Social networks lead activity as Digital Sky invests in Facebook

•

1 gostou•635 visualizações

- The month of May saw the highest level of financing activity in over 12 months, totaling $327.1 million across 20 financings. This was buoyed by a $200 million investment by Digital Sky Technologies in Facebook. - Excluding the Facebook transaction, May would have seen the lowest financing total for 2009 at $127.1 million. Ad networks saw the highest level of activity over the last three months. - The report analyzes 93 public web 2.0 companies with a total market cap of around $53 billion. On average, companies have $577 million in market cap and $152 million in revenue.

Recomendados

Recomendados

Mais conteúdo relacionado

Semelhante a Social networks lead activity as Digital Sky invests in Facebook

Semelhante a Social networks lead activity as Digital Sky invests in Facebook (20)

Mais de David Shore

Mais de David Shore (20)

Último

Último (20)

Social networks lead activity as Digital Sky invests in Facebook

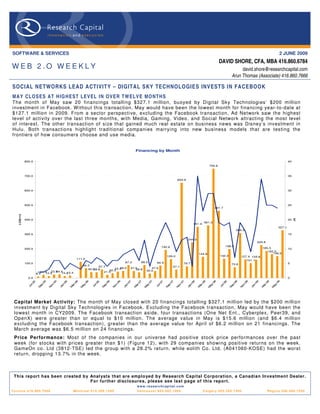

- 1. SOFTWARE & SERVICES 2 JUNE 2009 DAVID SHORE, CFA, MBA 416.860.6784 WEB 2.O WEEKLY david.shore@researchcapital.com Arun Thomas (Associate) 416.860.7666 SOCIAL NETWORKS LEAD ACTIVITY – DIGITAL SKY TECHNOLOGIES INVESTS IN FACEBOOK MA Y CL O S E S AT H IG H E S T L E V EL I N OV E R T W EL V E MO NT H S The month of May saw 20 financings totalling $327.1 million, buoyed by Digital Sky Technologies’ $200 million investment in Facebook. W ithout this transaction, May would have been the lowest month for financing year-to-date at $127.1 million in 2009. From a sector perspective, excluding the Facebook transaction, Ad Network saw the highest level of activity over the last three months, with Media, Gaming, Video, and Social Network attracting the most level of interest. The other transaction of size that gained much real estate on business news was Disney’s investment in Hulu. Both transactions highlight traditional companies marrying into new business models that are testing the frontiers of how consumers choose and use media. Financing by Month 800.0 40 750.6 700.0 35 653.9 600.0 30 500.0 25 461.7 (U $m ) S m (#) 400.0 20 361.3 351.4 327.1 308.3 300.0 15 244.0 225.8 192.6 198.0 200.0 185.5 10 162.5 144.9 149.5 129.0 132.3 127.4 125.6 111.0 101.1 100.0 87.3 88.5 84.9 79.7 5 66.3 73.6 57.7 57.1 40.5 48.0 43.4 47.5 47.6 38.8 32.3 38.8 21.4 24.4 23.9 21.5 30.0 9.4 12.5 15.4 13.2 0.0 0 6 7 8 9 5 5 6 6 6 7 7 7 8 8 8 9 06 07 08 09 5 6 7 8 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 -0 l-0 l-0 l-0 l-0 n- n- n- n- ov ay ov ay ov ay ov ay ep ep ep ep ar ar ar ar Ju Ju Ju Ju Ja Ja Ja Ja M M M M M M M M N N N N S S S S Capital Market Activity: The month of May closed with 20 financings totalling $327.1 million led by the $200 million investment by Digital Sky Technologies in Facebook. Excluding the Facebook transaction, May would have been the lowest month in CY2009. The Facebook transaction aside, four transactions (One Net Ent., Cyberplex, Peer39, and OpenX) were greater than or equal to $10 million. The average value in May is $15.6 million (and $6.4 million excluding the Facebook transaction), greater than the average value for April of $6.2 million on 21 financings. The March average was $6.5 million on 24 financings. Price Performance: Most of the companies in our universe had positive stock price performances over the past week (for stocks with prices greater than $1) (Figure 12), with 29 companies showing positive returns on the week. GameOn co. Ltd (3812-TSE) led the group with a 28.2% return, while eolith Co. Ltd. (A041060-KOSE) had the worst return, dropping 13.7% in the week. This report has been created b y Anal ysts that are emplo yed b y Research Capital Corporation, a Canadian Investment Dealer. For further disclosures, please see last page of this report. w w w . r e s e a rc h c a p i t a l . c o m T o ro n t o 4 1 6 . 8 6 0 . 7 6 0 0 Montreal 514.399.1500 Vancouver 604.662.1800 Calgary 403.265.7400 Regina 306.566.7550

