Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (20)

Semelhante a 3 February Daily market report

Semelhante a 3 February Daily market report (20)

Mais de QNB Group

Mais de QNB Group (20)

Último

Último (20)

3 February Daily market report

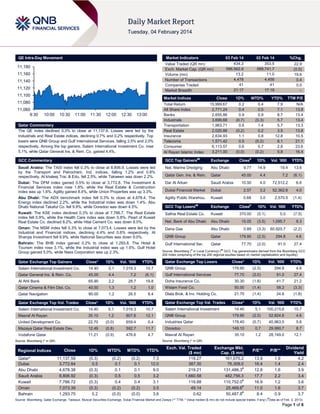

- 1. QE Intra-Day Movement Market Indicators 11,180 11,160 11,140 11,120 11,100 Market Indices 11,080 11,060 9:30 03 Feb 14 434.3 586,562.9 13.2 4,478 41 21:17 Value Traded (QR mn) Exch. Market Cap. (QR mn) Volume (mn) Number of Transactions Companies Traded Market Breadth 10:00 10:30 11:00 11:30 12:00 12:30 13:00 Qatar Commentary The QE index declined 0.3% to close at 11,137.6. Losses were led by the Industrials and Real Estate indices, declining 0.7% and 0.2% respectively. Top losers were QNB Group and Gulf International Services, falling 2.5% and 2.0% respectively. Among the top gainers, Salam International Investment Co. rose 5.1%, while Qatar General Ins. & Rein. Co. gained 4.4%. 02 Feb 14 353.5 589,741.7 11.0 4,458 41 17:19 %Chg. 22.9 (0.5) 19.6 0.4 0.0 – Close Total Return All Share Index Banks Industrials Transportation Real Estate Insurance Telecoms Consumer Al Rayan Islamic Index 1D% WTD% YTD% TTM P/E 15,999.67 2,771.24 2,655.86 3,699.68 1,963.71 2,020.88 2,634.93 1,571.42 6,113.57 3,211.00 0.2 0.4 0.9 (0.7) 0.6 (0.2) 1.1 0.5 0.6 (0.0) 0.4 0.5 0.9 (0.3) 1.4 0.2 0.8 (0.2) 0.7 (0.2) 7.9 7.1 8.7 5.7 5.7 3.5 12.8 8.1 2.8 5.8 N/A 13.8 13.4 13.4 13.3 13.8 10.5 21.1 23.6 16.4 GCC Commentary GCC Top Gainers## Exchange Close# 1D% Saudi Arabia: The TASI index fell 0.3% to close at 8,806.9. Losses were led by the Transport and Petrochem. Ind. indices, falling 1.2% and 0.8% respectively. Al khaleej Trai. & Edu. fell 2.5%, while Takween was down 2.2%. Nat. Marine Dredging Abu Dhabi 9.77 14.9 19.4 13.6 Qatar Gen. Ins. & Rein. Qatar 45.00 4.4 7.2 (6.1) Dubai: The DFM index gained 0.5% to close at 3,772.8. The Investment & Financial Services index rose 1.8%, while the Real Estate & Construction index was up 1.6%. Agility gained 8.4%, while Union Properties was up 3.3%. Dar Al Arkan Saudi Arabia 10.50 4.0 72,512.2 6.6 Dubai Financial Market Dubai 2.57 3.2 52,362.8 4.0 Abu Dhabi: The ADX benchmark index fell 0.3% to close at 4,678.4. The Energy index declined 2.2%, while the Industrial index was down 1.4%. Abu Dhabi National Takaful Co. fell 9.9%, while Ooredoo was down 4.5%. Agility Public Warehou. Kuwait 0.68 3.0 2,570.5 (1.4) GCC Top Losers Exchange Close 1D% Vol. ‘000 Kuwait: The KSE index declined 0.3% to close at 7,786.7. The Real Estate index fell 0.9%, while the Health Care index was down 0.8%. Pearl of Kuwait Real Estate Co. declined 8.2%, while Hilal Cement Co. was down 8.0%. Salhia Real Estate Co. Kuwait 370.00 (5.1) 5.0 (7.5) Nat. Bank of Abu Dhabi Abu Dhabi 15.05 (3.5) 1,095.7 8.3 Oman: The MSM index fell 0.3% to close at 7,073.4. Losses were led by the Industrial and Financial indices, declining 4.4% and 0.6% respectively. Al Sharqia Investment fell 9.9%, while National Securities was down 9.0%. Dana Gas Abu Dhabi 0.89 (3.3) 60,920.7 (2.2) QNB Group Qatar 179.90 (2.5) 294.8 4.6 Gulf International Ser. Qatar 77.70 (2.0) 91.0 27.4 Bahrain: The BHB index gained 0.2% to close at 1,293.8. The Hotel & Tourism index rose 3.1%, while the Industrial index was up 1.6%. Gulf Hotel Group gained 5.0%, while Nass Corporation was up 2.3%. Qatar Exchange Top Gainers Salam International Investment Co. ## # Vol. ‘000 YTD% YTD% Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Close* 1D% Vol. ‘000 YTD% Qatar