Andrew Webber game apps opportunities in 2013 [source slides]

•Transferir como PPTX, PDF•

0 gostou•2,196 visualizações

Watch presentation at http://www.youtube.com/watch?v=dYO1pGE3kBs View From The Bridge: Game Apps Opportunities in 2013 by Microsoft UK's Andrew Spooner. These are the source data slides he used at Gaming Reimagined 2013 in Dublin

Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

Último

Último (20)

Andrew Webber game apps opportunities in 2013 [source slides]

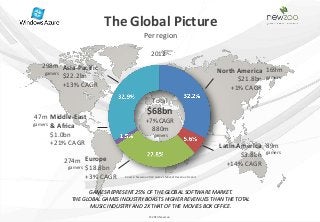

- 1. The Global Picture Per region 2012 298m Asia-Pacific gamers North America 169m $22.2bn $21.8bn gamers +13% CAGR +1% CAGR Total $68bn 47m Middle-East +7% CAGR gamers & Africa 880m $1.0bn gamers +21% CAGR Latin America 89m $3.8bn gamers 274m Europe +14% CAGR gamers $18.8bn +3% CAGR Source: Newzoo 2012 Games Market Revenue Report GAMES REPRESENT 25% OF THE GLOBAL SOFTWARE MARKET. THE GLOBAL GAMES INDUSTRY BOASTS HIGHER REVENUES THAN THE TOTAL MUSIC INDUSTRY AND 2X THAT OF THE MOVIES BOX OFFICE. © 2013 Newzoo

- 2. The Global Picture Per Market Segment Casual Websites PC/Mac Download $4.2bn $7.6bn -1% CAGR +2% CAGR Social Networks $3.9bn +5% CAGR PC/Mac Boxed Total $8.0bn Mobile $68bn Devices -11% CAGR +7% CAGR 9.0bn +32% CAGR Consoles $21.2 MMOs -2% CAGR $13.6bn Source: Newzoo 2012 Games Market Revenue Report +21% CAGR © 2013 Newzoo

- 3. Microsoft is Already a Leader But Dramatic Market Changes Spark Opportunities for All Business Units © 2013 Newzoo

- 4. Kings of Free-to-Play New companies set up to manage games-as-a-service ALL GAMES ARE MULTIPLAYER AND CONTINUOSLY RUN AND CONNECTED THROUGH THE CLOUD. FREE-TO-PLAY | PLATFORM/SCREEN: PC PUBLISHER: RIOTGAMES (US) OWNED BY TENCENT (CHINA) LAUNCH: OCTOBER 2009 MONTHLY ACTIVE PLAYERS: +/- 35,000,000 MONTHLY REVENUES: +/- $40,000,000 FREE-TO-PLAY | PLATFORM/SCREEN: PC PUBLISHER: WARGAMING.NET (RUSSIA) LAUNCH: APRIL 2008 MONTHLY ACTIVE PLAYERS: +/- 13,000,000 MONTHLY REVENUES: +/- $55,000,000 ESTIMATED PROFIT/MONTH: $25,000,000 ESTIMATED CLOUD COSTS/MONTH: $1.5-2M, $3-4M incl hardware FREE-TO-PLAY | PLATFORM/SCREEN: SMARTPHONE, TABLET PUBLISHER: SUPERCELL (FINLAND) LAUNCH: AUGUST 2012 MONTHLY DOWNLOADS: +/- 4,000,000 MONTHLY REVENUES: +/- $15,000,000 © 2013 Newzoo

- 5. Time is Money eSports and Spectator Mode double time spent and load on the cloud Prize money season 2: $5,000,000 Video Watch live games of gamers that are (slightly) better than you. © 2013 Newzoo

- 6. Mobile Games Market tablet and smartphone games (global, 2012) $9bn +32% >500M CONSUMER SPEND ANNUAL GROWTH MOBILE PLAYERS >175M PAYING PLAYERS 33% OF ALL* 66% OF ALL* DOWNLOADS MONEY $ TO SMARTPHONES SPENT ON SMARTPHONES AND TABLETS WERE AND TABLETS WAS SPENT ON GAMES *BASED ON iOS APP STORE DATA IN 44 COUNTRIES & PLAYSTORE GAMES DATA OF 17 COUNTRIES © 2013 Distimo/Newzoo

