstock. HK-based Global Bio-Chem produces PG using corn glucose Greencol Taiwan, India Glycols producing bioMEG from sugarcane- based ethanol BUTANEDIOL Genomatica, Myriant, BioAmber, LanzaTech EPICHLOROHYDRIN Vinythai produces glycerol-based ECH in RUBBER FEEDSTOCK – BUTADIENE, ISOPRENE, ISOBUTENE

- 31. 31 Thailand, plans another 100KTY facility in China Reports of Chinese plans for bio-ECH Butadiene – Amyris/Kuraray, LanzaTech/Invista, Versalis/Genomatica, Global Bioenergies/Synthos, Cobalt Biotechnologies Isoprene – Amyris/Michelin, Ajinomoto/Bridgestone, DuPont/Goodyear, Aemetis, Glycos Biotechnologies Isobutylene - Global Bioenergies/LanzaTech, Gevo/Lanxess FARNESENE Start of Amyris‘ 50m liters/year sugarcanebased fermentation plant in Brazil this year Building block for lubricants, base oil, isoprene, squalene, F&F ingredients POLYAMIDES Brand owners such as Nike, Puma, Gucci are using castor oil-based PA10 and PA11 Bio-based PA producers include Arkema, Evonik, BASF, Solvay, DSM, Radici Group, DuPont, EMS-Chemie Commercial Success (Biopolymers) (2011 Status – Global Bioplatic Production Capacity) Bio-based / Non-biodegradable (58.10%) Biodegradable (41.90%) Bio-PA (1.6%) PLA (16.1%) Bio-PE (17.2%) PHA (1.6%) Bio-PET 30 (38.9%) Biodegradable Polysters (10%) Others (0.4%) Biodegradable Starch Blends (11.3%) Regenerated Cellulose (2.4%) Others (05%) Source: European Bioplastics, Institute for Bioplastics and Biocomposites (Oct. 2012)

- 32. 32 Recent Large Projects from bio-based feedstocks 1. DuPont Bio-PDO (SeronaR ) – fermented product is 1,3 Propane diol – 45 KTA plant - Key processes are fermentation, condensation, polymerization – Initial product is PDO/TPO copolymer 2. NatureWorksTM - PLA – fermented product is lactic acid – 140 KTA plant – Key processes are fermentation, Oligomerization, ring closing and ring opening, Polymerization – Initial product is Polylactic acid 3. Braskem – Polyethylene – fermented product is ethanol - 200 KTA plant – Key processes are fermentation, dehydration, polymerization – Initial product is Ethylene, Polyethylene copolymers 4. Archer Daniel Midland (ADM) – Propylene Glycol Plant 5. Arkema – High performance polyamides 6. Solvay Indupa (Brazil) – Polyvinyl Chloride The bio feedstock platform for the production of bio products is mainly focused on the following chemical functionalities. Vegetable oil/fatty acid esters of glycerol Vegetable oils and fats provide useful chemical functionalities such as unsaturation and ester groups for further modifications using conventional schemes such as hydrogenation, selective oxidation, epoxidation, meta thesis reaction and others to introduce functionality of value in diverse applications such as plasticizers, coatings, adhesives, polymers, composites, etc. Several bio products such as bioplasticizers for PVC, bio toners, biopolyols based on this approach have been commercialized recently. Sugar-based platform Platforms based on sugars have been deployed to create acids such as succinic acid and convert the acid to high value chemicals such as 2- pyrrolidone, 1, 4 butane diol, tetra hydrofuran and others. More recently cellulosic feedstock has been converted to 5-hydroxymethyl furfural (HMF) using some novel catalysts and ionic liquids as platform chemical to make a variety a high value chemicals derived from petroleum sources Cellulosic Platform Various building block molecules such as 5-hydroxymethylfurfural (HMF), derived from cellulosic biomass, can be converted into many types of value added chemicals now obtained from petroleum sources. Startup companies such as Segetis are developing novel chemicals based on levulinic acid for use as replacement solvents and plasticizers. Roquette has been actively pursuing commercial

- 33. 33 scale production of isosorbide from sugar feedstock useful in the development of bioplasticizers and bisphenol free polycarobonate resins. Glycerine Platform Bio products are derived from crude glycerine, a co-product of biodiesel production. Challenges for Bio-based Chemicals Industry 1. Availability of crude oil and their price 2. Concern that food security can be impacted 3. Concern about destroying forest 4. Transition from petro to bio not smooth in the beginning 5. Technological challenges 6. Investments required for scaleup and downstream processing 7. Feedstock availability 8. Using cellulosic biomass and agricultural wastes as raw material 9. The technology for converting biomass to chemicals is being developed in US and Europe, but the biomass is in South East Asia and in Latin America 10. Market pull is there but capital investments (risk averse) are difficult 11. Price competition of biorefinaries with petrorefinary 12. Partnering with feedstock producers and technology possessors is pivotal

