Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (20)

Semelhante a 6 August Daily market report

Semelhante a 6 August Daily market report (20)

Mais de QNB Group

Mais de QNB Group (20)

6 August Daily market report

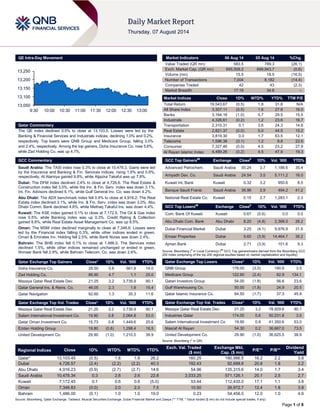

- 1. Page 1 of 8 QE Intra-Day Movement Qatar Commentary The QE index declined 0.5% to close at 13,103.5. Losses were led by the Banking & Financial Services and Industrials indices, declining 1.0% and 0.2%, respectively. Top losers were QNB Group and Medicare Group, falling 3.0% and 2.4%, respectively. Among the top gainers, Doha Insurance Co. rose 5.6%, while Zad Holding Co. was up 4.7%. GCC Commentary Saudi Arabia: The TASI index rose 0.3% to close at 10,478.3. Gains were led by the Insurance and Banking & Fin. Services indices, rising 1.6% and 0.9%, respectively. Al Alamiya gained 9.8%, while Aljazira Takaful was up 7.8%. Dubai: The DFM index declined 2.4% to close at 4,726.6. The Real Estate & Construction index fell 3.5%, while the Inv. & Fin. Serv. index was down 3.1%. Int. Fin. Advisors declined 6.1%, while Gulf General Inv. Co. was down 4.2%. Abu Dhabi: The ADX benchmark index fell 0.9% to close at 4,916.2. The Real Estate index declined 3.1%, while Inv. & Fin. Serv. index was down 3.0%. Abu Dhabi Comm. Bank declined 4.8%, while Methaq Takaful Ins. was down 4.4%. Kuwait: The KSE index gained 0.1% to close at 7,172.5. The Oil & Gas index rose 0.5%, while Banking index was up 0.3%. Credit Rating & Collection gained 8.8%, while Real Estate Asset Management Co. was up 8.5%. Oman: The MSM index declined marginally to close at 7,346.8. Losses were led by the Financial index falling 0.3%, while other indices ended in green. Oman & Emirates Inv. Holding fell 2.5%, while Bank Nizwa was down 2.4%. Bahrain: The BHB index fell 0.1% to close at 1,486.0. The Services index declined 1.5%, while other indices remained unchanged or ended in green. Ithmaar Bank fell 2.9%, while Bahrain Telecom. Co. was down 2.6%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Doha Insurance Co. 28.50 5.6 561.9 14.0 Zad Holding Co. 86.90 4.7 1.1 25.0 Mazaya Qatar Real Estate Dev. 21.25 3.2 3,739.9 90.1 Qatar General Ins. & Reins. Co. 46.05 2.3 1.8 15.4 Qatar Navigation 92.60 1.3 30.3 11.6 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Mazaya Qatar Real Estate Dev. 21.25 3.2 3,739.9 90.1 Salam International Investment Co. 19.90 0.8 2,064.8 53.0 Qatar Oman Investment Co. 15.73 0.8 1,449.6 25.6 Ezdan Holding Group 19.80 (0.8) 1,298.4 16.5 United Development Co. 29.90 (1.0) 1,210.5 38.9 Market Indicators 06 Aug 14 05 Aug 14 %Chg. Value Traded (QR mn) 583.5 789.3 (26.1) Exch. Market Cap. (QR mn) 695,508.2 699,943.7 (0.6) Volume (mn) 15.5 18.5 (16.5) Number of Transactions 7,004 8,182 (14.4) Companies Traded 42 43 (2.3) Market Breadth 17:19 34:6 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 19,543.67 (0.5) 1.8 31.8 N/A All Share Index 3,307.11 (0.5) 1.6 27.8 16.0 Banks 3,164.16 (1.0) 0.7 29.5 15.5 Industrials 4,326.61 (0.2) 1.2 23.6 16.7 Transportation 2,310.31 0.1 3.6 24.3 14.8 Real Estate 2,821.37 (0.0) 5.0 44.5 15.2 Insurance 3,819.30 0.0 1.7 63.5 12.1 Telecoms 1,596.38 (0.1) 1.2 9.8 22.6 Consumer 7,327.46 (0.0) 4.5 23.2 27.9 Al Rayan Islamic Index 4,489.26 (0.2) 4.5 47.9 19.3 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Advanced Petrochem. Saudi Arabia 55.24 3.7 1,188.6 35.4 Arriyadh Dev. Co. Saudi Arabia 24.54 3.5 5,111.2 16.0 Kuwait Int. Bank Kuwait 0.32 3.2 950.6 8.5 Banque Saudi Fransi Saudi Arabia 36.96 2.9 494.2 41.2 National Real Estate Co. Kuwait 0.15 2.7 1,283.1 2.3 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Com. Bank Of Kuwait Kuwait 0.67 (5.6) 0.0 0.5 Abu Dhabi Com. Bank Abu Dhabi 8.20 (4.8) 2,368.0 26.2 Dubai Financial Market Dubai 3.25 (4.1) 9,976.9 31.6 Emaar Properties Dubai 9.60 (3.9) 14,464.7 38.2 Ajman Bank Dubai 2.71 (3.9) 101.6 9.3 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% QNB Group 178.00 (3.0) 190.9 3.5 Medicare Group 122.90 (2.4) 92.9 134.1 Qatari Investors Group 54.00 (1.8) 56.6 23.6 Gulf Warehousing Co. 50.00 (1.8) 24.9 20.5 Qatar Islamic Insurance Co. 84.50 (1.7) 37.3 45.9 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Mazaya Qatar Real Estate Dev. 21.25 3.2 78,929.6 90.1 Industries Qatar 174.00 0.6 50,231.8 3.0 Salam International Investment Co 19.90 0.8 41,350.6 53.0 Masraf Al Rayan 54.30 0.2 36,667.0 73.5 United Development Co. 29.90 (1.0) 36,625.5 38.9 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 13,103.45 (0.5) 1.8 1.8 26.2 160.25 190,986.5 16.2 2.2 3.8 Dubai 4,726.57 (2.4) (2.2) (2.2) 40.3 192.43 92,688.8 20.8 1.8 2.2 Abu Dhabi 4,916.23 (0.9) (2.7) (2.7) 14.6 54.96 135,315.6 14.0 1.7 3.4 Saudi Arabia 10,478.34 0.3 2.6 2.6 22.8 2,033.25 571,126.1 20.1 2.5 2.7 Kuwait 7,172.45 0.1 0.6 0.6 (5.0) 53.44 112,435.0 17.1 1.1 3.8 Oman 7,346.83 (0.0) 2.0 2.0 7.5 10.50 