Exchange Top Losers Close* 1D% Vol. ‘000 14.40 5.1 7,019.3 10.7 QNB Group 179.90 (2.5) 294.8 4.6 77.70 (2.0) 91.0 27.4 YTD% Qatar General Ins. & Rein. Co. 45.00 4.4 7.2 (6.1) Gulf International Services Al Ahli Bank 65.90 2.2 28.7 19.8 Doha Insurance Co. 30.30 (1.8) 41.7 21.2 Qatar Cinema & Film Dist. Co. 40.50 1.3 1.2 1.0 Widam Food Co. 50.00 (1.4) 58.2 (3.3) Qatar Navigation 90.00 1.2 26.5 8.4 Dlala Brok. & Inv. Holding Co. 21.70 (1.4) 24.6 (1.8) Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Close* 1D% Val. ‘000 YTD% Salam International Investment Co. 14.40 5.1 7,019.3 10.7 Salam International Investment 14.40 5.1 100,215.6 10.7 Masraf Al Rayan 35.10 1.2 807.8 12.1 QNB Group 179.90 (2.5) 52,824.6 4.6 United Development Co. 22.70 (0.0) 659.4 0.4 Industries Qatar 178.40 (0.7) 40,963.5 5.6 Mazaya Qatar Real Estate Dev. 12.49 (0.8) 592.7 11.7 Ooredoo 149.10 0.7 29,990.7 8.7 Vodafone Qatar 11.21 (0.9) 476.6 4.7 35.10 1.2 28,149.0 12.1 Qatar* Dubai Abu Dhabi Saudi Arabia Kuwait Oman Bahrain Masraf Al Rayan Source: Bloomberg (* in QR) Source: Bloomberg (* in QR) Regional Indices Qatar Exchange Top Val. Trades Close 1D% WTD% MTD% YTD% 11,137.59 3,772.84 4,678.38 8,806.92 7,786.72 7,073.39 1,293.75 (0.3) 0.5 (0.3) (0.3) (0.3) (0.3) 0.2 (0.2) 0.1 0.1 0.5 0.4 (0.2) (0.0) (0.2) 0.1 0.1 0.5 0.4 (0.2) (0.0) 7.3 12.0 9.0 3.2 3.1 3.5 3.6 Exch. Val. Traded ($ mn) 119.27 387.30 219.21 1,660.58 119.88 49.14 0.62 Exchange Mkt. Cap. ($ mn) 161,070.2 76,309.0 131,486.3# 482,756.3 110,752.0# 25,469.6# 50,487.8# P/E** P/B** 13.9 16.4 12.8 17.7 16.9 11.0 8.4 1.9 1.4 1.6 2.2 1.2 1.6 0.9 Dividend Yield 4.2 2.4 3.9 3.4 3.6 3.7 3.7 # Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) ( Data as of Feb. 2, 2013) Page 1 of 6

- 2. Qatar Market Commentary The QE index declined 0.3% to close at 11,137.6. The Industrials and Real Estate indices led the losses. The index declined on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. Overall Activity Sell %* Net (QR) Qatari 60.41% 62.96% (11,091,224.27) Non-Qatari QNB Group and Gulf International Services were the top losers, falling 2.5% and 2.0% respectively. Among the top gainers, Salam International Investment Co. rose 5.1%, while Qatar General Ins. & Rein. Co. gained 4.4%. Buy %* 39.59% 37.04% 11,091,224.27 Source: Qatar Exchange (* as a % of traded value) Volume of shares traded on Monday rose by 19.6% to 13.2mn from 11.0mn on Sunday. Further, as compared to the 30-day moving average of 10.6mn, volume for the day was 24.7% higher. Salam International Investment Co. and Masraf Al Rayan were the most active stocks, contributing 53.4% and 6.1% to the total volume respectively. Ratings, Earnings and Global Economic Data Ratings Updates Company Ooredoo (ORDS) Agency S&P Market Qatar Type* Old Rating New Rating Rating Change Outlook Outlook Change LT corporate credit rating/ ST corporate credit rating/ Ooredoo's debt/ SACP A/A-1/A/bbb A-/A-1/A/bbb- Stable – Source: News reports (* LT – Long Term, ST – Short Term, SACP - Stand-alone credit profile) Earnings Releases Company Market Union Properties (UPP) * Oman Investment & Finance Co. (OIFC)** Oman International Development & Investment Co. (Ominvest) * SMN Power Holding * Currency Revenue (mn) 4Q2013 % Change YoY Operating Profit (mn) 4Q2013 % Change YoY Net Profit (mn) 4Q2013 % Change YoY Dubai AED 4,491.3 139.5% – – 1,579.7 798.6% Oman OMR – – 2.9 -3.7% 5.1 188.6% Oman OMR 69.6 13.5% – – 14.2 37.4% Oman OMR 74.6 -12.3% 20.9 3.8% 7.8 19.5% Source: Company data, DFM, ADX, MSM (*FY2013 results) (**9 