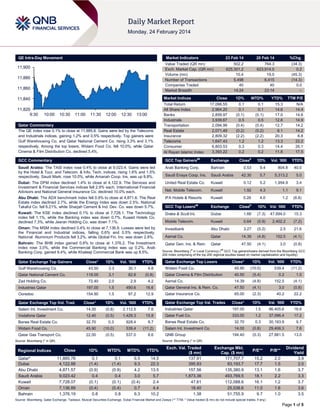

1. QE Intra-Day Movement

Market Indicators

11,900

11,880

11,860

20 Feb 14

%Chg.

502.2

625,301.2

10.4

5,498

40

14:24

764.3

623,914.0

19.0

6,415

40

23:14

(34.3)

0.2

(45.3)

(14.3)

0.0

–

Market Indices

11,840

11,820

9:30

23 Feb 14

Value Traded (QR mn)

Exch. Market Cap. (QR mn)

Volume (mn)

Number of Transactions

Companies Traded

Market Breadth

10:00

10:30

11:00

11:30

12:00

12:30

13:00

Qatar Commentary

The QE index rose 0.1% to close at 11,885.8. Gains were led by the Telecoms

and Industrials indices, gaining 1.2% and 0.5% respectively. Top gainers were

Gulf Warehousing Co. and Qatar National Cement Co. rising 3.3% and 3.1%

respectively. Among the top losers, Widam Food Co. fell 10.0%, while Qatar

Cinema & Film Distribution Co. declined 5.4%.

Close

Total Return

All Share Index

Banks

Industrials

Transportation

Real Estate

Insurance

Telecoms

Consumer

Al Rayan Islamic Index

1D%

WTD%

YTD%

TTM P/E

17,098.55

2,964.20

2,859.97

3,939.67

2,094.99

2,071.49

2,809.32

1,647.43

6,803.53

3,393.22

0.1

0.1

(0.1)

0.5

(0.4)

(0.2)

(2.2)

1.2

0.3

0.2

0.1

0.1

(0.1)

0.5

(0.4)

(0.2)

(2.2)

1.2

0.3

0.2

15.3

14.6

17.0

12.6

12.7

6.1

20.3

13.3

14.4

11.8

N/A

14.4

14.6

14.9

14.2

14.2

6.8

22.2

26.1

17.5

GCC Commentary

GCC Top Gainers##

Exchange

Saudi Arabia: The TASI index rose 0.4% to close at 9,023.4. Gains were led

by the Hotel & Tour. and Telecom. & Info. Tech. indices, rising 1.6% and 1.5%

respectively. Saudi Mark. rose 10.0%, while Amanah Coop. Ins. was up 9.8%.

Arab Banking Corp.

Bahrain

Saudi Enaya Coop. Ins.

Saudi Arabia

Dubai: The DFM index declined 1.4% to close at 4,122.9. The Services and

Investment & Financial Services indices fell 2.9% each. International Financial

Advisors and National General Insurance Co. declined 10.0% each.

United Real Estate Co.

Nat. Mobile Telecom.

Abu Dhabi: The ADX benchmark index fell 0.9% to close at 4,871.6. The Real

Estate index declined 2.7%, while the Energy index was down 2.5%. National

Takaful Co. fell 6.21%, while Sharjah Cement & Ind. Dev. Co. was down 5.7%.

IFA Hotels & Resorts

GCC Top Losers

Exchange

Kuwait: The KSE index declined 0.1% to close at 7,728.1. The Technology

index fell 1.1%, while the Banking index was down 0.7%. Kuwait Hotels Co.

declined 7.3%, while Jeeran Holding Co. was down 7.1%.

Drake & Scull Int.

Dubai

1.66

(7.3)

47,694.0

15.3

Mobile Telecom.

Kuwait

0.64

(5.9)

2,402.2

(7.2)

Oman: The MSM index declined 0.4% to close at 7,136.9. Losses were led by

the Financial and Industrial indices, falling 0.6% and 0.5% respectively.

National Aluminium Products fell 3.2%, while Global Fin. Inv. was down 2.8%.