26,972.7 12.4 1.8 3.8 Bahrain 1,486.00 (0.1) 1.0 1.0 19.0 0.23 54,456.0 12.0 1.0 4.6 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 13,050 13,100 13,150 13,200 13,250 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 8 Qatar Market Commentary The QE index declined 0.5% to close at 13,103.5. The Banking & Fin. Services and Industrials indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. QNB Group and Medicare Group were the top losers, falling 3.0% and 2.4%, respectively. Among the top gainers, Doha Insurance Co. rose 5.6%, while Zad Holding Co. was up 4.7%. Volume of shares traded on Wednesday fell by 16.5% to 15.5mn from 18.5mn on Tuesday. However, as compared to the 30-day moving average of 14.7mn, volume for the day was 4.9% higher. Mazaya Qatar Real Estate Dev. and Salam International Investment Co. were the most active stocks, contributing 24.2% and 13.4% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change AIG MEA Limited (AMEA) S&P Dubai LT CCR/IFSR – A/A – Stable – Bank of Sharjah (BOS) CI Abu Dhabi FSR/LT FCR/ST FCR/SR BBB+/A-/A2/2 BBB+/ A- /A2/2 – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Currency Ratings, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, IFSR – Insurer Financial Strength Rating, CCR – Counterparty Credit Rating) Earnings Releases Company Market Currency Revenue (mn)2Q2014 % Change YoY Operating Profit (mn) 2Q2014 % Change YoY Net Profit (mn) 2Q2014 % Change YoY Dana Gas Abu Dhabi AED 685.0 29.7% – – 169.0 69.0% Al Anwar Holding* Oman OMR 2.4 25.7% – – 1.6 27.8% Dhofar Cattle Feed Co. Oman OMR 15.0 4.4% – – -1.7 NA Nass Corporation Bahrain BHD 20.2 4.3% – – 1.3 237.6% Source: Company data, DFM, ADX, MSM (* 1Q2015 results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 08/06 US MBA MBA Mortgage Applications 1 August 1.60% – -2.20% 08/06 US US Census Bureau Trade Balance June -$41.5B -$44.8B -$44.7B 08/06 EU Markit Markit Eurozone Retail PMI July 47.6 – 50.0 08/06 France Markit Markit France Retail PMI July 45.6 – 47.6 08/06 Germany Markit Markit Germany Construction PMI July 48.2 – 45.5 08/06 Germany Markit Markit Germany Retail PMI July 52.1 – 56.2 08/06 UK ONS Industrial Production MoM June 0.30% 0.60% -0.60% 08/06 UK ONS Industrial Production YoY June 1.20% 1.50% 2.30% 08/06 UK ONS Manufacturing Production MoM June 0.30% 0.60% -1.30% 08/06 UK ONS Manufacturing Production YoY June 1.90% 2.10% 3.70% 08/06 UK NIESR NIESR GDP Estimate July 0.60% – 0.80% 08/06 Italy ISTAT Industrial Production MoM June 0.90% 0.80% -1.20% 08/06 Italy ISTAT Industrial Production WDA YoY June 0.40% -1.10% -1.70% 08/06 Italy ISTAT Industrial Production NSA YoY June 0.40% – -4.80% 08/06 Italy Markit Markit Italy Retail PMI July 43.4 – 43.8 08/06 Italy ISTAT GDP WDA QoQ 2Q2014 -0.20% 0.10% -0.10% 08/06 Italy ISTAT GDP WDA YoY 2Q2014 -0.30% 0.10% -0.40% 08/06 Japan ESRI Leading Index CI June 105.5 105.5 104.8 08/06 Japan ESRI Coincident Index June 109.4 109.6 111.3 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) Overall Activity Buy %* Sell %* Net (QR) Qatari 62.31% 64.88% (15,000,368.46) Non-Qatari 37.68% 35.11% 15,000,368.46

- 3. Page 3 of 8 News Qatar Qatar set to award projects worth $26.2bn – Qatar will award projects worth $26.2bn in 2014 as compared to $9.4bn in 2013. According to latest figures released by construction intelligence firm Ventures Onsite, the infrastructure project awards across the GCC are forecasted to exceed $86bn in 2014, indicating an increase of 77.8% over 2013. In the UAE, projects worth $15.18bn will be awarded, almost five times more than what was awarded in 2013, while in Oman infrastructure awards are expected to reach $7.4bn. Bahrain, which awarded projects worth $382mn in 2013, is expected to award $3.4bn. Kuwait is expected to award projects worth $3.45bn. Saudi Arabia’s forecasted award of $29.34bn — the highest in the region — represents a YoY decrease. The infrastructure projects make up 16% of the total construction value of GCC projects, and rail projects like the Riyadh Metro are the main beneficiary. According to Ventures, it is estimated that the rail sector is worth $200bn as the six countries aim for an integrated GCC-wide network by 2018. (Reuters) Qatar infrastructure upgrade drive to boost insurance, transport – The insurance and transport sectors were seen going through their troughs in terms of profitability during 1H2014, but they exhibit inherent intrinsic strengths in view of the country’s capital expenditure-driven economy. The cumulative profit of the insurance sector, under which there are five listed constituents, had fallen 33.26% in 1H2014 as against a stupendous growth of 148.71% in 1H2013. The five national insurers were among the consortium that recently won a big- ticket risk cover contract for Qatar’s mammoth metro rail project, which is now progressing as per the schedule