Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (9)

Semelhante a RPC Report 11.7.14

Semelhante a RPC Report 11.7.14 (17)

RPC Report 11.7.14

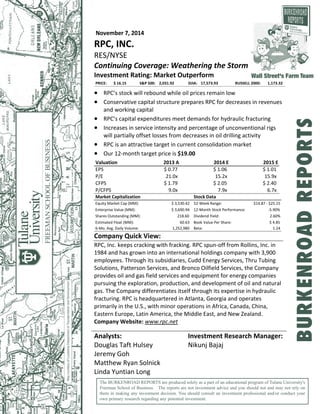

- 1. November 7, 2014 RPC, INC. RES/NYSE Continuing Coverage: Weathering the Storm Investment Rating: Market Outperform PRICE: $ 16.15 S&P 500: 2,031.92 DJIA: 17,573.93 RUSSELL 2000: 1,173.32 RPC’s stock will rebound while oil prices remain low Conservative capital structure prepares RPC for decreases in revenues and working capital RPC’s capital expenditures meet demands for hydraulic fracturing Increases in service intensity and percentage of unconventional rigs will partially offset losses from decreases in oil drilling activity RPC is an attractive target in current consolidation market Our 12‐month target price is $19.00 Valuation EPS P/E CFPS P/CFPS 2013 A $ 0.77 21.0x $ 1.79 9.0x 2014 E $ 1.06 15.2x $ 2.05 7.9x 2015 E $ 1.01 15.9x $ 2.40 6.7x Market Capitalization Stock Data Equity Market Cap (MM): $ 3,530.42 52‐Week Range: $14.87 ‐ $25.15 Enterprise Value (MM): $ 3,690.94 12‐Month Stock Performance: ‐5.90% Shares Outstanding (MM): 218.60 Dividend Yield: 2.60% Estimated Float (MM): 60.63 Book Value Per Share: $ 4.85 6‐Mo. Avg. Daily Volume: 1,252,980 Beta: 1.24 Company Quick View: RPC, Inc. keeps cracking with fracking. RPC spun‐off from Rollins, Inc. in 1984 and has grown into an international holdings company with 3,900 employees. Through its subsidiaries, Cudd Energy Services, Thru Tubing Solutions, Patterson Services, and Bronco Oilfield Services, the Company provides oil and gas field services and equipment for energy companies pursuing the exploration, production, and development of oil and natural gas. The Company differentiates itself through its expertise in hydraulic fracturing. RPC is headquartered in Atlanta, Georgia and operates primarily in the U.S., with minor operations in Africa, Canada, China, Eastern Europe, Latin America, the Middle East, and New Zealand. Company Website: www.rpc.net Analysts: Investment Research Manager: Douglas Taft Hulsey Nikunj Bajaj Jeremy Goh Matthew Ryan Solnick Linda Yuntian Long The BURKENROAD REPORTS are produced solely as a part of an educational program of Tulane University's Freeman School of Business. The reports are not investment advice and you should not and may not rely on them in making any investment decision. You should consult an investment professional and/or conduct your own primary research regarding any potential investment. Wall Street's Farm Team BURKENROADREPORTS

- 3. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 3 Oil and natural gas production is in the process of changing from conventional drilling to unconventional, horizontal drilling. Pressure pumping, the process of hydraulic fracturing in unconventional rigs, makes up over 55% of RPC’s revenue. RPC meets the growing demand of its customers for higher service intensity and more unconventional drilling with its advanced and growing fleet of pressure pumping equipment. In fact, RPC will spend over $250 million in the second half of 2014 to expand and maintain its pressure pumping fleet in order to meet increasing customer demands. However, going forward RPC will decrease its capital expenditures in preparation for decreases in new oil drilling activity when contracts expire in the second half of 2015. Although rig counts will decrease in the near future with the drop in oil prices, service intensity and the percentage of unconventional rigs will continue to rise. These market trends will cushion RPC’s losses from decreases in new oil drilling activity. Table 1: Historical Burkenroad Ratings and Prices Date Rating Price* 11/08/2013 Market Perform $17.45 10/26/2012 Market Perform $10.61 11/11/2011 Market Outperform $12.82 11/08/2010 Market Outperform $10.31 11/30/2009 Market Outperform $3.78 12/08/2008 Market Outperform $3.43 12/04/2007 Market Perform $4.19 11/30/2006 Market Perform $5.51 03/15/2005 Market Outperform $2.44 02/02/2004 Market Perform $1.21 03/14/2003 Market Perform $1.13 03/20/2002 Market Outperform $1.63 04/15/2001 Buy $1.34 *Price at time of report date INVESTMENT THESIS We established a 12‐month target price of $19.00 and a rating of Market Outperform for RPC, Inc. Our analysis of RPC’s future performance is driven by several market and internal conditions: oil prices, service intensity and unconventional rig counts, and RPC’s capital structure, capital expenditures, and share ownership. RPC’s stock will rebound while oil prices remain low The recent drop in oil prices to $80 per barrel will likely persist over the next two years or even longer. The U.S. move towards oil independence caused OPEC to maintain production quotas in Saudi Arabia and remain comfortable with oil prices around $80 per barrel. As such, energy companies have plummeted in the markets, seeing average losses in the industry of 30%. RPC’s stock price dropped from $22.37 on September 26 to $16.15 on November 7. We believe this (27.8%) drop is an extreme overreaction to the recent decline in oil prices and RPC’s stock is currently undervalued.

