16 January Daily market report

•

0 gostou•602 visualizações

The QE index rose 0.3% led by gains in the banking and insurance sectors, with Al Ahli Bank and Mazaya Qatar Real Estate Dev. as top gainers. Regional markets were mostly higher with Abu Dhabi and Dubai rising over 1% and 0.8% respectively. Volume on the Qatar Exchange increased 46.6% compared to the previous day.

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a 16 January Daily market report

Semelhante a 16 January Daily market report (20)

Mais de QNB Group

Mais de QNB Group (20)

Último

Último (20)

16 January Daily market report

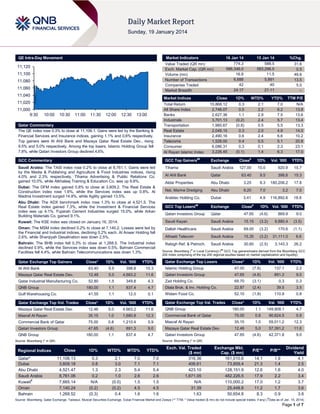

- 1. QE Intra-Day Movement Market Indicators 11,120 11,100 11,080 11,060 11,040 Market Indices 11,020 11,000 9:30 16 Jan 14 774.3 586,346.0 16.8 6,688 42 24:17 Value Traded (QR mn) Exch. Market Cap. (QR mn) Volume (mn) Number of Transactions Companies Traded Market Breadth 10:00 10:30 11:00 11:30 12:00 12:30 13:00 Qatar Commentary The QE index rose 0.3% to close at 11,106.1. Gains were led by the Banking & Financial Services and Insurance indices, gaining 1.1% and 0.6% respectively. Top gainers were Al Ahli Bank and Mazaya Qatar Real Estate Dev., rising 9.5% and 5.0% respectively. Among the top losers, Islamic Holding Group fell 7.8%, while Qatari Investors Group declined 4.6%. 15 Jan 14 588.5 583,296.5 11.5 5,891 40 21:11 %Chg. 31.6 0.5 46.6 13.5 5.0 – Close Total Return All Share Index Banks Industrials Transportation Real Estate Insurance Telecoms Consumer Al Rayan Islamic Index 1D% WTD% YTD% TTM P/E 15,868.12 2,748.07 2,627.36 3,701.13 1,960.67 2,049.15 2,490.16 1,528.00 6,086.31 3,226.45 0.3 0.5 1.1 (0.2) (0.8) 0.3 0.6 0.4 0.3 (0.1) 2.1 2.2 2.9 2.4 0.5 2.0 2.4 0.5 0.1 1.4 7.0 6.2 7.5 5.7 5.5 4.9 6.6 5.1 2.3 6.3 N/A 13.8 13.6 13.4 13.3 14.0 10.2 20.8 23.1 17.0 GCC Commentary GCC Top Gainers## Exchange Close# 1D% Saudi Arabia: The TASI index rose 0.2% to close at 8,761.1. Gains were led by the Media & Publishing and Agriculture & Food Industries indices, rising 4.0% and 2.3% respectively. Tihama Advertising & Public Relations Co. gained 10.0%, while Alkhaleej Training & Education Co. was up 9.8%. Tihama Saudi Arabia 127.00 10.0 920.9 15.7 Al Ahli Bank Qatar 63.40 9.5 398.8 15.3 Aldar Properties Abu Dhabi 3.25 8.3 180,206.2 17.8 Nat. Marine Dredging Abu Dhabi 9.20 7.0 3.2 7.0 Arabtec Holding Co. Dubai 3.41 4.9 116,892.6 18.8 Dubai: The DFM index gained 0.8% to close at 3,609.2. The Real Estate & Construction index rose 1.6%, while the Services index was up 0.8%. Al Madina Investment surged 14.8%, while Agility gained 13.5%. Abu Dhabi: The ADX benchmark index rose 1.3% to close at 4,521.5. The Real Estate index gained 7.3%, while the Investment & Financial Services index was up 4.1%. Fujairah