FirstPartner Mobile Payments and Banking Market Map 2014

Full PDF version downloadable at www.firstpartner.net. This updated Market Map provides an essential visual overview of the Mobile Payments & Banking market landscape. It includes NFC and other proximity payments, Mobile Commerce, Mobile Money in developed and developing markets and Mobile Banking. It describes typical target customer segments, differences between key geographic markets and the role of Mobile Wallets. The map gives a concise overview of the service provision and technology value chain and the roles played by Mobile Network Operators, banks, Payment Service Providers, payment networks and technology vendors. Key players are named and important trends and figures are highlighted. FirstPartner is an independent research and proposition development company specialising is areas including Payments, Mobile Advertising, Mobile Value Added Services and M2M. For more information visit www.firstpartner.net

Recomendados

Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

FirstPartner Mobile Payments and Banking Market Map 2014

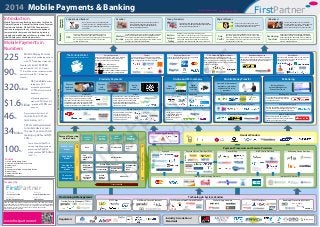

- 1. 2014 Mobile Payments & Banking +44 (0)870 874 8700 FirstPartnerwww.firstpartner.net Regulators Industry Associations / Standards USA The US has been at the forefront of mobile payments innovation in Western markets however offerings are fragmented and true mass market adoption is still some way off. The largest consortium Initiative, ISIS, launched nationwide in Nov 2013. Eastern Europe/ Turkey Western Europe Asia Pacific Developing Countries The powerful Sony/NTT DoCoMo alliance in Japan and aggressive deployment by Korean carriers has put Asia in the lead in mobile payment deployment. NTT DoCoMo, China Mobile and KT have announced standards for NFC roaming between countries. With large unbanked populations, developing countries have been at the forefront of mobile banking/payment innovation. Kenya's M-PESA demonstrated the potential and similar services are now widely deployed. National carrier consortia are forming to facilitate co-ordinated NFC payment ecosystems, often including retail banks and card networks. Money transfer agencies are embracing mobile as a remittance and bill payment channel and partnering aggressively with carriers to deliver international services. Retail banks lead some MMT services and will be the consumer channel for many mobile wallet and proximity payment services. Carrier Consortia Carriers Payment Processors OS & Hardware Platform Owners Remittance Agencies Retail Banks Migrant Worker Often cash centric, the need to send money home drives use of international and domestic remittance services. Have regular needs to transfer money between family members and for parental control of spend. Potential adopters of mobile money transfer in developed markets. Low payment card ownership, high levels of group social activity and comfort with mobile devices makes this segment likely early adopters. Unbanked Those without ready access to traditional banking facilities, or having a low propensity to use them for cultural reasons. Mobile makes essential financial service accessible. Sophisticated Banked Families Acceptance Carriers are leading and branding many Mobile Money Transfer and NFC services, partnering with banks and payment processors as required. Leading Payment Processors are launching mobile wallets supporting multiple services. Google and Apple combine leading handset platforms with high levels of consumer engagement and established payment processing capabilities. Google Wallet launched in 2011 and an Apple launch is widely speculated on. Proximity Payments On-line and M-Commerce Mobile Money Transfer M-Banking PaymentServices Physical Goods and Services Transport and Ticketing Loyalty and Couponing Mobile NFC Other Contactless Acceptance Terminals Mobile Point of Sale Reader equipped smartphones and tablets enable micro merchants and roving sales people to easily accept card and mobile payments. E&M Commerce Digital Goods and Services Domestic & international remittance; sole trader, merchant, bill & salary payments Balance Enquiry, Account Management, Money Transfer, etc. Carrier and In App Billing E&M Wallet Carrier Billing In App Billing Stored value or payment account linked M-Wallets support a simplified M-commerce payment experience. Mobile Money Transfer for the Unbanked Person to Person and Small Trader Payments International Remittance Banking the Unbanked Driving Convenience Mobile Authentication Banks in developed markets are widely deploying