- 16. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 16 PEER ANALYSIS The U.S. oil and gas field services industry is highly competitive, with three companies, Baker Hughes, Inc., Halliburton Company, and Schlumberger Limited covering 32.5% of the industry’s market share. However, these companies are much larger than RPC, Inc. As such, smaller, more focused oil and gas field service companies represent better comparables than these services giants. Based on recommendations from RPC’s management and our own analysis, we chose the following four companies for comparison (see Table 2): Basic Energy Services, Inc., C&J Energy Services, Inc., Patterson‐UTI Energy, Inc., and Seventy Seven Energy, Inc. Table 2: RPC Comparable’s Key Ratios Revenue Mkt Cap P/E ROIC (%) Debt/Equity RPC, Inc. $2.192B $4.724B 23.14 9.5 0.14x Patterson $2.940B $4.668B 38.73 2.0 0.24x C&J $1.390B $1.641B 30.55 5.1 0.40x Seventy Seven $2.097B $1.205B N/A (1.1) 5.48x Basic $1.398B $0.884B 271.13 0.3 2.18x Source: S&P Capital IQ ‐ LTM as of September 30, 2014 Patterson‐UTI Energy, Inc. (NASDAQ/PTEN) Patterson‐UTI Energy, Inc., headquartered in Snyder, Texas, provides pressure pumping and onshore contract drilling services to oil and natural gas producers in the U.S. and western Canada. The pressure pumping segment delivers well stimulation through hydraulic and nitrogen fracturing predominantly in Texas and the Appalachian Basin. The onshore contract drilling segment provides drilling rigs and crews to oil and gas field operators. Patterson‐UTI controls over 275 land‐based drilling rigs in North America. C&J Energy Services, Inc. (NYSE/CJES) C&J Energy Services, Inc., headquartered in Houston, Texas, provides oil and gas field services in the U.S. The company operates through its subsidiaries to provide services categorized into three segments: stimulation and well intervention services, wireline services, and equipment manufacturing. C&J Energy Services’ biggest segment is stimulation & well intervention services, which accounts for about 69% of total revenue. Hydraulic fracturing accounts for about 80% of revenue within the segment. Other significant services provided by C&J include constructing and maintaining equipment used by themselves and other companies.