for completion by late 2019. Qatar Rail – which is at the forefront of building a Doha Metro, Lusail Light Rail Transit and Long Distance Freight and Passenger – recently awarded the “single project tunneling and rail construction” insurance to a consortium of national insurance companies that also include Qatar General & Reinsurance, Al Khaleej Takaful Group, Doha Insurance, Qatar Islamic Insurance and Al Koot Insurance and Reinsurance. The listed insurance companies together reported a profit of QR839.28mn in 1H2014 with Qatar Insurance Company contributing about 76%. Their cumulative net profit stood at QR1.26bn in 2013. According to market sources, Qatar’s large- scale investments in infrastructure, including Qatar Rail, is expected to have a positive “spin off” for the insurance sector, which now comes under the ambit of the Qatar Central Bank as part of a single financial regulatory set up. The transport sector, which has three listed constituents, saw its net profit rise 4.65% to QR1.03bn in 1H2014 against 14.26% in the corresponding period of the previous year. (Gulf-Times.com) HotStats: Doha hotels occupancy levels on growth path – Hotels in Doha city experienced an 11.4% growth in occupancy to 75.9% in 1H2014, pushing revenue per available room rates (RevPAR) up by 11.5% to $166.66 despite average room rates (ARR) declining 5.3%. The latest HotStats survey of hotels in five Mena cities noted that the Food & Beverages (F&B) activities generated 45.8% of hotel revenues, which is a high contribution relative to other regional markets. The F&B operations benefited from double-digit growth in revenues coupled with lower departmental expenses and payroll costs, leading Doha’s TRevPAR to grow by 12% during 1H2014. Elevated by the top-line performance, the efficient operating cost control coupled with a 1.5% reduction in payroll expenses, boosted gross operating profit per available room (GOPPAR) by 19.1% to $166.74. (Peninsula Qatar) Two West Bay towers sold for QR1.5bn – Two towers in the posh West Bay area of the city were sold for a staggering QR1.5bn late last month. The transactions took the total value of real estate deals concluded in a week to an all-time high of QR2.76bn. Real estate registration details for the week (July 20 to 24) show that one of the towers, measuring 3,126 square meters in Al Dafna, was sold for a billion riyals. This is one of the highest values recorded for a real estate deal in Qatar’s known history, property market observers say. The second tower, also in Al Dafna, was sold for QR500mn. (Peninsula Qatar) International US Treasury looks to hold more cash to deal with future crises – A senior official said the US Treasury wants to increase its daily cash holdings, a measure that would help Washington pay its bills during a crisis. If adopted, the new policy would help the government in the event an emergency shutdown of markets and left Washington unable to borrow money to pay creditors and other obligations. Treasury Assistant Secretary Matt Rutherford said that holding more cash on hand is a prudent measure. He added that the measures would help public finances weather events like the September 11, 2001 attacks or 2012's Superstorm Sandy, both of which disrupted Wall Street trading. Washington borrows vast sums in weekly auctions to pay its bills. Investors who met Treasury officials on Tuesday urged the government to increase its daily cash holdings to around $500bn. That would be enough to cover about 10 days worth of outlays. A change in policy, however, would not buy the government any additional time if it runs into a legal limit on borrowing next year. The current law will limit the amount of cash Treasury can hold when a cap on federal borrowing becomes binding again in March 2015. The US government suspended the debt ceiling in February 2014. (Reuters) US trade gap at five-month low, to boost second-quarter GDP – The US trade deficit narrowed more than expected in June as petroleum imports dropped to a 3-1/2-year low, suggesting that trade was less of a drag on second-quarter economic growth than initially thought. The Commerce Department said the trade gap shrank 7.0% to $41.5bn, the lowest reading since January. That was smaller than the roughly $44.8bn shortfall the government had assumed in its first snapshot of second-quarter GDP published last week. When adjusted for inflation, the deficit narrowed to $48.8bn from $52.0bn in May. As a result, economists expect the GDP growth estimate for the April-June quarter to be raised by as much as 0.3 percentage point later this month. The government estimated a week ago that trade subtracted 0.61 percentage point from growth during the April-June period. In that report, it said the economy expanded at a 4.0% annual rate during that quarter after shrinking 2.1% in the first three months of 