Investbank

Abu Dhabi

3.27

(5.2)

2.5

21.6

Aamal Co.

Qatar

14.39

(4.8)

152.5

(4.1)

Qatar Gen. Ins. & Rein.

Qatar

47.50

(4.1)

3.0

(0.8)

Bahrain: The BHB index gained 0.8% to close at 1,376.2. The Investment

index rose 3.0%, while the Commercial Banking index was up 0.2%. Arab

Banking Corp. gained 9.4%, while Khaleeji Commercial Bank was up 8.5%.

Gulf Warehousing Co.

Qatar National Cement Co.

Close*

1D%

Vol. ‘000

YTD%

43.50

Qatar Exchange Top Gainers

3.3

30.1

4.8

82.6

(0.8)

##

Close#

1D%

0.53

9.4

804.8

40.0

42.30

5.7

5,313.2

5.0

Kuwait

0.12

5.2

1,954.9

3.4

Kuwait

1.92

4.3

1.1

9.1

Kuwait

0.26

4.0

1.2

(8.8)

#

Close

Vol. ‘000

1D% Vol. ‘000

YTD%

YTD%

Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC

200 Index comprising of the top 200 regional equities based on market capitalization and liquidity)

Close*

1D%

Vol. ‘000

YTD%

Widam Food Co.

45.90

(10.0)

539.4

(11.2)

Qatar Cinema & Film Distribution

40.50

(5.4)

0.2

1.0

Qatar Exchange Top Losers

118.00

3.1

Zad Holding Co.

72.40

2.0

2.9

4.2

Aamal Co.

14.39

(4.8)

152.5

(4.1)

Industries Qatar

197.00

1.5

490.6

16.6

Qatar General Ins. & Rein. Co.

47.50

(4.1)

3.0

(0.8)

Ooredoo

154.90

1.5

97.2

12.9

Qatar Insurance Co.

65.00

(2.3)

40.2

22.2

Close*

1D%

Vol. ‘000

YTD%

Qatar Exchange Top Val. Trades

Close*

1D%

Val. ‘000

YTD%

Salam Int. Investment Co.

14.00

(0.8)

2,112.5

7.6

Industries Qatar

197.00

1.5

96,405.6

16.6

Vodafone Qatar

12.40

(0.5)

1,429.3

15.8

Qatar Fuel Co.

333.00

1.2

37,096.4

17.2

Barwa Real Estate Co.

32.70

0.3

928.4

9.7

Barwa Real Estate Co.

32.70

0.3

30,193.9

9.7

Widam Food Co.

45.90

(10.0)

539.4

(11.2)

Salam Int. Investment Co.

14.00

(0.8)

29,406.3

7.6

Qatar Gas Transport Co.

22.00

(0.5)

537.0

8.6

194.40

(0.3)

27,881.5

13.0

Qatar Exchange Top Vol. Trad.

Source: Bloomberg (* in QR)

Source: Bloomberg (* in QR)

Regional Indices

Qatar*

Dubai

Abu Dhabi

Saudi Arabia

Kuwait

Oman

Bahrain

QNB Group

Close

1D%

WTD%

MTD%

YTD%

11,885.78

4,122.88

4,871.57

9,023.42

7,728.07

7,136.89

1,376.19

0.1

(1.4)

(0.9)

0.4

(0.1)

(0.4)

0.8

0.1

(1.4)

(0.9)

0.4

(0.1)

(0.4)

0.8

6.5

9.3

4.2

3.0

(0.4)

0.7

6.3

14.5

22.3

13.5

5.7

2.4

4.4

10.2

Exch. Val. Traded

($ mn)

137.91

395.93

157.56

1,873.36

47.61

18.40

1.38

Exchange Mkt.

Cap. ($ mn)

171,707.7

83,193.7

135,380.9

493,769.5

112,088.6

25,538.6

51,755.9

P/E**

P/B**

15.2

17.7

13.1

18.1

16.1

11.0

9.7

2.0

1.5

1.6

2.2

1.2

1.6

1.0

Dividend

Yield

3.9

2.0

3.7

3.3

3.7

3.6

3.5

Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any)

Page 1 of 5

2. Qatar Market Commentary

The QE index rose 0.1% to close at 11,885.8. The Telecoms and

Industrials indices led the gains. The index rose on the back of

buying support from non-Qatari shareholders despite selling

pressure from Qatari shareholders.

