Leerink Swann Research Report on Ventrus Bio ($VTUS)

•

1 gostou•1,794 visualizações

Ventrus Biosciences (NASDAQ: VTUS; Stock Twits; $VTUS) is a development stage specialty pharmaceutical company focused on the development of late-stage prescription drugs for gastrointestinal disorders, specifically hemorrhoids, anal fissures and fecal incontinence.

Recomendados

Recomendados

Mais conteúdo relacionado

Destaque

Destaque (20)

Semelhante a Leerink Swann Research Report on Ventrus Bio ($VTUS)

Semelhante a Leerink Swann Research Report on Ventrus Bio ($VTUS) (20)

Mais de ProActive Capital Resources Group

Mais de ProActive Capital Resources Group (20)

Último

Último (20)

Leerink Swann Research Report on Ventrus Bio ($VTUS)

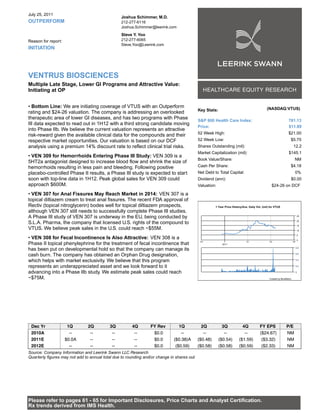

- 1. July 25, 2011 Joshua Schimmer, M.D. OUTPERFORM 212-277-6116 Joshua.Schimmer@leerink.com Steve Y. Yoo Reason for report: 212-277-6065 Steve.Yoo@Leerink.com INITIATION VENTRUS BIOSCIENCES Multiple Late Stage, Lower GI Programs and Attractive Value: Initiating at OP • Bottom Line: We are initiating coverage of VTUS with an Outperform (NASDAQ:VTUS) Key Stats: rating and $24-26 valuation. The company is addressing an overlooked therapeutic area of lower GI diseases, and has two programs with Phase S&P 600 Health Care Index: 781.13 III data expected to read out in 1H12 with a third strong candidate moving Price: $11.89 into Phase IIb. We believe the current valuation represents an attractive 52 Week High: $21.00 risk-reward given the available clinical data for the compounds and their respective market opportunities. Our valuation is based on our DCF 52 Week Low: $5.75 analysis using a premium 14% discount rate to reflect clinical trial risks. Shares Outstanding (mil): 12.2 Market Capitalization (mil): $145.1 • VEN 309 for Hemorrhoids Entering Phase III Study: VEN 309 is a Book Value/Share: NM 5HT2a antagonist designed to increase blood flow and shrink the size of hemorrhoids resulting in less pain and bleeding. Following positive Cash Per Share: $4.18 placebo-controlled Phase II results, a Phase III study is expected to start Net Debt to Total Capital: 0% soon with top-line data in 1H12. Peak global sales for VEN 309 could Dividend (ann): $0.00 approach $600M. Valuation: $24-26 on DCF • VEN 307 for Anal Fissures May Reach Market in 2014: VEN 307 is a topical diltiazem cream to treat anal fissures. The recent FDA approval of Rectiv (topical nitroglycerin) bodes well for topical diltiazem prospects, 1 Year Price History/Ave. Daily Vol. (mil) for VTUS although VEN 307 still needs to successfully complete Phase III studies. A Phase III study of VEN 307 is underway in the EU, being conducted by 25 S.L.A. Pharma, the company that licensed U.S. rights of the compound to 20 15 VTUS. We believe peak sales in the U.S. could reach ~$55M. 10 5 • VEN 308 for Fecal Incontinence Is Also Attractive: VEN 308 is a 0 Phase II topical phenylephrine for the treatment of fecal incontinence that Q3 Q1 Q2 Q3 2011 has been put on developmental hold so that the company can manage its 0.8 cash burn. The company has obtained an Orphan Drug designation, 0.6 which helps with market exclusivity. We believe that this program 0.4 represents an underappreciated asset and we look forward to it 0.2 advancing into a Phase IIb study. We estimate peak sales could reach 0 ~$75M. Created by BlueMatrix Dec Yr 1Q 2Q 3Q 4Q FY Rev 1Q 2Q 3Q 4Q FY EPS P/E 2010A -- -- -- -- $0.0 -- -- -- -- ($24.67) NM 2011E $0.0A -- -- -- $0.0 ($0.38)A ($0.48) ($0.54) ($1.59) ($3.32) NM 2012E -- -- -- -- $0.0 ($0.59) ($0.58) ($0.58) ($0.59) ($2.33) NM Source: Company Information and Leerink Swann LLC Research Quarterly figures may not add to annual total due to rounding and/or change in shares out. Please refer to pages 61 - 65 for Important Disclosures, Price Charts and Analyst Certification. Rx trends derived from IMS Health.

- 2. VENTRUS BIOSCIENCES July 25, 2011 Ventrus Biosciences (VTUS): Multiple Late Stage GI Assets and Attractive Valuation Joshua Schimmer, M.D., Biotechnology Analyst 212-277-6116; Joshua.Schimmer@Leerink.com Steve Yoo, Biotechnology VP 212-277-6065; Steve.Yoo@Leerink.com 2

- 3. VENTRUS BIOSCIENCES July 25, 2011 Investment Thesis • We are initiating coverage of VTUS with an Outperform rating and $24- $26/share valuation • The company has 2 Phase III compounds and a Phase II compound all focused on distal GI tract disorders, each addressing a meaningful unmet need • Lean operations that could translate to good operating leverage • Attractive valuation: ~$150M market cap, with ~$4/share in cash and ~$100M enterprise value are quite modest, in our view, given multiple shots on goal • We believe the VEN 307 (anal fissures) and VEN 308 (fecal incontinence) programs alone support upside to the current valuation, yielding attractive risk-reward on the lead VEN 309 (hemorrhoids) program 3

- 4. VENTRUS BIOSCIENCES July 25, 2011 3 Attractive GI Programs • Phase III- VEN 309 (topical 5HT2a antagonist) for hemorrhoids • Placebo-controlled Phase II study demonstrated reductions in both pain and bleeding • No drug therapy currently approved for hemorrhoids; unmet need for a medical therapy to follow standard OTC regimens and before intervention with banding or hemorrhoidectomy • We model peak global sales approaching $600M, peak U.S. sales approaching $400M • Phase III- VEN 307 (topical diltiazem) for anal fissures • Painful condition, inadequate treatments; surgical correction an option but risks fecal incontinence • Small studies suggest VEN 307 is as efficacious as recently approved Rectiv, but without side effect of headaches. MEDACorp specialists note positive anecdotal experience with topical diltiazem • We model peak U.S. sales >$50M, could be higher if additional patent protection procured • Phase II- VEN 308 (topical phenylephrine) for fecal incontinence • Very high unmet medical need with inadequate treatment options • Development on hold due to finite resources, but should move into Phase IIb studies in 2H12; we are very eager to see this program advance • We model peak U.S. sales of ~$75M 4