- 18. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 18 Table 3: Return on Assets (ROA) Period RPC, Inc. Patterson‐UTI Energy, Inc. C&J Energy Service, Inc. Seventy‐ Seven Energy, Inc. Basic Energy Services, Inc. 2011 22.1% 7.6% 30.1% 1.7% 3.1% 2012 20.1% 6.6% 18.0% 3.3% 1.2% 2013 12.1% 4.0% 5.9% (1.0%) (2.3%) 9/30/14 (LTM) 12.7% 2.4% 3.5% (0.9%) 0.2% Source: S&P Capital IQ R. Randall Rollins Chairman of the Board of Directors (82) R. Randall Rollins has managed RPC since the spin off from Rollins, Inc. in 1984. Mr. Rollins served RPC as Chief Executive Officer from 1984 to 2003 and is currently Chairman of the Board, a position he has held since 1984. In addition to his roles at RPC, Mr. Rollins is the Chairman of the Board for Marine Products Corporation and Rollins, Inc. Mr. Rollins is also a Director of Dover Downs Gaming & Entertainment and Dover Motorsports, Inc. He has over 30 years of experience in the U.S. oil and gas field services industry. Richard A. Hubbell President and Chief Executive Officer (69) Richard A. Hubbell has served as President of RPC since 1987 and the Chief Executive Officer (CEO) since 2003. Mr. Hubbell has also served as a Director for RPC since 1987. Prior to becoming CEO, Mr. Hubbell served as Chief Operating Officer at RPC from 1987 to 2003. In addition to his roles at RPC, Mr. Hubbell is a Director and the President and Chief Executive Officer at Marine Products Corporation. He has over 27 years of experience in the U.S. oil and gas field services industry. Ben M. Palmer Chief Financial Officer (54) Ben M. Palmer has served as Chief Financial Officer, Treasurer, Vice President, and Principal Accounting Officer of RPC since 1996. Mr. Palmer also serves as the Treasurer of RPC’s subsidiary, Cudd Energy Services. In addition to his roles at RPC, Mr. Palmer is the Chief Financial Officer, Treasurer, Vice President, and Principal Accounting Officer at Marine Products Corporation. He has over 18 years of experience in the U.S. oil and gas field services industry.

- 20. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 20 SHAREHOLDER ANALYSIS RPC, Inc.’s equity structure, as at September 30, 2014, is comprised of 215.2 million shares outstanding with a free float of 60.26 million shares. The outstanding common stock is distributed among various investor types including investment managers, brokerage firms, and strategic entities composed of two corporations and nine individuals. An important aspect to note is the limited number of shares available for purchase in the open market due to high internal holdings. The Rollins Family Trust holds the largest stake in the Company at approximately 68.8 percent. This figure, in combination with ownership of a select few inside officers and directors, totals around 71.04% (see Table 4). As indicated by the low float ratio, the Company’s equity structure has a high internal ownership in order to obtain the status of a “Controlled Corporation.” This allows the Board of Directors to effectively control the operations of the Company, including the election of the board of directors. The high internal concentration of Company ownership also mitigates the risk of possible third party takeovers. In 1993, RPC initiated a share buyback program that authorized the repurchasing of 26.57 million shares over an unspecified amount of time. On June 5, 2013, the program was supplemented by an additional authorization of another five million shares able for repurchase. As of September 30, 2014, 4.1 million shares remain available for repurchase. RPC has consistently purchased its shares from the market over the last few years and has announced share repurchases in both the first and third quarters of 2014 in the amounts of 399,611 and 209,485 shares, respectively. This consistent exercising of the buyback program reflects RPC’s priorities of maintaining internal control as well as increasing the value of each share by limiting available shares in the open market. Table 4: Top Ten Investors (2014) Investor Name % O/S R. Randall Rollins 66.40 Gabelli Funds, LLC 4.37 Gary W. Rollins 2.35 The Vanguard Group, Inc. 1.97 BlackRock, Inc. 1.48 Milennium Management LLC 1.34 Richard A. Hubbell 1.19 Henry B. Tippie 1.10 Citadel Investment Group, LLC 0.84 TIAA‐CREF 0..76 Source: S&P Capital IQ September 30, 2014

- 23. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 23 Financial Risks Liquidity Risk Liquidity measures how easily assets can be converted into cash. The current liquidity ratio measures a company’s ability to quickly pay off current liabilities with liquid assets by dividing current assets by current liabilities. RPC’s current liquidity ratio more than two and a half times the industry average (see Table 5). A high level of liquidity puts RPC at a low financial risk because the Company three times more current assets than current liabilities. Table 5: RPC Liquidity and Solvency RPC, Inc. Industry Average Current Liquidity Ratio 3.3x 1.3x Leverage Ratio 14.3% 39.4% Source: S&P Capital IQ September 30, 2014 Solvency Risk RPC’s leverage is driven by the Company’s level of debt. RPC currently has a $350 million revolving credit facility with an expiration date of January 17, 2019. This means RPC can borrow up to $350 million over the life of the revolving credit facility. As of September 30, 2014 RPC had outstanding borrowings of $152 million with $78 million of the balance borrowed in the first two quarters of 2014. The leverage ratio measures a company’s capital structure by comparing debt‐to‐equity. RPC’s current leverage ratio on September 30, 2014 is three times less than the U.S. oil and gas field services industry average. RPC achieved this low ratio because the Company maintains an extremely conservative capital structure compared to its peers. A conservative capital structure mitigates RPC’s financial risk because the Company does not use debt to finance its operations. RPC’s leverage ratio at year‐end 2013 was 5.5% and rose to 12.9% at June 30, 2014. This significant increase is attributed to the $78 million debt borrowed through the revolving credit facility in the first two quarters of 2014. RPC’s leverage ratio is still conservative compared to the industry average, but RPC will face increased financial risk from its leverage if the Company continues to borrow debt. Interest Rate on Debt Risk RPC’s $152 million outstanding balance on the revolving credit facility bears interest on a floating rate. If the interest rate on the outstanding balance changed one percent, interest costs would consequentially change $1.5 million. Although small compared to other risks, the interest rate risk creates financial risk for RPC.

