Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Destaque

Destaque (8)

Semelhante a 14 August Daily market report

Semelhante a 14 August Daily market report (20)

Mais de QNB Group

Mais de QNB Group (20)

14 August Daily market report

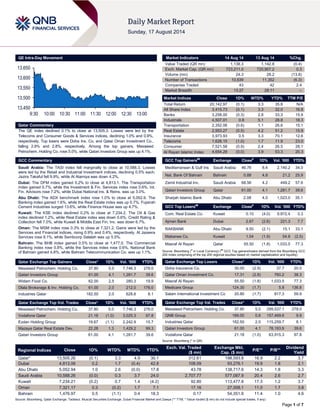

- 1. Page 1 of 7 QE Intra-Day Movement Qatar Commentary The QE index declined 0.1% to close at 13,505.3. Losses were led by the Telecoms and Consumer Goods & Services indices, declining 1.0% and 0.9%, respectively. Top losers were Doha Ins. Co. and Qatar Oman Investment Co., falling 2.9% and 2.8%, respectively. Among the top gainers, Mesaieed Petrochem. Holding Co. rose 5.0%, while Qatari Investors Group was up 4.1%. GCC Commentary Saudi Arabia: The TASI index fell marginally to close at 10,588.3. Losses were led by the Retail and Industrial Investment indices, declining 0.5% each. Jazira Takaful fell 9.9%, while Al Alamiya was down 4.2%. Dubai: The DFM index gained 0.2% to close at 4,813.1. The Transportation index gained 0.7%, while the Investment & Fin. Services index rose 0.6%. Int. Fin. Advisors rose 7.2%, while Dubai National Ins. & Reins. was up 3.0%. Abu Dhabi: The ADX benchmark index rose 1.0% to close at 5,052.9. The Banking index gained 1.6%, while the Real Estate index was up 0.7%. Fujairah Cement Industries surged 13.6%, while Finance House was up 4.7%. Kuwait: The KSE index declined 0.2% to close at 7,234.2. The Oil & Gas index declined 1.2%, while Real Estate index was down 0.6%. Credit Rating & Collection fell 7.0%, while Kuwait & Middle East Fin. Inv. was down 6.7%. Oman: The MSM index rose 0.3% to close at 7,321.2. Gains were led by the Services and Financial indices, rising 0.9% and 0.4%, respectively. Al Jazeera Services rose 9.1%, while Sembcorp Salalah was up 5.5%. Bahrain: The BHB index gained 0.5% to close at 1,477.0. The Commercial Banking index rose 0.8%, while the Services index rose 0.6%. National Bank of Bahrain gained 4.8%, while Bahrain Telecommunication Co. was up 1.1%. Qatar Exchange Top Gainers Close* 1D% Vol. ‘000 YTD% Mesaieed Petrochem. Holding Co. 37.80 5.0 7,746.3 278.0 Qatari Investors Group 61.00 4.1 1,281.7 39.6 Widam Food Co. 62.00 2.5 280.3 19.9 Dlala Brokerage & Inv. Holding Co. 61.00 2.0 212.0 176.0 Industries Qatar 182.50 2.0 628.8 8.1 Qatar Exchange Top Vol. Trades Close* 1D% Vol. ‘000 YTD% Mesaieed Petrochem. Holding Co. 37.80 5.0 7,746.3 278.0 Vodafone Qatar 21.18 (1.0) 3,025.3 97.8 Ezdan Holding Group 19.67 (1.1) 2,242.9 15.7 Mazaya Qatar Real Estate Dev. 22.28 1.3 1,429.2 99.3 Qatari Investors Group 61.00 4.1 1,281.7 39.6 Market Indicators 14 Aug 14 13 Aug 14 %Chg. Value Traded (QR mn) 1,138.3 1,142.8 (0.4) Exch. Market Cap. (QR mn) 723,211.0 720,907.2 0.3 Volume (mn) 24.3 28.2 (13.8) Number of Transactions 10,639 11,352 (6.3) Companies Traded 43 42 2.4 Market Breadth 13:27 28:11 – Market Indices Close 1D% WTD% YTD% TTM P/E Total Return 20,142.97 (0.1) 3.3 35.8 N/A All Share Index 3,415.73 (0.1) 3.3 32.0 16.8 Banks 3,258.00 (0.3) 2.8 33.3 15.9 Industrials 4,507.01 0.8 5.1 28.8 18.3 Transportation 2,352.06 (0.6) 1.1 26.6 15.1 Real Estate 2,953.27 (0.5) 4.2 51.2 15.9 Insurance 3,973.93 0.5 3.3 70.1 12.6 Telecoms 1,626.15 (1.0) 1.7 11.9 23.0 Consumer 7,521.58 (0.9) 2.4 26.5 28.1 Al Rayan Islamic Index 4,654.29 (0.0) 3.9 53.3 20.3 GCC Top Gainers## Exchange Close# 1D% Vol. ‘000 YTD% Mediterranean & Gulf Ins Saudi Arabia 46.76 8.4 2,140.2 34.0 Nat. Bank Of Bahrain Bahrain 0.88 4.8 21.2 25.9 Zamil Industrial Inv. Saudi Arabia 68.56 4.2 449.2 57.6 Qatari Investors Group Qatar 61.00 4.1 1,281.7 39.6 Sharjah Islamic Bank Abu Dhabi 2.08 4.0 1,023.0 35.1 GCC Top Losers## Exchange Close# 1D% Vol. ‘000 YTD% Com. Real Estate Co. Kuwait 0.10 (4.0) 9,972.4 3.3 Ajman Bank Dubai 2.67 (2.6) 221.3 7.7 RAKBANK Abu Dhabi 9.50 (2.1) 15.1 33.1 Mabanee Co. Kuwait 1.04 (1.9) 54.8 (2.5) Masraf Al Rayan Qatar 55.50 (1.8) 