Gulf Warehousing Co. and Qatar National Cement Co. were the

top gainers, rising 3.3% and 3.1% respectively. Among the top

losers, Widam Food Co. fell 10.0%, while Qatar Cinema & Film

Distribution Co. declined 5.4%.

Overall Activity

Buy %*

Sell %*

Net (QR)

Qatari

61.32%

76.01%

(73,806,460.48)

Non-Qatari

38.68%

23.99%

73,806,460.48

Source: Qatar Exchange (* as a % of traded value)

Volume of shares traded on Sunday fell by 45.3% to 10.4mn

from 19.0mn on Thursday. Further, as compared to the 30-day

moving average of 12.7mn, volume for the day was 18.1% lower.

Salam International Investment Co. and Vodafone Qatar were

the most active stocks, contributing 20.3% and 13.8% to the total

volume respectively.

Earnings

Earnings Releases

Company

Gulf Pharmaceutical

Industries (Julphar)*

Fujairah Cement Industries

Co (FCI)*

Revenue

(mn) 4Q2013

% Change

YoY

Operating Profit

(mn) 4Q2013

% Change

YoY

Net Profit (mn)

4Q2013

% Change

YoY

AED

1,362.07

15.4%

–

–

230.36

14.9%

AED

588.22

3.3%

–

–

-12.19

NA

Market

Currency

Abu Dhabi

Abu Dhabi

Source: Company data, DFM, ADX, MSM (*FY2013 results)

News

Qatar

GISS reports QR217.8mn net profit in 4Q2013 – Gulf

International Services (GISS) reported a net profit of

QR217.8mn in 4Q2013, an increase of 31.1% QoQ. Net profit

for 2013 amounted to QR677mn, rising 45.8% YoY. Revenue

rose by 5.6% QoQ to QR607.3mn, while it rose by 46.2% YoY to

QR2,301.7mn in 2013. EPS amounted to QR4.55 in 2013 as

compared to QR3.12 in 2012. GISS board of directors has

proposed an annual dividend distribution of QR2 per share and

25% bonus shares. Delving into details, GISS posted annual

revenue of QR2.3bn up 47.1% YoY and 18.1% above their own

guidance (2013 budget). Revenue in the drilling segment was

QR912.2mn, up 46.3% YoY. This performance was driven

largely by the offshore sector, which contributed QR181.0 million

of additional revenue compared to last year, and can be further

attributed to the deployment of Al-Jassra and Leshat (previously

referred to as „B-341‟) offshore rigs in the second and fourth

quarters of 2013 respectively, and the roll-over of three other

rigs, Al-Doha, Al-Zubarah and Al-Rayyan, on new, higher rate

contracts. Additional contributions to the overall revenue

improvement came from the two land rigs, GDI-5 and GDI-6,

which completed their first full year of operation, and the lift boat,

Dixie Patriot, that commenced operations in the early part of

2013. QoQ, the results were higher by QR52.8mn, primarily due

to the deployment of the Leshat rig. Aviation segment revenue

touched QR618.5mn, up 20.4% YoY. A number of factors

contributed to this increase on last year: revised contract rates,

an increase in the number of helicopters in the fleet (2013, Q4:

45 helicopters versus 2012, Q4: 42 helicopters) in operations in

a number of new territories. The group‟s insurance subsidiary

registered gross insurance revenue of QR707.0mn, a growth of

13.2% YoY. The main contributor to this growth was the medical

line of business, as an additional 15,000 members joined Al

Koot Global Care Medical Insurance Scheme during the year.