- 2. Page 2 THE WEB 2.0 UNIVERSE Ninety-three public Web 2.0 companies identified: Our W eb 2.0 universe contains 93 companies, with a combined market cap of ~$53 billion (Figure 1). The average market cap for the group is ~$577 million (but a median of only $50.9 million), with average trailing revenue of $152.1 million (median $54.3 million). The companies are also generally profitable, with a median EBITDA margin of 14.2%. On a valuation basis, the overall average is 4.9x trailing revenue (median 2.0x) and 10.0x trailing EBITDA (median 9.6x). Fourteen of the companies have more than 500 employees. C omparable C o mpany A nalys is > W eb 2.0 Trading Current U S D Market U S D LT M To tal US D L TM T otal E BITDA TE V/LT M T E V/LT M C om pan y Nam e L TM as of T icker E xc hange Cu rrency H Q P rice C ap ($m) R ev ($m) E B ITDA ($m) % R evenu e E B IT DA E mployees Acce le rize N ew Me dia, Inc. 3 /31 /200 9 AC LZ OT C B B USD U nited S ta tes 0 .35 9 .7 4.1 (4 .4) NM 3.5 x - 11 Actoz S of t C o., L td. 3 /31 /200 9 A0 527 90 K OS E KR W S outh K orea 26, 300 18 2.2 93. 7 2 0.4 21 .7% 1.6 x 7.5x NA AQ Inte ractive , Inc. 1 2/31 /200 8 38 38 TSE JPY J apan 80 ,000 .00 4 5.0 62. 4 5 .0 8 .0% 0.2 x 3.0x NA As s o cia ted Media H oldings Inc. 6 /30 /200 7 AS MH OT C P K USD U nited S ta tes 0 0 .1 0.1 (2 .3) NM 8.1 x - 3 B igstring Co rp. 3 /31 /200 9 BS GC OT C B B USD U nited S ta tes 0 .02 1 .0 0.1 (2 .0) NM 30.7 x - 4 B e tawave Corpora tion 3 /31 /200 9 B W AV OT C B B USD U nited S ta tes 0 2 .3 8.4 (1 2.6) NM - - 53 B e yo nd Commerce, In c. 3 /31 /200 9 B Y OC OT C B B USD U nited S ta tes 1 .01 4 4.8 7.1 (9 .5) NM 7.0 x - 69 B right T hings plc 9 /30 /200 8 AIM:B G T AIM GBP U nited K ingdom 0 4 .8 0.3 (1 .9) NM 17.6 x - 9 B roa dW ebAs ia Inc. 9 /30 /200 8 BW BA OT C P K USD U nited S ta tes 0 .30 2 5.3 0.0 (4 .6) NM - - 46 C DC C orp. 3 /31 /200 9 C HIN .A N as da qG S USD H ong K on g 2 18 0.4 389 .9 3 0.8 7 .9% 0.5 x 6.3x NA C ha ngyou. com Limite d 3 /31 /200 9 C Y OU N as da qG S USD C hina 35 .77 1,9 67.4 222 .5 13 5.1 60 .7% 8.0 x 1 3.2 x 628 C hina G ate wa y C orpo ra tion 9 /30 /200 8 C GW Y OT C P K USD U nited S ta tes 0 0 .0 6.7 (6 .6) -9 8.9% 0.0 x - 37 C hine s e G amer International 3 /31 /200 9 G T S M:308 3 GTSM TWD T aiwan 376 .50 98 0.3 57. 2 3 2.0 56 .0% 16.0 x 2 8.5 x NA C ornerW orld C orporation 1 /31 /200 9 C WR L OT C B B USD U nited S ta tes 0 5 .8 1.3 NM NM 5.5 x - NA C yberplex Inc. 3 /31 /200 9 T S X:C X TSX C AD C ana da 1 .57 7 7.4 74. 9 7 .7 10 .3% 1.0 x 9.5x NA DADA S pA 9 /30 /200 8 C M:D A CM EUR Ita ly 6 13 6.7 240 .4 3 8.4 16 .0% 0.8 x 4.9x 578 DXN Holdings B hd 2 /28 /200 9 DXN KLSE MY R Ma la ys ia 0 .40 2 6.2 79. 7 1 0.9 13 .7% 0.5 x 3.9x NA Dibz Inte rnational, Inc. NA DIB Z OT C P K USD U nited S ta tes 0 0 .0 NA NM NM - - NA DigitalP ost Inte ra ctive , Inc. 3 /31 /200 9 DG LP OT C B B USD U nited S ta tes 0 .02 1 .1 0.7 (2 .6) NM 3.8 x - 7 DigitalT own, In c. 2 /28 /200 9 DG T W OT C B B USD U nited S ta tes 2 5 4.2 NM (3 .0) NM - - 3 Dolphin D igital Me dia, Inc. 3 /31 /200 9 DP DM OT C B B USD U nited S ta tes 0 .53 2 7.4 0.8 (3 .7) NM 36.7 x - NA E o lith C o. L td. 1 2/31 /200 8 A0 410 60 K OS E KR W S outh K orea 725 4 2.8 14. 9 (3 .5) -2 3.6% 3.0 x - NA E xte ns ions , Inc. 3 /31 /200 9 E XT I OT C P K USD U nited S ta tes 0 .15 1 4.2 NM NM NM - - 2 F inancia l Media G roup, Inc. 2 /28 /200 9 F NG P OT C B B USD U nited S ta tes 0 0 .2 7.2 2 .4 34 .1% - - 22 F luid Mus ic Ca nada, In c. 3 /31 /200 9 T S X:F MN TSX C AD U nited S ta tes 0 .75 3 6.2 5.0 (6 .9) NM 5.2 x - NA F rogs te r Interactive P ictu re s AG 6 /30 /200 8 FRG XT R A EUR G ermany 7 2 4.8 5.7 (3 .5) -6 0.6% 4.3 x - NA G a ma nia Digital E ntertainmen t C o., L td. 3 /31 /200 9 61 80 GTSM TWD T aiwan 58 .60 27 5.6 128 .3 2 1.3 16 .6% 2.0 x 1 1.8 x NA G a me On C o L td. 3 /31 /200 9 38 12 TSE JPY J apan 1 24, 000 12 4.0 76. 1 1 8.0 23 .7% 0.8 x 3.5x NA G e oS e ntric O yj 3 /31 /200 9 G E O1 V H LS E EUR F inland 0 .05 6 3.7 6.0 (1 5.5) NM 9.9 x - 108 G ian t Intera ctive G roup, Inc. 3 /31 /200 9 GA NYS E USD C hina 8 1,7 86.7 219 .1 NM NM - - NA G iga Media Ltd. 1 2/31 /200 8 G IG M N as da qG S USD T aiwan 6 .19 33 4.4 190 .4 4 6.0 24 .2% 1.4 x 5.6x NA G ravity C o., L td 9 /30 /200 8 GR VY N as da qG M USD S outh K orea 1 3 0.6 39. 7 7 .6 19 .2% - - 636 G ree, Inc. 6 /30 /200 8 T S E : 363 2 TSE JPY J apan 5 ,630 .00 1,3 00.4 30. 4 1 0.9 36 .0% 40.1 x - NA G u ngH o O nline E ntertainment, Inc. 1 2/31 /200 8 37 65 OS E JPY J apan 2 48, 000 29 3.8 116 .3 2 0.7 17 .8% 2.3 x 1 3.1 x NA H anbitS of t, Inc. 3 /31 /200 9 A0 470 80 K OS E KR W S outh K orea 5 ,290 .00 9 4.0 56. 0 (1 5.0) -2 6.8% 1.4 x - NA IAC /InterActiveC orp. 3 /31 /200 9 IAC I N as da qG S USD U nited S ta tes 17 2,5 00.7 1 ,40 6.4 4 2.6 3 .0% 0.4 x 1 4.4 x 3 ,20 0 IAS E n ergy, Inc. 1 /31 /200 9 IAS C.A OT C B B USD C ana da 0 .23 1 6.1 0.0 (0 .8) NM - - NA is ee media Inc. 1 2/31 /200 8 IE E T S XV C AD C ana da 0 3 .8 1.4 (5 .5) NM 1.4 x - NA J umbuck E ntertainment P ty Ltd. 1 2/31 /200 8 AS X:J MB AS X AU D Aus tra lia 0 .45 1 8.0 14. 5 5 .4 37 .2% 0.9 x 2.4x 72 J umpT V Inc. 1 2/31 /200 8 T S X:J T V TSX C AD C ana da 1 8 3.7 13. 4 (8 .4) -6 2.6% 4.7 x - 237 K a boos e Inc. 3 /31 /200 9 T S X:K AB TSX C AD C ana da 0 .61 7 8.5 75. 7 9 .0 11 .9% 1.1 x 9.3x NA K ings oft Co. Ltd. 3 /31 /200 9 38 88 S E HK HKD C hina 5 73 1.5 129 .2 5 2.0 40 .3% 5.2 x 1 2.9 x 2 ,27 1 Lin go M edia Corporation 1 2/31 /200 8 T S XV : LM T S XV C AD C ana da 1 .05 1 2.4 0.9 (1 .5) NM 11.6 x - NA Live Wo rld Inc. 3 /31 /200 9 LV WD OT C P K USD U nited S ta tes 0 2 .6 11. 