Motilal Oswal finds investor perception improving on Crompton Greaves; Buy

•

1 like•322 views

Motilal Oswal recommends Crompton Greaves, investor perception improves as promoter exits Consumer business

Recommended

More Related Content

Viewers also liked

Viewers also liked (9)

More from IndiaNotes.com

More from IndiaNotes.com (20)

Recently uploaded

Recently uploaded (20)

Motilal Oswal finds investor perception improving on Crompton Greaves; Buy

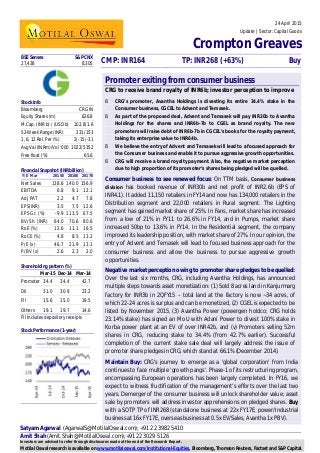

- 1. Satyam Agarwal (AgarwalS@MotilalOswal.com); +91 22 3982 5410 Amit Shah (Amit.Shah@MotilalOswal.com);+91 22 3029 5126 24 April 2015 Update | Sector: Capital Goods Crompton Greaves CMP: INR164 TP: INR268 (+63%) Buy Investors are advised to refer through disclosures made at the end of the Research Report. Motilal Oswal research is available on www.motilaloswal.com/Institutional-Equities, Bloomberg, Thomson Reuters, Factset and S&P Capital. Promoter exiting from consumer business CRG to receive brand royalty of INR6b; investor perception to improve § CRG’s promoter, Avantha Holdings is divesting its entire 34.4% stake in the Consumer business, CGCEL to Advent and Temasek. § As part of the proposed deal, Advent and Temasek will pay INR20b to Avantha Holdings for the shares and INR6b-7b to CGEL as brand royalty. The new promoters will raise debt of INR6b-7b in CGCEL’s books for the royalty payment, taking its enterprise value to INR64b. § We believe the entry of Advent and Temasek will lead to a focused approach for the Consumer business and enable it to pursue aggressive growth opportunities. § CRG will receive a brand royalty payment. Also, the negative market perception due to high proportion of its promoter’s shares being pledged will be quelled. Consumer business to see renewed focus: On TTM basis, Consumer business division has booked revenue of INR30b and net profit of INR2.6b (EPS of INR4.1). It added 11,150 retailers in FY14 and now has 134,000 retailers in the Distribution segment and 22,000 retailers in Rural segment. The Lighting segment has gained market share of 25%. In Fans, market share has increased from a low of 21% in FY11 to 26.6% in FY14, and in Pumps, market share increased 50bp to 13.6% in FY14. In the Residential segment, the company improved its leadership position, with market share of 27%. In our opinion, the entry of Advent and Temasek will lead to focused business approach for the consumer business and allow the business to pursue aggressive growth opportunities. Negative market perception owing to promoter share pledges to be quelled: Over the last six months, CRG, including Avantha Holdings, has announced multiple steps towards asset monetization: (1) Sold 8 acres land in Kanjurmarg factory for INR3b in 2QFY15 – total land at the factory is now ~34 acres, of which 22-24 acres is surplus and can be monetized, (2) CGEL is expected to be listed by November 2015, (3) Avantha Power (powergen holdco; CRG holds 23.14% stake) has signed an MoU with Adani Power to divest 100% stake in Korba power plant at an EV of over INR42b, and (v) Promoters selling 52m shares in CRG, reducing stake to 34.4% (from 42.7% earlier). Successful completion of the current stake sale deal will largely address the issue of promoter share pledges in CRG, which stand at 66.1% (December 2014). Maintain Buy: CRG's journey to emerge as a 'global corporation' from India continues to face multiple 'growth pangs'. Phase-1 of its restructuring program, encompassing European operations has been largely completed. In FY16, we expect to witness fructification of the management’s efforts over the last two years. Demerger of the consumer business will unlock shareholder value; asset sale by promoters will address investor apprehensions on pledged shares. Buy with a SOTP TP of INR268 (standalone business at 22x FY17E, power/Industrial business at 16x FY17E, overseas business at 0.5x EV/Sales, Avantha 1x PBV). BSE Sensex S&P CNX 27,438 8,305 Stock Info Bloomberg CRG IN Equity Shares (m) 626.8 M.Cap. (INR b) / (USD b) 102.8/1.6 52-Week Range (INR) 231/153 1, 6, 12 Rel. Per (%) 2/-15/-31 Avg Val (INRm)/Vol ‘000 1022/5352 Free float (%) 65.6 Financial Snapshot (INR billion) Y/E Mar 2015E 2016E 2017E Net Sales 138.6 140.0 156.9 EBITDA 6.8 9.1 12.1 Adj PAT 2.2 4.7 7.8 EPS(INR) 3.5 7.5 12.6 EPS Gr. (%) -9.9 113.5 67.5 BV/Sh. (INR) 64.0 70.6 80.6 RoE (%) 12.6 11.1 16.5 RoCE (%) 4.8 8.5 13.2 P/E (x) 46.7 21.9 13.1 P/BV (x) 2.6 2.3 2.0 Shareholding pattern (%) Mar-15 Dec-14 Mar-14 Promoter 34.4 34.4 42.7 DII 31.0 30.9 23.2 FII 15.6 15.0 19.5 Others 19.1 19.7 14.6 FII Includes depository receipts Stock Performance (1-year)