- 5. VENTRUS BIOSCIENCES July 25, 2011 Key VTUS Risks • Clinical data risk: • VEN 309 (hemorrhoids): We estimate 65% probability of success in Phase III. VEN 309 must also successfully complete tQTc study (see later in report) • VEN 307 (anal fissures): Topical diltiazem is used in the GI community, but the clinical evidence for activity is mixed. We estimate 50% probability of success in Phase III • VEN 308 (fecal incontinence): Topical phenylephrine has shown mixed results in small clinical trials. Selecting the ideal patient population to show benefit may be key to clinical success. We estimate 55% probability of success in Phase III • IP risk: • VEN 309 (hemorrhoids) composition of matter expires 2015; new method of use IP to 2030 should issue • VEN 307 (anal fissures) method of use IP to 2018, but additional formulation work may generate new IP • VEN 308 (fecal incontinence) method of use IP to 2017 but also has Orphan Drug Designation • As topical drugs, Citizen’s Petitions could be used to buy additional time before entry of generic challenges • Commercial risk: • All 3 indications may best be served with a primary care sales force, although a targeted commercial effort toward GI specialists and colorectal surgeons could claim decent market share 5

- 6. VENTRUS BIOSCIENCES July 25, 2011 VEN 309 for Hemorrhoids 6

- 7. VENTRUS BIOSCIENCES July 25, 2011 Hemorrhoids • Inflammation and swelling of veins around the anus or lower rectum • Can cause bleeding, itching, pain and difficulty defecating • Estimated prevalence in U.S. is ~12.5M; 1M new cases/year • About 3.5M seek medical treatment • Present in 4% of U.S. population and 50% of over-50 population 7

- 8. VENTRUS BIOSCIENCES July 25, 2011 Hemorrhoids – Classification Stage 0 Stage 1 Stage 2 Stage 3 Stage 4 Morphology Anal cushion Small hemorrhoids Intermediate hemorrhoids Large hemorrhoids Very large hemorrhoids Symptoms Very rare bleeding, no Intermittent bleeding, no Prolapse during straining Prolapse, need manual Permanent prolapse, prolapse prolapse but spontaneously return; aid to put back in anal bleed profusely, blood frequent bleeding, canal, bleed frequently & stains on underwear even sometimes profusely often profusely. without bowel movement Additional features None None, with exception of Anal itching (pruritus ani), Anal itching (pruritus ani), Severe pain, anal itching, some pain and sometimes skin tags discomfort, skin tags severe discomfort, soilings, skin tags Visual No increase Minor, but definite Moderate increase of Major increase in size, Extreme increase in size, increase as can be individual masses that prolapse visible skin tags, observed by proctoscopy prolapse during straining secondary hemorrhoids may develop Age group All ages, <20 if 20 - 45 >30 > 40 > 50 symptomatic Treatment Change in bowel habit & Sclerotherapy & Infrared Rubber band ligation & Hemorrhoidectomy Hemorrhoidectomy, diet, sclerotherapy / coagulation. Rubber band stapling. Surgery in some sometimes with anoplasty infrared coagulation for ligation & surgery for cases. stubborn cases certain cases. Source: http://www.hemorrhoidsinplainenglish.com/hemorrhoid/classification.htm Majority of patients fall into Stages I-III, which is the population that VEN 309 would address 8

- 9. VENTRUS BIOSCIENCES July 25, 2011 Characteristics of the Hemorrhoid Market • Patients reticent to broach topic with doctors • May be due to lack of approved products or embarrassment of topic • Patients more likely to approach doctors for bleeding or pain • Bleeding and pain are the major source of discomfort (or anxiety) for patients • Primary care doctors may refer patients to GI specialists to screen for colorectal cancer (more so than for therapeutic intervention) • Increases the likelihood of GI specialists seeing these patients, which is important if considering a targeted commercial effort 9

- 10. VENTRUS BIOSCIENCES July 25, 2011 Hemorrhoids – Current Treatment Options • High fiber/high fluids diet or stool softener to lessen straining during defecation • Preparation H – generally regarded as ineffective. Primary agent is shark liver oil • Sitz baths (shallow tub of warm water) for 10-15min mitigates symptoms • OTC corticosteroid/lidocaine creams reduce pain and swelling • Anusol (hydrocortisone cream) – Used off label. Approved for relief of dermatoses • Roughly 4M scripts/year for anorectal steroids, of which >3M are likely for hemorrhoids • Translates to over $1B potential market for hemorrhoids using VEN 309 price assumption • Rubber band ligation – 60-80% success rate. New CHR Medical Products banding procedure offers even higher success rates with reduced discomfort versus traditional banding with forceps • >50M hemorrhoid banding procedures globally each year, according to CRH Medical Products (makers of a new banding device) • Infrared coagulation – about 70% success rate but effects may not last • Hemorrhoidectomy – saved for stage III, IV patients. Long-term symptom resolution of 95%. Recovery time could be a week. Reserved for most severe/refractory cases 10

- 11. VENTRUS BIOSCIENCES July 25, 2011 VEN 309 – Iferanserin Ointment for Hemorrhoids • Serotonin 5-HT2A receptor antagonist S-isomer acts as vasodilator and antiplatelet agent, helping to increase blood flow out of dilated rectal venous plexus veins that are characteristic of hemorrhoidal tissue • Administered as ointment for topical administration • Limits systemic exposure and therefore AE risk profile • Composition of matter patent expires in August 2015 but patent applications for method of dosing (through 2030) under review • SPA pursued for Phase III trial but will advance without formalizing agreement after sufficient progress made • We do not view this as a concern or regulatory risk 11

- 12. VENTRUS BIOSCIENCES July 25, 2011 Development History of VEN 309 • Proof of concept established by Sam Amer, former director of R&D at BMY • Patent filed for method of use in 1992 • Product licensed to Tsumura in 1998 but returned to Amer when Tsumura ran into financial difficulties • Product licensed to NVS in 2003 but returned to Amer in 2005 when NVS shifted focus away from GI drugs • Product licensed to VTUS in 2008 after end of Phase II meeting with FDA • VTUS concluded $12.5M deal in June 2011 to reduce payments to Amer by about 66% • Amer now will receive 3-4% royalty on US sales, 1-1.3% royalty on OUS sales 12

- 13. VENTRUS BIOSCIENCES July 25, 2011 VEN 309 – Preclinical Safety • The dosing range that produces preclinical toxicity is 17-88x the Phase III dose of 0.5% applied topically 2x daily • The range that produces QTc prolongation effects in animals is 45-85x the Phase III dose of 0.5% applied topically 2x daily • The range that produces QTc prolongation effects in vitro is 60-100x the Phase III dose of 0.5% applied topically 2x daily • Therefore, despite Herg channel inhibition seen in vitro, topical administration is unlikely to result in serum concentrations high enough for this to be a concern 13

- 14. VENTRUS BIOSCIENCES July 25, 2011 VEN 309 QTc Prolongation Risk Appears Small • A thorough QTc prolongation study (TQT) for VEN 309 will be run in parallel with the Phase III study • VEN309 is metabolized by CYP2D6; some patients can have inactive CYP2D6 enzymes and therefore risk relative accumulation of VEN 309 in serum • 1 patient in an earlier trial had lower expression of CYP2D6, which resulted in Cmax blood levels of VEN 309 3x higher compared to other patients • No other adverse events noted for the patient • In preclinical hERG channel studies, doses representing 60-100x the human dose resulted in potential QTc elongation • In Phase III trial, may limit use of drugs that are metabolized through CYP2D6, but risk will be fully characterized in the tQTc study 14

