Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (18)

Semelhante a Paris Pv Presentation Part2

Semelhante a Paris Pv Presentation Part2 (20)

Mais de cooppower

Mais de cooppower (10)

Último

Último (20)

Paris Pv Presentation Part2

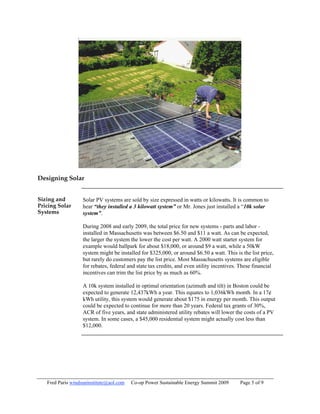

- 1. Designing Solar Sizing and Solar PV systems are sold by size expressed in watts or kilowatts. It is common to Pricing Solar hear “they installed a 3 kilowatt system” or Mr. Jones just installed a “10k solar Systems system”. During 2008 and early 2009, the total price for new systems - parts and labor - installed in Massachusetts was between $6.50 and $11 a watt. As can be expected, the larger the system the lower the cost per watt. A 2000 watt starter system for example would ballpark for about $18,000, or around $9 a watt, while a 50kW system might be installed for $325,000, or around $6.50 a watt. This is the list price, but rarely do customers pay the list price. Most Massachusetts systems are eligible for rebates, federal and state tax credits, and even utility incentives. These financial incentives can trim the list price by as much as 60%. A 10k system installed in optimal orientation (azimuth and tilt) in Boston could be expected to generate 12,437kWh a year. This equates to 1,036kWh month. In a 17¢ kWh utility, this system would generate about $175 in energy per month. This output could be expected to continue for more than 20 years. Federal tax grants of 30%, ACR of five years, and state administered utility rebates will lower the costs of a PV system. In some cases, a $45,000 residential system might actually cost less than $12,000. Fred Paris windsuninstitute@aol.com Co-op Power Sustainable Energy Summit 2009 Page 5 of 9

- 2. Not enough room on the roof? Consider a pole-mounted or ground mount system. Fred Paris windsuninstitute@aol.com Co-op Power Sustainable Energy Summit 2009 Page 6 of 9

- 3. The Financial Perspective Payback, Tax Payback Credits, The idea of payback in years is the holy grail of a solar investment, but ask ten Rebates and people how payback is computed and we get several perspectives. The most common Life Cycle definition is simple payback expressed as the number of years it takes for the Costs cumulative monthly savings in electricity to equal the investment. Contrasting this measure with another financial gauge – life cycle cash flow – easily demonstrates that simple payback may not be the most appropriate measure for residential PV applications. If we define simple payback (SP) as the net cost (NC) to the owner, and given the yearly revenue (YR) as the average revenue of the PV system (reduced electric bills minus expenses), the simple payback SP in years is given by: SP=NC/YR Continued on next page Fred Paris windsuninstitute@aol.com Co-op Power Sustainable Energy Summit 2009 Page 7 of 9

- 4. The Financial Perspective, Continued Payback The simple payback perspective however does not capture all of the financial benefits that may be available to homeowners. These include: • The possibility of borrowing to pay for the system through a home equity loan or a mortgage where payments are spread over the life of the loan with relatively low interest that is also tax deductible. • The commodity value of renewable energy credits (RECs). • The tax credits on both federal and state tax liability. • The value of the energy produced over the life of the system. • The Commonwealth Solar rebate incentives including a base rebate, home value rebate, household income rebate, and regional incentives. Accounting for these factors changes the financial picture to a cash flow model: CF = (MVE – PMT) +TXB where MVE is the monthly value of energy resulting from utility bill savings, PMT is the payment on the loan based on the principle after all rebates and REC values, and TXB is the tax benefit resulting from the loan interest write-off. It can often be demonstrated that with no money down PV systems could provide a positive cash flow to the owner every single year starting in year one. Fred Paris windsuninstitute@aol.com Co-op Power Sustainable Energy Summit 2009 Page 8 of 9

- 5. Financial Incentives for Massachusetts Residential Projects State Personal Massachusetts provides a personal income tax credit for individuals who install solar Income Tax photovoltaic (PV) systems in their residences. The system must be new, in Credit compliance with all applicable performance and safety standards, and expected to remain in operation for at least 5 years. The credit is 15% of the net expenditure for the system including installation, or $1,000, whichever is less. The credit can be carried over for a period of 3 years if it is greater than one's state income tax liability in individual years. M.G.L. c. 62, sec. 6(d) State Sales Tax Purchases of equipment directly relating to PV systems are exempted from the state Exemption sales tax if they are to be used as a primary or auxiliary source of energy supplying the needs of a person's principal residence in the state. M.G.L. c. 64H, sec. 6(dd) Local Property Solar energy systems supplying the energy needs of a residence are eligible for an Tax Exemption exemption from local property tax. This exemption, which is good for 20 years from the date of system installation, applies only to the value of the renewable energy equipment reflected on the property tax bill, not the full amount of the bill. M.G.L. c. 59, sec. 5, cl. 45 Renewable Owners of solar energy facilities can sell their RECs under a variety of pricing and Energy Credits contract terms without compromising their ability to capitalize on the monetary benefits associated with on-site electricity generation, net metering, and power supply agreements. Commonwealth Brand new for 2008 is the Commonwealth Solar Plan. Commonwealth Solar has $68 Solar Rebates million available for funding over the next four years to support PV installations in Massachusetts. Federal Tax Federal Residential Grants for PV and other renewable technologies provide for Grants residential energy payments of up to 30%. There is no cap. Fred Paris windsuninstitute@aol.com Co-op Power Sustainable Energy Summit 2009 Page 9 of 9