months ended December 31, 2013) Global Economic Data Date Market Source Indicator Period 02/03 US ISM ISM Manufacturing January 02/03 US US Census Bureau Construction Spending MoM December 02/03 EU Markit PMI Manufacturing 02/03 France Markit PMI Manufacturing 02/03 Germany Markit 02/03 UK 02/03 02/03 Actual Consensus Previous 51.3 56.0 56.5 0.10% 0.00% 0.80% January 54.0 53.9 52.7 January 49.3 48.8 47.0 PMI Manufacturing January 56.5 56.3 54.3 Hometrack Hometrack Housing Survey MoM January 0.30% – 0.50% UK Hometrack Hometrack Housing Survey YoY January 4.80% – 4.40% UK Markit PMI Manufacturing January 56.7 57.3 57.2 02/03 Italy Markit PMI Manufacturing January 53.1 53.2 53.3 02/03 China China Fed. of Logistics Non-manufacturing PMI January 53.4 – 54.6 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar QNB Group to open 100% capital-protected note subscription – QNB Group is set to open subscription for QNB Note 2 (Qatar Opportunities), a 100% Capital-Protected Note investment returns linked to the performance of a basket of eight international (European and US) company stocks, which are listed on the equity markets of their respective countries of origin. It’s a closed three year investment, with a minimum capital investment of QR20,000. The eight international companies which form the investment basket have been selected on the basis of their existing close ties to Qatar, either due to their existing local presence or due to substantial business interests in the country. A further aim is to provide satisfactory geographical diversification. The eight international companies selected are Total (France-Energy), Vinci (FranceIndustrials), Siemens (Germany-Industrials), ArcelorMittal (Netherlands-Materials), Iberdrola (Spain-Utilities), Royal Dutch Shell Plc (UK-Energy), ConocoPhillips (US-Energy) and Halliburton Co (US-Energy). Subscription is available via QNB branches to Qatari and non-Qatari investors starting from February 4, 2014 and ending March 5, 2014. (QNB Group Press Release) SIIS reports QR6.7mn net profit, recommends 10% cash dividend – Salam International Company (SIIS) reported a net Page 2 of 6

- 3. profit of QR6.7mn in 4Q2013, falling 92.8% QoQ. Net profit for 2013 amounted to QR113.8mn, reflecting an increase of 35.3% YoY. Operating income increased by 24.4% QoQ to QR622.3mn in 4Q2013, while it was up by 2.5% YoY to QR2,046.5mn in 2013. EPS stood at QR1.00 in 2013 as compared to QR0.74 in 2012. Meanwhile, SIIS’ board of directors has recommended a cash dividend of QR1 per share (10% of the nominal value) to its shareholders. The company’s AGM is scheduled to be held on February 24, 2014. (QE) S&P downgrades Ooredoo to A-, outlook Stable – S&P has lowered its long-term corporate credit rating on Ooredoo to Afrom A, with a Stable outlook. The company’s A-1 short-term corporate credit rating was affirmed at A-1. At the same time, S&P lowered its ratings on Ooredoo's debt to A- from A. Meanwhile, S&P has revised the stand-alone credit profile to bbb- from bbb. The downgrade reflected expectation of higherthan-expected volatility in economic conditions in emerging markets, including negative exchange rate dynamics and Ooredoo’s plans to increase capital expenditure (capex). (GulfTimes.com) MARK’s subsidiary acquires IBB; raises IBB’s Tier 1 capital to £100mn – Masraf Al Rayan (MARK) announced that its subsidiary Al Rayan (UK) Limited has acquired the Islamic Bank of Britain (IBB). MARK has raised IBB’s Tier 1 capital to £100mn by issuing new shares totaling 