1,033.5 77.3 Source: Bloomberg ( # in Local Currency) ( ## GCC Top gainers/losers derived from the Bloomberg GCC 200 Index comprising of the top 200 regional equities based on market capitalization and liquidity) Qatar Exchange Top Losers Close* 1D% Vol. ‘000 YTD% Doha Insurance Co. 30.00 (2.9) 37.7 20.0 Qatar Oman Investment Co. 17.31 (2.8) 760.2 38.3 Masraf Al Rayan 55.50 (1.8) 1,033.5 77.3 Medicare Group 124.30 (1.7) 5.8 136.8 Salam International Investment Co 20.80 (1.7) 817.3 59.9 Qatar Exchange Top Val. Trades Close* 1D% Val. ‘000 YTD% Mesaieed Petrochem. Holding Co. 37.80 5.0 299,537.1 278.0 QNB Group 189.00 0.6 157,469.6 9.9 Industries Qatar 182.50 2.0 115,259.7 8.1 Qatari Investors Group 61.00 4.1 78,193.9 39.6 Vodafone Qatar 21.18 (1.0) 63,915.3 97.8 Source: Bloomberg (* in QR) Regional Indices Close 1D% WTD% MTD% YTD% Exch. Val. Traded ($ mn) Exchange Mkt. Cap. ($ mn) P/E** P/B** Dividend Yield Qatar* 13,505.26 (0.1) 3.3 4.9 30.1 312.61 198,593.8 16.9 2.2 3.7 Dubai 4,813.06 0.2 1.7 (0.4) 42.8 108.09 93,276.1 19.9 1.8 2.1 Abu Dhabi 5,052.94 1.0 2.6 (0.0) 17.8 43.78 138,717.6 14.3 1.8 3.3 Saudi Arabia 10,588.26 (0.0) 0.3 3.7 24.0 2,707.77 577,087.9 20.4 2.6 2.7 Kuwait 7,234.21 (0.2) 0.7 1.4 (4.2) 92.80 113,477.8 17.3 1.2 3.7 Oman 7,321.17 0.3 (0.2) 1.7 7.1 17.16 27,008.1 11.0 1.7 3.8 Bahrain 1,476.97 0.5 (1.1) 0.4 18.3 0.17 54,351.9 11.4 1.0 4.6 Source: Bloomberg, Qatar Exchange, Tadawul, Muscat Securities Exchange, Dubai Financial Market and Zawya (** TTM; * Value traded ($ mn) do not include special trades, if any) 13,450 13,500 13,550 13,600 13,650 9:30 10:00 10:30 11:00 11:30 12:00 12:30 13:00

- 2. Page 2 of 7 Qatar Market Commentary The QE index declined 0.1% to close at 13,505.3. The Telecoms and Consumer Goods & Ser. indices led the losses. The index fell on the back of selling pressure from Qatari shareholders despite buying support from non-Qatari shareholders. Doha Insurance Co. and Qatar Oman Investment Co. were the top losers, falling 2.9% and 2.8%, respectively. Among the top gainers, Mesaieed Petrochem. Holding Co. rose 5.0%, while Qatari Investors Group was up 4.1%. Volume of shares traded on Thursday fell by 13.8% to 24.3mn from 28.2mn on Wednesday. However, as compared to the 30- day moving average of 16.9mn, volume for the day was 44.1% higher. Mesaieed Petrochem. Holding Co. and Vodafone Qatar were the most active stocks, contributing 31.8% and 12.4% to the total volume respectively. Source: Qatar Exchange (* as a % of traded value) Ratings, Earnings and Global Economic Data Ratings Updates Company Agency Market Type* Old Rating New Rating Rating Change Outlook Outlook Change Abu Dhabi National Insurance Co. (ADNIC) AM Best Abu Dhabi FSR/ICR A/a A/a – Stable – National Takaful Insurance Co (NTIC) Moody’s Kuwait IFSR Ba1 Ba1 – Stable Source: News reports (* LT – Long Term, ST – Short Term, FSR– Financial Strength Rating, FCR – Foreign Credit Rating, LCR – Local Currency Rating, IDR – Issuer Default Rating, SR – Support Rating, LC – Local Currency, ICR – Issuer Credit Rating. IFSR – Insurance Financial Strength Rating) Earnings Releases Company Market Currency Revenue (mn)2Q2014 % Change YoY Operating Profit (mn) 2Q2014 % Change YoY Net Profit (mn) 2Q2014 % Change YoY United Foods Co. (UFC) Dubai AED 117.8 9.5% – – 6.0 -17.5% Al Firdous Holdings Dubai AED 3.5 -2.9% – – -0.6 -242.0% Dubai Islamic Insurance & Reinsurance Co. (Aman) Dubai AED 69.4 3.7% -6.1 NA -6.4 NA National Cement Co. (NCC) Dubai AED 69.0 3.6% – – 33.1 51.0% United Kaipara Dairies Co. (Unikai) Dubai AED 94.8 14.6% – – -6.9 NA Al Khazna Insurance Co. (AKIC)* Abu Dhabi AED 54.8 11.6% 7.9 0.5% -44.4 NA Hits Telecom Holding Co. Kuwait KD – – – – 0.4 2498.8% National Industries Group Holding (NIG) Kuwait KD 28.2 2.6% – – 3.0 -48.1% Agility Public Warehousing Co. Kuwait KD 341.7 -3.8% – – 12.9 11.8% Al Fajar Al Alamia Co.