4 (0 .0) -0 .4% 0.1 x - NA Lo okS mart, Ltd. 3 /31 /200 9 LOOK N as da qG M USD U nited S ta tes 1 .30 2 2.2 60. 7 (3 .8) -6 .3% - - 90 Magnitu de Information S ys tems Inc. 3 /31 /200 9 MA G Y OT C B B USD U nited S ta tes 0 6 .8 0.1 (3 .1) NM - - 14 Mixi, In c. 3 /31 /200 9 21 21 TSE JPY J apan 458 ,000 .00 72 8.2 124 .7 4 4.2 35 .4% 4.9 x 1 3.8 x NA Mode rn Times G rou p Mtg AB 3 /31 /200 9 MT G B OM S EK S weden 233 2,0 68.2 1 ,81 7.2 27 8.4 15 .3% 1.5 x 9.5x 2 ,96 9 Moggle , Inc 3 /31 /200 9 MMOG OT C B B USD U nited S ta tes 2 .30 8 3.5 NM NM NM - - 3 MOK O.mobi L imited 1 2/31 /200 8 MK B AS X AU D Aus tra lia 0 4 .6 1.2 (2 .4) NM 3.0 x - NA Myriad G rou p AG 1 2/31 /200 8 MY R N SWX C HF S witzerla nd 5 .75 11 4.5 40. 0 0 .8 1 .9% 3.1 x - 405 N E OW IZ G ames C orpora tion 1 2/31 /200 8 A0 956 60 K OS E KR W S outh K orea 77, 100 60 2.0 200 .9 5 3.9 26 .8% 2.9 x 1 1.0 x NA N etD rago n W ebS oft, Inc. 3 /31 /200 9 77 7 S E HK HKD C hina 5 .42 36 9.6 87. 0 3 4.4 39 .5% 2.7 x 6.8x 2 ,42 6 N ete as e.com I nc. 3 /31 /200 9 NT E S N as da qG S USD C hina 36 4,4 06.5 470 .9 30 6.0 65 .0% - - NA N eXplo re Co rpora tion 9 /30 /200 7 N XP C OT C P K USD U nited S ta tes 0 .70 3 9.0 NM (4 .9) NM - - 19 N gi G roup Inc. 1 2/31 /200 8 24 97 TSE JPY J apan 34, 700 4 4.3 101 .7 3 1.3 30 .8% - - NA N orthgate Te chno lo gies L imited 3 /31 /200 9 59 005 7 BS E INR India 47 .05 3 5.0 119 .4 (2 8.0) -2 3.5% 0.3 x - NA Open T e xt Corp. 3 /31 /200 9 OT E X N as da qG S USD C ana da 36 1,8 77.1 782 .6 19 9.2 25 .5% 2.5 x 9.8x 3 ,40 0 Openwave S ys tems Inc. 3 /31 /200 9 OP W V N as da qG S USD U nited S ta tes 1 .86 15 4.5 197 .2 (2 .1) -1 .0% 0.3 x - 630 P e rf ect W orld C o., Ltd. 3 /31 /200 9 PW R D N as da qG S USD C hina 23 1,1 89.7 228 .3 12 4.7 54 .6% 0.1 x 0.1x NA P h otoChann el N etwork s Inc. 3 /31 /200 9 T S XV : P N T S XV C AD C ana da 1 .54 4 8.5 19. 9 0 .5 2 .3% 2.4 x - NA Qu epa s a C orp. 3 /31 /200 9 QP S A N as da qC M USD U nited S ta tes 1 1 3.0 0.1 (1 0.8) NM - - 74 OA O R B C Information S ys tems 1 2/31 /200 7 R BCI R TS USD R us s ia 1 .35 18 7.3 154 .7 2 0.2 13 .1% 0.0 x 0.3x NA S h anda In teractive E ntertainme nt L td. 1 2/31 /200 8 S N DA N as da qG S USD C hina 60 4,1 78.9 522 .6 24 0.1 46 .0% 0.4 x 0.8x NA S h utte rf ly, In c. 3 /31 /200 9 S F LY N as da qG S USD U nited S ta tes 15 .13 38 0.9 215 .2 2 8.3 13 .2% 1.5 x 1 1.1 x 514 S K C ommun ications Co., Ltd. 1 2/31 /200 8 A0 662 70 K OS E KR W S outh K orea 12, 000 40 0.2 186 .7 1 2.1 6 .5% 2.1 x 3 3.0 x NA S N AP Inte ra ctive , Inc. 3 /31 /200 9 S T VI OT C B B USD U nited S ta tes 0 .79 8 .5 3.3 0 .9 28 .0% 2.2 x 7.7x 11 S N M G lobal H oldings 9 /30 /200 8 S N MN OT C P K USD U nited S ta tes 0 0 .0 2.0 (0 .7) -3 4.8% 1.1 x - 33 S o cia l Media V e nures , In c. 1 2/31 /200 8 S MV I OT C P K USD U nited S ta tes 0 .01 0 .0 0.1 (0 .1) -6 0.5% 0.0 x - NA S o cia lwis e, Inc. 3 /31 /200 9 S C LW OT C B B USD U nited S ta tes 1 3 0.3 0.0 (4 .8) NM - - NA S o hu. com Inc. 3 /31 /200 9 S OH U N as da qG S USD C hina 66 .25 2,5 35.0 460 .0 20 0.5 43 .6% 4.7 x 1 0.8 x 3 ,19 7 S ite s earch C orpo ration 1 /31 /200 9 S T PC OT C B B USD U nited S ta tes 3 2 8.2 NM (1 .1) NM - - 15 S park N etworks , Inc. 3 /31 /200 9 LOV AME X USD U nited S ta tes 2 .29 4 7.1 54. 3 1 1.8 21 .7% 0.9 x 4.0x 183 S pectrumDN A, Inc. 3 /31 /200 9 S P XA OT C B B USD U nited S ta tes 0 1 8.0 0.1 (2 .6) NM - - 7 T encent Holdin gs L td. 3 /31 /200 9 70 0 S E HK HKD C hina 85 .60 19,9 07. 1 1 ,20 4.5 57 7.1 47 .9% 18.0 x 3 7.5 x 6 ,19 4 T he P aren t C ompan y 8/2/2008 K IDS .Q OT C P K USD U nited S ta tes 0 0 .4 112 .0 (1 3.5) -1 2.0% 0.2 x - 347 T he 9 L imited 1 2/31 /200 8 N CT Y N as da qG S USD C hina 9 .27 24 8.6 250 .1 8 4.2 33 .7% - - NA T he S treet.com, Inc. 3 /31 /200 9 TSCM N as da qG M USD U nited S ta tes 2 6 0.0 67. 0 1 .9 2 .9% - - 310 T otal S po rt Online A S 3 /31 /200 6 T OS O OT C NO NOK N orwa y 0 .03 0 .1 2.2 (1 .1) -5 0.6% 4.6 x - 16 T ree.C om, Inc. 3 /31 /200 9 TR EE N as da qG M USD U nited S ta tes 11 11 5.8 215 .6 (1 3.3) -6 .2% 0.5 x - 700 U nis erve C ommu nication s Co rp. 2 /28 /200 9 T S XV : US S T S XV C AD C ana da 0 .06 1 .2 24. 0 0 .1 0 .2% 0.2 x - NA U nited Online Inc. 3 /31 /200 9 U NT D N as da qG S USD U nited S ta tes 7 58 1.7 811 .2 17 7.3 21 .9% 1.1 x 4.9x 1 ,46 9 U OMO Media , Inc 1 /31 /200 9 U OMO OT C B B USD C ana da 0 .16 1 3.7 0.6 (0 .5) -7 8.2% 22.1 x - NA V a lueC lick Inc. 3 /31 /200 9 V C LK N as da qG S USD U nited S ta tes 11 98 0.1 591 .7 10 5.5 17 .8% 1.5 x 8.3x 1 ,18 9 V O IS , Inc. 3 /31 /200 9 V OIS OT C B B USD U nited S ta tes 0 .35 2 .9 0.0 (1 .1) NM - - 4 W ebze n Inc. 3 /31 /200 9 W ZE N N as da qG M USD S outh K orea 5 5 3.4 23. 3 (0 .4) -1 .9% - - 314 W izza rd S of twa re Corpora tion 3 /31 /200 9 W ZE AME X USD U nited S ta tes 0 .55 2 6.3 5.6 (5 .1) -9 1.5% 4.9 x - 110 W orlds .com In c. 3 /31 /200 9 W DD D OT C B B USD U nited S ta tes 0 5 .2 0.0 (0 .8) NM - - 1 W ynds torm C orporatio n NA W YND OT C B B USD U nited S ta tes 0 .51 9 .2 NA NM NM - - NA XIN G AG 3 /31 /200 9 O1B C XT R A EUR G ermany 34 25 1.6 53. 7 1 6.8 31 .2% 3.7 x 1 1.9 x 239 Y e dangOnline Co rp. 1 2/31 /200 7 A0 527 70 K OS E KR W S outh K orea 10 ,200 .00 12 9.8 55. 6 1 2.4 22 .4% 2.3 x 1 0.4 x NA Y n k K orea Inc. 1 2/31 /200 7 A0 237 70 K OS E KR W S outh K orea 7, 700 1 5.3 15. 8 (1 .2) -7 .6% 0.9 x - NA ZipLocal Inc. 3 /31 /200 9 T S XV : ZIP T S XV C AD C ana da 0 .01 0 .4 2.8 (2 .2) -7 8.3% 0.6 x - NA H igh 19,9 07. 1 1 ,817 .2 57 7.1 65 .0% 40.1 x 3 7.5 x 6 ,194 Lo w 0 .0 0.0 -28.0 -9 8.9% 0.0 x 0.1x 1 A vera ge 577.0 152 .1 32.9 6 .0% 4.9x 10.0x 671 Median 5 0.9 54. 3 0 .6 14 .2% 2.0 x 9.6x 237 Figure 1. Web 2.0 Universe Summary Source. Capital IQ