7,575,400,000 shares, at £75.75mn. As a result, Al Rayan UK’s equity holding in IBB will reach 11,921,189,979 shares, which is equivalent to 98.34% of the issued shares. (QE) DOHI eyeing bigger slice of local and international business – The Doha Insurance Company (DOHI) has its eyes firmly set on acquiring a bigger slice of business in the local and international markets, after its gross premium exceeded QR500mn for the first time. DOHI’s CEO Bassam Hussein said big contracts are in the pipeline and the company is hopeful that things will start rolling in the second half of this year, especially with QRail and other major projects infrastructure projects gearing up. Nonetheless, Hussein said these projects do pose big challenges for the local insurance market. (Gulf-Times.com) Ooredoo signs major global submarine deal – Ooredoo has signed a major deal to land a global submarine cable in Qatar. This new link will provide people in the country access to highspeed global routing that will increase broadband penetration, internet usage and enterprise applications. Recently, senior executives from Ooredoo took part in a ceremony in Hong Kong to mark the launch of the new high-capacity Asia-Africa-Europe1(AAE-1) submarine cable system. (Gulf-Times.com) GISS’ BoD to meet on February 23, AGM on March 11 – Gulf International Services Company’s (GISS) board of directors is scheduled to meet on February 23, 2014 to discuss the company’s financial results ending on December 31, 2013. Meanwhile, the company’s AGM will be held on March 11, 2014. (QE) DBIS postpones its board meeting to Feb. 12 – Dlala Brokerage & Investment Holding Company (DBIS) has postponed its board meeting, scheduled for discussing the disclosure of financial results for FY2013, to February 12, 2014 instead of February 4, 2014. (QE) Al Siddiqi to open restaurants, fashion outlets at PearlQatar – The Pearl-Qatar signed a contract with Al Siddiqi Holding to open eight new restaurant brands and luxury fashion outlets in Porto Arabia and Medina Central districts on the island. The agreement was signed by Ehab Kamel, General Manager–Retail Leasing at The Pearl-Qatar, and Aly Delawar, Board Member at Al Siddiqi Holding. The deal will see the opening of an exclusive Italian restaurant brand “Biella” that will offer Italian dishes, along with the “Lord of The Wings” restaurant in Medina Central district that is specifically designed for families. Other high-end retail outlets run by the group will be located at Porto Arabia. (Gulf-Times.com) International Yellen Sworn in as Fed chairman as Bernanke joins Brookings – Janet Yellen was sworn as the Chairman of the Federal Reserve’s Board of Governors in Washington, while her predecessor, Ben S. Bernanke, joined the Brookings Institution as a distinguished fellow in residence. The announcements completed a leadership transition, with Yellen becoming top policy maker as the Fed tries to wean financial markets off a bond purchase program that has pushed up central bank assets to $4.1tn. She is scheduled to report on monetary policy in semiannual testimony before the House and Senate next week. Her term will last through February 3, 2018. (Bloomberg) Markit: US manufacturing growth slows in January – Markit said the US manufacturing grew less briskly in January after hitting an 11-month high the prior month as output and overseas demand slowed. Market added that its final US Manufacturing Purchasing Managers Index fell to 53.7 in January, matching an advance reading earlier in the month. The