app and browser based M-Banking services to give consumers greater flexibility and choice. Mobile delivered one time passwords provide a convenient strong authentication tool for on-line financial services. Using the mobile to provide banking services where branch infrastructure and adoption is poor. Consumer Segments Young Socialisers • ISIS,:Verizon, AT&T, T-Mobile • Weve: Vodafone, EE, Telefonica UK • TDC, Telenor, TeliaSonera, Three • Mpass: Deutsche Telekom, Vodafone, Telefonica • Cityzi: Orange, Bouygues, SFR, NRJ Mobile The Mobile Wallet The battleground for the consumer Technology & System Vendors NFC Chips SIM Based Secure Elements Banking & Processing SystemsWallet & App Vendors Mobile payment for transport ticketing is well established in a number of countries. Turkey and Poland are among the most advanced payment markets in Europe with widespread deployment of contactless acceptance infrastructure and NFC services launched. The pace of mobile payments launches in Europe accelerated in 2013 & early 2014 with first commercial deployments of VisaV.me, MasterCard MasterPass,VodafoneWallet and Orange Cash. Signifcant upcoming launches include services from the French bank consortium AFSCM. NFC is the most widely backed technology for "touch and go" payments, ticketing and PoS promotions. Market adoption is dependent on compatible handset and terminal penetration. The adoption of Host Card Emulation by card companies facilitates carrier independent services. NFCStickers,MicroSDCards&Sleeves Heavy users of cards, on-line banking and e-commerce services . Mobile commerce and banking services fulfil needs for immediacy and control. Apple’s iBeacons and PayPal Beacons both based on Bluetooth Low Energy (BLE) may herald a significant alternative to NFC. Other technologies being deployed include QR codes, SMS and MF Tones and cloud based services. MMT Platforms Handset Vendors Payment Processors and Service Providers Acquirers Payment Service Providers (PSPs) Carrier Billing Couponing and Loyalty Consumer Account Provider Source of Funds Funds Transfers Funds Withdrawal / Settlement The Four Party Model Bank Wallet Provider • Card • Stored Value • Bank Carrier Bill/Prepaid Balance Mobile Network Operator • Carrier Bill • Mobile Money Agent • Mobile Wallet • Agent • Bank Mobile PSP Bank/Interbank Network Mobile Network Operator Partner Bank Issuer Card Network • Acquirer • PSP The E-Wallet Model The Mobile Money Transfer Model The Carrier Billing Model Transaction Fee Payment Processing Value Chain Card & Debit Processing Networks MMT Service Providers M-Banking Service Providers Interbank ACH Networks Merchant/ConsumerFacing Markets Mobile Trusted Service Managers (TSMs) Provisioning & Management The map includes information compiled from interviews and information available in the public domain. As information sources are outside our control, FirstPartner makes no representation as to its accuracy or completeness. Responsibility for any interpretation or actions based on this map lies solely with the reader. Copyright FirstPartner Ltd 2014 Prepared by +44 (0) 870 874 8700 FirstPartner find us atcall us on www.firstpartner.net email us at @firstpartner www.firstpartner.net Introduction Mobile Payments and Banking remain key for Mobile Network Operators, Financial Institutions and Payment Providers worldwide. While NFC PoS deployments continue to progress slowly, consumer adoption of remote mobile commerce and banking is growing strongly and mobile money schemes continue to be widely deployed in developing markets. Mobile Payments in Numbers Sources (1) GSMA Mobile Money Tracker (2) Safaricom Half Year Results 2013-2014 (3) ABI Research (4) Gartner (5) Chinese Central Bank - People’s Bank of China (6) Mobey Forum (7) ABI Research Feb 2014 (8) PayPal inc. 225 Mobile Money Services deployed in developing nations with 115additional planned (1) 90% Growth in P2B & B2P M-PESA transactions 2012-2103. Overall 11.6 million active customers make paments worth$1.1 Billion per month (2) 320Million NFC enabled devices shipped in 2013 accounting for around 17.5% of total mobile handsets 3, 4) $1.6Trillion of mobile payments made in China in 2013 - growth of 318% year on year(5) 46% Projected market share of mobile Point of Sale terminals by 2017(6) 100% Year on Year Growth in value of mobile payments processed by PayPal, which reached $27 billion in 2013. (8) 34Billion Tickets will be delivered to mobile devices over the next 5 years with QR making up 48% and NFC 30% (7) follow us hello@firstpartner.net FirstPartner EVALUATION COPY