- 3. Page 3 C A P I T A L M A R K E T S A C T I V I T Y (M & A A N D F I N A N C I N G ) Activit y peaks in May – the highest in last 12 months and YTD CY2009: The month of May closed with 20 financings totalling $327.1 million led by the $200 million investment by Digital Sky Technologies in Facebook. The Facebook transaction aside, four transactions (One Net Ent., Cyberplex, Peer39, and OpenX) were greater than or equal to $10 million. The average value in May is $15.6 million (and $6.4 million excluding the Facebook transaction), greater than the average value for April of $6.2 million on 21 financings. The March average was $6.5 million on 24 financings. For the last three months, except for four deals (Kaixin001.com, Collective Media, One Net Entertainment, and Facebook), all were below $20 million and a total of six deals were greater than or equal to $15 million. Financing Activity Last Three Months 350.0 18.0 16.0 300.0 15.6 14.0 250.0 12.0 200.0 10.0 (US$m) (US$m) 8.0 150.0 6.5 6.2 6.4 6.0 100.0 4.0 50.0 2.0 0.0 0.0 Mar-09 Apr-09 May-09 May-09 (excl FB) Total Average Figure 2. Financings, Last Three Months Source. Company reports Facebook largest deal in April: Digital Sky Technologies announced a $200 million investment in Facebook last week, the largest deal so far in the last 12 months. The Facebook transaction aside, 14 of the 20 deals in the month are equal to or greater than $5 million. For additional details, see Figures 29 and 30 (at end of note). Also note that the spin-off of StumbleUpon from E-bay on a $29 million valuation occurred in May. E-bay had bought StumbleUpon for $75 million.