* Oman OMR 16.9 16.1% – – 1.5 86.5% Gulf Finance House (GFH) Bahrain USD 58.5 337.0% – – 7.2 165.7% Source: Company data, DFM, ADX, MSM (*1H2014 results) Global Economic Data Date Market Source Indicator Period Actual Consensus Previous 08/14 US Department of Labor Initial Jobless Claims 9 August 311K 295K 290K 08/14 US BLS Import Price Index MoM July -0.20% -0.30% 0.10% 08/14 US BLS Import Price Index YoY July 0.80% 0.80% 1.10% 08/14 US Bloomberg Bloomberg Consumer Comfort 10 August 36.8 – 36.2 08/15 US Federal Reserve Bank Empire Manufacturing August 14.69 20 25.6 08/15 US BLS PPI Final Demand MoM July 0.10% 0.10% 0.40% 08/15 US BLS PPI Final Demand YoY July 1.70% 1.70% 1.90% 08/15 US US Treasury Net Long-term TIC Flows June -$18.7B – $18.6B 08/15 US US Treasury Total Net TIC Flows June -$153.5B – $33.1B 08/15 US Federal Reserve Industrial Production MoM July 0.40% 0.30% 0.40% 08/15 US Federal Reserve Capacity Utilization July 79.20% 79.20% 79.10% 08/15 US Federal Reserve Manufacturing (SIC) Production July 1.00% 0.40% 0.30% 08/14 EU Eurostat CPI MoM July -0.70% -0.60% 0.10% 08/14 EU Eurostat CPI YoY July 0.40% 0.40% 0.40% 08/14 EU Eurostat CPI Core YoY July 0.80% 0.80% 0.80% Overall Activity Buy %* Sell %* Net (QR) Qatari 54.67% 67.06% (141,020,700.93) Non-Qatari 45.33% 32.94% 141,020,700.93

- 3. Page 3 of 7 08/14 EU Eurostat GDP SA YoY 2Q2014 0.70% 0.70% 0.90% 08/14 France INSEE GDP YoY 2Q2014 0.10% 0.30% 0.80% 08/14 Germany Destatis GDP SA QoQ 2Q2014 -0.20% -0.10% 0.70% 08/14 Germany Destatis GDP WDA YoY 2Q2014 1.20% 1.40% 2.30% 08/14 Germany Destatis GDP NSA YoY 2Q2014 0.80% 1.30% 2.50% 08/14 UK RICS RICS House Price Balance July 49% 51% 52% 08/15 UK ONS GDP QoQ 2Q2014 0.80% 0.80% 0.80% 08/15 UK ONS GDP YoY 2Q2014 3.20% 3.10% 3.10% 08/15 UK ONS Index of Services MoM June 0.30% 0.30% 0.30% 08/15 UK ONS Index of Services 3M/3M June 1.00% 1.00% 1.00% Source: Bloomberg (s.a. = seasonally adjusted; n.s.a. = non-seasonally adjusted; w.d.a. = working day adjusted) News Qatar MPHC: no contractual relations with MSCI – Mesaieed Petrochemical Holding Company (MPHC) – a subsidiary of Qatar Petroleum (QP) – has issued a clarification statement advising shareholders of the statement issued by MSCI Inc. MSCI Inc. through their press release issued on August 13, 2014, included MPHC in their MSCI Emerging Market Index and MSCI ACWI Growth Index. MSCI Inc. through their press release issued on August 14, 2014 mentioned that MPHC will not be added to their Index contrary to what was stated earlier by MSCI Inc. In this regard, MPHC would like to confirm that it has no contractual relationship with MSCI Inc. nor does MSCI Inc coordinate with MPHC on any of its matters. MPHC is therefore not responsible for any of MSCI Inc’s decisions. (Peninsula Qatar) MRDS reports QR32.5mn net profit in 2Q2014 – Mazaya Qatar Real Estate Development Company (MRDS) reported a net profit of QR32.5mn in 2Q2014 vs. QR22.4mn in 1Q2014 (QR8.4mn in in 2Q2013), growing by 45.3% QoQ. Similarly, net profit in 1H2014 grew to QR54.9mn as compared to QR10.3mn in 1H2013. The jump in profit is a result of construction activity numbers, which were not included in 2Q2013. MRDS’ revenue (construction revenue + rental income) stood at QR88.1mn in 2Q2014 as compared to QR9.6mn in 2Q2013 (QR181.9mn in 1H2014 as compared to QR19.1mn in 1H2013). The company’s EPS amounted to QR0.549 in 1H2014 versus QR0.103 in 1H2013. (QE) QNB Group: World Cup to benefit Qatar economy in long term – According to QNB Group (QNBK), Qatar is likely to be an economic winner from the World Cup. QNB Group said in its recent report that Qatar can draw useful lessons from the experience of countries and cities which hosted major sporting events. It said that Qatar’s economy has now entered a new diversification phase driven by large infrastructure spending and rapid population growth in preparation for the 2022 World Cup. This