Q2FY15: Wipro consolidated sales grows 5%

•

0 gostou•214 visualizações

On sequential basis, for the quarter ended September 2014, Wipro consolidated sales grew 5% to 11816.00 crore. OPM fell 150 basis points to 22.1% which saw OP falling 2% to `2613.70 crore.

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (20)

Semelhante a Q2FY15: Wipro consolidated sales grows 5%

Semelhante a Q2FY15: Wipro consolidated sales grows 5% (20)

Mais de IndiaNotes.com

Mais de IndiaNotes.com (20)

Último

Último (20)

Q2FY15: Wipro consolidated sales grows 5%

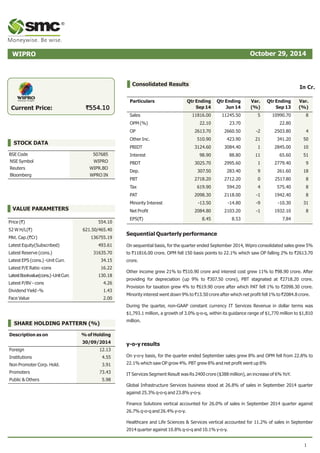

- 1. WIPRO Current Price: VALUE PARAMETERS Price (`) 554.10 52 W H/L( ` ) 621.50/465.40 Mkt. Cap.( ` Cr) 136755.19 Latest Equity(Subscribed) 493.61 Latest Reserve (cons.) 31635.70 Latest EPS (cons.) -Unit Curr. 34.15 Latest P/E Ratio -cons 16.22 Latest Bookvalue(cons.) -Unit Curr. 130.18 Latest P/BV - cons 4.26 Dividend Yield -% 1.43 Face Value 2.00 `554.10 STOCK DATA BSE Code 507685 NSE Symbol WIPRO Reuters WIPR.BO Bloomberg WPRO IN SHARE HOLDING PATTERN (%) Description as on % of Holding 30/09/2014 Foreign 12.13 Institutions 4.55 Non Promoter Corp. Hold. 3.91 Promoters 73.43 Public & Others 5.98 Consolidated Results In Cr. Particulars Qtr Ending Qtr Ending Var. Qtr Ending Var. Sep 14 Jun 14 (%) 13 (%) Sales 11816.00 11245.50 5 10990.70 8 OPM (%) 22.10 23.70 22.80 OP 2613.70 2660.50 -2 2503.80 4 Other Inc. 510.90 423.90 21 341.20 50 PBIDT 3124.60 3084.40 1 2845.00 10 Interest 98.90 88.80 11 65.60 51 PBDT 3025.70 2995.60 1 2779.40 9 Dep. 307.50 283.40 9 261.60 18 PBT 2718.20 2712.20 0 2517.80 8 Tax 619.90 594.20 4 575.40 8 PAT 2098.30 2118.00 -1 1942.40 8 Minority Interest -13.50 -14.80 -9 -10.30 31 Net Profit 2084.80 2103.20 -1 1932.10 8 EPS(`) 8.45 8.53 7.84 Sequential Quarterly performance On sequential basis, for the quarter ended September 2014, Wipro consolidated sales grew 5% to ` 11816.00 crore. OPM fell 150 basis points to 22.1% which saw OP falling 2% to `2613.70 crore. Other income grew 21% to ` 510.90 crore and interest cost grew 11% to ` 98.90 crore. After providing for depreciation (up 9% to ` 307.50 crore), PBT stagnated at ` 2718.20 crore. Provision for taxation grew 4% to ` 619.90 crore after which PAT fell 1% to ` 2098.30 crore. Minority interest went down 9% to ` 13.50 crore after which net profit fell 1% to ` 2084.8 crore. During the quarter, non-GAAP constant currency IT Services Revenue in dollar terms was $1,793.1 million, a growth of 3.0% q-o-q, within its guidance range of $1,770 million to $1,810 million. y-o-y results On y-o-y basis, for the quarter ended September sales grew 8% and OPM fell from 22.8% to 22.1% which saw OP grow 4%. PBT grew 8% and net profit went up 8% IT Services Segment Result was Rs 2400 crore ($388 million), an increase of 6% YoY. Global Infrastructure Services business stood at 26.8% of sales in September 2014 quarter against 25.3% q-o-q and 23.8% y-o-y. Finance Solutions vertical accounted for 26.0% of sales in September 2014 quarter against 26.7% q-o-q and 26.4% y-o-y. Healthcare and Life Sciences & Services vertical accounted for 11.2% of sales in September 2014 quarter against 10.8% q-o-q and 10.1% y-o-y. 1 Sep ® October 29, 2014