Cement Industries surged 15.0%, while Arkan Building Materials Co. gained 9.1%. ## # 1D% Vol. ‘000 YTD% GCC Top Losers Exchange Qatari Investors Group Qatar 47.65 (4.6) 869.9 9.0 Kuwait: The KSE index was closed on January 16, 2014. Saudi Kayan Saudi Arabia 15.15 (3.2) 9,880.4 (3.5) Oman: The MSM index declined 0.2% to close at 7,140.2. Losses were led by the Financial and Industrial indices, declining 0.2% each. Al Anwar Holding fell 2.6%, while Sharqiyah Desalination was down 2.5%. Dallah Healthcare Saudi Arabia 69.00 (3.2) 170.6 (1.1) Atheeb Telecom Saudi Arabia 15.35 (3.2) 31,111.0 6.6 Rabigh Ref. & Petroch. Saudi Arabia 30.60 (2.5) 3,143.3 26.2 Bahrain: The BHB index fell 0.3% to close at 1,268.5. The Industrial index declined 0.9%, while the Services index was down 0.5%. Bahrain Commercial Facilities fell 4.4%, while Bahrain Telecommunications was down 1.3%. Close Vol. ‘000 YTD% Source: Bloomberg (# in Local Currency) (## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Al Ahli Bank Mazaya Qatar Real Estate Dev. Close* 1D% Vol. ‘000 YTD% Close* 1D% Vol. ‘000 YTD% 63.40 Qatar Exchange Top Gainers 9.5 398.8 15.3 Islamic Holding Group 47.00 (7.8) 137.1 2.2 Qatari Investors Group 47.65 (4.6) 891.3 9.0 12.48 5.0 4,663.2 11.6 Qatar Exchange Top Losers Gulf Warehousing Co. 1.5 349.8 4.3 Zad Holding Co. 69.70 (3.1) 0.3 0.3 1.1 837.4 4.7 Dlala Brok. & Inv. Holding Co. 22.87 (2.4) 39.5 3.5 41.55 QNB Group 52.80 180.00 Qatar Industrial Manufacturing Co. 1.1 12.0 0.1 Widam Food Co. 52.10 (1.9) 110.9 0.8 Close* 1D% Vol. ‘000 YTD% Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Mazaya Qatar Real Estate Dev. 12.48 5.0 4,663.2 11.6 QNB Group 180.00 1.1 149,908.1 4.7 Masraf Al Rayan 35.15 1.0 1,680.8 12.3 Commercial Bank of Qatar 75.00 0.8 90,624.5 5.9 Commercial Bank of Qatar 75.00 0.8 1,210.4 5.9 Masraf Al Rayan 35.15 1.0 59,011.2 12.3 47.65 (4.6) 891.3 9.0 Mazaya Qatar Real Estate Dev. 12.48 5.0 57,391.2 11.6 180.00 1.1 837.4 4.7 Qatari Investors Group 47.65 (4.6) 42,371.8 9.0 Qatar Exchange Top Vol. Trades Qatari Investors Group QNB Group Source: Bloomberg (* in QR) Source: Bloomberg (* in QR) Regional Indices Qatar* Dubai Abu Dhabi Saudi Arabia Kuwait# Oman Bahrain Close 1D% WTD% MTD% YTD% 11,106.13 3,609.18 4,521.47 8,761.06 7,665.14 7,140.24 1,268.52 0.3 0.8 1.3 0.2 N/A (0.2) (0.3) 2.1 3.0 2.3 1.0 (0.0) (0.2) 0.4 7.0 7.1 5.4 2.6 1.5 4.5 1.6 7.0 7.1 5.4 2.6 1.5 4.5 1.6 Exch. Val. Traded ($ mn) 316.36 406.61 423.10 1,671.05 N/A 31.39 1.63 Exchange Mkt. Cap. ($ mn) 161,010.6 73,859.4 128,151.9 482,226.5 110,000.2 25,448.8 50,654.8 P/E** P/B** 14.1 21.3 12.6 17.9 17.0 11.2 8.3 1.9 1.4 1.6 2.2 1.2 1.7 0.9 Dividend Yield 4.1 2.5 4.0 3.4 3.7 3.6 3.8 # Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) ( Data as of Jan. 15, 2014) Page 1 of 7