- 15. VENTRUS BIOSCIENCES July 25, 2011 Early VEN 309 Trials • 7 clinical trials completed to date (1993-2003) by Tsumura and Amer • 220 patients dose; No SAE noted so far • Clinical results have not been formally published, which clouds visibility on Phase III studies and leads to our ~65% estimated probability of success • Because some trials were done in Japanese patients, can be used for Japanese approval 15

- 16. VENTRUS BIOSCIENCES July 25, 2011 VEN 309 Trial Summary Phase I Phase I Phase I proof of Phase II dose- Phase IIb Phase Iib concept ranging (German study) Date 1998 1999 1992 N/A 2002 2004 Patients 18 6 26 72 104 121 Duration (days) 1 6 5 14 28 14 Geography Japan Japan US Japan Japan EU Sponsor Tsumura Tsumura Amer Tsumura Tsumura Amer Dose strength 1% racemic 1% racemic 1% racemic 0.25%, 0.5%, 1.0% 0.25%, 0.5%, 1.0% 0.5% Frequency single dose bid tid bid bid bid Efficacy Significant improvement Significant 0.5% and 1.0% dose Significant in defecation, throbbing, improvement in ease showed most improvement in fullness, bleeding, of defecation at day 7 consistent bleeding, pain, tenderness improvements in itching and symptoms proposed Phase III endpoint Safety 3 mild AE where drug 4 mild AE where drug couldn't be N/A 5 VEN 309 related N/A Similar to previous couldn't be ruled out ruled out events trials 1 patient with low CYP2D6 activity mild diarrhea lower abdominal discomfort mild elevation of of total bilirubin Note half life is 1.6 hours no accumulation with bid dosing Rapid onset of benefit The 0.5% dose Rapid onset of unexpectedly signficant symptom provided the best relief (1-3 days) results Source: VTUS S-1, Leerink Swann analysis 16

- 17. VENTRUS BIOSCIENCES July 25, 2011 Phase IIb German Trial • Phase IIb German trial is largest trial to date -- 110 evaluable patients. Twice-daily 0.5% VEN 309 versus placebo for 14 days Source: Ventrus S1 Daily Bleeding Daily Pain Statistically significant improvement in the 2 key complaints for hemorrhoid patients. Rapid separation between drug and placebo 17

- 18. VENTRUS BIOSCIENCES July 25, 2011 Phase IIb German Trial – cont’d Itching Bleeding response Proposed endpoint for Phase III trial – No bleeding between days 7-14 Source: Ventrus S1 FDA has agreed in principle to the proposed endpoint. Patients in the German trial showed statistically significant efficacy signal 18

- 19. VENTRUS BIOSCIENCES July 25, 2011 Development Plan for VEN 309 • FDA agreed on primary endpoint during SPA discussions • Company will proceed with Phase III before finalizing SPA on basis of fundamental agreement with FDA on appropriate trial design. We do not view this as a concern. • Phase III trial design • 600 patients in 3 arms: b.i.d. VEN 309 for 2 weeks, b.i.d. VEN 309 for 1 week followed by 1 week of placebo, placebo for 2 weeks. Randomized 1:1:1 • Include grades I-III hemorrhoids. Need to bleed from hemorrhoids and have pain/itching for 2 consecutive days prior to randomization • Primary endpoint: No bleeding days during 2nd week of treatment • After randomized phase, patients eligible for active treatment for up to 12 months in case of recurrence • Second Phase III trial will be designed based on results of the first study • 2 year, 2 species carcinogenicity study required – rate limiting step • 1,500-patient safety database required 19

- 20. VENTRUS BIOSCIENCES July 25, 2011 Other Commercial Avenues To Explore • Chronic versus acute population • Generally, patients who have hemorrhoids are likely to have recurrence of symptoms • Phase III study will have 12-month open-label extension that will generate useful real-world treatment data. FDA asked for this data because it believed the drug could potentially be used as a chronic therapy • If there is a sizable recurrent hemorrhoids population, the 2nd Phase III trial may include a repeat dosing arm for chronic patients, especially if they respond to VEN 309 therapy better than the acute hemorrhoids patients • VTUS may conduct a separate chronic use study if incorporating into the 2nd Phase III study becomes too cumbersome or significantly delays the completion of the trial • Because VEN 309 is likely to be used intermittently, even if use is frequent, a single arm long-term extension study has the benefit of numerous “off” periods of drug that can be used to scrutinize any spurious safety signals that may emerge 20

- 21. VENTRUS BIOSCIENCES July 25, 2011 MEDACorp Specialist Comments – VEN 309 • Preparation H not effective, majority of patients have tried it before coming to see doctor • About 75% of current patients can be treated with non-surgical treatment (high fiber diet, stool softeners) with symptom alleviation within couple weeks • Stage IV patients are rare (around 10% of patients or less). These patients are directly referred over to colorectal surgeons for repair • Banding is effective and safe but would prefer to use topical therapy prior to banding • Important role seen for VEN 309 in management of hemorrhoids if Phase III results are positive 21

- 22. VENTRUS BIOSCIENCES July 25, 2011 VEN 309 Market Assumptions • U.S. hemorrhoid population – 12M, growing 1.5% y/y • Estimate 33% of patients seek treatment • May increase if patients find out about effective FDA-approved therapy • Market penetration for VEN 309 – gradually rises to 16% of patients seeking treatment • Revenue per patient – $425, growing at 2% y/y • VTUS plans to focus commercialization efforts on the 4M anorectal steroid prescriptions per year • Can promote with modest-sized sales force and supplement with commercial agreement with a pharma company targeting the broad PCP market, although our model only assumes ex-U.S. agreement 22

- 23. VENTRUS BIOSCIENCES July 25, 2011 CRH Medical (CRM:TSX-V) Banding Procedure Highlights Commercial Opportunity • An improved hemorrhoid banding device using syringe for suction instead of using forceps to grab hemorrhoidal tissue. Lowers the pain complication rate • Unique sales approach of using KOL/physician trainers and no salesforce to promote the technique • Estimated 10% share of the banding procedures done in U.S., annualizing at $5M revenue; $65/procedure implies $50M banding market or greater if this device can expand the market • We believe this technology could overtake the banding market in the future. However, doctors indicate they will be willing to try topical therapy before opting for rubber band ligation Source: CRH Building up from banding procedure market (and adjusting for price) also suggests peak U.S. sales of $400M for VEN 309 is achievable 23

- 24. VENTRUS BIOSCIENCES July 25, 2011 VEN 309 Revenue Projections VEN 309 Sales 400 350 300 109 250 79 OUS 200 51 US 150 25 251 100 202 0 156 50 113 0 73 35 0 0 2014 2015 2016 2017 2018 2019 2020 Source: Leerink Swann estimates We expect that extended patent protection with method of dosing will be achieved (note recent experience with ACOR’s Ampyra helps support ability to delineate novel dosing IP) 24