- 4. Page 4 Financing & M/A Summary - Last Three Months 250.0 200.0 150.0 May-09 (US$m) Apr-09 Mar-09 100.0 50.0 0.0 Pixazza Mixercast Collective Media Marin Software Miva EveryZing AnySource Media VoxPop Myngle Cyberplex Buzznet OpenX OLX Socialtext TubeMogul GOOM Radio Vidyo Greystripe Viximo IMShopping Tribal Nova I Love Rewards Medialets Topsy Resonate Networks Bit.ly Mo'Minis Brandtology Kaixin001.com SendMe Inc. OMGPOP DoubleTwist Tynt GoViral LendingClub Peer39 Auditude Cellufun Glam Media Batanga DocuSign Apture SoundCloud Tripbase Hunch AdultSpace Jodange Foodista Facebook Visible Measures Azuki Systems Loop'd Network 33Across Three Melons The Rubicon Project SuperSecret Conductor Inc. ScanScout BlogHer Inc. Gist Fuhu Inc. Sports Composite DE Socialcast Scan & Target StumbleUpon TimeBridge One Net Entertainment Simulmedia Imeem FreeWheel Figure 3. Capital Market Activity, Last Three Months Source. Company reports Social Network remains the most active sector: Activity over the last three months was busiest in the Social Network sector, with eight companies raising over $249.3 million (Figure 4). The Ad Network sector has the next highest totals, with 12 companies raising $99.2 million. W e would note that the Facebook transaction at $200 million has skewed the results significantly in favour of Social Networks. Nevertheless, the following sectors continue to generate the most capital activity over the last few months: Ad Network, Media, Gaming, Video, and Social Networks.