phase is just an interim milestone in the larger vision of establishing a knowledge-based economy as set out in the Qatar National Vision 2030, it said; adding in this sense, hosting the World Cup is a means to achieving a longer-term goal of modernizing the Qatari economy. Highlighting that for a knowledge-based economy to flourish, the right physical and human capital are needed, QNBK said the 2022 FIFA World Cup provides a useful focal point to complete the required infrastructure and move to the next growth phase and also helps promote Qatar to the world and attract a growing number of skilled workers. In this respect, QNBK said that Qatar is likely to be an economic winner from the World Cup. QNBK said a longer-term perspective, however, is needed to judge the economic merits of hosting a major sporting event. This perspective could provide useful lessons for Qatar, where the 2022 World Cup will take place. (Gulf-Times.com) ORDS launches services in Myanmar – Ooredoo (ORDS) officially launched its mobile services in Myanmar with celebrations held in the country’s capital city, Naypyidaw. With the launch, affordable telecommunications services are available to Myanmar’s people for the first time. Internet access on a mobile device has also become widely available for the first time. ORDS has achieved a world first by rolling out a new network using next generation UMTS900 technology, which offers customers in Myanmar 3G service and fast Internet, as well as a solid foundation for a future move into 4G services. (Peninsula Qatar) Expert sees bright future for solar technology in Qatar – According to an expert, solar power technology has a huge potential in Qatar despite the country being one of the strongholds of the oil & gas industry in the Middle East. Denmark-based SolarDrive’s General Manager Kim Ahrenfeldt said he is optimistic in the future of solar technology in Qatar and that it could be a billion dollar investment even if the country is mostly dependent on its oil & gas sector. (Gulf-Times.com) International US industrial production edged up in July; Consumer sentiment fell in August to 9-month low – Industrial production in the US rose 0.4% in July 2014, remaining unchanged from June. Economists polled by Reuters had forecast industrial output to rise by 0.3%. Manufacturing output grew 1.0%, in what the Fed said was the largest increase since February. Mining production moved up 0.3%, the ninth consecutive monthly increase. However, utility output fell 3.4% due to mild July weather that cut demand for air conditioning. Meanwhile, consumer confidence unexpectedly declined in August to a nine-month low, repressed by gloomy wage perceptions. According to the Thomson Reuters/University of Michigan, the Preliminary Sentiment Index dropped to 79.2, the lowest since November, from 81.8 in July. It was lower than any figure projected by economists surveyed by Bloomberg and represented the biggest negative surprise in a decade. The retreat in confidence was due to mounting concerns about the economic outlook as households said earnings would probably not climb as fast as prices. That bolsters the Federal Reserve Chairperson Janet Yellen’s argument that there is weakness in the labor market that requires the central bank to maintain monetary stimulus well into 2015. (Reuters, Bloomberg) UK economy grows at fastest pace in 6 years in 2Q2014 – The data from the Office for National Statistics (ONS) showed that Britain's economy maintained its strong growth in the second quarter of 2014, registering its best performance in more than six years. GDP expanded by 0.8% in the April-June period, as reported in preliminary data last month, which is at the same pace as in 1Q2014. The economy expanded by 3.2% YoY, up slightly from an estimate of 3.1% in the preliminary reading, which was the fastest yearly growth since the end of 2007.