- 2. Qatar Market Commentary The QE index rose 0.3% to close at 11,106.1. The Banking & Financial Services and Insurance indices led the gains. The index rose on the back of buying support from non-Qatari shareholders despite selling pressure from Qatari shareholders. Overall Activity Sell %* Net (QR) Qatari 50.83% 77.51% (206,589,046.08) Non-Qatari Al Ahli Bank and Mazaya Qatar Real Estate Dev. were the top gainers, rising 9.5% and 5.0% respectively. Among the top losers, Islamic Holding Group fell 7.8%, while Qatari Investors Group declined 4.6%. Buy %* 49.17% 22.50% 206,589,046.08 Source: Qatar Exchange (* as a % of traded value) Volume of shares traded on Thursday rose by 46.6% to 16.8mn from 11.5mn on Wednesday. Further, as compared to the 30-day moving average of 11.3mn, volume for the day was 48.3% higher. Mazaya Qatar Real Estate Dev. and Masraf Al Rayan were the most active stocks, contributing 27.8% and 10.0% to the total volume respectively. Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market A.M. Best Qatar FSR/ ICR Fitch Kuwait LT IDR/ VR Qatar General Insurance & Reinsurance Co. (QGRI) National Bank of Kuwait (NBK) Type* Old Rating New Rating Rating Change Outlook Outlook Change B++/bbb+ A-/a- Stable AA-/a AA-/a – Stable – Source: News reports (* LT – Long Term, ST – Short Term, FSR- Financial Strength Rating, FCR – Foreign Credit Rating, IDR – Issuer Default Rating, ICR – Issuer Credit Rating) Earnings Releases Revenue (mn) 4Q2013 % Change YoY Operating Profit (mn) 4Q2013 % Change YoY Net Profit (mn) 4Q2013 % Change YoY SR – – 29.3 12.3% 26.4 11.4% Saudi Arabia SR – – 1.3 107.8% 1.3 485.0% Saudi Arabia SR – – 131.0 73.3% 276.1 278.2% Saudi Arabia SR – – 87.6 96.0% 178.2 176.3% Saudi Arabia SR – – -0.8 38.0% -0.7 28.0% Saudi Arabia SR – – -9.1 9.4% -27.7 NA Saudi Arabia SR – – 1.5 25.0% 1.0 61.0% Saudi Arabia SR – – -1.2 NA 12.8 55.3% Saudi Arabia SR 1,398.1 -10.4% – – 13.5 3.5% Saudi Arabia SR – – -742.0 19.3% -661.0 -39.4% Saudi Arabia SR 30.1 -55.7% – – 0.4 -79.2% Saudi Arabia SR – – -6.1 344.2% -6.1 344.2% Saudi Arabia SR – – 46.0 -0.2% 38.8 4.3% Saudi Arabia SR – – 142.7 21.6% 133.3 20.7% Dubai AED – – 549.3 -8.9% 103.9 42.6% Oman OMR – – – – 4.2 207.6% Company Market Aldrees Petroleum & Transport Services Co. (Aldrees) Food Products Co. (wafrah) The National Shipping Co. (Bahri) Sahara Petrochemical Co. (Sahara) Bishah Agriculture Development Co. (Bisha Agri) Jazan Development Co. (JAZADCO) Saudi Industrial Export Co. (SIECO) Saudi Automotive Services Co. (SASCO) The Company for Cooperative Insurance (Tawuniya) Saudi Electricity Co. (SEC) Al Sagr Co-operative Insurance Co. (Al Sagr Ins) Al-Baha Investment & Development Co. (Al-baha) Bawan Company (Bawan) Fawaz Abdulaziz AlHokair Company (Fawaz Al Hokair) Tamweel Currency Saudi Arabia Gulf Investment Services Source: Company data, DFM, ADX, MSM Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 01/16 US Bureau of Labor Stat. CPI MoM December 0.30% 0.30% 0.00% 01/16 US Bureau of Labor Stat. CPI YoY December 1.50% 1.50% 1.20% 01/16 US Bloomberg Bloomberg Economic Expectations January -5 – -11 01/16 US Bloomberg Bloomberg Consumer Comfort 12-January -31 – -28.4 01/17 US US Census Bureau Building Permits December 986K 1,014K 1,017K Page 2 of 7