- 5. Page 5 Capital Market Activity by Sector - Last Three Months 300.0 250.0 200.0 (US$m) 150.0 249.3 100.0 50.0 99.2 63.4 50.6 49.5 30.2 21.3 14.4 12.0 12.0 10.4 8.9 7.5 7.0 6.8 5.9 5.5 0.0 5.0 4.7 4.1 3.1 2.0 2.0 2.0 1.3 1.3 0.6 Comment/Reputation Social Commerce Gaming Visual Commerce Travel Wiki Media Mobile Enterprise Collaboration Publishing Microblog Online Learning Mobile Ad Widget Search Lending Infrastructure Blog Social Networks SAS Video Virtual World Aggregation Crowdsourced Ad Network Analytics Content # companies 8 12 8 9 5 2 3 3 1 1 2 2 2 1 1 1 1 1 1 1 1 1 1 1 1 1 1 Figure 4. Capital Market Activity, by Sector, Last Three Months Source. Company reports Average round size decreases: On a trailing 12-month basis, total financing dollars fell as of May 2009, with average round sizes decreasing slightly (Figure 5).

- 6. Page 6 LTM Financing 4,000.0 18.0 16.0 3,500.0 14.0 3,000.0 12.0 2,500.0 10.0 (US$m) (US$m) 2,000.0 ` 8.0 1,500.0 6.0 1,000.0 4.0 500.0 2.0 0.0 0.0 May-06 May-07 May-08 May-09 Nov-05 Mar-06 Nov-06 Mar-07 Nov-07 Mar-08 Nov-08 Mar-09 Jul-05 Sep-05 Jan-06 Jul-06 Sep-06 Jan-07 Jul-07 Sep-07 Jan-08 Jul-08 Sep-08 Jan-09 Total Average Figure 5. Financings, Last 12 Months Source. Company reports Cumulative total nears $6.8 billion: Overall, on a cumulative basis, W eb 2.0 financings have totalled nearly $6.8 billion, with the majority of the financing coming in late 2007 and the first three quarters of 2008 (Figure 6). Financing for the first quarter of 2009 passed that raised in the fourth quarter of 2008 – reversing the downtrend since the second quarter last year. However, for the period ended Q1/CY09, total capital raised was below the Q1/CY08 level (at $748.2 million). The total capital raise in Q2-to-date was $477.1 million, buoyed by the $200 million Facebook transaction, and is well below Q2/CY08 totals ($1.3 billion). It does not seem likely the Q2/CY09 will be better on a Y/Y basis.