index hit an 11-month high of 55.0 in December. Output fell to 53.5, a four-month low, from 57.5. (ET) US banks ease loan standards in Fed survey as demand rises – According to a Federal Reserve report, banks in the US saw increased demand from businesses and consumers for lending and in turn made those loans more readily available. Domestic banks, on balance, reported having eased their lending standards on many types of business and consumer loans and having experienced increases in loan demand, on average, over the past three months. The report shows banks loosening the reins of credit for many categories of lending, including commercial real estate, commercial and industrial loans for firms of all sizes, credit cards, auto loans and other consumer loans. An exception was declining demand for mortgages. (Bloomberg) EU mulls economic lifeline for Ukraine – The EU Foreign Policy Chief Catherine Ashton’s spokeswoman Maja Kocijancic said the EU, US and IMF are mulling economic assistance to Ukraine to help end the country's crisis, but only once Kiev embarks on political reforms. She said that they are looking at how they could support Ukraine when it comes to the economic as well as the political situation. (ET) Eurozone deficit shrinks to almost within European Union limit in third quarter – According to data released by Eurostat, the Eurozone's government deficit shrank for the third consecutive quarter in the three months to last September to near the European Union's official limit of 3% of economic output. The seasonally adjusted government gap fell to 3.1 % of GDP in 3Q2013 from 3.3% in the previous period and down from 3.4% in 1Q2013. The 3.1% shortfall is the smallest since 3Q2008, when it stood at -2.2% of the bloc's economic output, according to Eurostat. The narrowing of the deficit comes from total revenue rising to 47.1% of the GDP from 46.9% in AprilJune, with total expenditure flat at 50.2%. (ET) Italy’s Labor Minister: 4Q2013 GDP growth seen at 0.2 to 0.3% – Italy's Labor Minister Enrico Giovannini said the country’s economy is expected to have posted growth of between 0.2 and 0.3% in 4Q2013. He added that there will finally be a plus sign: the expectation is for 0.2, 0.3% and the Page 3 of 6

- 4. forecasts, which ISTAT has also published recently is for growth to continue in 2014. (ET) Russian manufacturing shrinks for third month running in January – The HSBC purchasing managers' index (PMI) showed Russian manufacturing shrank in January for the third month in a row, and at the fastest rate since June 2009. The index's headline reading fell to 48.0 from December's 48.8, moving further below the 50.0 mark that separates expansion from contraction. (ET) BOJ: Japan to eye 2% inflation in latter half of FY2014 – Bank of Japan’s (BOJ) Governor Haruhiko Kuroda stressed that the country will see 2% inflation around the latter half of fiscal 2014 through early fiscal 2015. He added that Japan is making steady progress toward achieving 2% inflation. The BOJ offered an intense burst of monetary stimulus in April last year, pledging to double base money via aggressive asset purchases to achieve 2% inflation in roughly two years in a country mired. (ET) Regional Al Jouf ADC to raise capital to SR300mn through bonus shares – Al Jouf Agricultural Development Company’s (Al Jouf ADC) board has recommended a capital increase of 20% through bonus shares. The company’s capital is to be raised from SR250mn to SR300mn by issuing one bonus share for every five shares. This increase