- 2. Crompton Greaves 24 April 2015 2 Avantha to exit from CGCEL In a press release filed with the BSE, CRG has stated that Avantha Holdings proposes to divest its entire 34.4% stake in Crompton Greaves Consumer Electricals Limited (CGCEL) to one or more SPVs managed by Advent and Temasek for INR20b. Advent and Temasek will raise debt of INR6b-7b on CGCEL’s books, which will be paid to CRG for allowing CGCEL to use the Crompton brand, taking the enterprise value of CGCEL to INR64b. Consumer business to see renewed focus On TTM basis, CGEL has booked revenue of INR30b and net profit of INR2.6b (EPS of INR4.1). It added 11,150 retailers in FY14 and now has 134,000 retailers in the Distribution segment and 22,000 retailers in Rural segment. The Lighting segment has gained market share of 25%. In Fans, market share has increased from a low of 21% in FY11 to 26.6% in FY14, and in Pumps, market share increased 50bp to 13.6% in FY14. In the Residential segment, the company improved its leadership position, with market share of 27%. In our opinion, the entry of Advent and Temasek will lead to focused business approach for the consumer business and allow the business to pursue aggressive growth opportunities. Exhibit 1: Consumer business financials (INR m) 3QFY14 4QFY14 FY14 1QFY15 2QFY15 3QFY15 Revenues 6,620 7,599 28,985 8,611 7,431 7,232 PBT 750 897 3,329 1,077 893 860 PAT 534 638 2,367 732 608 586 PAT Margin 8.1% 8.4% 8.2% 8.5% 8.2% 8.1% EPS 0.85 1.02 3.78 1.17 0.97 0.93 Source: MOSL, Company Exhibit 2: CRG has outperformed industry growth rates in each of the last three years FY12 FY13 FY14 Industry CRG Industry CRG Industry CRG Fans -2% 2% 15% 22% 10% 15% Lighting 12% 17% 12% 13% 2% 12% Pumps -8% -4% 6% 26% -10% flat Source: MOSL, Company Exhibit 3: Product-wise revenue and Traded Goods (INR m) Source: MOSL, Company Exhibit 4: Ad-spends witnessing an increased trend (INR m) Source: MOSL, Company 5,790 12,848 9,010 1,817 3,555 4,617 4,980 1,383 Power driven pumps Electric fans andventillation equipments Electric Lamps Appliances Revenues (INR m) Cost of Purchase Goods (INR m) 156 211 256 227 345 474 691 766 1.6 1.9 1.9 1.4 1.7 2.2 2.7 2.7 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 AdSpend (INR M) Ad(% of Consumer Rev)