- 7. Page 7 Web 2.0 Financing (cumulative) 1,600.0 8,000.0 1,400.0 1,344.6 7,000.0 1,200.0 6,000.0 977.6 1,000.0 5,000.0 857.6 (US$m) (US$m) 800.0 4,000.0 579.9 573.8 600.0 3,000.0 477.1 378.6 400.0 354.1 2,000.0 178.7174.8162.4 200.0 1,000.0 126.4145.6111.5 88.3 47.5 33.5 61.5 38.8 24.7 22.2 43.3 0.0 0.0 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 Qtr3 Qtr4 Qtr1 Qtr2 2004 2005 2006 2007 2008 2009 Figure 6. Financing, Cumulative Source. Company reports U.S. remains dominant: U.S. companies continue to dominate capital market activity – with 70.0% of financings/M&A involving U.S. companies (based on dollars) (Figure 7). Based on number of transactions, the U.S. leads with 73.6% of deals, while Canada and UK each took 4.8% share of the total number of financings (Figure 8). Fi nancin g/M &A by Country - LTM ($) Financing/M&A by Country - LTM (#) China UK Canada 14.6% Israel 4.8% 4.8% 3.1% Russia France 3.4% 3.1% UK 2.3% Fr ance 1.9% Canada ROW 1.7% 10.6% Israe l 1 .6% ROW 4.5 % USA USA 70.0% 73.6% Figures 7 & 8. Financing/M&A, by Country (LTM, $, #) Source. Company reports