- 4. Page 4 of 7 Economists in a Reuters poll had expected a quarterly growth of 0.8% and a yearly expansion of 3.1%. The ONS said the upward revision of the annual growth rate was due to a sturdy performance by the construction sector, which was stronger than assumed at the time of the preliminary estimate. The data also confirmed that Britain's economy was 0.2% bigger than its previous peak before the financial crisis in 1Q2008. The ONS is changing its methodology for calculating GDP and will provide those details shortly. Despite the strong pace of economic growth, the Bank of England dampened expectations of a rate hike this year. The central bank said it was paying close attention to prospects for pay, which has been very weak in recent months. (Reuters) Fitch raised Ireland’s rating to A- on growing economy – Ireland’s sovereign credit rating was raised to A- by Fitch Ratings as the country’s economy has begun to grow. Fitch said the rating was increased from BBB+ with a stable outlook. Ireland is recovering from the collapse of its real estate market after a decade-long housing boom, a crash that forced the country to take an international bailout. According to Dublin- based Davy, Ireland’s largest securities firm, the country exited the rescue program in 2013 and its economy is expected to grow by 3.5% this year. Fitch said market financing conditions have steadily improved over the past two years. Economic growth will become more balanced as domestic demand turns positive driven by private consumption and investment. The yield on Ireland’s benchmark 10-year government bonds fell below 2% for the first time on record today, reaching a low of 1.97%. Irish borrowing costs have tumbled since the height of the country’s financial crisis, when the nation’s government pledged to inject €67.5bn into its banking system. Earlier in June, Standard & Poor’s boosted its rating on the country’s debt to A- from BBB+, which indicates that Ireland’s capacity to repay bondholders is strong. Moody’s Investors Service also raised its ranking to Baa1 in May 2014. (Bloomberg) Eurozone economy grinds to halt even before Russia sanctions bite – Economic growth in the Eurozone came to a halt in the second quarter as Germany's economy shrank and France's stagnated. The zero growth reported by statistics agency Eurostat was a major cause for alarm throughout the 18- nation region, which is already bracing up for the impact of sanctions imposed on and by Russia over Ukraine. Germany contracted by 0.2% in 2Q2014, undercutting Bundesbank’s forecasts that GDP would remain unchanged. France fared little better; its GDP failed to grow for the second quarter in a row. That forced the French government to confront reality, saying it would miss its budget deficit target this year and cut its 2014 forecast for 1% growth in half. Italy, the Eurozone's third-largest economy, slid back into recession for the third time since 2008, shrinking by 0.2% in 2Q2014. Pressure grew on Italian Prime Minister Matteo Renzi to complete the promised structural reforms. (Reuters) ABC to sell 40bn yuan preferred stock this year – Agricultural Bank of China Ltd. (ABC) may raise as much as 40bn yuan by selling preferred shares this year as part of its plan to raise a total of 80bn yuan. The Beijing-based lender has applied to the China Securities Regulatory Commission to sell 400 million of its preferred shares this year after getting an approval from the China Banking Regulatory Commission. The share sale will bolster ABC’s capital position and allow it to conform to stricter requirements introduced by the government in January 2013. The bank first announced its plan for the sale in May 2014. Earlier, Mizuho Securities Asia had estimated that China’s four biggest banks will face a capital shortfall of $87bn under the new rules by 2019. (Bloomberg) Regional SATLUB achieves ISO certificate – Saudi Total Lubricants Company (SATLUB) has achieved ISO 9001 Quality Management System Certification for its plant in King Abdullah Economic City. The certificate was rewarded within 10 months of plant operation. (GulfBase.com) Eiger Trading launches automated Murabaha platform – Eiger Trading launched the first fully-automated, Shari’ah compliant Commodity Murabaha platform. Rolled out in conjunction with Gulf International Bank’s KSA retail arm, under the ‘Meem’ brand name, this fully-automated Islamic e-banking solution will offer 24/7 online personal finance and deposits to retail clients in Saudi Arabia. (GulfBase.com) Wared buys land in KAEC Industrial Valley – Wared Logistics has signed a contract to buy 75,000 square meters of land in the Industrial Valley Phase 2 of King Abdullah Economic City (KAEC) to provide exclusive logistic services for KAEC companies. Wared is a joint venture between Zahid Group Holding and Saudi Binladin Group. (GulfBase.com) KSA spending on telecom, IT to reach SR108.7bn in 2014 – According to a financial report by Al-Eqtisadiah daily, spending on telecom and IT in Saudi Arabia is poised to grow by more than 6% to SR108.7bn in 2014, as compared to