- 3. Crompton Greaves 24 April 2015 3 Exhibit 5: Consumer business product-wise revenue (INR m) FY09 FY10 FY11 FY12 FY13 FY14 Fans and Ventilation equipments 6,032 7,645 9,097 9,122 11,138 12,848 Electric Lamps 4,636 4,923 5,703 6,667 7,689 9,010 Power driven Pumps 2,794 3,854 5,217 5,019 5,869 5,790 Appliances 210 683 969 1,211 2,120 1,817 Total 13,672 17,105 20,986 22,019 26,816 29,465 Source: MOSL, Company Asset monetization to drive value unlocking CRG, including Avantha Holdings, has recently announced multiple steps towards asset monetization, and several of the transactions are in advanced stages. n Land sale at Kanjurmarg: CRG has sold 8 acres of land at its Kanjurmarg factory for INR3b in 2QFY15. We understand that the total land at the factory is now ~34 acres, of which 22-24 acres is surplus and can be monetized. n Consumer business demerger and now, promoter stake sale: The promoter, Avantha Holdings proposes to divest its entire 34.4% in CGCEL to one or more SPVs managed by Advent and Temasek for INR20b. n MoU for sale of Korba power plant: Avantha Power (powergen holdco; CRG’s stake 23.14%) has signed an MoU with Adani Power to divest 100% stake in Korba power plant. The enterprise value is over INR42b. The first unit of 600MW at Korba was commissioned in March 2014. n Jhabua Power sale discussions with Tata Power-ICICI Ventures consortium: Media articles state that there are serious negotiations to divest 1.3GW of Jhabua Power with Tata Power-ICICI Ventures consortium. Avantha Power is executing two power projects at Korba and Jhabua (capacity of 2.5GW) and another 1.3GW is under planning at Gujarat. The above transactions will largely complete the exit of Avantha Group from powergen business. Avantha Power had raised USD125m from KKR (stake ~19%) through structured instruments. Successful completion will largely address the share pledge issue n Increased investments in Avantha Power had led to higher promoter share pledge in CRG at 66.1% (December 2014). Besides, continued need for fund infusion has remained an important area of discomfort for investors. n CRG had invested INR2.3b as equity in Avantha Power (stake of 23.1%), and thus the direct financial commitment was not meaningful. n Successful exit from the powergen business and stake sale in Consumer business will address liquidity constraints and largely resolve the issue of pledged shares, in our opinion. Exhibit 6: CRG – promoter shares pledged (%) Source: MOSL, Company 5.1 34.7 47.9 61.6 64.2 68.3 54.3 57.5 59.2 61.4 66.1 1QFY13 2QFY13 3QFY13 4QFY13 1QFY14 2QFY14 3QFY14 4QFY14 1QFY15 2QFY15 3QFY15

