Recomendados

Mais conteúdo relacionado

Último

Último (20)

Destaque

Destaque (20)

The Truth about Long Term Care Insurance

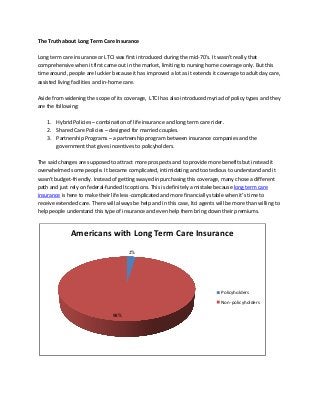

- 1. The Truth about Long Term Care Insurance Long term care insurance or LTCI was first introduced during the mid-70’s. It wasn’t really that comprehensive when it first came out in the market, limiting to nursing home coverage only. But this time around, people are luckier because it has improved a lot as it extends it coverage to adult day care, assisted living facilities and in-home care. Aside from widening the scope of its coverage, LTCI has also introduced myriad of policy types and they are the following: 1. Hybrid Policies – combination of life insurance and long term care rider. 2. Shared Care Policies – designed for married couples. 3. Partnership Programs – a partnership program between insurance companies and the government that gives incentives to policyholders. The said changes are supposed to attract more prospects and to provide more benefits but instead it overwhelmed some people. It became complicated, intimidating and too tedious to understand and it wasn’t budget-friendly. Instead of getting swayed in purchasing this coverage, many chose a different path and just rely on federal-funded ltc options. This is definitely a mistake because long term care insurance is here to make their life less-complicated and more financially stable when it’s time to receive extended care. There will always be help and in this case, ltci agents will be more than willing to help people understand this type of insurance and even help them bring down their premiums. Americans with Long Term Care Insurance 2% Policyholders Non-policyholders 98%

- 2. This chart shows that despite the efforts of the ltc insurance industry in making the policy more attractive to consumers, there are still some who are scared to jump into the bandwagon. Americans are more comfortable in purchasing policy for their homes, cars and pets than take the risk by going to unfamiliar territory and buying ltci. There are still a lot of facts that people should know about this type of insurance, which in turn can make this much easier for them to grasp. Misconceptions on Long Term Care Insurance: 1. Medicare doesn’t provide long term care coverage According to Medicare’s website, it doesn’t provide coverage for indefinite long term care but provides coverage for illness and injury recover or in other words for short-term care. In addition to that, Medicare also offers coverage for home health care, hospice care and medically necessary skilled nursing facility. However, it doesn’t provide assistance on ADLs or activities of daily living such as eating, bathing, toileting and dressing. 2. Long term care insurance is exclusive to seniors The first thing that comes into everyone’s mind when they hear LTCI is old people. It is often associated to seniors but what people need to understand is the fact that even those who aren’t old can receive long term care. No one knows what can happen in the future, one might get injured, face an accident or develop a chronic illness while they are young. A proof of this is a report submitted by the National Care Planning Council, showing that young and old will need long term care at any point of their lives.

- 3. Long Term Care Recipients by Age Under Age 18 Ages 18 to 64 Age 65 and Older 3% 40% 57% 3. Long term care insurance is not a necessity Most people think that it’s not necessary to purchase ltci thinking that their family will always be there to take care of them. Of course, your family will take the responsibility but do you think they are capable of providing you with the proper care you need and do you want to become a burden to them? And besides, more elderly people today are living independently, so when the inevitable happens a back-up plan is necessary. Without coverage, people will have to pay for all their long term care expenses using their savings and other assets. It will be much easier to handle ltc expenses through long term care policy. 4. Purchase insurance when you need it Purchasing ltc coverage right at the time you really need it is not possible. It’s just the same as buying home insurance while your house is already burning. People choose to neglect the fact that they will most likely need long term care, so they age without coverage and suffer the consequences of their negligence in the future. It’s a lot harder and more expensive to purchase coverage if you are at risk of developing a serious condition or you already have one. It’s much better to consider this early, the healthier and younger you are, the lower your premiums will be and you’re well- prepared. 5. Long term care coverage is expensive LTCI is expensive in nature but there are ways to cut the cost. The younger you are when you purchase the policy, the lower the cost of coverage will be. It’s much cheaper if you buy this while

- 4. you’re in your 50’s or even much younger than that. To give you an idea of how much you’re going to spend annually, the average annual premium of a married couple in good health is $2,350. According to Jesse Slome, the executive director of AALTCI or American Association for Long-Term Care Insurance, the range of a couple’s premium every year is between $2,085 and $3,970, and this still depends on their family history and risk factors. It’s possible that the cost will rise but you need not worry because this will still be subject to state regulatory approval. Below you can find different ways on how you can keep your premiums more affordable: Eight Ways to Save on LTCI Premiums Purchasing Early Spousal Discounts Good Health Discounts Group Discounts Tax Deductions Smaller Policy Longer Elimination Period Annual Premium Payments