SR102.6bn in 2013. In the past 13 years (2001-2013), spending on telecom and IT in the Kingdom reached SR731.5bn, an average of SR56.3bn per year. (GulfBase.com) KSA oil exports hit SR657bn in 7 months – Saudi Arabia's oil exports reached 1.6bn barrels in the first seven months of 2014 with proceeds amounting to SR657bn. Meanwhile, domestic consumption during the same period is expected to stand at 475mn barrels or 23% of the total output. Global demand for oil is expected to be strong for the remaining period of 2014 due to geopolitical turmoil, notably in the Middle East, North Africa and Eurasia. (GulfBase.com) SABIC taps shale gas as alternative feedstock at UK site – Saudi Basic Industries Corporation (SABIC) is capitalizing on shale gas opportunities in the US by modifying its cracker at Teesside, UK, into a gas cracker. The cracker upgrade for using shale gas-based feedstock is scheduled to be completed during 2016, and is expected to result in long-term, reliable supply of cost-competitive products. The project reflects SABIC’s strong determination to take advantage of the cutting edge technology in creating new sources of competitive feedstock. (GulfBase.com) Abraaj Group, TPG Capital to acquire majority stake in Kudu – Abraaj Group and TPG Capital are about to finalize a deal to buy majority stake in the Saudi Arabian fast-food chain, Kudu. The transaction, which is expected to be signed by September, will value Kudu at around $400-500mn. Abraaj and TPG are in talks with various banks to borrow about $187mn to finance the Kudu acquisition. (Bloomberg) Jarir opens new showroom in Delma Mall – Jarir Bookstore announced the opening of its new showroom in Delma Mall in Abu Dhabi on August 14, 2014 as a replacement of its existing showroom which decided to be closed due to the declining sales. Jarir bookstore invested more than SR12mn in the new showroom which includes all Jarir items of office and school supplies, wide range of Arabic and English books, in addition to a huge number of arts and engineering materials. (Tadawul) Bahri announces transfer of Virgo Star to its fleet – The National Shipping Company of Saudi Arabia (Bahri) announced that Virgo Star, one of the VLCCs in Vela fleet, was transferred

- 5. Page 5 of 7 to Bahri's ownership on August 14, 2014 and its name was changed to ‘Ghinah’. The remaining Vela vessels shall be transferred to Bahri on a staggered basis as per the agreed vessel delivery schedule with Vela, which is expected to be completed before the end of 2014. (Tadawul) Multi-entry visa to boost cruise, medical tourism sector – Regulatory changes in the UAE’s visa system will have a transformative effect on Dubai’s cruise sector and further boost medical tourism in the Emirates. A new ruling signed by the UAE’s Vice-President HH Sheikh Mohammed Bin Rashid Al Maktoum took effect on August 1, 2014, which will ensure implementation of a new visa and fees system in the UAE. Amendments include a new multiple entry tourism permit for cruise passengers and a range of new entry permits for medical tourists and their companions. (GulfBase.com) Awards International begins operation in UAE – Awards International, an organization that develops and implements professional business awards programs, has been officially launched in Dubai. The company will be running its own awards programs, while offering services to develop and manage bespoke awards programs for clients. Awards International aims to develop several awards programs which appeal to companies from across the world. (GulfBase.com) Adnoc Distribution opens three temporary service stations – Adnoc Distribution (Abu Dhabi National Oil Company) announced the opening of three temporary service stations in the Western Region, covering the areas of Madinat Zayed, Zayed Industrial City and Baynounah in the Emirate of Abu Dhabi. This move is in line with Adnoc Distribution’s ongoing commitment for fulfilling its customer needs across the UAE. (GulfBase.com) DIFC Investments plans sukuk issue – DIFC Investments, the investment arm of the company running Dubai's financial free zone, is planning to issue Sukuk. The company has appointed banks and could come to market as early as September 2014. (GulfBase.com) DIA revamp to ease air traffic congestion – According to the head of the emirate’s civil aviation authority, the refurbishment of two runways at the Dubai International Airport (DIA) is expected to help the airport handle a third more aircraft per hour, easing air traffic congestion concerns. The Dubai Air Navigation Services (Dans) said that the Dubai air traffic has been consistently growing between 5 to 7% annually, higher than the global average of 3.5%, with Dubai International handling 34.67mn passengers in 1H2014, an increase of 6.2% YoY. (Gulf-Base.com) Arabtec’s former CEO nets nearly $50mn from share sales – Arabtec Holding’s former CEO Hasan Ismaik has earned $48mn from the sale of shares in the company over the past month. Hasan sold 41.8mn shares, at different prices, and at an uneven pace over the eight trading days since July 23. The