- 4. Crompton Greaves 24 April 2015 4 Financials and valuations Income statement (INR Million) Y/E March 2010 2011 2012 2013 2014 2015E 2016E 2017E Net Sales 91,409 100,051 112,486 120,944 134,806 138,570 140,008 156,932 Change (%) 4.6 9.5 12.4 7.5 11.5 2.8 1.0 12.1 Raw Materials 57,966 64,980 76,850 83,461 91,353 94,431 98,302 107,845 Staff Cost 11,131 11,811 14,662 17,405 19,521 19,400 18,560 19,416 Other Mfg. Expenses 9,542 9,822 12,937 16,247 17,113 17,911 14,035 17,549 EBITDA 12,770 13,438 8,036 3,832 6,820 6,828 9,112 12,121 % of Net Sales 14.0 13.4 7.1 3.2 5.1 4.9 6.5 7.7 Depreciation 1,551 1,936 2,600 2,029 2,621 2,642 2,547 2,669 Interest 428 352 567 955 1,366 930 530 454 Other Income 1,100 1,142 628 1,000 2,115 1,440 1,233 1,458 EO Items (as rep.) 352 -381 0 -1,207 0 2,675 0 0 PBT 12,243 11,910 5,497 640 4,947 7,371 7,268 10,456 Tax 3,650 3,100 1,821 1,009 2,361 2,534 2,605 2,623 Rate (%) 29.8 26.0 33.1 157.6 47.7 34.4 35.8 25.1 Reported PAT 8,593 8,810 3,676 -369 2,587 4,837 4,663 7,834 Extra-ordinary Inc.(net) 352 -381 0 -2,287 0 2,675 0 0 Adjusted PAT 8,241 9,191 3,676 1,918 2,587 2,162 4,663 7,834 Minority Int 6.0 76.5 59.9 7.3 -143.4 38.7 34.0 34.0 Consolidated PAT 8,247 9,268 3,736 1,927 2,443 2,200 4,697 7,868 Change (%) 47.3 12.4 -59.7 -48.4 26.8 -9.9 113.5 67.5 Balance Sheet (INR Million) Y/E March 2010 2011 2012 2013 2014 2015E 2016E 2017E Share Capital 1,283 1,283 1,283 1,283 1,254 1,254 1,254 1,254 Reserves 23,760 31,464 34,826 34,332 35,192 38,876 42,990 49,243 Net Worth 25,043 32,747 36,109 35,615 36,446 40,130 44,244 50,496 Loans 5,010 3,955 9,849 18,515 21,930 19,843 16,126 14,958 Deffered Tax Liability 49 160 -122 -1,681 -1,532 -1,426 -1,162 -1,162 Minority Interest 43 157 157 95 118 118 118 118 Capital Employed 30,145 37,019 45,992 52,544 56,962 58,665 59,325 64,410 Gross Fixed Assets 29,858 37,805 44,087 53,424 59,233 59,198 56,393 57,733 Less: Depreciation 17,234 19,490 23,005 24,726 26,825 28,915 29,349 32,290 Net Fixed Assets 12,623 18,315 21,083 28,699 32,408 30,284 27,044 25,443 Capital WIP 1,137 1,102 1,493 1,965 2,184 2,677 5,473 7,973 Investments 5,536 6,747 7,864 7,907 2,989 8,948 12,892 19,086 Curr. Assets 41,018 45,646 55,343 59,807 69,168 66,798 63,978 70,360 Inventory 10,412 11,893 12,233 16,367 16,714 17,307 16,823 18,416 Debtors 21,463 25,427 31,432 31,605 35,913 36,748 36,360 40,172 Cash & Bank Balance 6,688 2,984 4,976 5,834 8,150 4,679 2,998 3,343 Loans & Advances 2,455 5,342 6,702 6,002 8,392 8,063 7,798 8,430 Current Liab. & Prov. 30,170 34,790 40,186 45,834 49,787 50,043 50,061 58,451 Creditors 16,098 18,585 21,076 24,618 27,737 27,310 27,904 31,876 Other Liabilities 10,469 12,148 15,319 16,994 17,985 18,597 18,155 22,275 Provisions 3,603 4,058 3,791 4,222 4,064 4,136 4,002 4,300 Net Current Assets 10,849 10,856 15,157 13,973 19,381 16,755 13,917 11,909 Application of Funds 30,145 37,020 45,993 52,544 56,961 58,665 59,325 64,410 E: MOSL Estimates; Consolidated Financials