- 34. 34 Chapter 2 Worldwide Scenario of Biobased Chemicals 2.1 Key Drivers for Bio-based Economy 2.2 Where bio-based chemicals are produced? 2.3 Key Drivers Affecting Bio-based Chemicals Market 2.4 Biobased Chemicals in US 2.5 Biobased Chemicals in Europe 2.6 Biobased Chemicals in Asia 2.7 Biobased Chemicals in Japan 2.8 Biobased chemicals in China 2.9 Biobased chemicals in Canada 2.10 Biobased Chemicals in Malaysia 2.11 Bio-based Chemicals in North America 2.12 Biobased Chemicals Companies in 2013 Key Drivers for Bio-based Economy Oil age will end. Oil will be very expensive as it will run out (Every single day world uses 100 million barrels of oil) Carbon emissions are expected to increase by 88% by 2030 Global population will reach 9 billion by 2040-2050. Energy and food needs will grow exponentially. Bio-based chemical investments are driven by raw material availability, price and cost of production, but other factors such as political and financial support play an important role when the first large-scale facility is decided. China, Brazil, Thailand and the US are clear winners in the game. Shale gas has had and will continue to have a direct and indirect impact on bio-based chemical investments. Where bio-based chemicals are produced? Total market for bio-based chemicals is $12 billion. Production share of different countries of this market in 2013 was as follows. U. S. 15.4% China 12.2% Argentina 07.8%

- 35. 35 Brazil 06.5% Indonesia 09.0% Malaysia 08.0% Thailand 04.0% France 04.7% Germany 07.3% Netherlands 06.8% Other Europe 10.0% Key Drivers Affecting Bio-based Chemicals Market Moving away from petroleum dependency Increased Consumer environmental responsibility Movement towards sustainability by manufacturers These drivers result in policies and regulations supporting adoption of bio-based chemicals. Over 70% consumers equate ―Green‖ with products made from natural or organic ingredients. 44% Senior executives of organizations believe that sustainability is critical to success. (Ref. Norman Deschamps Presentation for ―Meet the Expert Series‖) According to Lux Research, a Boston based company global bio-based capacity in 2017 will be 13.2 million tonnes. North America‘s share will decrease from 15% to 13%, whereas Asia‘s will increase from 52% to 55% and South America‘s from 13% to 18%. Biobased Chemicals in US The US chemicals and plastics industry was in the forefront for four decades from World War II. Historically, the U.S. chemicals and plastics industry was the envy of the world. At its peak in the 1950s, the industry was responsible for over 5 million U.S. jobs and a $20 billion positive trade balance for the United States. Jobs associated with the industry were typically among the highest paid in U.S. manufacturing. Over the last two decades, competitive advantage for chemicals and plastics manufacturing has shifted towards the Middle East and Asia, as has the industry. U.S. employment in the sector has dropped over the last decade and is projected to shrink further as capital investment for the petroleum-based industry has essentially shifted away from the United States. Biobased chemicals and plastics represent a historic opportunity to reverse these trends through the creation of a new generation of renewable, sustainable products developed and produced in the United States. As production of chemicals and plastics moved to other countries

- 36. 36 after 1980 this chemicals industry eroded in US. The number of jobs in the sector is indicator of this. The nascent biobased products industry employed over 5,700 Americans at 159 facilities in 2007. Presently, less than 4 percent of U.S. chemicals sales are biobased. But a recent USDA analysis puts the potential market share in excess of 20 percent by 2025 with adequate federal policy support. Conditions favourable for US to lead again in Biobased products as alternative to petroleum based products are – Leading position in industrial biotechnology, strong agriculturable base with large arable land, largest chemicals and plastics market, downstream industry for biobased products (e.g., converting, logistics, warehousing) is already in place The global chemical industry produced approximately US$1.9 trillion worth of products through conventional petrochemical-based processes using more than 2 billion barrels of crude oil in 2005. The processes are energy intensive and environmentally unfriendly emitting about 1.5 billion tons of CO2. The industrial chemical business in USA is $340 billions. In the US, 5% of each barrel of oil goes to petrochemicals, whereas 70% goes for the transportation fuels. The US chemical industry contributes greatly to the US economy. It contributes $720 billion to US economy which is 5% of GDP. Out of this $170 billion is in exports. However global share of USA in chemical market has come down from 27% in 1999 to 19% in 2009. Bio-based chemical production is suitable for exploiting America‘s strong agriculture and forestry infrastructure. The global interest in bio-based chemicals and products is developing at pace. Current research indicates that the green chemical industry market will reach $98.5 billion by 2020 (Pike research). To foster growth of the biobased products sector in the United States, federal policy should provide strong support for research, development and commercialization of innovative biobased products, including grants and loans for construction of biorefineries, a strong biobased markets program, and tax incentives for pioneering commercial production. President Obama has declared ―Bio-economy‖ as major engine for American innovation and economic growth. Biobased Chemicals in Europe In 2004, global chemical production amounted to 1736 billion. European Union (EU) accounted for more than one third of this at 580 billion. EU was ahead of USA and Asia. Europe is losing