- 7. UK Market Overview Quarter 3 2012 - selected results Ukie Event: 24 Jan Ian Bramley

- 8. WHAT IS GAMETRACK? APPS ONLINE PACKAGED FREE APPS SOCIAL DISC/CART PAID APPS FREE DOWNLOAD NEW PAID EXTRAS PAID DOWNLOAD PRE OWNED PAID EXTRAS RENTAL MULTIPLAYER BROWSER TIME SPENT ACQUISITION VALUE

- 9. HOW DO WE DO IT? MONTHLY FIELDWORK PER MARKET 1,000 Nat Rep 1,000 Online Face to Face Rep SAMPLES COMBINED AND WEIGHTED TO BE NATIONALLY REPRESENTATIVE AGED 6+ REPORTING QUARTERLY PER MARKET ON 6,000+ INTERVIEWS 24,000 INTERVIEWS PER QUARTER ACROSS EUROPE from Q3 2012 from Q1 2013 9

- 10. HOW MANY PEOPLE GAME? 10

- 11. WHAT ARE THE MAIN FORMS OF GAMING? Base: all 6+ population % Play... Q3 2012 Q4 ‘11 Any video gaming 20m people 35% 38% ANY Packaged 22% 26% ANY Apps 14% 12% ANY Online 19% 18% Downloads 8% 8% Social 8% 8% Multiplayer 8% 8% Browser game sites 8% 6% 11

- 12. HOW DIFFERENT IS GAMING BY AGE? 12

- 13. % PLAY ANY PACKAGED GAMES Base: all 6+ population 100% % Play... % Q3 2012 75% % Q4 2011 PACKAGED 50% 25% 0% 6 to 10 11 to 14 15 to 24 25 to 34 35 to 44 45+ % point -1% +5% -5% -7% -9% -2% Change 13

- 14. % PLAY ANY APP GAMES Base: all 6+ population 100% % Play... % Q3 2012 75% % Q4 2011 APPS 50% 25% 0% 6 to 10 11 to 14 15 to 24 25 to 34 35 to 44 45+ % point +9% +11% +1% +2% +2% +2% Change 14

- 15. % PLAY ANY ONLINE GAMES Base: all 6+ population 100% % Play... % Q3 2012 75% % Q4 2011 ONLINE 50% 25% 0% 6 to 10 11 to 14 15 to 24 25 to 34 35 to 44 45+ % point +6% +4% +2% +1% -2% +1% change 15

- 16. WHAT DEVICES ARE BEING USED TO GAME ON? 16

- 17. WHAT DEVICES ARE BEING USED TO GAME ON? Base: all 6+ population % Play devices... Q3 2012 Q4 ‘2011 Play any device 20m people 35% 38% CONSOLES 24% 27% COMPUTERS 24% 26% SMARTPHONE / iPODs 18% 17% PORTABLES 11% 12% TABLETS 7% 4% 17

- 18. WHAT IS DRIVING MARKET VALUE, VOLUME, AND TIME 18

- 19. % SHARE OF TOTAL MARKET: VALUE Base: 11+ in the UK, % SHARE OF TOTAL VALUE £972m £292m £235m £321m ONLINE APPS PACKAGED Q4 2011 Q1 2012 Q2 2012 Q3 2012 19

- 20. % SHARE OF TOTAL MARKET: VOLUME Base: 11+ in the UK, % SHARE OF VOLUME 93m 49m 40m 51m ONLINE APPS PACKAGED Q4 2011 Q1 2012 Q2 2012 Q3 2012 20

- 21. % SHARE OF TOTAL MARKET: GAMING TIME Base: 11+ in the UK, % SHARE TOTAL GAMING TIME IN TYPICAL WEEK 154m 155m 160m 156m hrs/wk hrs/wk hrs/wk hrs/wk ONLINE APPS PACKAGED Q4 2011 Q1 2012 Q2 2012 Q3 2012 21