- 3. 01/17 US US Census Bureau Building Permits MoM December -3.00% -0.30% -2.10% 01/17 US Federal Reserve Industrial Production MoM December 0.30% 0.30% 1.00% 01/17 US Federal Reserve Manufacturing (SIC) Production December 0.40% 0.30% 0.60% 01/16 EU Eurostat CPI MoM December 0.30% 0.30% -0.10% 01/16 EU Eurostat CPI YoY December 0.80% 0.80% 0.90% 01/17 EU Eurostat Construction Output MoM November -0.60% – -1.10% 01/17 EU Eurostat Construction Output YoY November -1.70% – -2.30% 01/16 China NSB Foreign Direct Investment YoY December 3.30% 2.50% 2.40% 01/16 Japan Ministry of Eco. Trade Tertiary Industry Index MoM November 0.60% 0.70% -0.90% 01/16 Japan Bank of Japan Domestic CGPI MoM December 0.30% 0.30% 0.00% 01/16 Japan Bank of Japan Domestic CGPI YoY December 2.50% 2.60% 2.60% 01/17 Japan ESRI Consumer Confidence Index December 41.3 43.0 42.5 Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar QCB issues government bonds, sukuk worth QR24bn – The Qatar Central Bank (QCB) has issued government bonds and sukuk for durations of 3 years and 5 years. The total amount of issuance is worth QR24bn. (QCB) NLCS’ net profit declines 55.5% QoQ in 4Q2013 – Alijarah Holding Company (NLCS) reported a net profit of QR3.3mn in 4Q2013, reflecting a decrease of 55.5% QoQ. Net profit for 2013 amounted to QR87.2mn, falling 54.1% YoY. Total income rose by 15.6% QoQ to QR52.9mn in 4Q2013, while it was down by 54.8% YoY to QR284.1mn in 2013. EPS amounted to QR1.76 in 2013 as compared to QR4.21 in 2012. Meanwhile, NLCS’ board of directors has proposed dividend distribution of QR1.5 per share (15% of the nominal value) to its shareholders. The company’s AGM has been scheduled on February 12, 2014, which will be adjourned to March 17, 2014 in the event of incomplete quorum. (QE) QATI reports QR753mn profit for 2013 – Qatar Insurance Company (QATI) has posted a net profit of QR753mn for the full-year of 2013 as compared to QR610mn in 2012. QATI’s board of directors has recommended a cash dividend of QR2.5 a share and a special bonus share of 25%. (Gulf-Times.com) MARK’s subsidiary completes IBB acquisition – Masraf Al Rayan (MARK) announced that its wholly-owned subsidiary Al Rayan (UK) Ltd had completed its acquisition of the Islamic Bank of Britain (IBB). IBB’s acquisition by Al Rayan UK follows a cash offer made on November 28, 2013, for which MARK has received valid shareholder acceptances exceeding 95% along with the approval of the Prudential Regulatory Authority. (QE) Fitch: Regional growth, debut issues to drive sukuk rebound in 2014 – According to Fitch Ratings, Qatar's imminent sukuk issuance worth roughly $3bn will kick start what may be a record year for the Shari’ah-compliant debt market. Regional growth and robust government spending are likely to be partially funded through sukuk programs in established GCC sukuk markets. At the same time, strong investor demand is likely to attract debut issues from Islamic and non-Islamic states in 2014. The push by the region’s sovereigns to become an Islamic finance hub is also likely to spur sukuk issuance. Fitch has estimated that issuance dropped around 12% to $120bn in 2013 partly due to market jitters over the US bond purchase tapering. However, demand remains strong and Fitch expect this decline to be a blip in the long-term trend of steady growth, with 2014 issuance likely to be at least in line with 2012's record of $137bn. (Peninsula Qatar) QNB Group’s AGM to be held on February 2 – QNB Group has announced that its AGM will be held on February 2, 2014 at Fareej Sharq Hotel and Resort. In absence of required quorum, the second meeting will be conducted on February 5, 2014 at the same place. The agenda of the AGM includes the board’s approval of the proposal to distribute to shareholders a cash dividend at the rate of 70% of the nominal value of the share, representing QR7.0 per share, among others. (QE) QISI’s BoD to meet on February 13 – Qatar Islamic Insurance Company’s (QISI) board of directors will meet on February 13, 2014 to discuss the company’s financial results ending on December 31, 2013. The board has also invited new membership nominations for QISI’s board for a period of three years (2014-2016). Nominations are open for 11 positions from January 19, 2014 until January 30, 2014. (QE) DBIS’ BoD to meet on February 4 – Dlala Brokerage & Investment Holding Company’s (DBIS) board of directors will meet on February 4, 2014 to discuss the company’s financial results ending December 31, 2013. (QE) QA to launch Saudi operations by 3Q2014; signs cargo deal with IAG – Qatar Airways’ (QA) CEO Akbar Al Baker said that the airline has reached an agreement with Saudi authorities on solving problems that blocked its entry into Saudi Arabia's domestic market. He said that Qatar Airways have already now appointed a new CEO for its Saudi operations, and planning to launch the Saudi operations anytime between the middle to the third quarter of this year. Meanwhile, Qatar Airways has reached a deal with British Airways’ parent IAG to provide it with cargo capacity. QA will operate five Boeing 777 freighters between London and Hong Kong on behalf of IAG Cargo starting from May 2014. The company said that these measures will curtail IAG’s cargo capacity by about 13%. London-based IAG’s Chief Executive Officer Willie Walsh said that this new partnership is an important step that enhances its relationship with Qatar. (Gulf-Times.com, Qatar Tribune) Cargo flights at HIA set to begin within a month – According to sources, cargo flights at the new Hamad International Airport (HIA) are expected to begin within a month. The New Doha International Airport Steering Committee’s Chairman Abdul Aziz al-Noaimi said that they are using the cargo terminal for the freight, but the actual landing will take place a month’s time from now. The committee’s spokesperson also confirmed that cargo flights were not landing at HIA at the moment, but the terminal was being used to store freight. HIA’s cargo terminal received the first cargo shipment from Qatar Airways on December 1, 2013, which was transferred from Europe to Doha International Airport by air and then onwards to the new cargo terminal at HIA via land. The new cargo terminal at HIA has an annual capacity of 1.4mn tons. (Gulf-Times.com) Page 3 of 7