will be paid by transferring SR50mn from the retained earnings account to the company's capital. Consequently, Al Jouf ADC’s outstanding shares will rise from 25mn shares to 30mn shares. The bonus shares will be allotted to registered shareholders at the close of trading on the day of the extraordinary general assembly (to be announced). (Tadawul) Decree issued for SNOC restructuring – The Supreme Council Member and Ruler of Sharjah, HH Dr. Shaikh Sultan bin Mohammed Al Qasimi has issued Emiri Decree on the restructuring of the Sharjah National Oil Corporation (SNOC). The decree stipulates the merging of Sharjah Liquefaction Gas Company (Shalco), and the Sharjah Oil Company into one corporation called “SNOC”. SNOC shall be a legal entity and enjoy the full capacity to take necessary legal actions for achieving the purposes for which it has been established. (GulfBase.com) ING Group closes ME Asset management operations – ING Group NV said it was closing its Middle East asset management operation, based in Dubai, after the team there resigned. The closure is in line with ING's restructuring drive, which involves only maintaining asset management operations in countries where it has a strong insurance presence, Karl Hanuska, a spokesman for ING Investment Management in the Netherlands, said by telephone."We will stop the main equities activity and turn Dubai into a sales office," Hanuska said. "We had been reviewing the team because we had a small asset base." (Reuters) StanChart appoints CEO for UAE – Standard Chartered (StanChart) has appointed Mohsin Nathani as its Chief Executive Officer for the UAE effective from February 1, 2014. Previously, Nathani was the CEO of the bank's Pakistani business. (Reuters) Dubai expects 4.7% GDP growth in 2014, 5% in 2015 – According to the Dubai Department of Economic Development, the Emirate’s economy is expected to grow at an inflationadjusted 4.7% in 2014, and accelerate to over 5% in 2015. According to earlier official data, the economy had expanded 4.9% in 1H2013 from a year earlier. (Reuters) Damac Towers completes first phase of construction – Damac Properties announced the completion of the first major construction phase at Damac Towers by Paramount located in the Burj Area of Dubai. The concrete raft has been cast at the $1bn project, allowing the main construction to begin on all the four towers. Work is now underway on the four main 70-storey towers, which will eventually rise 250 meters. The project includes around 1,800 units comprising one, two and threebedroom serviced hotel rooms and residences. (GulfBase.com) Dubai creates first energy regulatory framework in Middle East – Dubai has established a new regulatory framework for private energy service companies (Escos) – the first of its kind in the Middle East. The Regulatory & Supervisory Bureau for Electricity and Water Sector will work on reducing energy consumption by 30% in 2030 through enhancing energy efficiency in 30,000 buildings in Dubai. The Dubai Supreme Council of Energy’s (DSCE) Vice Chairman Saeed Mohammed Al Tayer and the Dubai Electricity & Water Authority’s (DEWA) MD and CEO stated that Escos have an important role as they contribute to achieve the basic objective of the Dubai Integrated Energy Strategy 2030. (GulfBase.com) DSI signs AED110mn contract for mall MEP work – Drake & Scull International (DSI) has signed a contract worth around AED110mn to execute the complete Mechanical, Electrical & Plumbing (MEP) works for the redevelopment of the Mall of the Emirates