- 25. VENTRUS BIOSCIENCES July 25, 2011 Timeline for VEN 309 • Summer 2011 – Start Phase III trial, start LT carcinogenicity study • 1H12 – Phase III results • 2012 – Start second Phase III trial in recurrent hemorrhoids patients • Mid-2014 – NDA expected to be filed after second Phase III trial results • 2015 – Launch • August 2015 – Composition of matter patent expiration • 2030 – Potential patent protection if concentration range patent granted 25

- 26. VENTRUS BIOSCIENCES July 25, 2011 VEN 307 for Anal Fissures 26

- 27. VENTRUS BIOSCIENCES July 25, 2011 Anal Fissures • Small tears or cuts in the distal anal canal anoderm • Results in severe anal pain and bleeding with or after bowel movements • Thought to be caused by increased internal anal sphincter (IAS) tone and poor flood flow to anal epithelium • Estimated 4.3M cases in the U.S. with 1.1M office visits in the U.S. • Verispan Physician Drug and Diagnosis Audit at Cellegy FDA Advisory meeting in April 2006 estimated 84K compounded nitroglycerin ointment uses from Oct. 2003 to Sept. 2004 • Conservative therapy consists of diet modification, fiber, sitz baths and stool softeners, which are often ineffective • Most fissures heal over several weeks, but discomfort over this time can be substantial • More aggressive therapies include topical calcium channel blockers or nitrates • Surgery can be performed for severe or refractory cases • Healing is a difficult endpoint for registration studies 27

- 28. VENTRUS BIOSCIENCES July 25, 2011 Current Anal Fissure Treatments • Compounded nitroglycerin or compounded diltiazem • Pro – Widely used so doctors are familiar • Con – Need to be made by a compounding pharmacy so potential variability in strength and geographic availability • Rectiv - Nitroglycerin 0.4% ointment – first approved therapy for this indication • Prostrakan (subsidiary of Kyowa Hakko Kirin) acquired from Cellegy after prolonged registration course • Finally approved in June 2011, 1Q12 launch expected • Pro – FDA approved product. Doctors familiar with use. Easy to use for patients • Con – May cause headaches, dizziness. Efficacy modest at best • Botox injection into anal sphincter • Pro – Effect lasts for 3-8 months • Con – Invasive, usually not reimbursed • Surgery – most often lateral sphincterectomy, which relaxes the muscle • Pro – highly effective in alleviating pain • Con – Invasive. Can result in fecal incontinence in up to 10%, although fewer have QOL impacted by this complication 28

- 29. VENTRUS BIOSCIENCES July 25, 2011 VEN 307 – Diltiazem Cream for Anal Fissures • Reduces maximal resting pressure (MRP) of anal sphincter, to improve blood supply and reduce pain • Daily doses for fissures range from 15-45mg • Vs. cardiovascular applications, which require doses up to 240-360mg/d • Currently diltiazem cream is available through compounding pharmacies • Diltiazem cream is listed as a preferred agent prior to surgery in anal fissure treatment guidelines • Nifedipine topical products also available for treatment of fissure • MEDACorp specialists note preference to prescribe approved product given variability of compounding formulations and erratic availability of cream from compounding pharmacies 29

- 30. VENTRUS BIOSCIENCES July 25, 2011 Development Status of VEN 307 • Diltiazem use for anal fissures identified in 1997 at St. Mark hospital in London (Kamm, Phillips) with IP filed then • Method of use patent protection until 2018 • Patents assigned to S.L.A. Pharma in 1997 • Patents licensed to Solvay in 2001, which improved the manufacturing and formulation process and conducted PK studies • License returned to S.L.A. in 2004 after Solvay exited GI and women’s health development • North American rights licensed by VTUS in Aug. 2007 (via Paramount Biosciences) • Phase III EU trial started by S.L.A. in Nov. 2010 • 2Q12 finish expected • 505b2 pathway being pursued in U.S. • NDA filing could happen in 2013 • VTUS plans for internal GI specialty salesforce to commercialize the product 30

- 31. VENTRUS BIOSCIENCES July 25, 2011 VEN 307 Results From S.L.A. Pharma Mixed, But Small Studies and Did Not Use Optimal Endpoints • S.L.A. Pharma 4-day PK study in anal fissure patients • 8 doses of 2%, 4%, 8% cream single dose on d1 then t.i.d. doses on d2, 3, then single dose on d4 • Side effects (anal irritation, headache, nausea) were mild • 4-8 mmHg SBP (blood pressure) decline by day 4; transient, asymptomatic and returned to normal by next reading with no clear dose related effects; comparable with blood pressure declines reported in placebo subjects of HTN trials • S.L.A. Pharma clinical study in anal fissure patients • 2% diltiazem cream versus 0.2% glyceryltrinitrate (GTN) cream; b.i.d. application in and around anus x 6 weeks • 60 patients: 26% healed and 52% improved with diltiazem, versus 41% healed and 45% improved with GTN group; no recurrences after 4 weeks post therapy. • 42% treatment-related AE with diltiazem, 72% with GTN; headaches in 26% of diltiazem, 59% in GTN • S.L.A. Pharma healing endpoint exploratory trial • 2% diltiazem cream vs. placebo; 31 patients randomized. Creams applied b.i.d. x 8 weeks • Healing rates were 10% diltiazem, 19% placebo; no difference in pain at end of study or daily pain • Highlights challenges of using a healing study over 8 weeks 31

- 32. VENTRUS BIOSCIENCES July 25, 2011 Previous VEN 307 Clinical Trial Results Publication Patients Indication Drug Design Duration Results Side effects Kocher, Br J Surg Chronic anal Diltiazem 2% cream vs GTN 26% healed, 51% improved with diltiazem, 41% healed, 59% headache with GTN 2002 61 fissures 0.2% bid to anal verge Double blind 6 weeks 45% improved with GTN vs 26% with diltiazem Mean anal resting pressure reduction of 23% with topical, 15% with oral. Complete fissure healing in 65% topical None with topical; oral Jonas, Dis Col Chronic anal Open label, versus 38% oral, p=0.09. Among prior GTN failures, had headaches, GI side Rec 2001 50 fissures Diltiazem, oral or 2% gel bid randomized 8 weeks healing in 78% of topical versus 11% of oral. effects Bielecki, Colorectal Dis Chronic anal Diltiazem 2% ointment vs Open label, Headaches with GTN 2003 43 fissures GTN 0.5% ointment bid randomized 8 weeks Healing in 85.7% of GTN patients versus 90% of diltiazem (33%) Diltiazem 2% ointment Complete healing in 80% of diltiazem, 73% of GTN and Shrivastava, Surg Chronic anal versus GTN 0.2% ointment Open label, 33% of control. Mean decrease in pain of 75% with 67% headaches with Today 2007 90 fissures vs control randomized 6 weeks diltiazem, 59% with GTN and 29% with control GTN Carapeti, Dis Col Chronic anal Diltiazem 2% gel tid versus Open label, Rect 2000 15 fissures 0.1T bethanechol gel tid randomized 8 weeks 67% healed with diltiazem gel, 60% with bethanechol. Well tolerated Complete pain relief in 88%; complete rectal bleeding Chronic anal cessation in 92%; fissure healed in 56%. Mean resting Bhardwaj, 2000 44 fissures Diltiazem 2% gel tid Single arm 8 weeks anal sphincter pressure fell 24% Well tolerated Knight, Br J Surg Chronic anal 73% healed; 47% healed after additional course of 2001 71 fissures Diltiazem 2% gel bid Single arm 8 weeks therapy 6% with perianal itching DasGupta, Col Chronic anal Dis 2002 23 fissures Diltiazem gel tid Single arm 8 weeks 48% healed, including 6/8 who previously failed GTN Well tolerated Nash, Int J Clin Chronic anal 68% considered initial treatment a success in resolving Pract 2006 112 fissures Diltiazem 2% cream bid Single arm 6 weeks pain and bleeding. 77% of prior GTN failures had success Well tolerated Chronic anal Griffin, Col Dis fissures, failed Diltiazem 2% cream to anal 25% had perianal itching 2002 47 GTN verge bid Single arm 8 weeks 48% healed; 42% of the remainder were improved with prolonged use Chronic anal 10% with side effects, fissures, failed Diltiazem 2% ointment bid including mild perianal Jonas 39 GTN to distal anal canal Single arm 8 weeks 58% healed itching Source: VTUS S-1 Despite mixed clinical results, MEDACorp specialists believe that topical diltiazem does benefit patients with anal fissures 32