The medical line of business has now grown on average by an

annual average of ~20% per year since 2009, and now

contributes ~33.9% of Al Koot‟s annual revenue. Results in the

core Energy line showed a growth of 5.1%, in line with Qatar

Petroleum‟s reduced capital expenditure activity. Revenue was

up on the last quarter by QR8.5mn, or 4.7%, mainly due to an

increase in net commission income in the Energy insurance

business. The Catering segment (Amwaj) was the largest

contributor to group revenue, accounting for QR976.9mn, or

42.4%; it was up 123.8% YoY following its acquisition on June 1,

2012; the growth was also due to the expansion of the core

industrial catering and manpower contracting services to almost

100 projects throughout Qatar. On a quarterly basis, Amwaj‟s

performance was strong with revenue increasing by 10.0%. (QE,

GISS Press Release)

KCBK gets nod to hike foreign ownership to 49% – Al Khalij

Commercial Bank (KCBK) has received approval from its

shareholders to increase the foreign ownership limit to 49% from

the current 25%. The bank is not only planning to raise funds

through specific private placements, but also seeking bigger

contribution from its Paris-based subsidiary, Al Khaliji France.

KCBK‟s Chairman & Managing Director Sheikh Hamad bin

Faisal Thani al-Thani said that higher foreign ownership limit

allows the bank to open up to international investors and

increase the liquidity of its shares. He said the bank had

reviewed its foreign ownership limit to qualify for the inclusion in

the MSCI Index, once Qatar gets upgraded to the emerging

market status. KCBK shareholders also approved its board's

proposal to distribute 10% cash dividend of the shares nominal

value (QR1.00 per share) for the year ended 31 December 2013

(Gulf-Times.com, QE)

QTA: $45bn to be spent on tourism by 2030 – The Qatar

Tourism Authority‟s (QTA) Chairman Issa bin Mohamed alMohannadi disclosed that up to $45bn will be spent to boost

tourism in Qatar by 2030 in anticipation of around 7mn

international travelers visiting the country every year. Tourism

currently accounts for 1% of Qatar‟s GDP, which is one of the

highest in the world, while its contribution to global GDP has

reached 9.3%. Tourism is expected to grow four fold, boosting

Qatar‟s GDP by up to 3% by 2030. For the first time in 2012, the

Page 2 of 5

3. number of tourists that travel across international borders

reached 1bn with Qatar receiving up to 1.2mn. Al-Mohannadi

asserted that focusing on tourism would enable Qatar to

improve its infrastructure and visitor facilities and services. He

described the target of welcoming more than 7mn tourists a year

as “the cornerstone” of the QTA‟s National Tourism Strategy,

pointing out that the figure was a seven-fold increase from the

current number. (Gulf-Times.com)

Qatar trade surplus shrinks 7% YoY QR33.92bn in

December – A double-digit growth in imports and lower exports

led Qatar report 7% YoY shrinkage in trade surplus to

QR33.92bn in December 2013. According to the preliminary

estimates of the Ministry of Development Planning and Statistics

(MD&PS), the energy-rich Gulf country‟s total exports (valued

free-on-board) fell 3% to QR43.32bn, mainly on a double-digit

fall in shipments to South Korea and India. Japan continued to

be the top destination of Qatar‟s exports, followed by South

Korea, China, India and Singapore. However, Qatar‟s re-exports

surged 52% to QR0.6bn during the review period. The country‟s

total exports of domestic products shrank 3% to QR42.72bn in

December, mainly on lower shipments of gas and non-crude

products as well as other commodities; even as crude were on

the rise. Qatar‟s exports of petroleum gases and other gaseous

hydrocarbons (liquefied natural gas, condensates, propane and

butane) fell 2% to QR27.65bn, non-crude petroleum oils and oil

obtained from bituminous minerals by 6% to QR2.44bn and

other commodities by 17% to QR4.93bn. However, crude

petroleum exports expanded 7% to QR7.69bn. (GulfTimes.com)

Barwa project first phase to house 24,000 workers – Barwa

Real Estate‟s Project Manager Engineer Abdulla Hiji said that

the company‟s mega project Barwa Al Baraha will be ready to

accommodate 24,000 workers in 32 residential buildings by

3Q2014. Hiji said that Barwa Al Baraha extends over 1.8mn

square meters, with a total planned capacity of accommodating

53,000 workers. He added that the company has signed a MoU

with Qatar Navigation, while other companies such as Qatar

Airways, Qatari Diar and QDVC have shown interest. (GulfTimes.com)

International

G20 aims to lift GDP by another 2% in five years – The

world‟s largest economies have set a target of adding more than

$2tn to the global economy over the next five years, signaling

optimism following years of crisis-era austerity. Finance

ministers and central bankers at the G20 meeting in Sydney

said they would take concrete action to increase investment,

boost employment and promote competition. The G20 group of

countries accounts for around 85% of the global economy.