2014. Economists had expected a trade gap of $44.7bn in June, a slight widening from the previously reported $44.4bn May shortfall. The May gap was revised to $44.7bn. Imports fell 1.2% in June, the largest drop in a year, to $237.4bn. That came as petroleum imports declined to $27.4bn, the lowest level since November 2010, from $28.3bn in May. (Reuters) BofA said to near mortgage deal for up to $17bn – According to sources, the Bank of America Corp. (BofA) is nearing a $16bn to $17bn settlement with the US Justice Department to resolve probes into sales of mortgage-backed bonds in the run-up to the financial crisis. Under the proposed terms, the bank would pay about $9bn in cash and the rest in consumer relief to settle federal and state claims. The details of the proposed accord, such as the relief and a statement of facts, are still being negotiated. The outlines of the deal were reached last week

- 4. Page 4 of 8 after a phone call between Attorney General Eric Holder and BofA CEO Brian T. Moynihan. During the July 30 call, Holder said that the government was ready to file a lawsuit in New Jersey if the bank did not offer an amount closer to the department’s demand of about $17bn. BofA separately said it is raising its quarterly dividend to 5 cents a share, while dropping a plan to buy back stock, after securing Federal Reserve approval of its proposal for managing capital. The dividend increase, the first in seven years, had been postponed earlier this year while the company fixed errors in its initial plan submitted to the Fed. (Bloomberg) Standard Chartered faces more US fines as profit drops 20% – Standard Chartered Plc (STAN) said it faces further US fines over efforts to block money laundering and posted a 20% earnings decline on losses in Asia. The London-based bank said the pretax profit, excluding adjustments to the value of the company’s own debt, fell to $3.3bn in 1H2014 from $4.1bn in 1H2013. That matched the average of 11 analysts’ estimates in a Bloomberg survey. Standard Chartered said it is likely to face more penalties after New York’s banking regulator found “certain issues” with its anti-money laundering systems. That’s adding to pressure from disgruntled investors on CEO Peter Sands, as he navigates faltering economies in Asia, where the bank generates about three-quarters of its earnings. The lender posted a $127mn loss in Korea for the period, and said it made provisions for a fraud in China. (Bloomberg) NIESR: UK economic growth slows in May-July – The National Institute of Economic & Social Research said Britain's economy grew at its slowest pace in a year in the three months through July due to virtually flat industrial output. The think tank estimated gross domestic product rose 0.6% during the May- July period of 2014, from the previous three-month period. That marks a slowdown after it increased 0.8% in April-June, and the lowest rate for any three-month period since July last year. NIESR bumped up its 2014 economic growth forecast for Britain to 3.0% in a quarterly update, from 2.9% previously. It does not expect the Bank of England to raise interest rates until February next year – a prospect that signs of a modest slowdown may bolster. Official data showed that the industrial output grew by just 0.3% in June, half the rate economists had forecast. NIESR said the output per person might not recover to its pre-financial crisis level until 2017, citing weak productivity. (Reuters) Draghi outlook menaced by Putin as Ukraine crisis bites – The crisis in eastern Europe could disrupt Mario Draghi’s economic outlook. Evidence is building that the conflict in Ukraine and European Union sanctions against Vladimir Putin’s Russia are undermining a Euro area recovery that the European Central Bank (ECB) president already describes as weak. With the ECB expected to keep interest rates on hold near zero today and refrain from any new policy measures, Draghi is likely to face questions on how he plans to keep the economy on track. The ECB will announce its interest-rate decision in Frankfurt and Draghi will hold a press conference later. All 57 economists in a Bloomberg survey say officials will keep the benchmark rate at 0.15%. The Bank of England’s Monetary Policy Committee is also predicted to leave its key interest rate unchanged, at a record-low of 0.5%, when it meets in London. (Bloomberg) German orders fall at their sharpest rate in almost three years in June – German industrial orders slid in June at their steepest rate since September 2011 as Euro zone demand fell and geopolitical risks made firms cautious, suggesting this sector of Europe's largest economy will have a weak start to the third quarter. According to the Economy Ministry data, contracts fell by 3.2% on the month as orders from the single currency bloc plunged by 10.4%. That missed the Reuters