- 33. VENTRUS BIOSCIENCES July 25, 2011 VEN 307 Ongoing Phase III EU Study • Being conducted in Europe by S.L.A. Pharma • 465 patients, 30 sites • Started Nov. 2010 • 2-month treatment, 1:1:1 double blind study versus fiber + 2% VEN 207 versus fiber + 4% VEN 207 versus placebo • Primary endpoint is pain reduction upon defecation at 1 month • Daily diaries • VTUS has an opportunity to learn from this study before launching its own U.S. Phase III study in 2012 33

- 34. VENTRUS BIOSCIENCES July 25, 2011 VEN 307 Development • VTUS will conduct 3 short-term dermal tox studies and file IND • VTUS then plans to conduct its own U.S. Phase III study shortly after the end of the S.L.A. Phase III study results in 2Q12 • May compare to Rectiv in the Phase III study or in a separate Phase IV study • Likely to show similar efficacy to Rectiv but much better tolerability and lower discontinuation • NDA filing expected 2013 34

- 35. VENTRUS BIOSCIENCES July 25, 2011 Rectiv Sets Approval Precedent for Anal Fissures • 0.4% nitroglycerin ointment, b.i.d. application • Originally developed by Cellegy, filed with FDA in 2004 on basis of 3 Phase III studies (3rd was under SPA) and approved in June 2011 • Not approvable letter issued Dec. 2004 • Approvable letter issued Jan. 2006 • April 2006 FDA Advisory Panel split 6:6 on approvability • Approved June 22, 2011 • Expected launch 1H12; price has not yet been announced • Registration-enabling Phase III study was 3-week, placebo-controlled for patients with moderate or severe pain • Primary endpoint: Rate of change in the 24-hour pain intensity during the first 21 days of treatment 35

- 36. VENTRUS BIOSCIENCES July 25, 2011 Rectiv Clinical Trial Results Source: FDA briefing documents, 4/26/06 Primary endpoint analysis. Note that the data for studies 1, 2 were retrospective analysis 36

- 37. VENTRUS BIOSCIENCES July 25, 2011 Rectiv Discontinuation Due to Adverse Events 23 patients out of 304 withdrew due to adverse event. Most common adverse event cited was headaches (10 patients), which is to be expected with nitroglycerin therapy 37 Source: FDA briefing document, 4/26/06

- 38. VENTRUS BIOSCIENCES July 25, 2011 Rectiv Difficulty With FDA Different p-values depending on analytical method used Source: FDA briefing document, 4/26/06 Data analysis disagreement stemmed from how to address patients who dropped out due to adverse events, primarily headaches. Shouldn’t be a problem with VEN 309 38

- 39. VENTRUS BIOSCIENCES July 25, 2011 MEDACorp Specialist Comments – VEN 307 • Will try Rectiv in patients that would normally consider for nitroglycerin therapy • Topical diltiazem more appealing since it doesn’t cause headaches • Would prefer that any new therapy includes lidocaine to help with pain management • Could be a franchise-extension strategy for VEN 307 • FDA-approved product would make prescribing diltiazem much easier • Compounding pharmacies are slowly disappearing as big pharmacy chains consolidate the industry 39

- 40. VENTRUS BIOSCIENCES July 25, 2011 VEN 307 Market Assumptions • U.S. anal fissure population – 750k, growing 1.5% y/y • Estimate 50% of patients seek treatment • Market penetration for VEN 307 – rising to 18% in 2020, assuming Citizen’s Petition challenge buys a couple of extra years beyond patent expiry • Will compete against Rectiv, compounded nitroglycerin and compounded diltiazem • Revenue per patient - $650 per year, growing at 2% y/y 40

- 41. VENTRUS BIOSCIENCES July 25, 2011 VEN 307 Revenue Projections VEN 307 Sales 60 50 40 30 VEN 307 55 44 20 37 27 10 18 10 5 0 2014 2015 2016 2017 2018 2019 2020 Source: Leerink Swann estimates U.S. sales only, as S.L.A. has ex-U.S. rights. Could get patent protection extended into early 2030’s if new formulation patents issued 41

- 42. VENTRUS BIOSCIENCES July 25, 2011 VEN 308 for Fecal Incontinence 42

- 43. VENTRUS BIOSCIENCES July 25, 2011 Fecal Incontinence • Inability to control defecation resulting from inadequate anal sphincter function, and can be caused by muscle/sphincter weakness, neurologic impairment, physical trauma or surgery • Conservative therapy includes: • Diet modification • Sitz baths • OTC antidiarrheal medications • Medical therapy: • Solesta: Injectable inert bulking agent product for patients who have failed conservative therapy; injected submucosally around the sphincter • Administered in outpatient setting • Surgical therapy: • Sphincteroplasty for physical injury – success rates are low • Colostomy – extreme • Other: • Sacral nerve stimulation; direct sphincter electrical stimulation 43

- 44. VENTRUS BIOSCIENCES July 25, 2011 VEN 308 Profile • Topically applied phenylephrine gel • Increases anal sphincter tone, improves fecal continence • Internal sphincter receives sympathetic innervation to maintain resting sphincter tone • Phenylephrine is a1 adrenergic agonist that can increase anal sphincter pressure and contract the internal sphincter muscle • Phenylephrine is available as OTC meds but not as a gel, doses typically 40-60mg/d • Use for this indication identified in 1996 at St. Mark hospital in London (Kamm, Phillips) with IP filed then • Patents assigned to S.L.A. Pharma in 1997 • Patents licensed to Solvay in 2001, which improved the manufacturing and formulation process and conducted PK studies • License returned to S.L.A. in 2004 after Solvay exited GI and women’s health development 44