- 4. International US Senate passes $1.1tn spending bill – The US Senate has passed the $1.1tn omnibus spending bill that eliminates the threat of another government shutdown at least until October. Passed by the House of Representatives a day earlier, the bill now goes to the White House for President Barack Obama’s approval, thus preventing another shutdown. While the Senate passed the massive bill by 72-26 votes, the House approved it by 359-67 votes earlier. All Senate Democrats supported the spending package, while 17 Republicans also voted in its favor. (ET) EU wants common rules for shale gas fracking – The European Commission wants EU member states to accept common environment and health rules if they use the controversial fracking method to develop their shale gas resources. A document prepared for the Commission's 2030 Energy & Climate Package recognizes the importance of the shale gas revolution, which has driven the US gas prices down sharply, but also recommends strong regulation to prevent environmental damage. (ET) Eurozone’s inflation slows in December on one-off effect in Germany – According to the European Union's statistics office, inflation in the Eurozone slowed in December, in what the ECB attributed last week to a one-off change in the method of calculating price growth in Germany. Consumer prices among 17 countries sharing the euro rose 0.3%, putting the annual inflation rate at 0.8%, down from 0.9% in November, but a tad above 0.7% in October. The ECB, which wants to keep inflation at around 2% over the medium-term, expects a prolonged period of low inflation, but sees no immediate risk of deflation. (Reuters) Ireland regains investment grade from Moody’s – Ireland’s credit rating was restored to investment grade by Moody’s after the country became the first to exit the EU bailout since the debt crisis erupted in 2009. Moody’s raised the country’s rating to Baa3 from Ba1 with a positive outlook. Earlier, Moody’s had cut the nation’s ranking five times in two years before assigning junk status in July 2011. The increase means all the three main credit rating companies now rate Ireland as investment grade. (Bloomberg) OPEC outages cut its oil output to below 2014 demand – The oil exporter group OPEC stated that it has lowered its output further and is pumping less than 2014’s global need for its crude oil, underlining the toll that outages in Libya and elsewhere are taking on production. The OPEC’s monthly report kept its global supply and demand forecasts unchanged, which point to a smaller market share in 2014 due to increasing supply from non-OPEC countries. However, the OPEC is relatively upbeat on economic prospects, seeing faster growth in 2014 of 3.5%, up from 2.9% in 2013 as monetary stimulus continues. (Reuters) Regional QNB Group: Africa needs infrastructure boost, prudent policies to reach emerging market status – According to a report by QNB Group, strong infrastructure investment and continued prudent macroeconomic policies will be essential if the African subcontinent is to achieve double-digit growth and reach an emerging market status. QNB Group’s latest estimates show that Sub-Saharan Africa (SSA) continues on its rapid growth momentum; the subcontinent grew by 5% in 2013 and is expected to reach 6-6.5% this year on the back of high investment spending and a growing middle class. QNB Group said this makes it the second fastest economic growth performance in the world, placing it next to China. QNB Group said from stagnation and high inflation in the 1980s, several African countries have managed to grow rapidly over the last two decades under moderate inflation. Countries such as Ethiopia, Mozambique, Rwanda, Tanzania and Uganda quadrupled their real GDP growth on average, while bringing inflation down into single digits, which has enabled millions of Africans. (Gulf-Times.com) GCC, China sign strategic action plan – GCC countries and China have signed a strategic dialogue action plan for the period from 2014 until 2017. Under the four-year blueprint, the two sides have pledged to boost bilateral relations in terms of political, economic, trade, educational, technical, environmental, health and sporting ties, in addition to promoting joint investments. (GulfBase.com) Al Rajhi Bank reports SR1,547mn net profit in 4Q2013 – Al Rajhi Bank has reported a net profit of SR1,547mn in 4Q2013, reflecting an decrease of 9.9% QoQ (-19.1% YoY). EPS stood at SR4.96 for the period ended December 31, 2013 as compared to SR5.26 on December 31, 2012. Total assets at the end of 2013 stood at SR279.9bn, growing 4.7% YoY. Loans & advances were up by 8.7% YoY to SR186.8bn, while consumer deposits rose by 4.6% YoY to SR231.6bn. (Tadawul) Medical insurance makes up 55% of total premiums in KSA – According to Standard & Poor’s (S&P), medical insurance now comprises about 55% of total insurance premiums paid in Saudi Arabia, up from around 40% in 2008. The ratings agency pointed out that the big Saudi insurance companies effectively control majority of the market’s distribution and ownership now. S&P said the Council of Cooperative Health Insurance has proven to be effective at steering the market to a more stable direction with a sustainable level of provision across the GCC region. Compulsory health schemes are now the norm. S&P expects a progressive surge in premium income from the introduction of compulsory medical insurance in Dubai, but probably not much of a material increase until 2015. (GulfBase.com) Madinah Investment Forum to explore SR4bn projects – The forthcoming Madinah Investment Forum will explore a series of mega projects in the region predicted to be worth SR4bn. The Forum’s Coordinator Ali Awari said that the forum is being organized by the Madinah Chamber of Commerce & Industry on February 12. Further, Ali Awari said that the two-day forum will discuss projects related to endowments, real estate and industry, in addition to a key project offered by the Yanbu Royal Commission. (GuflBase.com) Gulf Union to provide SR11.9mn technical reserve – The Gulf Union Cooperative Insurance Company (Gulf Union) has provided for an additional technical reserve of SR11.9mn. The additional reserve is based on the report of an independent actuary dated December 15, 2014, in accordance with SAMA Implementation Regulations for Insurance Companies. Consequently, this additional reserve will negatively impact on Gulf Union's financial statements for 4Q2013 and the year ended December 31, 2013, but it would enhance the company's ability to meet its obligations in the future. (Tadawul) Saudi construction on track to reach SR1.12tn – The construction & building sector in Saudi Arabia is forecasted to reach SR1.12tn in 2016, and stand second only to the oil sector. Dhahran International Exhibition’s CEO Mohamed Al-Husaini stated that the sector’s contribution to the country’s GDP in 2012 reached 16.5%. The construction sector grew by around 5.7% YoY in 3Q2013, down from 6.5% in 2Q. (GulfBase.com) Page 4 of 7