Australian Treasurer Joe Hockey hailed the announcement as a

new dawn for cooperation in the G20. He also said the G20 is

putting a real number to achieve for the first time, aiming to add

over $2tn more in economic activity and tens of millions of new

jobs. (The Telegraph, Peninsula Qatar)

BoE not to take risks with UK recovery – The Bank of

England‟s (BoE) Governor Mark Carney said a new phase of

forward guidance has been introduced to give assurance that

officials will support the economic rebound. Carney said that

BoE will not take risks with the UK‟s economic recovery. He

added that BoE is going to set the path of monetary policy in a

way that ensures that a sustainable growth is seen in jobs,

income and spending. Carney said the revised framework for

forward guidance introduced earlier this month reflects the need

for a more complex set of judgments than was needed in the

first phase, where there was a single link to the unemployment

rate. The bank changed its approach after the jobless rate fell

faster than forecast toward a 7% threshold for considering an

interest-rate increase. (Bloomberg)

ECB prepared for stimulus if deflation risks rise – The

European Central Bank‟s (ECB) President Mario Draghi said

that policy makers are ready to add more stimulus if the outlook

for prices deteriorates, though there are currently no signs of

deflation in the Eurozone. Draghi said that ECB does not find

any evidence of people postponing their expenditure plans with

a view to buying the same thing at lower prices. He added that

ECB is aware of the deflation risk and its Governing Council is

willing to take any action in case these risks were to gain

strength. (Bloomberg)

US urges Ukraine to begin IMF discussions soon – The US

Treasury Secretary Jack Lew has appealed Ukraine to begin

discussions with the International Monetary Fund (IMF) for an

assistance package as soon as possible once a transitional

government is in place in Kiev. Lew said, the US along with

Europe and others in the international community is ready to

supplement an IMF program to cushion the impact of harsh

reforms on low-income Ukrainians. (Reuters)

Regional

SEC: No plans to rely on solar energy for power – The Saudi

Electricity Company (SEC) stated that the cost of solar energy is

currently too high to replace traditional methods of energy

production. SEC‟s Chief Executive, Zeyad Al-Sheha said that

electricity production from fossil fuel currently costs seven halala

per kilowatt-hour (kwh), compared to 50 halala per kwh from

solar energy. SEC currently uses 2mn bpd to generate electricity

and would not stop using oil any time soon. (GulfBase.com)

UAE Central Bank’s board to review reports – The Central

Bank of the UAE has reviewed numerous reports during its

recent board meeting and has approved applications from

various banks and financial institutions for the extension of

activities and opening new branches. The board reviewed a

report on the study of money changing business project, along

with a report on the preparation of an IT strategy for the central

bank and the actions taken so far. Further, the board reviewed a

report on systemic prudential ratios for the banking system,

banking stability, and liquidity indicators of the banking sector,

submitted by the Monetary Policy & Financial Stability

Department. (GulfBase.com)

Deloitte ranks LuLu as fastest growing retailer – Deloitte

ranked UAE-based LuLu Group 11th in a list of the biggest

growing retail businesses over a five-year period. The list

included the world‟s 250 biggest names in the sector. Emerging

market retailers accounted for more than half (26) of the world‟s

top 50 fastest growing retailers. Deloitte said that LuLu has

averaged a CAGR of around 25% between 2007-2012. LuLu,

with revenues exceeding $4.5bn in 2012, has been ranked

197th in the Global 250 list. The company plans to open 42 new

Lulu Hypermarkets in the next two years, with 7 outlets in the

UAE, 6 in Oman, 4 each in Qatar, Kuwait, 3 each in Bahrain,

Egypt and 15 in Saudi Arabia. (GulfBase.com)