- 45. VENTRUS BIOSCIENCES July 25, 2011 VEN 308 – Development Status • In-licensed from S.L.A. Pharma for North American rights (via Paramount BioCapital) • Part of same agreement that brought in VEN 307 • Not actively developing at this time due to resource limitations but Phase IIb ready • Likely to advance this product in 2012 and could be submitted for approval by 2015 • Although VEN 308 trails in development, we still see this as a very attractive opportunity • High unmet medical need • Focused commercial effort • Plausible clinical mechanism 45

- 46. VENTRUS BIOSCIENCES July 25, 2011 Fecal Incontinence Is a Common Disorder • Medical literature suggests 7M patients in U.S. with any form of fecal incontinence • Ascertainment bias makes the true prevalence extremely difficult to discern; household survey by Nelson, JAMA 1995 found 2.2% prevalence among 6,959 households. Other estimates tend to range from 1-3% • No good treatment options currently, high unmet medical need based on social aspects of the disease • Estimated >$400M spent per year for adult diapers for incontinence • Fecal incontinence is 2nd leading cause for nursing home placement in U.S., may affect 30% of institutionalized patients 46

- 47. VENTRUS BIOSCIENCES July 25, 2011 But VEN 308 Is Being Developed for Orphan Indication • Company pursuing an Orphan indication of fecal incontinence due to ileal pouch anal anastomosis (IPAA) • Surgical procedure, part of colectomy to restore rectal function and eliminate need for an ostomy bag • Represents more homogeneous patient population and enables Orphan designation for market exclusivity • Fecal incontinence is a common consequence in up to 40% of patients; estimated 50-100K patients in the U.S. with incontinence resulting from this condition • Intrinsic neural control to internal anal sphincter is lost due to division of GI tract at anorectal junction; the neural connection can be re-established in some patients (evidence by return of the rectoanal inhibitor reflex) but in most patients it remains absent or is only partially restored 47

- 48. VENTRUS BIOSCIENCES July 25, 2011 Cause of Fecal Incontinence Is Important for Considering Role of Phenylephrine • Fecal incontinence can be to stool, diarrhea or flatus, all are meaningfully troubling to patients and can lead to social isolation or even cause entry into extended care facility • Most common cause of fecal incontinence appears to be muscular or structural damage to the external sphincter or internal sphincter • Functional (fecal impaction, diarrhea, cognitive) • Sphincter weakness (muscle injury, pudendal nerve injury. CNS injury) • Sensory loss (afferent nerve injury) • Smaller population with nerve innovation damage • Ileal pouch-anal anastomosis (IPAA) – about 30% of patients suffer seepage or incontinence • Can also be seen in neurologic deterioration such as MS, spinal cord injury, congenital disorders such as spina bifida We believe phenylephrine should have best activity in patients with neurologic defects as opposed to structural damage 48

- 49. VENTRUS BIOSCIENCES July 25, 2011 Phenylephrine Gel Investigator Initiated Studies Baseline Publication Patients Indication Drug Design Duration incontinence Results 40% improvement in 10% gel or placebo, Double-blind, incontinence score vs 0% for Carapeti, Dis Col Fecal incontinence for 17 (on 0-24 12 0.5mL topically to anal placebo-controlled 4 weeks placebo; 33% complete Rec 2000 IPAA scale) margin bid cross-over response versus 0% for placebo Fecal incontinence 10% cream or Double-blind, Negative; although 75% Carapeti, Br J 14 (on 0-24 36 with normal sphincter placebo; 0.5mL placebo-controlled 4 weeks improvement noted in 17% of Surg 2000 scale) structure topically to anus bid cross-over treated and 6% of untreated Fecal incontinence Cheetham, Gut 20% cream applied to Double blind, 30 with normal sphincter 4 weeks No clinical efficacy 2000 anal canal bid placebo-controlled structure Fecal incontinence 10% gel applied to 17% improvement in 17 (on 0-24 Badvie, 2005 15 post pelvic mucosa of anal canal Open label 4 weeks incontinence score; 50% scale) radiotherapy bid considered the gel helpful 34% improvement in Fecal incontinence 20% gel applied bid, 9 (on 0-24 incontinence score vs 18% for McCune, 2003 21 post- Placebo-controlled 4 weeks 0.5ml scale) placebo. QOL improvement hemorrhoidectomy also seen 38% improvement in Anal seepage with incontinence score, but 1/3 of 10% cream applied to 9.5 (on 0-24 Mutch, 2002 26 intact sphincter; Open labal 30 days patients with improvement did anus tid scale) multiple causes not have increased resting sphincter pressure Source: VTUS S-1 Results in IPAA are strongest; other studies have not clearly defined a homogeneous patient population for evaluation. We believe etiology of incontinence is important for predicting phenylephrine clinical success 49

- 50. VENTRUS BIOSCIENCES July 25, 2011 Why We See Meaningful Value In VEN 308 • Orphan drug indication provides 7+ years of protection against generics • May be able to identify novel dosing or method of use IP for further patent protection • Citizen’s Petition as a topical therapy may be able to buy an additional year • Extremely high unmet medical need • Prospects for success comparable to VEN 307 but commercial opportunity/market exclusivity more compelling • Potential to identify additional Orphan indications for incontinence • Individual neurologic conditions with associated fecal incontinence, such as MS • The Makena experience highlights the limitations on pricing, but even modest commercial opportunity is compelling relative to current valuation • Makena’s original price point was $20K, causing outrage in the ob/gyn and patient communities and among politicians • Less attention paid to pricing of AVNR’s Neudexta at ~$5K/treatment (although still a focal point for some Senators) • We doubt a $2.5k/year price point would attract much attention and would be sufficient to drive VEN 308 to >$75M/year in peak revenue 50

- 51. VENTRUS BIOSCIENCES July 25, 2011 VEN 308 Market Assumptions • US fecal incontinence population due to IPAA – 100k, growing 1.5% y/y • 60% of patients seeking treatment or actively followed by specialist • Market penetration for VEN 308 – rising to 35% until 7-year orphan drug protection runs out in 2024 with an extra year of exclusivity driven by Citizen’s Petition • Revenue per patient – $2,500 per year, growing at 2% y/y 51

- 52. VENTRUS BIOSCIENCES July 25, 2011 VEN 308 Revenue Projections VEN 308 Sales 70 60 50 40 VEN 308 64 30 52 20 40 29 10 19 9 5 0 0 2017 2018 2019 2020 2021 2022 2023 2024 Source: Leerink Swann estimates VTUS only has U.S. rights; could identify novel dosing or method of use IP to extend market exclusivity 52

- 53. VENTRUS BIOSCIENCES July 25, 2011 S.L.A. Pharma Agreement • Covers VEN 307 and VEN 308 • Signed in March 2007 between Paramount and S.L.A. • Paramount was required to form a company to develop the programs and issued 5% ownership to S.L.A. Future milestone payments up to $20M for regulatory events for the 2 products • Total payment obligation to S.L.A. for clinical development costs for VEN 308 will not exceed $1.2M; already paid $974k. Total payment obligation for clinical development costs for VEN 307 of up to $4M; has already paid $3.2M • Originally owed $800k for S.L.A. completing enrollment in EU Phase III study of VEN 307 and could terminate the agreement if VTUS failed to make a required payment and 3rd party wanted to enter an agreement for 307 and 308 • These terms were eliminated as part of a June 2011 amendment; in return, VTUS owes up to $1M milestones over 4 equal installments for progress in the EU Phase III study of VEN 307 and $400k upon receipt of the EU Phase III study results (in addition to the $4M obligation) • Owe mid- to high-single-digit royalty for VEN 307 • Owe mid-single-digit royalty for VEN 308 53