- 5. Aldrees declares SR60mn dividends for FY2013; to increase its capital through bonus shares – Aldrees Petroleum & Transport Services Company’s (Aldrees) board of directors has recommended the distribution of dividends worth SR60mn (SR2 per share), representing 20% of the face value for period FY2013. Those shareholders who are registered in the Security Depository Center on the day of the general assembly meeting (date to be announced) will be eligible for these dividends. The cash dividend will be distributed before the increase in company's capital, if approved. Meanwhile, Aldrees’ board of directors has recommended for an increase in the company’s capital through bonus shares. The company’s capital is to be raised by 33.33%, from SR300mn to SR400mn. With this, the number of shares would go up from 30mn shares to 40mn shares. The increase will be done through capitalization of SR100mn from account retained earnings and statutory reserves. (Tadawul) GGCIC gets SAMA’s approval for insurance products – The Gulf General Cooperative Insurance Company has obtained the Saudi Arabian Monetary Agency’s (SAMA) temporary approval to use of its insurance products for six months for various products. Some of the covered products are: burglary, travel, employers’ liability, workmen’s compensation, property all risks material damage, material damage and consequential loss, home insurance, marine open policy, marine cargo policy, etc. (Tadawul) SIECO declares SR5.4mn dividends for 2013 – Saudi Industrial Export Company’s (SIECO) board of directors has recommended the distribution of dividends worth SR5.4mn (SR0.5 per share), representing 5% of the face value for 2013. Those shareholders who are registered in the Security Depository Center on the day of shareholder meeting (date to be announced) will be eligible for these dividends. (Tadawul) ArcelorMittal’s plant begins production in Jubail – Global iron & steel company ArcelorMittal has begun commercial production at its plant in Jubail 2 Industrial Zone in the Kingdom. The mill located in Jubail Industrial City has a capacity of 600,000 tons a year built with an investment in excess of a billion dollars. ArcelorMittal’s CEO Timothy Erway said that about two-thirds of its capacity will be used for tubular products and the remainder for pipelines. (GulfBase.com) Vallourec sets up new venture in Dammam – The Eastern Province’s Governor Prince Saud bin Naif has opened the Vallourec plant for manufacturing oil & gas pipes at the second industrial city in Dammam. Meanwhile, the Minister of Commerce & Industry Tawfiq Al-Rabiah said that the ministry will continue to help commercial initiatives both from the public and private sectors. Al-Rabiah said that they have 647,220 plants and 94 of them are still under construction. The total cost of these plants has reached SR800bn and Saudization in these plants is 70%. Additionally, he said that there are now seven industrial cities in the Eastern Province, including Dammam and Hafr Al-Batin, and a few more are under construction. (GulfBase.com) Bahri receives Bahri Jeddah vessel – The National Shipping Company of Saudi Arabia (Bahri) has received a new vessel named “Bahri Jeddah” specialized in general cargo with a capacity of 26,000 DWT. Built by Hyundai MIPO in South Korea, Bahri Jeddah is the fifth vessel delivered among the six vessels that were contracted by the company in 2011 for a total value of SR1,543mn. The financial impact of the delivered vessel will materialize on the company’s revenue during 1Q2014. Bahri has one more general cargo vessel remaining under construction at Hyundai MIPO whose delivery is expected during 1Q2014. (GulfBase.com) Bank Al Jazira, MoneyGram sign deal – MoneyGram has announced an agreement with Bank Al Jazira to offer its services at multiple bank and remittance centers. The alliance gives access to over-the-counter global money transfers to consumers along with the ability to send and receive money in just 10 minutes. (GulfBase.com) Saudi Gulf signs $2bn deal to buy Bombardier planes – Dammam-based New Saudi Gulf Airlines has signed a $2bn deal with Canadian aircraft company Bombardier to buy 16 CSeries jets with options for 10 more. Delivery of these CS300 jets with seating capacity of 130-160 passengers is expected to happen by the end of 2015. Meanwhile, Saudi Gulf is expected to start operating in 2014 or in 2015. (Peninsula Qatar) UAE to attract $14.4bn FDI in 2014 – According to sources, the UAE is expected to attract foreign direct investment (FDI) worth $14.4bn in 2014, a 20% rise over 2013. The UAE Ministry of Economy’s Undersecretary for Foreign Trade Sector Abdulla Al Saleh said that the country also recorded a 20% YoY growth in FDI last year, reaching $12bn. Al Saleh said that in 2013, the UAE was able to attract three times more FDI than expected, adding that increased government spending and a significant resurgence in tourism, transport and trade have contributed to this upswing. He mentioned that FDI jumped by 200% to reach $12bn in 2013, rising from $4bn in 2007. (GulfBase.com) West Coast to set up AED60mn paper, plastic products plant – West Coast Company will set up a new manufacturing facility in the Khalifa Industrial Zone Abu Dhabi (Kizad), in order to expand its business targeting the GCC market. The new facility will be located in Kizad’s mixed-use cluster and will commence operations in June 2014. The facility’s first line will focus on producing paper-based products including facial tissues, toilet rolls and hand towels, and will have a production volume of 120-150 tons per month. The second line will focus on the production of plastic-based products such as shopping and waste bags, and will have a production volume between 60-80 tons per month. (GulfBase.com) Gulftainer increases its market dominance in 2013 – The Sharjah-based Gulftainer Company Ltd has increased its market dominance in 2013 by controlling one-fifth of total containerized trade in the GCC region. The cargo company achieved this significant milestone due to its streamlined operations and commercial efforts. Gulftainer now plans to increase its global portfolio to handle up to 18mn twenty-foot equivalent units (TEUs) by 2020. (GulfBase.com) Shuaa hires for its institutional brokerage – Shuaa Capital, which had cut jobs and shut its retail operations, is hiring for its institutional brokerage as the investment bank bets on a further increase in the stock market. The company’s spokesman Oliver Schutzmann said that it is planning to add equity traders on the back of the current positive momentum in the market. (GulfBase.com) Rotana plans to open four new hotels with 1,500 rooms in 1Q2014 – Rotana is planning to open four new hotels with nearly 1,500 rooms in the Middle East. Rotana manages a significant portfolio of properties throughout the Middle East, Africa, South Asia and Eastern Europe regions. The hotel management company plans to will add 1,096 rooms in Gulf countries including the UAE during 1Q2014, and an additional 400 rooms during the forthcoming summer in Jordan. (GulfBase.com) Page 5 of 7