shares sold equate to 0.9% of the company and 4.3% of Hasan’s stake. Ismaik sold tranches of shares worth between $850,000 and $13.6mn on July 24, July 27, July 31, August 3, August 4, and August 5. (GulfBase.com) DEWA releases tender for Solar Park Phase II – The Dubai Electricity & Water Authority (DEWA) has released a tender for the 100 MW-Phase II in the Mohammed bin Rashid Al Maktoum Solar Park to qualified Independent Power Producer (IPP) developers. The project supports the Green Economy for Sustainable Development and the Dubai Integrated Energy Strategy 2030 outlined by the Dubai Supreme Council of Energy to diversify the energy mix by 2030. (Bloomberg) Fitch Affirms Abu Dhabi at 'AA'; Outlook Stable – Fitch Ratings has affirmed Abu Dhabi's Long-term foreign and local currency Issuer Default Ratings (IDR) at 'AA'. The Outlooks are Stable. The issue ratings on Abu Dhabi's senior unsecured foreign and local currency bonds have also been affirmed at 'AA'. The Short-term foreign currency IDR has been affirmed at 'F1+'. The UAE Country Ceiling has been affirmed at 'AA+'; this Ceiling also applies to Ras al-Khaimah. (Reuters) ADIA reports 19.4% rise in 1H2014 air traffic – According to Abu Dhabi Airports (ADA), Abu Dhabi International Airport (ADIA) reported a 19.4% increase in passenger traffic during 1H2014, as compared to 1H2013. The statistics shows that a total of 9,481,744 passengers passed through the airport in 1H2014, as compared to 7,941,922 during 1H2013. Aircraft movements rose to 73,862, representing 11.8% growth compared with 65,072 aircraft movements reported in 1H2013. Cargo activity in 1H2014 comprised 377,885 tons handled at the three terminals, representing a 16% increase when compared to 1H2013. June alone saw 1,667,551 passengers pass through the airport, an increase of 21.4% compared with June 2013. (GulfBase.com) ADIB: Abu Dhabi’s real estate market witnesses rising investor confidence – According to MPM Properties, a real estate subsidiary of Abu Dhabi Islamic Bank (ADIB), the realty market in Abu Dhabi is stabilizing after six months of rising values, which has seen yields erode, lower loan to value ratios and limited availability of quality apartments. The reports covered Abu Dhabi’s residential, office, retail and hospitality sectors and featured the second ADIB Rental Index, which highlights the performance of its managed portfolio comprising of over 12,000 residential units spread across Abu Dhabi. For the residential sector overall, strong market confidence and investor interest has supported rising values in prime projects during the last quarter, which included a number of bulk deals and sales of land plots. (GulfBase.com) S&P affirms Kuwait credit rating at AA/A-1+ – Standard and Poor's (S&P) affirmed its "AA/A-1+" long- and short-term foreign and local currency sovereign credit ratings on Kuwait with "a stable outlook." According to S&P, Kuwait has a rich oil and gas endowment which enabled it to build strong external and fiscal balance sheet positions. The ratings, however, are constrained by the geopolitical tensions in the region, as well as Kuwait's unpredictable and undiversified economy. The stable outlook reflects expectations of continued strength in Kuwait's fiscal and external positions, backed by oil revenues. (GulfBase.com) NCSI: Oman posts budget surplus of OMR583mn – According to the National Centre for Statistics & Information (NCSI), Oman recorded a surplus of OMR582.9mn in the first five months of 2014, against a deficit of OMR110.4mn for the same period last year. The surge in budget surplus was mainly due to a marginal growth in government revenue, which edged up 0.5% YoY to OMR6.04mn in the period. Oman, which based its 2014 budget on a projected oil price of $85 per barrel, expects an expenditure of OMR13.5bn and a deficit of OMR1.8bn in 2014. Although net oil revenue in the first five months declined by 2.6% to OMR4,335.1mn, the overall revenue moved up by 0.5mn to OMR6,044.1mn. According to the monthly report, the average daily crude oil production for 1H2014 rose 1% to 943,700 barrels, against 934,200 barrels in 1H2013. Likewise, total oil production (including condensates) in 1H2014 also rose by 1% to 170.8mn barrels from 169.09mn barrels. Additionally, Oman’s total merchandise exports showed a 7.9% fall in 1H2014 at OMR5,143mn from OMR5,582.6mn in 1H2013, due to a dip in oil & gas exports, which fell by 9.3% to OMR3,372.3 million in 1Q2014. However, non-oil exports