- 54. VENTRUS BIOSCIENCES July 25, 2011 Financials at a Glance • Sufficient cash through 2014 when the second Phase III trial for VEN 309 should end • Sufficient cash to develop VEN 309 and VEN 307 • If receive upfront from a potential partner for VEN 309, then could move forward with VEN 308 without requiring raising additional capital • Estimated development cost until approval • VEN 309 - $40M • VEN 307 - $20M • VEN 308 - $15M • Diluted shares after recent financing – 15.2M • Expect minimum spend outside of clinical trials as headcount unlikely to exceed 15-20 in the near term 54

- 55. VENTRUS BIOSCIENCES July 25, 2011 Upcoming Catalysts • 3Q11 – VEN 309 hemorrhoids Phase III trial start • 1Q12 – VEN 309 hemorrhoids Phase III results • 2Q12 – VEN 307 anal fissure EU Phase III trial results (S.L.A. trial) • 2H12 – VEN 307 anal fissure U.S. Phase III trial start • 2013 – NDA filing for VEN 307 • Mid-2014 – NDA filing for VEN 309 55

- 56. VENTRUS BIOSCIENCES July 25, 2011 VTUS DCF Base Valuation: $24-26 per share • Downside Scenario Valuation: $2/share • Residual cash if all 3 programs fail • Base Scenario Valuation: $24-26/share • VEN 309 U.S. sales peak at ~$400M in 2025 with patent expiry in 2030 • VEN 307 U.S. sales peak at ~$55M in 2020 • VEN 308 U.S. sales peak at ~$75M in 2025 • Given clinical trial (and some IP) uncertainty, we use a premium 14% discount rate versus the standard 10% for biotech peers (roughly comparable to assuming 50% chance of successfully reaching our projections). We use a terminal multiple on 2025E earnings of 5-6x to reflect patent expiry for VEN 309 in 2030 • Upside Scenario Valuation: $70-75/share • VEN 309 U.S. sales peak at $1B in 2025; other assumptions unchanged, use 10% discount rate to reflect clinical and commercial success VTUS DCF BASE VALUATION ANALYSIS Discount Rate $ 26 11.0% 12.0% 13.0% 14.0% 15.0% 16.0% 17.0% Terminal Multiple 4 $31 $28 $25 $22 $19 $17 $15 5 $34 $30 $27 $24 $21 $19 $17 6 $37 $33 $29 $26 $23 $20 $18 7 $40 $35 $31 $27 $24 $22 $19 8 $43 $38 $33 $29 $26 $23 $20 Source: Leerink Swann estimates 56

- 57. VENTRUS BIOSCIENCES July 25, 2011 VTUS QUARTERLY P&L ($MM except per share data) 1Q11A 2Q11E 3Q11E 4Q11E 2011E 1Q12E 2Q12E 3Q12E 4Q12E 2012E Net Product Revenue $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Total Rev (MM) $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 $0.0 Y/Y N/M N/M N/M N/M N/M N/M N/M N/M N/M N/M COGS - - - - - - - - - - % product sales 0 0%0 0%0 0%0 0%0 N/M0 0%0 0%0 0%0 0% N/M 0 0 R&D 1.0 1.6 5.0 18.0 25.6 6.0 6.0 6.0 6.0 24.0 % Rev N/M N/M N/M N/M N/M 0% 0% 0% 0% N/M SG&A 1.7 1.8 1.7 1.7 6.9 1.7 1.7 1.7 1.7 6.8 % Rev N/M N/M N/M N/M N/M 0% 0% 0% 0% N/M Total operating expenses 2.7 3.4 6.7 19.7 32.5 7.7 7.7 7.7 7.7 30.8 Operating (loss)/gain -3 -3 -7 -20 -32 -8 -8 -8 -8 -31 Investment & other income (expense) Interest income $0.01 $0.0 $0.1 $0.1 $0.2 $0.5 $0.5 $0.5 $0.3 $1.8 Intererest expense ($0.07) $0 $0 $0 ($0) $0 $0 $0 $0 $0 Pre-tax Income ($2.7) ($3.4) ($6.6) ($19.6) ($32.3) ($7.2) ($7.2) ($7.2) ($7.4) ($29.0) Taxes (benefit) $0 $0 $0 $0 $0 $0 $0 $0 $0 $0 Tax rate 0% 0% 0% 0% 0% 0% 0% 0% 0% 0% Net Income/(loss) (MM) 0 ($2.7) 0 ($3.4) 0 ($6.6) 0 ($19.6) 0 ($32.3) 0 ($7.2) 0 ($7.2) 0 ($7.2) 0 ($7.4) 0 ($29.0) 0 Diluted EPS ($0.38) ($0.48) ($0.54) ($1.59) ($3.32) ($0.59) ($0.58) ($0.58) ($0.59) ($2.33) Y/Y 0 N/M 0% N/M 0% N/M 0% N/M 0% NM 0% N/M 0% N/M 0% N/M 0% N/M 0% NM 0% Basic shares 7.1 7.1 12.3 12.3 9.7 12.3 12.4 12.5 12.6 12.5 Diluted shares 9.9 9.9 15.2 15.2 12.6 15.0 15.4 15.4 15.4 15.4 Source: Company reports and Leerink Swann estimates 57

- 58. VENTRUS BIOSCIENCES July 25, 2011 VTUS MARKET MODEL ($MM except per share data) 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E VEN 309 (hemorrhoids) US hemorrhoids prevalence (000s) 12000 12000 12180 12363 12548 12736 12927 13121 13318 % seeking treatment 33% 33% 33% 33% 33% 33% 33% 33% 33% # seeking treatment (000s) 3960 3960 4019 4080 4141 4203 4266 4330 4395 % on VEN 309 0 0% 0% 0% 2% 4% 6% 8% 10% # on VEN 309 (000s) 0 0 0 0 83 168 256 346 439 Revenue per patient ($) 425 425 425 434 442 451 460 US VEN 309 sales (mm) $0 $0 $0 $0 $35 $73 $113 $156 $202 OUS VEN 309 sales (mm) $25 $51 $79 VEN 307 (anal fissures) US anal fissure prevalence (000s) 750 750 761 773 784 796 808 820 832 % seeking treatment 0 50% 50% 50% 50% 50% 50% 50% 50% # seeking treatment (000s) 248 375 381 386 392 398 404 410 416 % on VEN 307 0 0% 0% 2% 4% 7% 10% 13% 15% # on VEN 307 (000s) 0 0 0 8 16 28 40 53 62 Revenue per patient ($) 650 650 650 663 676 690 704 US VEN 307 sales (mm) $0 $0 $0 $5 $10 $18 $27 $37 $44 VEN 308 (fecal incontinence) - orphan US fecal incontinence prevalence (000s) 100 100 102 103 105 106 108 109 111 % seeking treatment 0 60% 60% 60% 60% 60% 60% 60% 60% # seeking treatment (000s) 33 60 61 62 63 64 65 66 67 % on VEN 308 0 0% 0% 0% 0% 0% 0% 3% 5% # on VEN 308 (000s) 0 0 0 0 0 0 0 2 3 Revenue per patient ($) 2500 2500 2500 2550 2601 2653 2706 US VEN 308 sales (mm) $0 $0 $0 $0 $0 $0 $0 $5 $9 Source: Leerink Swann estimates 58

