No tds

•

0 gostou•37,561 visualizações

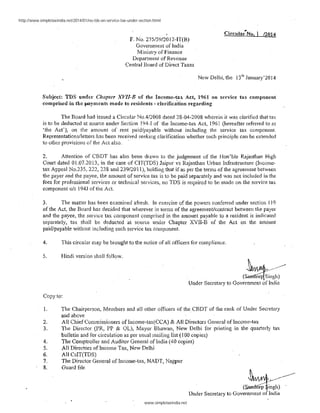

Service tax collected by a person is not subject to tax deduction at source under Section 194J of the Income Tax Act. The Central Board of Direct Taxes clarified that service tax collected by a service provider and paid to the government does not constitute income in the hands of the service provider. Therefore, service tax collected by a service provider need not be considered for the purposes of TDS under Section 194J of the Income Tax Act.