consensus forecast for a 1.0% rise and undershot even the lowest estimate for a 0.5% decrease. Senior economist at ING, Carsten Brzeski said while a stagnation of the German economy in the second quarter seems hard to avoid, the industrial engine is losing some fuel. A breakdown of data showed foreign orders slumped by 4.1%, with economists attributing this mainly to weakness in the single currency bloc rather than the Ukraine crisis. German firms also held back, with domestic orders down by 1.9%. (Reuters) China July data to give clues on recovery strength, more stimulus – A raft of China data over the coming week will give the first indications of the economy's third-quarter performance, after conflicting signals suggested that more stimulus measures may be needed to ensure a sustained recovery. While manufacturing appears to have picked up, thanks largely to government-backed measures and a modest resurgence in exports, data this week showed sudden and unexpected weakness in the services sector. The decline appeared linked to the cooling property market, which may be facing a prolonged slump that could hurt related businesses and dampen consumer confidence. A Reuters poll of 30 economists shows the factory output likely held steady in July, while overall investment growth ticked higher, chiming with expectations that a flurry of pro- growth steps from Beijing earlier this year is paying dividends. Anecdotal evidence, however, suggests property investment, sales and construction could show a seventh month of deterioration, suggesting the sector will be an increasing drag on activity even if other parts of the world's second-largest economy are gaining traction.(Reuters) Regional EIU: Food imports by Gulf countries to touch $53.1bn by 2020 – According to the Economist Intelligence Unit (EIU), the value of food imports by Gulf Cooperation Council (GCC) countries is forecasted to reach $53.1bn by 2020. The EIU attributes the expected increase to the fact that 90% of the Gulf's current food demands are met with imports, an over- reliance caused by climatic conditions and land use restrictions. However, the regional imports far exceed demand and the GCC's position as a major logistics hub for the global food industry is aided by significant re-export trade. Meanwhile, the Dubai Multi Commodities Center (DMCC) figures show that the UAE currently re-exports nearly 50% of its imported food products to other GCC countries, Russia, India, Pakistan and East Africa. One of the world's biggest re-exporters of goods such as coffee, tea, sugar and rice, the UAE was responsible for approximately 90% of global rice re-exports in 2010. With regional food demand set to grow, the World Bank projects the MENA region's food market to exceed $1tn by 2030. (GulfBase.com) Ramco wins order from Falcon Aviation Services – Ramco Systems has signed an agreement with Middle East based Falcon Aviation Services, with Falcon becoming its 65th aviation customer. As per the agreement, Ramco will provide its complete engineering, materials management, maintenance, quality, flight operations, and MRO modules along with ERP financials, HR and payroll. (GulfBase.com) Rising interest rates may revive appetite for Islamic commodity deals – A return to an era of higher interest rates could derail attempts by Islamic finance to create alternatives to a short-term funding instrument that has dominated the industry, but which some scholars and regulators want to see replaced. Islamic finance has been trying to diversify away from so-called commodity murabaha, a common cost-plus profit arrangement, in an attempt to reduce reliance on a single tool, stop money from "leaking" to western banks, and find instruments closer to

- 5. Page 5 of 8 the principles of sharia-compliant financing. Saudi banks alone handled nearly $20bn a day of murabaha transactions back in 2006, but western banks largely deserted the market after the 2008 financial crisis, turning instead to central banks as a source of cheap funds. Islamic finance has developed alternative inter-bank tools, but higher interest rates are expected to boost murabaha trading, luring back western borrowers looking for cheap finance and Islamic banks seeking better returns on surplus funds. (Reuters) Saudi organizations’ foreign assets reach SR385.3bn – Saudi organizations, including the Saudi Arabian Monetary Agency (SAMA) and Public Investment Fund (PIF), had financial assets totaling SR385.3bn in foreign countries in June 2014. The assets in foreign countries amounted to 63% of their total assets. The total assets of these organizations rose to SR608.3bn by the end of June 2014, showing an increase of SR4bn (1%), as compared to May 2014. The amount was down SR6bn as compared to the assets of SR614.3bn in June 2013. (GulfBase.com) Astra Group secures SR877.5mn Islamic Banking