Office market dashboard 2011 q2 central

Commercial real estate toronto, office space toronto, toronto office space, office search toronto, office space in toronto, office rentals toronto, office space price in toronto, office rent downtown toronto, office rent toronto, toronto offices for lease, small office space toronto, toronto recent listings, toronto office rentals, toronto office lease, cost of downtown toronto space, office lease price toronto downtown, toronto office leases, office lease prices toronto, toronto office rent, toronto loft spaces for rent, office space for rent in toronto, Toronto office real estate blog, office space for rent toronto, office space in toronto price, rent office toronto, offices for lease toronto, sublet office toronto, leasing companies downtown toronto, LinkedIn

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (16)

Semelhante a Office market dashboard 2011 q2 central

Semelhante a Office market dashboard 2011 q2 central (20)

Mais de Chris Fyvie

Mais de Chris Fyvie (20)

Último

Último (20)

Office market dashboard 2011 q2 central

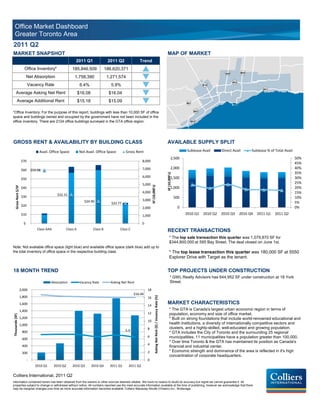

- 1. Office Market Dashboard Greater Toronto Area 2011 Q2 MARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 185,846,509 186,620,371 p Net Absorption 1,758,390 1,271,574 q Vacancy Rate 6.4% 5.9% q Average Asking Net Rent $16.08 $16.04 q Average Additional Rent $15.18 $15.09 q *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 2124 office buildings surveyed in the GTA office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 2,500 50% $70 8,000 45% $60 7,000 2,000 40% $59.98 35% SF (10,000's) 6,000 1,500 30% $50 5,000 25% SF (10,000's) 1,000 20% Gross Rent $/SF $40 4,000 15% $32.31 $30 500 10% $24.90 3,000 $22.77 5% $20 0 2,000 0% $10 1,000 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $- 0 Class AAA Class A Class B Class C RECENT TRANSACTIONS * The top sale transaction this quarter was 1,079,870 SF for $344,800,000 at 595 Bay Street. The deal closed on June 1st. Note: Not available office space (light blue) and available office space (dark blue) add up to the total inventory of office space in the respective building class. * The top lease transaction this quarter was 180,000 SF at 5550 Explorer Drive with Target as the tenant. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * GWL Realty Advisors has 644,952 SF under construction at 18 York Absorption Vacancy Rate Asking Net Rent Street. 2,000 18 $16.04 1,800 Asking Net Rent ($) / Vacancy Rate (%) 16 1,600 14 MARKET CHARACTERISTICS 1,400 * The GTA is Canada's largest urban economic region in terms of 12 population, economy and size of office market. Thousands (SF) 1,200 * Built on strong foundations that include world-renowned educational and 10 1,000 health institutions, a diversity of internationally competitive sectors and 8 clusters, and a highly-skilled, well-educated and growing population. 800 5.9 * GTA includes the City of Toronto and the surrounding 25 regional 6 municipalities. 11 municipalities have a population greater than 100,000. 600 * Over time Toronto & the GTA has maintained its position as Canada's 400 4 financial and industrial center. 200 2 * Economic strength and dominance of the area is reflected in it's high concentration of corporate headquarters. - 0 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 2. Office Market Dashboard Downtown 2011 Q2 MARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 69,731,115 70,382,021 p Net Absorption 774,454 791,217 p Vacancy Rate 5.7% 4.6% q Average Asking Net Rent $22.82 $23.30 p Average Additional Rent $22.87 $23.00 p *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 525 office buildings surveyed in the Downtown office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 800 20% $70 3,000 700 18% $60 $59.98 16% 2,500 600 14% SF (10,000's) 500 12% $50 $47.23 2,000 400 10% SF (10,000's) 8% Gross Rent $/SF $40 300 $35.76 1,500 6% $30 200 $30.74 4% 1,000 100 2% $20 0 0% $10 500 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $- 0 Class AAA Class A Class B Class C RECENT TRANSACTIONS * The top sale transaction this quarter was SF for $103,000,000 at 180 Dundas Street West. The deal closed January 25th. Note: Not available office space (light blue) and available office space (dark blue) add up to the total inventory of office space in the respective building class. * The top lease transaction this quarter was 78,000 SF at 18 York Street. The tenant was SNC Lavilin. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * GWL Realty Advisors has 644,952 SF under construction at 18 York Absorption Vacancy Rate Asking Net Rent Street. 1,000 $23.30 25 Asking Net Rent ($) / Vacancy Rate (%) 800 MARKET CHARACTERISTICS 20 * Submarkets within the Downtown market include: Financial Core, 600 Downtown East, Downtown North, Downtown South and Downtown West. Thousands (SF) 15 * Major Highways to Toronto Submarkets: Highway 400, Highway 401, Highway 427, Don Valley Parkway, Gardner Expressway, Queen Elizabeth 400 Way. 10 * Billy Bishop Toronto City Airport is minutes from the Downtown Core and 200 Financial District. * Public Transit available by TTC bus and subway systems. GO Transit 4.6 5 network connects Toronto to Peel, York, Durham and Halton Regions via - Bus and Train routes. 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 * Toronto remains the largest business centre in Canada and is home to the -200 0 five largest banks, five public research Universities and six community Colleges. Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 3. Office Submarket Dashboard Financial Core 2011 Q2 SUBMARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 33,631,324 33,618,409 q Net Absorption 454,190 464,522 p Vacancy Rate 6.3% 5.2% q Average Asking Net Rent $26.00 $26.30 p Average Additional Rent $28.28 $27.89 q *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 109 office buildings surveyed in the Financial Core office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 500 50% $70 1,400 450 45% $60 $59.98 1,200 400 40% 350 35% SF (10,000's) $52.73 300 30% $50 1,000 250 25% SF (10,000's) 200 20% Gross Rent $/SF $40 $40.75 800 $37.75 150 15% $30 600 100 10% 50 5% $20 400 0 0% $10 200 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $- 0 Class AAA Class A Class B Class C RECENT TRANSACTIONS * No sale transactions were recorded during this period. Note: Not available office space (light blue) and available office space (dark blue) add * The top lease transaction this quarter was 27,500 SF at 181 Bay up to the total inventory of office space in the respective building class. Street. The tenant was Global Prime Office. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * No under construction projects recorded during this period. Absorption Vacancy Rate Asking Net Rent 600 30 Asking Net Rent ($) / Vacancy Rate (%) 500 $26.30 25 SUBMARKET CHARACTERISTICS * The Financial Core is the most dense office submarket in the GTA, with 400 20 one of the lowest vacancy rates. Thousands (SF) * GTA top annual rental rates are located in buildings in this market. 300 15 * Prestige urban location and modern, state-of-the-art architecture. 200 10 * Limited parking, but great access to public transit and the PATH system 5.2 (Toronto's underground walkway). 100 5 * Proximity to multiple amenities and services are convenient for employees and customers. - 0 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 4. Office Submarket Dashboard Downtown East 2011 Q2 SUBMARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 3,980,709 3,924,812 q Net Absorption 60,116 98,743 p Vacancy Rate 6.0% 6.7% p Average Asking Net Rent $18.19 $18.76 p Average Additional Rent $9.94 $10.45 p *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 110 office buildings surveyed in the Downtown East office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 60 12% $40 250 $35.53 50 10% $35 $31.82 200 40 8% SF (10,000's) $30 $25 30 6% $24.13 150 SF (10,000's) Gross Rent $/SF $20 20 4% $15 100 10 2% $10 0 0% 50 $5 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $- 0 Class A Class B Class C RECENT TRANSACTIONS * No sale transactions were recorded during this period. Note: Not available office space (light blue) and available office space (dark blue) add * The top lease transaction this quarter was 14,000 SF at 143 Lake up to the total inventory of office space in the respective building class. Shore Blvd East. The deal closed May 12th. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * No under construction projects recorded during this period. Absorption Vacancy Rate Asking Net Rent 150 $18.76 20 18 Asking Net Rent ($) / Vacancy Rate (%) 100 16 SUBMARKET CHARACTERISTICS 50 14 * Public Transit available by TTC bus and subway systems. GO Transit network connects Toronto to Peel, York, Durham and Halton Regions via Bus and Train Thousands (SF) 12 routes. - 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 10 * VIA Rail, Amtrak and Ontario Northlands rail service from Union Station. -50 * Billy Bishop Toronto City Airport is minutes from the Downtown Core. 6.7 8 * Major Highways to Downtown East Submarket: Gardiner Expressway and Don -100 6 Valley Parkway. * The original 10 blocks of Toronto are located within this submarket, making it 4 home to many historical brick and beam buildings. -150 2 * Top Industries in Downtown East include: Business Services, Finance, Insurance and Real Estate, Information and Cultural Industries. -200 0 Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 5. Office Submarket Dashboard Downtown North 2011 Q2 SUBMARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 14,723,534 14,718,459 q Net Absorption 89,380 59,639 q Vacancy Rate 3.4% 3.1% q Average Asking Net Rent $18.32 $19.65 p Average Additional Rent $19.54 $19.70 p *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 74 office buildings surveyed in the Downtown North office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 80 50% $44 700 70 45% $43.02 600 40% $42 60 35% SF (10,000's) 50 30% 500 $40 40 25% SF (10,000's) 20% Gross Rent $/SF 400 30 $38 15% 300 20 10% $36 10 5% $36.16 $35.88 200 0 0% $34 100 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $32 0 Class A Class B Class C RECENT TRANSACTIONS * The top sale transaction this quarter was 1,079,870 SF for $344,800,000 at 595 Bay Street. The deal closed June 1st. Note: Not available office space (light blue) and available office space (dark blue) add up to the total inventory of office space in the respective building class. * No lease transactions were recorded during this period. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * No under construction projects recorded during this period. Absorption Vacancy Rate Asking Net Rent 100 20 $18.07 80 18 Asking Net Rent ($) / Vacancy Rate (%) SUBMARKET CHARACTERISTICS 60 16 * Public Transit available by TTC bus and subway systems. GO Transit network 40 14 connects Toronto to Peel, York, Durham and Halton Regions via Bus and Train Thousands (SF) 20 12 routes. * VIA Rail, Amtrak and Ontario Northlands rail service from Union Station. - 10 Billy Bishop Toronto City Airport is minutes from the Downtown Core. -20 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 8 * Major Highway to Downtown North Submarket: Don Valley Parkway. -40 6 * Bordering the Financial Core, amenities within the Downtown North submarket include Provincial Courts, the Toronto Eaton Centre and the Toronto Discovery -60 3.1 4 District research park. -80 2 * Top Employers include: Rogers Telecommunication, Royal Bank of Canada, Bank of Montreal, and Ontario Power Generation. -100 0 * Top Industries in Downtown North include: Finance, Insurance and Real Estate, Public Administration and Business Services. Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 6. Office Submarket Dashboard Downtown South 2011 Q2 SUBMARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 3,087,471 3,815,463 p Net Absorption 12,995 65,526 p Vacancy Rate 7.1% 5.0% q Average Asking Net Rent $15.00 $22.02 p Average Additional Rent $13.16 $18.08 p *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 18 office buildings surveyed in the Downtown South office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 40 90% $60 250 35 80% $53.90 70% $50 30 200 60% SF (10,000's) 25 $40 50% 20 150 40% SF (10,000's) Gross Rent $/SF 15 $30 30% $29.31 10 20% 100 $20 5 10% $18.82 0 0% 50 $10 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $- 0 Class A Class B Class C RECENT TRANSACTIONS * No sale transactions were recorded during this period. Note: Not available office space (light blue) and available office space (dark blue) add * The top lease transaction this quarter was 78,000 SF at 18 York Street. up to the total inventory of office space in the respective building class. The tenant was SNC Lavilin. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * GWL Realty Advisors has 644,952 SF under construction at 18 York Street. Absorption Vacancy Rate Asking Net Rent 500 25 Asking Net Rent ($) / Vacancy Rate (%) 400 $22.02 SUBMARKET CHARACTERISTICS 20 * Public Transit available by TTC bus and subway systems. GO Transit network 300 connects Toronto to Peel, York, Durham and Halton Regions via Bus and Train Thousands (SF) 15 routes. * VIA Rail, Amtrak and Ontario Northlands rail service from Union Station. 200 * Billy Bishop Toronto City Airport is minutes from the Downtown Core. 10 * Major Highway to Downtown South Submarket: Gardiner Expressway. 100 * Significant Office developments south of Union Station are redefining the 5.0 boundaries of the Financial Core. 5 * New facilities include: Corus Entertainment Headquarters, George Brown - College Waterfront Campus. 