- 6. Dubai’s inflation rises 1.31% in 2013 – According to a report by the Dubai Statistics Centre, the inflation rate in Dubai in 2013 increased 1.31% over 2012, mainly due to an increase in the prices of the beverages & tobacco group by 14.79%. Other factors that affected the inflation rate included a rise in the education group by 4.58%; furnishings, household equipment & routine household maintenance by 3.37%; food by 2.55%; recreations & culture by 1.79%; transport by 1.62%; housing, water, electricity, gas & other fuels by 1.22%; restaurants & hotels by 1.16%; and health by 1.14%. On the other hand, the inflation rate for clothing & footwear declined by 2.65%; communication by 1.04%; and miscellaneous goods & services by 0.28%. (GulfBase.com) Dubal converted into PJSC with AED3bn capital – The UAE Prime Minister & Vice President, HE Highness Shaikh Mohammed bin Rashid Al Maktoum has issued Law No. (1) of 2014 converting Dubai Aluminium (Dubal) into a private joint stocks company (PJSC). Pursuant to the law, the name of the new company is “Dubai Aluminium PJS” with a declared capital of AED3bn, which would be headquartered in Dubai and may establish branches inside and outside the UAE. The law stated that Dubai Aluminium PJS subrogates Dubai Aluminium in all legal and business obligations and rights starting from the date of effective of this law, and the employees of Dubai Aluminium shall benefit from their vested right. (GulfBase.com) Dubai Group signs $10bn debt restructuring deal – According to sources, Dubai Group has signed a $10bn debt restructuring agreement, bringing an end to the last major issue remaining from the Emirate’s 2009 financial crisis. The investment vehicle owned by the Emirate’s ruler signed the restructuring deal. Lenders to the unit of Dubai Holding, which include France’s Natixis and Dubai’s Emirates NBD, still have to sign the last piece of documentation. Out of its total $10bn debt, Dubai Group owes $6bn to banks and the remaining $4bn is classified as inter-company loans. (Peninsula Qatar) DEWA signs new electrical contracts – The Dubai Electricity & Water Authority’s (DEWA) Managing Director & CEO Saeed Mohammed Al Tayer has signed a contracts with Power Magic Electrical Works LLC and Gulf Sands Contracting LLC, to complete low voltage cable-laying works within a week of receiving requests made by Dewa’s relevant departments. The contracts ensure the highest standards of excellence and through such agreements, DEWA aims to strengthen the electricity infrastructure of Dubai. (GulfBase.com) du Telecom doubles 4G LTE footprint in 2013 – The Emirates Integrated Telecommunications Company (du Telecom) has increased its 4G LTE footprint by more than double during 2013. Du also doubled the original radio capacity to accommodate the significant increase in mobile data traffic, since the launch of its 4G network in June 2012. During 2012-13 alone, du Telecom’s investments in its 3G and 2G network capabilities have resulted in an increase of its radio network capacity by 60%. (GulfBase.com) RAKBANK’s BoD will meet on January 27 – The National Bank of Ras Al Khaimah's (RAKBANK) board of directors will meet on January 27, 2014 to approve of financial statements for the year ended December 2013 and the distribution of profits and appropriation of reserves. (ADX) NBO revamps SBU to motivate SME sector – The National Bank of Oman (NBO) will revamp its Small Business Unit (SBU) in a bid to extend support the small & medium enterprises (SME) sector in Oman. The bank will launch specific segment offerings under the Tijarati Banking Unit, a specialized department that will focus on services for SMEs, to fully cater to the diversity within the segment, and offer targeted support to customers. The SBU will offer a comprehensive range of products including collateral-backed and collateral-free financial offerings. (GulfBase.com) BAC signs BHD1.2mn deal for new passenger boarding bridges – Bahrain Airport Company (BAC) has signed an agreement with Shenzhen CIMC TIANDA Airport Support Ltd to replace the existing passenger bridges at Bahrain International Airport with new state-of-the-art passenger boarding bridges. As per the BHD1.2mn agreement, 7 CIMC TIANDA passenger boarding bridges will be installed to replace the existing bridges to further enhance the airport’s operations and travel experience. The new bridges will not only provide weather protection, comfort, and safe walkway between terminal and aircrafts; but they will also be designed to create a welcoming ambience for passengers. (GulfBase.com) Gulf Air signs $100m deal with Rolls-Royce; unveils $20mn A330 retrofit – Bahrain-based Gulf Air has signed a five-year agreement to extend Rolls-Royce TotalCare support for its fleet of six A330 aircraft powered by Trent 700 engines. The agreement worth over $100mn extends the previous five-year agreement that was signed in 2009. Meanwhile, Gulf Air has also signed contracts totaling approximately $20mn to appoint Avianor, Zodiac Aerospace and BE Aerospace as partners for the retrofit of its A330 fleet. Gulf Air’s planned A330 retrofit, scheduled to be completed in 4Q2014, is part of the airline’s ongoing proactive re-fleeting and product enhancement strategy. (GulfBase.com) Aero Gulf signs MoU with KHCB for financing – Bahrainbased Aero Gulf Group has signed a memorandum of understanding (MoU) with Khaleeji Commercial Bank (KHCB) for financing support of its aviation investment program. KHCB is committed to provide Islamic finance to underpin the business growth plans of Aero Gulf Group and in particular its operations within the aviation maintenance, repair and overhaul (MRO) sector. The Aero Gulf Sola Engine Centre in Norway, which was purchased from Pratt & Whitney late 2013, forms the cornerstone of a growing aviation portfolio that will focus on the provision of MRO services across the Middle East and North Africa. (GulfBase.com) Batelco, Huawei sign MoU on 4G delivery – Bahrain Telecommunications Company (Batelco) and Chinese telecom company Huawei have signed a memorandum of understanding (MoU) on the sidelines of Bahrain International Airshow 2014. Batelco’s Chairman Shaikh Hamad bin Abdullah Al Khalifa and Huawei’s VP Middle East Huang Ji signed the MoU covering the delivery of 4G services for Batelco’s subsidiary SURE Telecom in Guernsey, Jersey and the Isle of Man. Under the agreement, Huawei will deliver and integrate 4G LTE base stations into SURE's network. (GulfBase.com) Investcorp sells TDX Group to Equifax for £200mn – Investcorp, together with the founders of the TDX Group (TDX) has agreed the sale of TDX to Equifax Inc., for £200mn. Through its technology fund, Investcorp Technology Partners III, Investcorp had acquired a substantial minority stake in TDX in 2008, becoming the largest and only institutional shareholder alongside TDX's three founders. (GulfBase.com) Ithmaar Bank appoints new CEO – Ithmaar Bank has appointed Ahmed Abdul Rahim as the new chief executive officer. Abdul Rahim had been the bank's acting chief executive officer since September 2013. (Bloomberg) Page 6 of 7