Facilities from SABB – Astra Industrial Group has signed Islamic Banking Facilities agreement with The Saudi British Bank (SABB) for an amount of SR877.5mn. The term of the loan is 6 years ending on August 6, 2020. Astra Group is aiming to use the loan amount to fund the capital expenditure. (Tadawul) SAMA approves UCA’s SR210mn capital increase through rights issue – The Saudi Arabian Monetary Agency (SAMA) has approved United Cooperative Assurance Company’s (UCA) request to raise its capital by SR210mn through a rights issue. The reasons for capital increase are to maintain the solvency margin of the business and support the future growth of the company. (Tadawul) AM Best withdraws ratings of TUCI – AM Best has removed from under review with negative implications and downgraded the financial strength rating to B+ (Good) from B++ (Good) and the issuer credit rating to "bbb-" from "bbb" of Trade Union Cooperative Insurance Company - A Saudi Joint Stock Company (TUCI). The outlook assigned to the ratings is negative. Concurrently, AM Best has withdrawn the ratings due to managements' request to no longer participate in AM Best's interactive rating process. (AM Best) Al-Khodari terminates remaining JV agreement with Al Arfaj Group – Abdullah A. M. Al-Khodari Sons Company (Al-Khodari) has terminated the remaining joint venture agreement with Abdullatif M. Al Arfaj & Brothers Holding Company (Al Arfaj Group). The agreement is concerning the replacement and upgrading of infrastructure of King Khaled Hospital in Hail. The JV agreement is terminated due to the cancellation of this project by the Ministry of Health. This was the last JV agreement between the two groups out of the six agreements signed. (Tadawul) Bank AlJazira reports net income of SR326.04mn in 1H2014 – Bank AlJazira reported net income of SR326.04mn for 1H2014 as compared to SR311.64mn in 1H2013. Net income for 2Q2014 was SR166.7mn as compared to SR167.4mn in 2Q2014. EPS for 1H2014 amounted to SR0.82 as against SR0.78 in 1H2013. Bank registered total operating income of SR1.09bn in 1H2014 as against SR891mn in 1H2013. Total assets as of June 30, 2014 stood at SR65.80bn as against SR59.98bn as of December 31, 2013. Net loans & advances as of June 30, 2014 stood at SR38.97bn, while customer deposits were SR51.84bn. (Bloomberg) UAE CB to link switch with China Union Pay – The UAE Central Bank (USE CB) is set to link the UAE Electronic Switch with China Union Pay, which is China’s electronic switch. This move will enable Chinese tourists and traders to withdraw cash from the automatic telling machines (ATMs) across the UAE. The UAE CB decision comes following the recent substantial increase of Chinese tourists and traders. This procedure would allow Chinese tourists to easily withdraw cash using their debit cards issued by Chinese banks from UAE ATMs, knowing that previously they could withdraw money only by credit cards and that exaggerated fees were imposed on such withdrawals if made outside China. (GulfBase.com) TIME Hotels wins management contract for five-star Egypt property – UAE-headquartered hospitality company, TIME Hotels Management, has bagged the management contract for a luxury five-star property in the upmarket development of Sahl Haseesh, on Egypt’s Red Sea coast. Constructed by Egyptian developer Prime Estates International, the TIME Renero Resort Azzurra and TIME Suites Azzurra are located within the Azzurra project. The low-rise landscaped hotel, which will open under the TIME Hotels banner in November 2014, offers a total of 87 guestrooms and 110 suites, with the residences comprising a collection of 287 one, two and three-bedroom luxurious homes. (Bloomberg) EIBank reports net profit of AED35.3mn in 1H2014 – Emirates Investment Bank (EIBank) reported a net profit of AED35.3mn in 1H2014 as compared to AED27.8mn in 1H2013, reflecting an increase of 27%. Net profit for 2Q2014 increased by 28% to reach AED15.8mn from AED12.3mn in 2Q2013. Customer deposits as of June 30, 2014 increased by 50% to AED2.51bn from AED1.67bn as of December 31, 2013. Total assets under management increased by 44% to AED6.14bn as compared to AED4.27bn as of December 31, 2013. (DFM) Daman Investments to revive IPO plans – According to sources, Dubai-based fund manager Daman Investments is reviving plans for an initial public offering (IPO) nearly two years after it placed the share sale on hold. Daman is interviewing banks for an advisory role to help manage the offer. The company is expected to hire a local bank to arrange the sale and the IPO is expected in 2015. (Bloomberg) Emirates signs deal with BAE Systems – BAE Systems has signed a five-year agreement with Emirates Airline to provide maintenance and technical support for its entire Boeing fleet. Under the terms of the agreement, BAE Systems will deliver on agreed-upon turnaround