Dubai’s food trade jumps to AED46bn in 9M2013 – According

to the data compiled by Dubai Exports, Dubai‟s local food trade

strikes a healthy balance between imports, exports and reexports, in addition to targeting new export markets. Dubai‟s

total foreign trade in food products during 9M2013 rose to

AED46bn from AED43bn in 9M2012, with imports increasing to

AED31-32bn. Further, exports and re-exports rose from AED1214bn between the corresponding periods. In this, the value of

Page 3 of 5

4. exports aided by Dubai Exports saw a 114% rise from

AED605mn to AED1.3bn. (GulfBase.com)

the distribution of a cash dividend of 20 baisas per share for the

year ended December 31, 2013. (MSM)

DED: Stability boosts business outlook in Dubai – According

to a quarterly survey by the Department of Economic

Development (DED), around 97% businesses expect their sales

to rise or remain steady in 1Q2014, as compared to 96% in

4Q2013 and 94% in 4Q2012. A total of 502 companies in Dubai

were covered in the survey that was conducted between

October to December 2013. The Composite Business

Confidence Index for 4Q2013 rose to 144.3 points, up 8.4 points

from 4Q2012 and the 141.6 points recorded in 3Q2013. The

overall business outlook for 1Q2014 also improved with 63%

businesses foreseeing better business conditions as against

58% for 4Q2013. (GulfBase.com)

ABG’s net profit rises 9% to $144.5mn – Al Baraka Banking

Group‟s (ABG) net profit increased by 9% to $144.5mn in 2013

as compared to $133mn in 2012. Total operating income grew

to $909.5mn in 2013 as compared to $879.8mn in 2012. Total

assets at the end of 2013 stood at $21bn, up 10% from $19bn a

year earlier. The bank‟s EPS stood at $13.90 as of December

31, 2013 as against $12.79 a year earlier. (Bahrain Bourse)

Nakheel initiates repayment of AED2.35bn bank debt –

Dubai-based developer Nakheel has initiated early repayment of

bank debts worth AED2.35bn ($639.8mn), nearly 18 months

ahead of their maturity in September 2015. Till now, the

company has accumulated bank debts worth AED6.8bn, while

building ambitious mega projects such as the Palm Island off

Dubai's coast. (Reuters)

UNB reports AED1,743mn net profit in 2013 – The Union

National Bank (UNB) has reported a net profit of AED1,743mn in

2013 as compared to AED1,600mn in 2012. The bank‟s net

interest income grew to AED2,270mn in 2013 as against

AED2,188mn in 2012. EPS amounted to AED0.62 at the end of

2013 as compared to AED0.56 a year earlier. Total assets stood

at AED87.5bn for the year ended December 31, 2013 as

compared to AED87.1bn a year earlier. Net loans & advances

grew to AED60bn in 2013 as against AED57bn in 2012, while

customer deposits stood at AED65bn as compared to AED63bn.

(ADX)

SCIDC’s BoD recommends 5% cash dividend – Sharjah

Cement & Industrial Development Company‟s (SCIDC) board of

directors has recommended the distribution of 5% cash dividend

to its shareholders for the year ended December 31, 2013.

(ADX)

Julphar’s BoD recommends 10% dividends, bonus shares –

Gulf Pharmaceutical Industries‟ (Julphar) board of directors has

recommended the distribution of 10% cash dividends and 10%

bonus shares to its shareholders. (ADX)

Burgan Bank’s Q4 net profit slumps – Kuwait-based Burgan

Bank reported a big drop in its 4Q2013 net profit, with its fullyear earnings also significantly lower than the previous period.