- 6. Page 6 of 7 showed a 23.4% YoY growth at OMR1,010mn from OMR818.2mn. (GulfBase.com) Omantel BoD approves 40% dividend – Oman Telecommunications Company’s (Omantel) board of directors has approved to distribute an interim dividend of 40% to its registered shareholders by the end of trading hours of August 31, 2014. (MSM) BHB announces increase in GFH paid-up capital – The Bahrain Bourse (BHB) announced increase in the paid-up capital of Gulf Finance House (GFH) due to the issuance of 129,452,537 shares, pursuant to the approval from the EGM held on April 14, 2014, and this will be effective August 17, 2014. The previous total outstanding shares were 3,621,455,832 and the new outstanding shares are 3,750,182,467, whereas the previous total paid-up capital was $1.113bn and the new total paid-up capital is $1.153bn. (Bahrain Bourse) ABC completes $750mn syndicated term loan facility – Arab Banking Corporation (ABC) has completed a $750mn syndicated term loan facility. Syndication was launched with an initial amount of $500mn and was significantly oversubscribed, raising in excess of $800mn from 17 leading international and regional banks. The three-year facility will be used for general corporate funding purposes and carries a margin of 120 basis points over Libor. HSBC Bank Middle East, National Bank of Abu Dhabi, Natixis and Sumitomo Mitsui Banking Corporation acted as initial mandated lead arrangers and bookrunners. National Bank of Abu Dhabi is the Facility Agent and HSBC acted as the co-coordinating bank. (GulfBase.com) Arcapita Bank hires JPMorgan to float Irish energy firm Viridian – Bahrain-based Arcapita Bank has hired JPMorgan to lead a share listing for Irish energy firm Viridian Group. The transaction could give the firm a value, including debt of $1.7bn. (Bloomberg) Ithmaar Bank reports net profit of $1.77mn for 1H2014 – Ithmaar Bank reported a net profit of $1.77mn for 1H2014, as compared to the net loss of $7.52mn during 1H2013. Net loss for 2Q2014 amounted to $0.34mn, as compared to net loss of $8.95mn in 2Q2013. Operating income increased by 17.68% to $114.88mn from $97.61mn reported for 1H2013. Liquid assets represent 13.77% of the bank’s total assets as of June 30, 2014. (Bloomberg)

- 7. Contacts Saugata Sarkar Abdullah Amin, CFA Shahan Keushgerian Head of Research Senior Research Analyst Senior Research Analyst Tel: (+974) 4476 6534 Tel: (+974) 4476 6569 Tel: (+974) 4476 6509 saugata.sarkar@qnbfs.com.qa abdullah.amin@qnbfs.com.qa shahan.keushgerian@qnbfs.com.qa Sahbi Kasraoui Ahmed Al-Khoudary QNB Financial Services SPC Manager – HNWI Head of Sales Trading – Institutional Contact Center: (+974) 4476 6666 Tel: (+974) 4476 6544 Tel: (+974) 4476 6548 PO Box 24025 sahbi.alkasraoui@qnbfs.com.qa ahmed.alkhoudary@qnbfs.com.qa Doha, Qatar DISCLAIMER: This publication has been prepared by QNB Financial Services SPC (“QNBFS”) a wholly-owned subsidiary of Qatar National Bank (“QNB”). QNBFS is regulated by the Qatar Financial Markets Authority and the Qatar Exchange; QNB is regulated by the Qatar Central Bank. This publication expresses the views and opinions of QNBFS at a given time only. It is not an offer, promotion or recommendation to buy or sell securities or other investments, nor is it intended to constitute legal, tax, accounting, or financial advice. We therefore strongly advise potential investors to seek independent professional advice before making any investment decision. Although the information in this report has been obtained from sources that QNBFS believes to be reliable, we have not independently verified such information and it may not be accurate or complete. While this publication has been prepared with the utmost degree of care by our analysts, QNBFS does not make any representations or warranties as to the accuracy and completeness of the information it may contain, and declines any liability in that respect. QNBFS reserves the right to amend the views and opinions expressed in this publication at any time. It may also express viewpoints or make investment decisions that differ significantly from, or even contradict, the views and opinions included in this report. COPYRIGHT: No part of this document may be reproduced without the explicit written permission of QNBFS. Page 7 of 7 Rebased Performance Daily Index Performance Source: Bloomberg Source: Bloomberg Source: Bloomberg Source: Bloomberg 80.0 90.0 100.0 110.0 120.0 130.0 140.0 150.0 160.0 170.0 180.0 190.0 200.0 210.0 Jul-10 Jul-11 Jul-12 Jul-13 Jul-14 QE Index S&P Pan Arab S&P GCC (0.0%) (0.1%) (0.2%) 0.5% 0.3% 1.0% 0.2% (0.4%) 0.0% 0.4% 0.8% 1.2% SaudiArabia Qatar Kuwait Bahrain Oman AbuDhabi Dubai Asset/Currency Performance Close ($) 1D% WTD% YTD% Global Indices Performance Close 1D% WTD% YTD% Gold/Ounce 1,304.83 (0.7) (0.5) 8.2 DJ Industrial 16,662.91 (0.3) 0.7 0.5 Silver/Ounce 19.56 (1.6) (1.7) 0.5 S&P 500 1,955.06 (0.0) 1.2 5.8 Crude Oil (Brent)/Barrel (FM Future) 103.53 1.5 (1.4) (6.6) NASDAQ 100 4,464.93 0.3 2.2 6.9 Natural Gas (Henry Hub)/MMBtu 3.77 (1.6) (3.8) (13.3) STOXX 600 329.72 (0.4) 1.5 0.4 LPG Propane (Arab Gulf)/Ton 102.75 1.7 0.2 (18.6) DAX 9,092.60 (1.4) 0.9 (4.8) LPG Butane (Arab Gulf)/Ton 120.13 0.5 1.3 (12.0) FTSE 100 6,689.08 0.1 1.9 (0.9) Euro 1.34 0.3 (0.1) (2.5) CAC 40 4,174.36 (0.7) 0.6 (2.8) Yen 102.36 (0.1) 0.3 (2.8) Nikkei 15,318.34 0.0 3.7 (6.0) GBP 1.67 0.0 (0.5) 0.8 MSCI EM 1,074.51 0.2 2.8 7.2 CHF 1.11 0.4 0.3 (1.1) SHANGHAI SE Composite 2,226.73 0.9 1.5 5.2 AUD 0.93 0.0 0.5 4.5 HANG SENG 24,954.94 0.6 2.6 7.1 USD Index 81.42 (0.2) 0.0 1.7 BSE SENSEX 26,103.23 0.0 3.1 23.3 RUB 36.19 0.7 0.0 10.1 Bovespa 56,963.65 2.1 2.5 10.6 BRL 0.44 0.3 1.0 4.5 RTS 1,232.34 0.0 5.3 (14.6) 194.1 162.6 146.5