times, position product in region, and provide technical support to Emirates. The company will provide maintenance support for products supplied at line fit to Boeing. These include flight controls, flight deck systems, and control and monitoring systems, at its service centers in the US, UK and Singapore. (Bloomberg) SKAI Holdings secures sales worth AED927mn – Dubai- based SKAI Holdings has secured AED927mn worth of sales for its new AED1.2bn four-star hotel in the SKAI. Located in Dubai’s Jumeirah Village Circle, the construction work on the hotel will begin in September 2014 with operations due to commence in 2017. SKAI Holdings officially launched the project in June 2014 and is reported to have sold all available hotel rooms and serviced apartments in the 60-storey tower. (Bloomberg) Rabobank to issue LCs for DME trading from Singapore – Dubai Mercantile Exchange (DME) announced that Rabobank has given its approval to issue Letters of Credit (LCs) for trading on DME directly from Singapore. The approval marks the culmination of extensive joint efforts to facilitate trading activities of DME’s and Rabobank’s mutual customers in Asia. Rabobank

- 6. Page 6 of 8 will now be able to issue LCs directly from Singapore to guarantee deliveries of Oman Blend crude oil through the DME, helping to create a more efficient, cost-effective and reliable trading ecosystem around the exchange. (Bloomberg) Dubai’s foreign trade in phones hits AED163bn in 2013 – According to data released by Dubai Customs, Dubai’s foreign trade in phones totaled AED163bn in 2013, representing about 12% of the emirate’s overall foreign trade volume. Trade in telephones amounted to AED42.5bn in 1Q2014, up 126% as compared to AED18.8bn recorded in the same period four years ago. Trade in phones ranked first among other commodities traded in the emirate, according to statistics. (Bloomberg) Dubai Trade records impressive growth in 1H2014 – Dubai Trade announced a 94% increase in the number of its services accessed online in 1H2014 as compared to 1H2013. 1H2014 also saw a 27% growth in new companies joining the Dubai Trade Portal, resulting in 8,985 new registered companies, taking the newly registered numbers from 79,083 in 2013 to 96,889 so far in 2014. This generated a 12% growth in transactions with a total of 9.1mn transactions processed by users on the Dubai Trade Portal. The increased activity also had a positive impact on the secured e-Payment gateway, Rosoom, which handled 549,000 payment transactions valued at AED440mn, reflecting a 39% growth rate. (Bloomberg) UNB signs partnership with Orient Insurance – Union National Bank (UNB) has signed a strategic partnership with Orient Insurance for distributing Orient Insurance products through UNB branches across the UAE. As part of the launch, a range of capital guaranteed products across diverse categories such as children’s education, women care, savings and life insurance will be launched and promoted across all UNB branches in the UAE. (GulfBase.com) Takaful Chairman steps down – Abu Dhabi National Takaful Company’s (Takaful) Chairman, Khadem Al Qubaisi, has resigned from his position. He has been replaced by Vice- Chairman Khamis Buharoon. Nasser M. Al Murr Al Za’abi has filled the vacated board seat. (GulfBase.com) OAMC to sign agreement to manage duty-free at Salalah airport – Oman Airports Management Company (OAMC) has selected ATU Turizm Isletmeciligi as master concessionaire for the management and operation of duty-free, retail and food and beverage concessions at the new Salalah airport. ATU duty-free was selected thorough a competitive bidding process. OAMC will sign a 10-year contract with ATU duty-free airport after successful satisfaction of the pre-award requirements. (GulfBase.com) CI affirms Oman currency ratings; outlook stable – Capital Intelligence (CI) has affirmed Oman’s long-term foreign and local currency sovereign ratings at A and its short-term foreign and local currency ratings at A1, with a stable outlook for the ratings. CI said the sultanate’s track record of reasonably prudent economic management, which – combined with favorable oil prices – has led to a run of budget surpluses, low levels of public debt and comparatively strong external finances. The agency said the ratings are also underpinned by the government’s substantial stock of external assets and the currently sound banking system, adding that Oman’s economic performance remains satisfactory. The economy expanded by about 5% for the second year in a row in 2013, supported by increased hydrocarbon production and an expansionary fiscal policy. (GulfBase.com) Salalah Port Services renews agreement with Maersk Line – Salalah Port Services Company has renewed and signed a multi-year agreement with Maersk Line, which has been an integral customer of the port since the start of