in Dubai. The contract was awarded by Khansaheb Civil Engineering, the main contractor for the project. DSI will procure, install, test and commission all the MEP works at the iconic shopping mall by 2015. (DFM) Pearl Dubai sold $1.9bn prime property assets – UAE-based Pearl Dubai FZ has sold prime property assets worth $1.9bn in its 20mn square foot Dubai Pearl Development Project to Hong Kong-based Chow Tai Fook Endowment Industry Investment Development Group. The purchase includes many high-end residences and serviced apartments and two 5-star hotels. This is the largest bulk asset sale for the development, which is 100% owned by Pearl Dubai FZ – a consortium of investors led by the UAE's Al Fahim Group. (GulfBase.com) Flydubai plans $500mn bond issue – Flydubai’s Chief Financial Officer Mukesh Sodani said that the company seeks to raise funds through a bond issue in 2015 and is considering the sukuk option. Sodani added that company is aiming for a benchmark-sized offer, whose funds would be used for the company's general operating expenses as well as investing for some of its aircraft deliveries. (GulfBase.com) UPP’s BoD recommends 5% bonus share dividend – Union Properties’ (UPP) board of directors has recommended a dividend of 5% bonus shares to its shareholders for 2013. (DFM) Abu Dhabi sees 6.7% real GDP growth – Abu Dhabi’s Department of Economic Development said that the Emirate posted a real GDP growth of 7.4% in 2013, up from 5.6% in 2012. The government body’s Head of Development Indicators, Shorooq al-Zaabi forecasted Abu Dhabi’s GDP to grow 6.7% in 2014. Additionally, she predicted that the Emirate’s oil production would rise steadily through 2017, but oil prices would fall moderately to $95 a barrel by 2017 from $109 last year. (GulfBase.com) Hidd Al Saadiyat villa project to be ready by 2016 – Abu Dhabi-based Saadiyat Development & Investment Company’s (SDIC), Representative Mounir Haidar said that the construction Page 4 of 6

- 5. of villas at the Hidd Al Saadiyat development located at Saadiyat Island is expected to be completed in 2016. Haidar said around 35% of the infrastructure work and 80% of the coastal work have been completed. The development extends on a land area covering over 1.5mn square meters which consists of 450 villas, commercial centers, resorts, retail outlets, apartments, beach clubs and other amenities, along with around seven kilometers of waterfront. (GulfBase.com) KFH reports KD115.9mn net income in 2013 – Kuwait Finance House (KFH) posted a net profit of KD115.9mn in 2013, reflecting an increase of 32% YoY. Meanwhile, the bank’s board had proposed a 13% dividend distribution and 13% bonus shares. (Reuters) NCSI: Oman’s inflation rises 1.1% in 2013 – The National Centre for Statistics & Information (NCSI) reported that the general consumer price index (CPI) in Oman rose by 1.1% at the end of December 2013 as compared to December 31, 2012. The rise in inflation was attributed to the increase in food prices, which saw an overall rise of 2.8% in 2013. During the year, education costs witnessed the largest rise among non-food items, with prices rising by 4.2%. Prices for household furnishings & equipment and routine household maintenance rose by 2.2%, while health costs saw an increase of 1.5%. Prices of clothing & footwear climbed by 1.8% in 2013, and restaurants & hotel prices also witnessed 1.1% rise. Similarly, prices for housing, water, electricity and gas witnessed a marginal rise of 0.5% in 2013. Meanwhile, communication costs