- 8. Page 8 Larger volume of early-stage funding (by count): Almost half of financings in the last 12 months are for early-stage companies (Angel/Seed or Series A) (Figure 9). Series B rounds are 29.3% of the total, with later-stage (Series D, E and PIPE) deals accounting for just 7.5%. Financing by Type - LTM Series C 14.7% Series B 29.3% Series D 4.5% Series E 1.1% Angel/Seed 11.3% Debt financing Series A 3.0% 34.2% PIPE 1.9% Figure 9 Financing, by Type (LTM, #) Source. Company reports Equity financings smaller over last 12 months: In the last 12 months, the average size of Series A, C, and D rounds has all been lower than the overall average (Figure 10).

- 9. Page 9 Average financing round size 40.0 36.0 35.0 32.0 30.0 26.3 25.1 25.0 21.6 (US$m) 20.0 18.3 15.0 11.4 11.4 10.8 10.8 10.0 7.9 6.5 6.9 5.4 5.0 3.3 2.6 0.0 Angel/Seed Debt financing PIPE Series A Series B Series C Series D Series E LTM Average Size Overall Average Figure 10. Average Size per Round Source. Company reports

- 10. Page 10 C A P I T A L M A R K E T S A C T I V I T Y (P R I C E P E R F O R M A N C E ) Price Performance: Our W eb 2.0 index (market-cap weighted) underperformed the NASDAQ composite index from mid- 2008 until recently when it has moved sharply higher than the NASDAQ index (Figure 11). Web 2.0 Index Price Performance 103.63 93.63 83.63 73.63 63.63 53.63 43.63 Index: Web 2.0 X (Market Cap Weights) ^COMP - Share Pricing Figure 11. Web 2.0 Price Performance Source. Capital IQ GameOn Co. Ltd. leads; eolith Co. Ltd. falls: Most of the companies in our universe had positive stock price performances over the past week (for stocks with prices greater than $1) (Figure 12), with 29 companies showing positive returns on the week. GameOn Co. Ltd (3812-TSE) led the group with a 28.2% return, while eolith Co. Ltd. (A041060- KOSE) had the worst return, dropping 13.7% in the week.

- 11. Page 11 1 Week P rice P erformance G ameOn Co Ltd. 28.2% Northgate Technologies Limited 27.2% Changy ou.com Limited 23.3% S ohu.com Inc. 22.1% A ctoz S of t Co., Ltd. 20.9% A Q Interactiv e, Inc. 19.4% CDC Corp. 18.9% S K Communications Co., Ltd. 17.6% Perfect World Co., Ltd. 16.6% Open Tex t Corp. 13.2% V alueClick Inc. 12.4% Gamania Digital Entertainment Co., 11.0% S handa Interactive Entertainment Ltd. 9.6% Tencent Holdings Ltd. 9.4% Neteas e.com Inc. 9.3% IA C/InterA ctiveCorp. 7.1% Quepas a Corp. 6.3% G ree, Inc. 6.2% United Online Inc. 6.1% S hutterf ly , Inc. 5.9% Modern Times G roup Mtg A B 5.4% G igaMedia Ltd. 4.0% Openw ave S y s tems Inc. 3.6% XING A G 3.3% The9 Limited 3.3% TheS treet.com, Inc. 3.2% Ngi G roup Inc. 2.1% LookS mart, Ltd. 1.6% DA DA S pA 0.3% Lingo Media Corporation 0.0% Chines e Gamer International -0.4% NEOWIZ Games Corporation -0.5% NetDragon WebS of t, Inc. -0.6% Webz en Inc. -0.7% Mix i, Inc. -2.6% Y nk K orea Inc. -2.7% Giant Interactive G roup, Inc. -4.1% HanbitS of t, Inc. -4.2% Y edangOnline Corp. -5.6% Frogs ter Interactiv e Pictures A G -6.3% K ings of t Co. Ltd. -6.6% G ravity Co., Ltd -6.8% PhotoChannel Netw orks Inc. -9.9% Cy berplex Inc. -10.3% Tree.Com, Inc. -12.0% B ey ond Commerc e, Inc. -12.2% Eolith Co. Ltd. -13.7% -20.0% -15.0% -10.0% -5.0% 0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% Figure 12. 1-Week Price Performance Source. Capital IQ