- 22. WHAT IS DRIVING THE SHARE OF TIME IN THE GAMES MARKET? % SHARE TOTAL GAMING TIME Q3 2012 Portable 5% Console PS3 11% Downloads 7% 34% Paid Free Console Xbox 360 X% Console X% X% Game sites 5% Wii X% PC X% X% PC/Mac Other Social 11% 12% X% Other X% X% Total X% X% 156m Multiplayer 11% hrs/wk Other Other Android 4% Paid Free X% X% iOS 10% Paid Free X% X% 22

- 23. WHAT IS THE MACRO VIEW OF THE MARKET NOW? 23

- 24. WHERE IS THE MARKET NOW? Base: all 11+ population Size of the bubble is the share total value of market Q3 2012 PLAY REACH - % PLAY IN POPULATION Q2 2012 Q1 2012 Q4 2011 TIME SPENT – % SHARE OF TOTAL GAMER HOURS 24 D2, B3

- 25. IN SUMMARY 25

- 26. IN SUMMARY Gaming is an increasingly complex and currently fragmented market Kids embrace multiple gaming formats, indicating where the market is heading What drives market VALUE is not the same as what drives VOLUME and TIME Market dynamics shifting: low revenue formats take significant share of time HOW WILL THESE DYNAMICS TREND OVER TIME AND WHAT ARE THE LONG TERM IMPACTS? 26

- 27. February 2013 Thriving in the Mobile First Economy Richard Firminger, GM, EMEA

- 28. Topics Flurry Background and Services App Consumption Trends WW Freemium, Virtual Goods, Advertising & ARPDAU Loyalty Matrix by Games Genre

- 29. Flurry Track Record Number 1 Mobile Reach Monthly Unique Users 850M Number 1 Analytics Application Developers 95K Applications 290K Monthly Unique 74B Sessions Number 2 Ad Network Monthly Clips 130M

- 30. Flurry Two-Sided Advertising Platform • Publishers: Direct, Indirect, desk-traded ad monetization • Advertisers: Ad effectiveness, measurement and ROI analysis • Built-in network effects

- 31. Unstoppable Market Growth Worldwide in-application events measured by Flurry (billions) 1,200 1,100 1,000 900 800 700 600 500 400 300 200 100 - May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov Jan Mar May Jul Sep Nov 08 08 08 08 09 09 09 09 09 09 10 10 10 10 10 10 11 11 11 11 11 11 12 12 12 12 12 12 Source: Flurry Analytics, May 2008 – November 2012, Billions

- 32. Competition for Consumers Continues to Increase Over 1.4 million available apps on iOS and Android GOOGLE PLAY iTUNES APP STORE 700 675 650 600 600 500 460 425 400 350 250 250 200 160 80 28 20 2 March 2009 December 2009 August 2010 May 2011 July 2011 October 2011 April 2012 June 2012 September 2012 Sources: Google, Apple; number in thousands

- 33. Addressable Market to Surpass 1 Billion Next Year Active smartphone & tablet devices Total Addressable Market Aggressive: 5B WW Mobile Device Owners Conservative: 2B WW Adults, Middle Class or higher 1.1 B Upside: Smartphones – dropping prices, especially Android Tablets – little replacement, mainly new; sub for PCs Connected TVs – to be shipped Reference: 800 M 2.3 Billion Internet Subscribers today 331 M 76 M 23 M Aug 2009 Aug 2010 Aug 2011 Aug 2012 Aug 2013E Source: Flurry Analytics

- 34. A Global Phenomenon Top Countries by Active iOS & Android Devices (millions) 181 167 35 28 27 22 19 19 14 14 US China UK Japan S. Korea Germany France Canada Brazil Spain Source: Flurry Analytics active devices Oct 2012

- 35. 30+ Countries Doubled in Last 12 Months Fastest Growing iOS & Android Markets by Active Devices 293% 269% 260% 235% 209% 202% 197% 181% 180% 180% China Vietnam Colombia Chile Ukraine Venezuela Turkey Philippines Egypt Russia Source: Flurry Analytics, Oct 2011 – Oct 2012, countries with at least 500k active devices as of Oct 2011

- 36. App Economy Expanding Internationally Distribution of iOS and Android App Sessions 100% 25% 90% 80% 32% 70% 60% 27% 50% 39% 40% 48% 30% 20% 10% 29% 0% Oct 2011 Oct 2012 UNITED STATES (TOP RANK) REST OF TOP 10 (RANKS 2 – 9) REST OF WORLD Source: Flurry Analytics