The bank, 58% owned by conglomerate Kuwait Projects

Company, made a net profit of KD2.52mn 4Q2013. This

compares poorly with KD9.22mn in the corresponding period of

2012. Burgan Bank reported a net profit of KD20.1mn in 2013,

63.8% lower YoY. This was due to the bank reporting a

KD10.3mn loss in the 3Q2013. Meanwhile, the bank said it is

recommending a cash dividend of 7 fils per share and a 7%

bonus share issue for 2013. (Reuters)

CBO declares results of OMR287mn certificates of deposit –

The results of certificates of deposit tender held at the Central

Bank of Oman (CBO), with the allotted amount of OMR287mn

for the Issue No 855, have been declared. CBO stated that the

average interest rate of these certificates was 0.13%, while the

maximum accepted interest rate was also 0.13%. The tenor of

these certificates is 28 days with maturity date on March 19. The

Repo rate during February 19-25 stood at 1%. (GulfBase.com)

ATMI’s BoD proposes cash dividend – Al Jazeera Steel

Products Company‟s (ATMI) board of directors has proposed

Page 4 of 5

5. Rebased Performance

Daily Index Performance

180.0

170.0

160.0

150.0

140.0

130.0

120.0

110.0

100.0

90.0

80.0

0.5%

144.1

0.1%

0.0%

131.2

0.4%

(0.5%)

(0.1%)

(0.4%)

(1.0%)

(0.9%)

(1.5%)

S&P Pan Arab

Dec-13

S&P GCC

Source: Bloomberg

Asset/Currency Performance

Gold/Ounce

Silver/Ounce

Crude Oil (Brent)/Barrel (FM

Future)

Natural Gas (Henry

Hub)/MMBtu

North American Spot LPG

Propane Price

North American Spot LPG

Normal Butane Price

Euro

Source: Bloomberg

Close ($)

1D%

WTD%

YTD%

1,324.28

0.0

0.0

9.8

21.85

0.0

0.0

12.2

109.85

0.0

0.0

6.21

0.0

135.38

Global Indices Performance

Close

1D%

WTD%

YTD%

16,103.30

0.0

0.0

(2.9)

S&P 500

1,836.25

0.0

0.0

(0.7)

(0.9)

NASDAQ 100

4,263.41

0.0

0.0

2.1

0.0

43.1

STOXX 600

336.09

0.0

0.0

2.4

0.0

0.0

7.2

DAX

9,656.95

0.0

0.0

1.1

134.63

0.0

0.0

(1.4)

FTSE 100

6,838.06

0.0

0.0

1.3

DJ Industrial

1.37

0.0

0.0

0.0

102.51

0.0

0.0

(2.7)

GBP

1.66

0.0

0.0

0.4

MSCI EM

CHF

1.13

0.0

0.0

0.6

SHANGHAI SE Composite

AUD

0.90

0.0

0.0

0.7

USD Index

80.24

0.0

0.0

RUB

35.53

0.0

0.0

BRL

0.43

0.0

0.0

0.7

Yen

Dubai

May-13

Oman

Oct-12

Abu Dhabi

QE Index

Mar-12

Bahrain

Aug-11

Kuwait

Jan-11

(1.4%)

Qatar

(2.0%)

Saudi Arabia

Jun-10

0.8%

1.0%

170.8

CAC 40

Nikkei

4,381.06

0.0

0.0

2.0

14,865.67

0.0

0.0

(8.8)

959.26

0.0

0.0

(4.3)

2,113.69

0.0

0.0

(0.1)

HANG SENG

22,568.24

0.0

0.0

(3.2)

0.3

BSE SENSEX

20,700.75

0.0

0.0

(2.2)

8.1

Bovespa

47,380.24

0.0

0.0

(8.0)

1,315.54

0.0

0.0

(8.8)

Source: Bloomberg

RTS

Source: Bloomberg

Contacts

Saugata Sarkar

Ahmed M. Shehada

Keith Whitney

Sahbi Kasraoui

Head of Research

Head of Trading

Head of Sales

Manager - HNWI

Tel: (+974) 4476 6534

Tel: (+974) 4476 6535

Tel: (+974) 4476 6533

Tel: (+974) 4476 6544

saugata.sarkar@qnbfs.com.qa

ahmed.shehada@qnbfs.com.qa

keith.whitney@qnbfs.com.qa

sahbi.alkasraoui@qnbfs.com.qa

QNB Financial Services SPC

Contact Center: (+974) 4476 6666

PO Box 24025

Doha, Qatar

DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar

Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an

offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential

investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be

reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts,

QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the

right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the

views and opinions included in this report.

COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS.

Page 5 of 5