decreased by 2.3%, signaling increased competition in the market, while prices for recreation and culture also saw a drop of 1.1% over the same period. (GulfBase.com) BBK reports BHD45.1mn net profit for 2013 – The Bank of Bahrain & Kuwait (BBK) reported net profits of BHD45.1mn for the year ended December 31, 2013, with a growth of 6.4% YoY. EPS stood at 49 fils in 2013 as compared to 46 fils in 2012. The bank’s net interest income rose 4.7% to reach BHD68.9mn as compared to BHD65.8mn in 2012. Net loans & advances grew by 8.0% to reach BHD1,619mn as compared to BHD1,499mn in 2012, while customer deposits grew by 6.7% to BHD2,353mn as compared to BHD2,205mn in 2012. (GulfBase.com) ASBB, BMI bank conclude business combination – Bahrainbased BMI Bank and Al Salam Bank Bahrain (ASBB) have concluded a combination of their business after shareholders of both banks approved it in their respective EGMs. ASBB would be issuing 643,866,927 new ordinary shares at a face value of 100 fils per share to BMI Bank’s shareholders. The business combination is based on the agreed exchange ratio of 11 ASBB shares for every BMI Bank share. (Bahrain Bourse) Arcapita sells Varel to Sandvik for $740mn – Bahrain-based Arcapita signed an agreement to sell Varel International Energy Services to Sweden-based Sandvik. The deal’s total transaction value stands at approximately $740mn. The transaction is subject to standard regulatory approvals and certain environmental due diligence. It is likely that the sale will be finalized within 1H2014. (GulfBase.com) ASBB’s BoD recommends cash dividend of 5% – Al Salam Bank Bahrain’s (ASBB) board of directors has recommended a cash dividend of 5% (5 fils per share), which needs to be approved by its shareholders in the AGM scheduled on March 3, 2014. (Bahrain Bourse) Page 5 of 6

- 6. Rebased Performance Daily Index Performance 170.0 160.0 150.0 140.0 130.0 120.0 110.0 100.0 90.0 80.0 0.0% (0.3%) (0.3%) (0.3%) QE Index Oct-12 May-13 S&P Pan Arab Dec-13 S&P GCC Source: Bloomberg Asset/Currency Performance Gold/Ounce Silver/Ounce Crude Oil (Brent)/Barrel (FM Future) Natural Gas (Henry Hub)/MMBtu North American Spot LPG Propane Price North American Spot LPG Normal Butane Price Euro Source: Bloomberg Close ($) 1D% WTD% YTD% 1,257.68 1.1 1.1 4.3 19.34 0.9 0.9 (0.6) 106.04 (0.3) (0.3) 5.02 0.2 154.00 155.00 Global Indices Performance Close 1D% WTD% YTD% 15,372.80 (2.1) (2.1) (7.3) S&P 500 1,741.89 (2.3) (2.3) (5.8) (4.3) NASDAQ 100 3,996.96 (2.6) (2.6) (4.3) 0.2 15.5 STOXX 600 318.21 (1.3) (1.3) (3.1) (1.9) (1.9) 21.7 DAX 9,186.52 (1.3) (1.3) (3.8) 0.6 0.6 14.2 FTSE 100 6,465.66 (0.7) (0.7) (4.2) DJ Industrial 1.35 0.3 0.3 (1.6) CAC 40 100.98 (1.0) (1.0) (4.1) Nikkei GBP 1.63 (0.8) (0.8) (1.5) MSCI EM CHF 1.11 0.6 0.6 (0.9) SHANGHAI SE Composite* AUD 0.88 (0.0) (0.0) (1.8) USD Index 81.01 (0.4) (0.4) RUB 35.45 0.8 0.8 BRL 0.41 (0.8) (0.8) (2.9) Yen Dubai Mar-12 Bahrain Aug-11 Kuwait Jan-11 Qatar (0.3%) (0.3%) (0.3%) (0.6%) Abu Dhabi 127.5 0.2% 0.3% Oman 140.3 Saudi Arabia Jun-10 0.5% 0.6% 160.0 4,107.75 (1.4) (1.4) (4.4) 14,619.13 (2.0) (2.0) (10.3) 926.74 (1.0) (1.0) (7.6) 2,033.08 0.0 0.0 (3.9) HANG SENG* 22,035.42 0.0 0.0 (5.5) 1.2 BSE SENSEX 20,209.26 (1.5) (1.5) (4.5) 7.8 Bovespa 46,147.52 (3.1) (3.1) (10.4) 1,293.20 (0.6) (0.6) (10.4) Source: Bloomberg RTS Source: Bloomberg (*Market closed on February 03, 2014) Contacts Saugata Sarkar Ahmed M. Shehada Keith Whitney Sahbi Kasraoui Head of Research Head of Trading Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 6 of 6