the port’s operations in November 1998. (MSM) OIFC appoints new CEO – Oman Investment & Finance Company (OIFC) has appointed Mr. Said Ahmed Safrar as its Chief Executive Officer (CEO). Mr. Safrar will take charge by the third week of August 2014 and has more than twenty years of professional experience in the banking and telecom industry. (MSM) 11 firms competing for 2,600MW power plant in Oman – 11 international power giants have submitted their requests for prequalification to develop Oman's biggest gas-fired power plant, to be built in two locations, with a combined generation capacity of 2,600 megawatt. The companies that have submitted their request for qualification are CHD Power Plant Operational co-led consortium, EDF International, GDF Suez, General Electric-led consortium, Korea Electric Power Corporation, Mapna Group-led consortium, Marubeni Corporation, Mitsubishi- led consortium, Mitsui, Sembcorp Utilities-led consortium and Sojitez Corporation. The state-owned Oman Power and Water Procurement (OPWP) floated a request for qualification by mid- June, giving potential developers to submit their proposals up to August 3, 2014 for developing the mega power plant within the main interconnected system (MIS) region. (Bloomberg) Bank Muscat unveils biometric ID system – Bank Muscat has introduced for the first time in the banking sector in Oman a state-of-the-art biometric system compatible with the national identification card (NID). The new system available across the network of 137 branches is aimed at improving efficiency and speed of transaction processing. The NID enables accurate data capture during banking transactions, especially opening new accounts. The new biometric identification system has been launched in collaboration with the Royal Oman Police to provide the latest solutions in national identity during banking services. (Bloomberg) Batelco steps up efforts to get $212mn from Sivasankaran – Batelco Group’s subsidiary, Batelco Millennium India Company (BMIC), was successful in two applications before the English High Court as part of its ongoing efforts to enforce a judgment for the sum of $212mn against C. Sivasankaran and Siva Ltd. BMIC’s first successful application was to extend indefinitely a worldwide freezing order against the assets of C. Sivasankaran and Siva Ltd. The court also ordered Mr. Sivasankaran to provide a further affidavit to BMIC on an expedited basis addressing apparent deficiencies with the statements of assets he has provided pursuant to the freezing order. BMIC’s second successful application was for an order against Mr. Siva to provide comprehensive documentary disclosure about the nature, value and location of his assets globally and then to attend court to be cross-examined about those assets. (Bahrain Bourse) AUB reports net profit of $262.5mn in 1H2014 – Ahli United Bank (AUB) reported a net profit of $262.5mn for 1H2014 as compared to core net profit of $190.1mn during 1H2013, reflecting an increase of 38.1%. Bank’s 2Q2014 net profit was $125.9mn, a 35.1% increase over 2Q2013 profit of $93.2mn. The basic EPS for 1H2014 amounted to 4.4 US cents as against 3.3 US cents in 1H2013 (adjusted for the exceptional gain in 1H2013). Net interest income for 1H2014 increased by 13.7% to $381.7mn from $335.8mn in 1H2013. AUB’s total assets as of June 30, 2014 stood at $33.92bn as compared to $32.65bn as of December 31, 2013. The loans & advances as of June 30, 2014 stood at $18.62bn, while customer deposits stood at $23.11bn. (Bahrain Bourse)

- 7. Page 7 of 8

- 8. Contacts Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509 saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 8 of 8 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 QE Index S&P Pan Arab S&P GCC 0.3% (0.5%) 0.1% (0.1%) (0.0%) (0.9%) (2.4%) (3.2%) (2.4%) (1.6%) (0.8%) 0.0% 0.8% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,305.85 1.3 1.0 8.3 DJ Industrial 16,443.34 0.1 (0.3) (0.8) Silver/Ounce 20.04 1.3 (1.4) 2.9 S&P 500 1,920.24 0.0 (0.3) 3.9 Crude Oil (Brent)/Barrel (FM Future) 104.59 (0.0) (0.2) (5.6) NASDAQ 100 4,355.05 0.1 0.1 4.3 Natural Gas (Henry Hub)/MMBtu 3.89 1.2 3.9 (10.4) STOXX 600 329.19 (0.9) (0.8) 0.3 LPG Propane (Arab Gulf)/Ton 100.25 0.9 0.0 (20.8) DAX 9,130.04 (0.6) (0.9) (4.4) LPG Butane (Arab Gulf)/Ton 118.50 0.9 0.6 (12.7) FTSE 100 6,636.16 (0.7) (0.6) (1.7) Euro 1.34 0.1 (0.3) (2.6) CAC 40 4,207.14 (0.6) 0.1 (2.1) Yen 102.10 (0.5) (0.5) (3.0) Nikkei 15,159.79 (1.0) (2.3) (6.9) GBP 1.69 (0.2) 0.2 1.8 MSCI EM 1,056.77 (0.6) (0.3) 5.4 CHF 1.10 0.2 (0.2) (1.6) SHANGHAI SE Composite 2,217.47 (0.1) 1.5 4.8 AUD 0.94 0.5 0.5 4.9 HANG SENG 24,584.13 (0.3) 0.2 5.5 USD Index 81.44 0.1 0.2 1.8 BSE SENSEX 25,665.27 (0.9) 0.7 21.2 RUB 36.17 0.4 1.1 10.0 Bovespa 56,487.18 0.5 1.0 9.7 BRL 0.44 0.5 (0.6) 4.0 RTS 1,160.86 (2.6) (4.3) (19.5) 188.3 160.2 144.5