- 37. How Mobile Stacks Up Against TV and The Web Web vs. Mobile App vs. TV Consumption, Minutes per Day 180 160 140 162 168 168 120 100 127 80 94 60 40 70 66 72 70 20 - Dec 2010 Dec 2011 Dec 2012 Web Browsing Mobile Applications Television Sources: comScore, Alexa, U.S. Bureau of Labor Statistics, Flurry Analytics

- 38. Tablet Usage More Games & Entertainment Oriented Time Spent per Category, Smartphones versus Tablets Productivity Entertainment News 1% 3% 2% Other Other Lifestyle Utilities 11% 7% 3% 4% Health & Fitness Games Entertainment 3% 39% 9% Social Utilities Networking 17% 10% Games 67% Social Networking 24% Smartphones Tablets

- 39. App Revenue Is Scaling 20 Billions 18 16 14 12 10 8 6 4 2 0 2008 2009 2010 2011 2012 Virtual Goods Advertising Source: eMarketer, Mary Meeker (KPCB)

- 40. Gaming: Money, Midcore and Maturity ARPDAU among top 1,000 grossing iOS free-to-play games Over $0.75, 3% Over $0.75, $0.25 - $0.75 15% 15% Under $0.25, 53% $0.25 - $0.75 Under $0.25, 32% 82% Sep 2011 Sep 2012 Source: Flurry Analytics, 480 free-to-play games

- 41. Loyalty by Application Category

- 42. Mobile Game Loyalty Matrix (Freemium, iOS)

- 43. Mobile Game Age & Gender Matrix (Freemium, iOS)

Notas do Editor

- At the overall level it is interesting to see levels of gaming but how do these levels differ by AGE

- The idea – dev should consider the METRICS and DEMOGRAPHICS of genresDo RESOURCES and capabilities align? Your DESIGNER has a kick-ass PvP or Endless Runner. Can you address the PREDICTABLE behaviors of that genre? Can you Acquire, Retain, and Monetize? Optimizing a game, team, and live operations AROUND METRICS. Should be CRITICAL to business strategy Going to give MARKET data to set context. Then new RESEARCH. research we just released this morning on the specific retention, usage metrics, and demographics of nine of the most popular free2play genres.

- This overcrowding increased the competition for consumers. There has beenan explosion in the number of apps across Android and iOS. Today, there are over a million unique apps to choose from. With this kind of competition for shelf space and consumers, no wonder discovery is top of mind for every developer around the world.

- 487 in Feb519 in March529 in April

- With all these apps…FEAR not…games STILL RULE rule!Phones productive 20% of time. LESS on tablets. These are GAMING devices! SUPERCELL is tablet-first. iPad = iPhone revenue

- Recently, Flurry examined key loyalty metrics for a wide range of apps. PEEL the ONION on the games category. Examine GENRESHow do METRICS differ? WHO is playing each?

- Quadrant 1 - “sweet spot” – used INTENSIVELY for long DURATION. Manyimpressions, but also IAP. APPOINTMENT mechanics to maintain and progress their experience. SOCIAL mechanics + CLASSIC gameplay “evergreen” gameplay for Social Turn-Based. RE-ENGAGEMENTQuad 2 – STRATEGY. not for FAINT ofheartThe audience is DEMANDING,lifecycles are short, LIVE SERVICES must be flawless. MVP not good enoughPvP and PACEChurn through CONTENT quickly. Have content readyQuad 3 – FICKLE and fewer sessions to monetizeCard-Battle impressive given short timeframe. TARGETED user acquisition. Most drop off quickly due to the “hardcore”Quad 4 – EASY, REPEATABLE for years. Low IAP b/c lack DEPTHSubstantialADVERTISING X-PROMO

- Quadrant I middle-aged FEMALES, attractive retention and usage metrics. Quadrant II - males GRADUATE to poker Quadrant III – HOT sector. Young, male “core” gamers coming to the devices and opening WALLETSDifficult to corral, but can monetize amazingly. Quadrant IV - younger females, more INVOLVED gameplay than middle-agedYOUNGEST quick solo experience of the Endless genreLatetwenties / early thirties use gameplay mechanics and SOCIAL