- 59. VENTRUS BIOSCIENCES July 25, 2011 VTUS ANNUAL P&L ($MM except per share data) 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E Net Product Revenue $0 $0 $0 $5 $45 $91 $140 $198 $255 Royalty/Milestone $0 $0 $0 $50 $0 $0 $5 $10 $16 Total Rev (MM) $0 $0 $0 $55 $45 $91 $145 $208 $271 Y/Y N/M N/M N/M N/M -18% 101% 59% 43% 30% COGS 0 0 0 1 5 10 15 21 24 % product sales N/M N/M N/M 14% 11% 11% 11% 11% 9% R&D 26 24 27 26 22 30 31 31 32 % Rev N/M N/M N/M N/M 48% 33% 21% 15% 12% SG&A 7 7 7 32 65 70 80 90 100 % Rev N/M N/M N/M N/M 143% 77% 55% 43% 37% Total operating expenses 32 31 34 59 92 110 126 143 156 Operating (loss)/gain -32 -31 -34 -4 -47 -19 20 66 115 Interest income 0 2 2 2 2 2 4 6 8 Intererest expense 0 0 $0 $0 $0 $0 $0 $0 $0 Pre-tax Income ($32) ($29) ($32) ($2) ($45) ($17) $24 $72 $123 Taxes (benefit) 0 $0 $0 $0 $0 ($4) $8 $25 $43 Tax rate 0% 0% 0% 0% 0% 25% 35% 35% 35% Net Income/(loss) (MM) ($32) ($29) ($32) ($2) ($45) ($12) $15 $47 $80 Diluted EPS ($3.32) ($2.33) ($2.21) ($0.10) ($2.65) ($0.73) $0.80 $2.42 $4.11 Y/Y NM NM NM NM NM NM -210% 201% 70% Basic shares 9.7 12.5 14.5 16.7 16.8 17.0 17.2 17.3 17.5 Diluted shares 13 15 18 19 19 19 19 19 20 Source: Company reports and Leerink Swann estimates 59

- 60. VENTRUS BIOSCIENCES July 25, 2011 VTUS ANNUAL CASH FLOWS ($MM except per share data) Cash Flows 2011E 2012E 2013E 2014E 2015E 2016E 2017E 2018E 2019E Net Income/Loss -32.3 -29.0 -32.0 -1.7 -44.6 -12.4 15.4 46.7 80.2 Use of NOLs 0 0 0 0 0 0 8 25 22 Deferred revenue (milestone/upfront adjustments) 0 0 0 0 0 0 0 0 0 Stock based comp 4 5 5 7 10 12 13 14 15 Depreciation/amortization 0 1 1 1 1 1 1 1 1 Change in operating assets and liabilities Accounts receivable 0 0 0 -2 -5 -5 0 0 0 Inventory 0 0 0 -10 -5 0 0 0 0 Accounts payable -1 -1 -1 -2 -5 -5 0 0 0 Other 0 0 0 0 0 0 0 0 0 Cash from operations -29 -24 -27 -8 -49 -9 38 87 118 PP&E $0 2 5 5 5 5 5 5 5 Other $0 0 0 0 0 0 0 0 0 FCF ($29) ($26) ($32) ($13) ($54) ($14) $33 $82 $113 FCF/share ($2.33) ($1.70) ($1.75) ($0.68) ($2.86) ($0.76) $1.71 $4.24 $5.78 Y/Y NM NM NM NM NM N/M N/M 148% 36% Common stock sale, options 50.0 2 50 75 3 3 3 3 3 Debt sale 0.0 0 0 0 0 0 0 0 0 Repayment of notes -2.5 0 0 0 0 0 0 0 0 Other financing 0.1 0 0 0 0 0 0 0 0 Cash from financing 48 2 50 75 3 3 3 3 3 Debt $0 $0 $0 $0 $0 $0 $0 $0 $0 Cash (MM) $33 $9 $27 $89 $38 $27 $63 $148 $263 Source: Company reports and Leerink Swann estimates VTUS DCF BASE VALUATION ANALYSIS Discount Rate $ 26 11.0% 12.0% 13.0% 14.0% 15.0% 16.0% 17.0% 4 $31 $28 $25 $22 $19 $17 $15 Terminal Multiple 5 $34 $30 $27 $24 $21 $19 $17 6 $37 $33 $29 $26 $23 $20 $18 7 $40 $35 $31 $27 $24 $22 $19 8 $43 $38 $33 $29 $26 $23 $20 Source: Leerink Swann estimates 60

- 61. VENTRUS BIOSCIENCES July 25, 2011 Disclosures Appendix Analyst Certification I, Joshua Schimmer, M.D., certify that the views expressed in this report accurately reflect my views and that no part of my compensation was, is, or will be directly related to the specific recommendation or views contained in this report. Valuation Our valuation range for VTUS is $24-26 based on our DCF calculations. Due to uncertainty surrounding the clinical success, regulatory success and duration of the patent protection, we use a higher discount rate of 14% versus our usual 10-12%. We model revenues of VEN309, VEN307 and VEN308 until the end of the patent or data exclusivity protection and assign only minimal sales beyond that time attributable to potential Citizen's Petitions against generic versions of topical drugs. Risks to Valuation • Poor efficacy or safety results in clinical trials for VEN309, VEN307, VEN308. • Regulatory setbacks from the FDA or EMA. • Inability to obtain favorable drug pricing and reimbursement for VEN309, VEN307, VEN308. • Difficulty competing against compounded generic drugs and/or OTC medication. Rating and Price Target History for: Ventrus Biosciences (VTUS) as of 07-22-2011 25 20 15 10 5 0 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q3 2009 2010 2011 OP=Outperform MP=Market Perform UP=Underperform D=Drop Coverage I=Initiate SC=Suspend Coverage Created by BlueMatrix 61

- 62. VENTRUS BIOSCIENCES July 25, 2011 Rating and Price Target History for: Acorda Therapeutics (ACOR) as of 07-22-2011 04/27/09 07/02/09 02/18/10 04/15/10 10/21/10 01/05/11 I:UP OP MP OP MP OP 48 40 32 24 16 8 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q3 2009 2010 2011 OP=Outperform MP=Market Perform UP=Underperform D=Drop Coverage I=Initiate SC=Suspend Coverage Created by BlueMatrix Rating and Price Target History for: Bristol-Myers Squibb (BMY) as of 07-22-2011 06/11/10 OP 32 28 24 20 16 12 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q3 Q1 Q2 Q3 2009 2010 2011 On July 15, 2004 Leerink Swann placed a Market Perform rating on BMY. OP=Outperform MP=Market Perform UP=Underperform D=Drop Coverage I=Initiate SC=Suspend Coverage Created by BlueMatrix 62