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 * Top Industries in Downtown South include: Finance, Insurance and Real Estate, -100 0 Business Services, Information and Cultural Industries. Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 7. Office Submarket Dashboard Downtown West 2011 Q2 SUBMARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 14,308,077 14,304,878 q Net Absorption 157,774 102,788 q Vacancy Rate 6.1% 4.0% q Average Asking Net Rent $17.91 $18.07 p Average Additional Rent $14.50 $15.03 p *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 214 office buildings surveyed in the Downtown West office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 160 25% $35 900 140 $34 $33.75 800 20% $33.38 120 $33 SF (10,000's) 700 100 15% $32 600 80 $31 SF (10,000's) 10% Gross Rent $/SF 500 60 $30 400 40 $29 5% $28.48 300 20 $28 0 0% $27 200 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $26 100 $25 0 Class A Class B Class C RECENT TRANSACTIONS * The top sale transaction this quarter was 3,500 SF for $1,360,000 at 123 John Street. The deal closed on March 31st. . Note: Not available office space (light blue) and available office space (dark blue) add up to the total inventory of office space in the respective building class. * The top lease transaction this quarter was 26,000 SF at 155 Wellington Street West. The tenant is Paliare Roland. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * No under construction projects recorded during this period. Absorption Vacancy Rate Asking Net Rent 200 20 18 Asking Net Rent ($) / Vacancy Rate (%) $18.07 150 16 SUBMARKET CHARACTERISTICS * Offering many downtown location advantages, but at lower rental prices 14 than in the Financial Core . Thousands (SF) 100 12 * This submarket is an excellent option for those tenants whose operations do not require a core location. 10 * Well connected to public transit (streetcars along King Street W and 50 8 Queen Street W) and to the Gardiner Expressway, making this submarket accessible to employees and customers. 6 * With many new residential high-rise developments (e.g. Concord City 4.0 - 4 Place), the labour pool will increase and diversify. 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 * Many former factory buildings (brick & beam) have been converted into 2 office buildings, specifically hosting the Information Technology, Art and -50 0 Design Industry. Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 8. Office Market Dashboard Midtown 2011 Q2 SUBMARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 18,300,645 18,232,300 q Net Absorption 153,787 153,463 q Vacancy Rate 4.8% 4.7% q Average Asking Net Rent $15.56 $15.90 p Average Additional Rent $18.66 $18.35 q *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 213 office buildings surveyed in the Midtown office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 250 50% $45 1,200 45% $40 $41.40 200 40% 1,000 35% SF (10,000's) $35 $33.85 150 30% $30 800 25% $28.76 SF (10,000's) 100 20% Gross Rent $/SF $25 600 15% $20 50 10% $15 400 5% 0 0% $10 200 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $5 $- 0 Class A Class B Class C RECENT TRANSACTIONS * The top sale transaction this quarter was 64,575 SF for $12,601,000 at 161 Eglinton Avenue East. The deal closed June 7th. Note: Not available office space (light blue) and available office space (dark blue) add up to the total inventory of office space in the respective building class. * No major lease transactions were recorded during this period. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * No under construction projects recorded during this period. Absorption Vacancy Rate Asking Net Rent 200 18 Asking Net Rent ($) / Vacancy Rate (%) 16 150 $15.90 SUBMARKET CHARACTERISTICS 14 * Submarkets within the Midtown Market include: Toronto West, Yonge & 100 12 Bloor, Yonge & St. Clair and Yonge & Eglinton. Thousands (SF) * Public Transit available by TTC bus and subway systems. GO Transit 10 network connects Toronto to Peel, York, Durham and Halton Regions via 50 Bus and Train routes. 8 * Major Highways to Midtown Market: Highway 401 and Don Valley - 6 Parkway. 4.7 * Major Corporations in the market include: RioCan, Canadian Tire, Toronto 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 4 Transit Commission (TTC) and Desjardins Credit Union. -50 * Top Industries in the Midtown Market include: Business Services, 2 Finance, Insurance and Real Estate and Public Administration. -100 0 Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.