- 7. Rebased Performance Daily Index Performance 170.0 160.0 150.0 140.0 130.0 120.0 110.0 100.0 90.0 80.0 139.2 0.8% 126.3 0.4% 1.3% 1.2% 0.8% 0.2% 0.3% 0.0% 0.0% May-13 S&P Pan Arab Dec-13 S&P GCC Source: Bloomberg Asset/Currency Performance Gold/Ounce Silver/Ounce Crude Oil (Brent)/Barrel (FM Future) Natural Gas (Henry Hub)/MMBtu North American Spot LPG Propane Price North American Spot LPG Normal Butane Price Euro Yen Dubai Oct-12 (0.2%) Abu Dhabi QE Index Mar-12 Bahrain Aug-11 Kuwait* Jan-11 (0.3%) Qatar (0.8%) Oman (0.4%) Saudi Arabia Jun-10 1.6% 159.6 Source: Bloomberg (*Market closed on January 16, 2014) Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% 1,254.05 0.9 0.4 4.0 DJ Industrial 16,458.56 0.3 0.1 (0.7) 20.33 1.1 0.8 4.4 S&P 500 1,838.70 (0.4) (0.2) (0.5) 106.48 (0.6) (0.7) (3.9) NASDAQ 100 4,197.58 (0.5) 0.5 0.5 4.39 (3.2) 11.2 1.1 STOXX 600 335.82 0.5 1.8 2.3 137.50 5.2 7.6 8.9 DAX 9,742.96 0.3 2.8 2.0 150.50 4.9 8.4 10.3 FTSE 100 6,829.30 0.2 1.3 1.2 1.35 (0.6) 104.32 (0.0) (0.9) (1.5) CAC 40 0.1 (0.9) Nikkei GBP 1.64 0.4 (0.4) (0.8) MSCI EM CHF 1.10 (0.6) (0.8) (1.9) SHANGHAI SE Composite AUD 0.88 (0.5) (2.4) (1.5) USD Index 81.23 0.4 0.7 RUB 33.56 0.4 1.5 BRL 0.43 0.6 0.8 0.6 4,327.50 0.2 1.8 0.7 15,734.46 (0.1) (1.1) (3.4) 972.27 (0.2) 0.2 (3.0) 2,004.95 (0.9) (0.4) (5.2) HANG SENG 23,133.35 0.6 1.3 (0.7) 1.5 BSE SENSEX 21,063.62 (0.9) 1.5 (0.5) 2.1 Bovespa 49,181.86 (1.0) (1.0) (4.5) 1,395.79 (0.1) (0.0) (3.3) Source: Bloomberg RTS Source: Bloomberg Contacts Saugata Sarkar Ahmed M. Shehada Keith Whitney Sahbi Kasraoui Head of Research Head of Trading Head of Sales Manager - HNWI Tel: (+974) 4476 6534 Tel: (+974) 4476 6535 Tel: (+974) 4476 6533 Tel: (+974) 4476 6544 saugata.sarkar@qnbfs.com.qa ahmed.shehada@qnbfs.com.qa keith.whitney@qnbfs.com.qa sahbi.alkasraoui@qnbfs.com.qa QNB Financial Services SPC Contact Center: (+974) 4476 6666 PO Box 24025 Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7