- 28. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 28 ANOTHER WAY TO LOOK AT IT ALTMAN Z‐SCORE The Altman Z‐score, designed by Edward Altman, was published in 1968 and is still widely used today to estimate a company’s risk of bankruptcy. After a Z‐score is calculated, the company under analysis will fall into one of three zones: distress (Z‐score below 1.8), grey (Z‐score between 1.8 and 2.99), and safe (Z‐score above 2.99) For our purposes, we use five key financial ratios to calculate the Z‐score: (1) working capital/total assets, (2) retained earnings/total assets, (3) EBITDA/total assets, (4) market value of equity/total liabilities, and (5) net sales/total assets. For 2013, RPC, Inc. has a Z‐score of 8.91. This places the Company deep in the “safe” zone, with little risk of bankruptcy. RPC has been in the “safe” zone since 2006 (see Table 6). This is largely due to RPC’s conservative capital structure, and reluctance to take out loans. Table 6: RPC’s Z‐scores Year Ended 2006 2007 2008 2009 2010 2011 2012 2013 Z‐score 14.12 6.15 5.27 7.65 10.11 7.79 7.06 8.91 Zone Safe Safe Safe Safe Safe Safe Safe Safe

- 30. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 30 WWBD?What Would Ben (Graham) Do? Benjamin Graham was a professional investor, known by many as “the father of value investing” and Warren Buffet’s mentor. Graham’s method of value investing made him one of the most successful investors in the world. Many investors still incorporate his method of minimizing risks into their own investment strategy today. Graham’s method analyzes a company’s stock based on ten criteria, eight of which are used in this report. Based on our analysis of RPC, Inc., the Company meets four out of the eight selected criteria. This puts RPC in the category where Ben Graham would “consider the possibility” of buying stock in RPC. The criteria that RPC meets are: (1) The dividend yield is more than half the yield on a 10‐year Treasury bond, (2) Total debt is less than its Book Value of equity, (3) Current Ratio (Current Assets divided by Current Liabilities) of two or more, and (4) An earnings growth of more than 7% over the past five years. The criteria that RPC does not meet are: (1) Earnings to price yield of two times more than the yield on the 10 year Treasury bond, (2) Price/Earnings ratio less than half of the stock’s highest in five years, (3) A stock price that is less than one and a half times Book Value of equity, and (4) Stability in growth of earnings. From the mixed results of Ben Graham’s analysis, RPC is shown to be a stock that is neither undervalued nor overvalued (see Figure 11). However, the fluctuation in earnings growth makes predicting RPC’s future performance very difficult. Figure 11: Ben Graham Analysis