- 9. Office Submarket Dashboard Yonge - Bloor 2011 Q2 MARKET SNAPSHOT MAP OF MARKET 2011 Q1 2011 Q2 Trend Office Inventory* 9,659,332 9,633,002 q Net Absorption 61,748 40,969 q Vacancy Rate 3.8% 4.0% p Average Asking Net Rent $16.71 $17.51 p Average Additional Rent $19.95 $19.39 q *Office Inventory: For the purpose of this report, buildings with less than 10,000 SF of office space and buildings owned and occupied by the government have not been included in the office inventory. There are 74 office buildings surveyed in the Yonge- Bloor office region. GROSS RENT & AVAILABILITY BY BUILDING CLASS AVAILABLE SUPPLY SPLIT Avail. Office Space Not Avail. Office Space Gross Rent Sublease Avail Direct Avail Sublease % of Total Avail. 70 50% $45 600 $42.83 45% 60 $40 40% 500 50 35% $36.20 SF (10,000's) $35 40 30% $30 $30.59 400 25% 30 SF (10,000's) 20% Gross Rent $/SF $25 300 20 15% $20 10% 10 $15 200 5% 0 0% $10 100 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 $5 $- 0 Class A Class B Class C RECENT TRANSACTIONS * The top sale transaction this quarter was 5,176 SF for $1,800,000 at 133 Lowther Avenue. The deal closed June 20th. Note: Not available office space (light blue) and available office space (dark blue) add up to the total inventory of office space in the respective building class. * No lease transactions were recorded during this period. 18 MONTH TREND TOP PROJECTS UNDER CONSTRUCTION * No under construction projects recorded during this period. Absorption Vacancy Rate Asking Net Rent 70 20 $17.51 18 Asking Net Rent ($) / Vacancy Rate (%) 60 16 MARKET CHARACTERISTICS 50 * Public Transit available by TTC bus and subway systems. GO Transit network 14 40 connects Toronto to Peel, York, Durham and Halton Regions via Bus and Train Thousands (SF) 12 routes. 30 10 * Largest Midtown Office Submarket in terms of Total Inventory and Occupied 20 Space. 8 * Major Highway to Yonge-Bloor Submarket: Don Valley Parkway. 10 * Labour pool intensification as a result of many new high-rise residential 6 4.0 developments in the Submarket. - 4 * Top Employers include: TD Waterhouse, Bank of Montreal, Royal Bank of 2010 Q1 2010 Q2 2010 Q3 2010 Q4 2011 Q1 2011 Q2 -10 2 Canada and Hudson Bay Company. * Top Industries in the Yonge-Bloor Submarket include: Finance, Insurance and -20 0 Real Estate, Business Services and Information and Cultural Industries. Colliers International, 2011 Q2 Information contained herein has been obtained from the owners or other sources deemed reliable. We have no reason to doubt its accuracy but regret we cannot guarantee it. All properties subject to change or withdrawal without notice. All numbers reported use the most accurate information available at the time of publishing, however we acknowledge that there may be marginal changes over time as more accurate information becomes available. Colliers Macaulay Nicolls (Ontario) Inc., Brokerage.