- 2. Americas accounted for 51.0% of sales in September 2014 quarter against 49.8% q-o-q and 49.8% y-o-y. Europe accounted for 527.8% of sales in September 2014 quarter against 29.6% q-o-q and 28.9% y-o-y. India & Middle East business accounted for 9.2% of sales in September 2014 quarter against 9.1% q-o-q and 8.3% y-o-y. APAC and Other Emerging Markets business accounted for 12.0% of sales in September 2014 quarter against 11.5% q-o-q and 13.0% y-o-y. $ 100 million clients stood at 10 in September 2014 quarter against 10 q-o-q and 10 y-o-y. $ 75 million clients stood at 15 in September 2014 quarter against 14 q-o-q and 15 y-o-y. $ 1 million clients stood at 524 in September 2014 quarter against 511 q-o-q and 487 y-o-y. Outlook for the Quarter ending December 31, 2014 The management expects Revenues from its IT Services business to be in the range of $ 1,808 million to $ 1,842 million*. *Guidance is based on the following exchange rates: GBP/USD at 1.65, Euro/USD at 1.31, AUD/USD at 0.92, USD/INR at 60.76 and USD/CAD at 1.10 The IT Services segment had a headcount of 154,297 as of September 2014. It added Over 6800 employees. Other Development The company added 50 new customers during the quarter. Globally it won contracts from clients like CLK Enerji (Turkey's largest electricity distribution and retail sales company), Philip Morris International, British Petroleum. During the quarter, Wipro completed the transaction announced on July 18, 2014 with ATCO Limited and the financials of the entities taken over were consolidated from August 2014. The company sees immense opportunity in Digital field. Wipro Digital has been chosen to partner in the digital transformation journey of a leading UK insurance firm, which is poised to re-imagine all aspects of its Life Insurance customer proposition, from engagement to servicing to product innovation. As a partner of choice, Wipro will establish a digital capability which offers a broad based human-centric design proposition, with an architecture directly focused on addressing core customer needs. While the industry landscape is still undergoing change, wipro sees multiple opportunity spaces for growth and gaining market share. It continues to execute to its stated strategy of leveraging platforms for non-linear growth and creating differentiated solutions around the new technology paradigms. In Q2, the company continued to build on leadership position in Infrastructure Services and continued the momentum of deal wins. 2 ®

- 3. ® SMC Research also available on Reuters Corporate Office: 11/6B, Shanti Chamber, Pusa Road, New Delhi - 110005 Tel: +91-11-30111000 www.smcindiaonline.com During the quarter, the benefits of rupee depreciation were negated by the US Dollar's appreciation against other major currencies. The company is seeing positive sentiment in India with the confidence that the Government is focused on driving an agenda of growth. Business leaders in the US continue to exhibit increased confidence on growth prospects. US Based clients are increasingly looking to drive business value from their technology investments. Management comments Azim Premji, Chairman of Wipro, said, "Business leaders in the US continue to exhibit increased confidence on growth prospects. Clients are increasingly looking to drive business value from their technology investments. We are seeing positive sentiment in India with the confidence that the Government is focused on driving an agenda of growth. The company sees good momentum in large deals. It expects H2FY15 (October-March) to be better than H1FY15. According to him, the current demand environment is better than last year. Mumbai Office: Dheeraj Sagar, 1st Floor, Opp. Goregaon sports club, link road Malad (West), Mumbai - 400064 Tel: 91-22-67341600, Fax: 91-22-28805606 E-mail: researchfeedback@smcindiaonline.com Kolkata Office: 18, Rabindra Sarani, "Poddar Court", Gate No. 4, 4th Floor, Kolkata - 700001 Tel: 91-33-39847000, Fax: 91-33-39847004 ® SMC Global Securities Limited is proposing, subject to receipt of requisite approvals, market conditions and other considerations, a further public offering of its equity shares and has filed the Draft Red Herring Prospectus with the Securities and Exchange Board of India (“SEBI”) and the Stock Exchanges. The Draft Red Herring Prospectus is available on the website of SEBI at www.sebi.gov.in and on the websites of the Book Running Lead Manager i.e., ICICI Securities Limited at www.icicisecurities.com and the Co- Book Running Lead Manager i.e., Elara Capital (India) Private Limited at www.elaracapital.com . Investors should note that investment in equity shares involves a high degree of risk and for details relating to the same, please see the section titled “Risk Factors” of the aforementioned offer document. DISCLAMIER: This report is for the personal information of the authorized recipient and doesn't construe to be any investment, legal or taxation advice to you. It is only for private circulation and use .The report is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. No action is solicited on the basis of the contents of the report. The report should not be reproduced or redistributed to any other person(s)in any form without prior written permission of the SMC. The contents of this material are general and are neither comprehensive nor inclusive. Neither SMC nor any of its affiliates, associates, representatives, directors or employees shall be responsible for any loss or damage that may arise to any person due to any action taken on the basis of this report. It does not constitute personal recommendations or take into account the particular investment objectives, financial situations or needs of an individual client or a corporate/s or any entity/s. All investments involve risk and past performance doesn't guarantee future results. The value of, and income from investments may vary because of the changes in the macro and micro factors given at a certain period of time. The person should use his/her own judgment while taking investment decisions. Please note that we and our affiliates, officers, directors, and employees, including persons involved in the preparation or issuance if this material;(a) from time to time, may have long or short positions in, and buy or sell the commodities thereof, mentioned here in or (b) be engaged in any other transaction involving such commodities and earn brokerage or other compensation or act as a market maker in the commodities discussed herein (c) may have any other potential conflict of interest with respect to any recommendation and related information and opinions. All disputes shall be subject to the exclusive jurisdiction of Delhi High court. 3