- 31. RPC Incorporated (RES) BURKENROAD REPORTS (www.burkenroad.org) November 7, 2014 31 Earnings per share (ttm) 0.65$ Price: 16.15$ Earnings to Price Yield 4.01% 10 Year Treasury (2X) 4.64% P/E ratio as of 12/31/09 (101.2) P/E ratio as of 12/31/10 27.1 P/E ratio as of 12/31/11 13.6 P/E ratio as of 12/31/12 9.6 P/E ratio as of 12/31/13 23.2 Current P/E Ratio 24.9 Dividends per share (ttm) $0.73 Price: 16.15$ Dividend Yield 4.49% 1/2 Yield on 10 Year Treasury 1.16% Stock Price 16.15$ Book Value per share as of 9/30/14 4.93$ 150% of book Value per share as of 9/30/14 7.39$ Interest‐bearing debt as of 9/30/14 152,000$ Book value as of 9/30/14 1,060,945$ Current assets as of 9/30/14 785,056$ Current liabilities as of 9/30/14 241,476$ Current ratio as of 9/30/14 3.3 EPS for year ended 12/31/13 0.77$ EPS for year ended 12/31/12 1.27$ EPS for year ended 12/31/11 1.35$ EPS for year ended 12/31/10 0.67$ EPS for year ended 12/31/09 (0.10)$ EPS for year ended 12/31/13 0.77$ ‐39% EPS for year ended 12/31/12 1.27$ ‐6% EPS for year ended 12/31/11 1.35$ 102% EPS for year ended 12/31/10 0.67$ 750% EPS for year ended 12/31/09 (0.10)$ Stock price data as of November 7, 2014 Yes Hurdle # 8: Stability in Growth of Earnings No Hurdle # 5: Total Debt less than Book Value Yes Hurdle # 6: Current Ratio of Two or More Yes Hurdle # 7: Earnings Growth of 7% or Higher over past 5 years No Hurdle # 3: A Dividend Yield of 1/2 the Yield on 10 Year Treasury Yes Hurdle # 4: A Stock Price less than 1.5 BV No RPC INC. (RES) Ben Graham Analysis Hurdle # 1: An Earnings to Price Yield of 2X the Yield on 10 Year Treasury No Hurdle # 2: A P/E Ratio Down to 1/2 of the Stocks Highest in 5 Yrs

- 39. BURKENROAD REPORTS RATING SYSTEM MARKET OUTPERFORM: This rating indicates that we believe forces are in place that would enable this company's stock to produce returns in excess of the stock market averages over the next 12 months. MARKET PERFORM: This rating indicates that we believe the investment returns from this company's stock will be in line with those produced by the stock market averages over the next 12 months. MARKET UNDERPERFORM: This rating indicates that while this investment may have positive attributes, we believe an investment in this company will produce subpar returns over the next 12 months. BURKENROAD REPORTS CALCULATIONS CPFS is calculated using operating cash flows excluding working capital changes. All amounts are as of the date of the report as reported by Bloomberg or Yahoo Finance unless otherwise noted. Betas are collected from Bloomberg. Enterprise value is based on the equity market cap as of the report date, adjusted for long‐ term debt, cash, & short‐term investments reported on the most recent quarterly report date. 12‐month Stock Performance is calculated using an ending price as of the report date. The stock performance includes the 12‐month dividend yield. 2014‐2015 COVERAGE UNIVERSE Amerisafe Inc. (AMSF) Bristow Group Inc. (BRS) The First Bancshares (FBMS) CalIon Petroleum Company (CPE) Cal‐Maine Foods Inc. (CALM) Carbo Ceramics Inc. (CRR) Cash America International Inc. (CSH) Conn's Inc. (CONN) Crown Crafts Inc. (CRWS) Cyberonics Incorporated (CYBX) Denbury Resources Inc. (DNR) EastGroup Properties Inc. (EGP) Era Group Inc. (ERA) Evolution Petroleum Corp. (EPM) Globalstar (GSAT) Gulf Island Fabrication Inc. (GIFI) Hibbett Sports (HIBB) Hornbeck Offshore Services Inc. (HOS) IBERIABANK Corp. (IBKC) ION Geophysical Corp. (IO) Key Energy Services (KEG) Marine Products Corp. (MPX) MidSouth Bancorp Inc. (MSL) Newpark Resources Inc. (NR) PetroQuest Energy Inc. (PQ) Popeyes Louisiana Kitchen (PLKI) Pool Corporation (POOL) Powell Industries Inc. (POWL) Rollins Incorporated (ROL) RPC Incorporated (RES) Ruth’s Hospitality Group Inc. (RUTH) Sanderson Farms Inc. (SAFM) SEACOR Holdings Inc. (CKH) Sharps Compliance Inc. (SMED) Stone Energy Corp. (SGY) Sunoco LP (SUN) Superior Energy Services Inc. (SPN) Team Incorporated (TISI) Vaalco Energy Inc. (EGY) Willbros Group Inc. (WG) PETER RICCHIUTI Director of Research Founder of Burkenroad Reports Peter.Ricchiuti@tulane.edu ANTHONY WOOD Senior Director of Accounting Awood11@tulane.edu JERRY DICOLO DAVID DOWTY ELLIOTT EDWARDS Associate Directors of Research BURKENROAD REPORTS Tulane University New Orleans, LA 70118‐5669 (504) 862‐8489 (504) 865‐5430 Fax