Notas de Administração financeira - noite, 2016.1

•

0 gostou•10,981 visualizações

http://financasaplicadasbrasil.blogspot.com/2016/11/notas-de-administracao-financeira-20161.html

Recomendados

Recomendados

Mais conteúdo relacionado

Mais de Felipe Pontes

Mais de Felipe Pontes (20)

Último

Último (20)

Notas de Administração financeira - noite, 2016.1

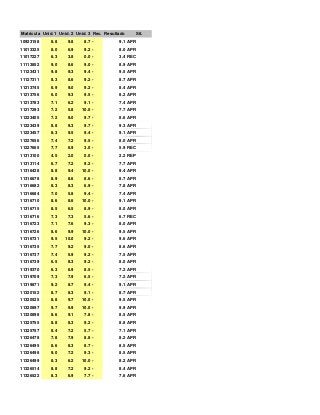

- 1. Matrícula Unid. 1 Unid. 2 Unid. 3 Rec. Resultado Sit. 10923158 8.8 9.8 8.7 - 9.1 APR 11013325 8.0 6.9 9.2 - 8.0 APR 11017227 6.3 3.8 0.0 - 3.4 REC 11113852 9.0 8.6 9.0 - 8.9 APR 11123431 9.8 9.3 9.4 - 9.5 APR 11127311 8.3 8.6 9.2 - 8.7 APR 11213745 6.9 9.0 9.2 - 8.4 APR 11213756 6.0 9.3 9.5 - 8.2 APR 11213783 7.1 6.2 9.1 - 7.4 APR 11217293 7.2 5.8 10.0 - 7.7 APR 11223405 7.2 9.0 9.7 - 8.6 APR 11223439 8.8 9.3 9.7 - 9.3 APR 11223457 8.3 9.5 9.4 - 9.1 APR 11227656 7.4 7.2 9.5 - 8.0 APR 11227665 7.7 6.9 3.0 - 5.9 REC 11313100 4.5 2.0 0.0 - 2.2 REP 11313114 6.7 7.2 9.2 - 7.7 APR 11316428 8.8 9.4 10.0 - 9.4 APR 11316678 8.9 8.6 8.6 - 8.7 APR 11316682 8.3 8.3 6.9 - 7.8 APR 11316684 7.0 5.8 9.4 - 7.4 APR 11316710 8.6 8.6 10.0 - 9.1 APR 11316715 8.5 6.5 8.9 - 8.0 APR 11316716 7.3 7.3 5.6 - 6.7 REC 11316723 7.1 7.6 9.3 - 8.0 APR 11316726 8.6 9.9 10.0 - 9.5 APR 11316731 9.5 10.0 9.2 - 9.6 APR 11316735 7.7 9.2 9.0 - 8.6 APR 11316737 7.4 5.9 9.2 - 7.5 APR 11316739 6.5 8.3 9.2 - 8.0 APR 11319370 6.3 6.9 8.5 - 7.2 APR 11319709 7.3 7.9 6.5 - 7.2 APR 11319871 9.2 8.7 9.4 - 9.1 APR 11320152 8.7 8.3 9.1 - 8.7 APR 11320525 8.8 9.7 10.0 - 9.5 APR 11320897 9.7 9.9 10.0 - 9.9 APR 11320898 8.6 9.1 7.8 - 8.5 APR 11325755 8.8 8.3 9.2 - 8.8 APR 11325757 8.4 7.2 5.7 - 7.1 APR 11326478 7.8 7.9 8.8 - 8.2 APR 11326495 8.6 8.3 8.7 - 8.5 APR 11326498 9.0 7.2 9.3 - 8.5 APR 11326499 8.3 6.2 10.0 - 8.2 APR 11326514 8.8 7.2 9.2 - 8.4 APR 11326522 8.3 6.9 7.7 - 7.6 APR

- 2. 11326525 7.3 8.3 7.8 - 7.8 APR 11327561 9.8 8.3 9.4 - 9.2 APR 11327577 9.6 8.6 8.5 - 8.9 APR 11329060 7.5 7.9 8.3 - 7.9 APR 11329067 8.0 8.3 9.2 - 8.5 APR 11329888 8.4 6.9 8.9 - 8.1 APR 11403283 8.3 7.9 7.8 - 8.0 APR