- 5. Crompton Greaves 24 April 2015 5 Financials and valuations Ratios Y/E March 2010 2011 2012 2013 2014 2015E 2016E 2017E Standalone EPS 9.0 10.8 7.9 6.9 8.3 8.2 10.0 12.9 Consolidated EPS 13.1 14.8 6.0 3.1 3.9 3.5 7.5 12.6 Growth (%) 46.5 12.5 -59.7 -48.4 26.8 -9.9 113.5 67.5 Cash EPS 15.3 17.3 9.8 6.2 8.3 7.7 11.5 16.8 Book Value 39.0 51.0 56.3 55.5 58.2 64.0 70.6 80.6 DPS 1.3 2.2 1.4 1.2 0.8 2.1 1.7 2.2 Payout (incl. Div. Tax.) 15.3 23.7 20.7 20.1 11.3 20.0 20.0 20.0 Valuation (x) P/E (standalone) 22.0 21.7 22.7 19.9 16.4 12.7 P/E (consolidated) 12.5 27.5 48.5 46.7 21.9 13.1 Cash P/E 18.4 19.4 16.7 14.1 11.3 EV/EBITDA 13.6 19.4 16.4 11.6 8.1 EV/Sales 1.0 1.0 0.8 0.8 0.6 Price/Book Value 5.1 3.0 3.2 2.6 2.3 2.0 Dividend Yield (%) 0.8 0.9 0.5 1.3 1.0 1.3 Profitability Ratios (%) RoE 39.6 30.5 10.7 -1.0 7.2 12.6 11.1 16.5 RoCE 30.9 28.1 9.8 2.8 6.0 4.8 8.5 13.2 Turnover Ratios Debtors (Days) 42 93 102 95 97 97 95 93 Inventory (Days) 42 43 40 49 45 46 44 43 Creditors. (Days) 64 68 68 74 75 72 73 74 Asset Turnover (x) 3.0 2.7 2.4 2.3 2.4 2.4 2.4 2.4 Leverage Ratio Debt/Equity (x) 0 -0.1 0.0 0.2 0.4 0.2 0.1 -0.1 Cash Flow Statement (INR Million) Y/E March 2010 2011 2012 2013 2014 2015E 2016E 2017E PBT before EO Items 11,891 12,291 5,497 1,848 4,947 4,696 7,268 10,456 Add : Depreciation 1,551 1,936 2,600 2,029 2,621 2,642 2,547 2,669 Interest 428 352 567 955 1,366 930 530 454 Less : Direct Taxes Paid 3,650 3,100 2,495 2,177 2,211 2,428 2,341 2,623 (Inc)/Dec in WC -125 -3,715 -2,310 2,046 -3,092 -844 1,156 2,353 CF from Operations 10,094 7,765 3,859 4,701 3,631 4,996 9,160 13,310 EO Income 352 -381 0 -1,207 0 2,675 0 0 CF from Oper. incl. EO Items 10,446 7,384 3,859 3,494 3,631 7,671 9,160 13,310 (Inc)/Dec in FA -1,526 -7,593 -5,758 -10,117 -6,550 -1,012 -2,102 -3,568 (Pur)/Sale of Investments -3,864 -1,211 -1,117 -43 4,919 -5,960 -3,943 -6,194 CF from Investments -5,389 -8,805 -6,875 -10,160 -1,631 -6,971 -6,046 -9,762 (Inc)/Dec in Net Worth -481 767 725 709 -1,147 415 702 34 (Inc)/Dec in Debt -2,173 -1,055 5,894 8,666 3,415 -2,087 -3,718 -1,168 Less : Interest Paid 428 352 567 955 1,366 930 530 454 Dividend Paid 944 1,644 1,044 897 587 1,568 1,251 1,615 CF from Fin. Activity -4,025 -2,284 5,008 7,524 316 -4,170 -4,796 -3,203 Inc/Dec of Cash 1,032 -3,705 1,992 857 2,316 -3,470 -1,682 345 Add: Beginning Balance 5,656 6,688 2,984 4,976 5,834 8,150 4,679 2,998 Closing Balance 6,688 2,988 4,981 5,833 8,150 4,679 2,998 3,343 E: MOSL Estimates

- 6. Crompton Greaves 24 April 2015 6 Disclosures This document has been prepared by Motilal Oswal Securities Limited (hereinafter referred to as Most) to provide information about the company(ies) and/sector(s), if any, covered in the report and may be distributed by it and/or its affiliated company(ies). This report is for personal information of the selected recipient/s and does not construe to be any investment, legal or taxation advice to you. This research report does not constitute an offer, invitation or inducement to invest in securities or other investments and Motilal Oswal Securities Limited (hereinafter referred as MOSt) is not soliciting any action based upon it. This report is not for public distribution and has been furnished to you solely for your general information and should not be reproduced or redistributed to any other person in any form. This report does not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual clients. Before acting on any advice or recommendation in this material, investors should consider whether it is suitable for their particular circumstances and, if necessary, seek professional advice. The price and value of the investments referred to in this material and the income from them may go down as well as up, and investors may realize losses on any investments. Past performance is not a guide for future performance, future returns are not guaranteed and a loss of original capital may occur. MOSt and its affiliates are a full-service, integrated investment banking, investment management, brokerage and financing group. We and our affiliates have investment banking and other business relationships with a some companies covered by our Research Department. Our research professionals may provide input into our investment banking and other business selection processes. Investors should assume that MOSt and/or its affiliates are seeking or will seek investment banking or other business from the company or companies that are the subject of this material and that the research professionals who were involved in preparing this material may educate investors on investments in such business. The research professionals responsible for the preparation of this document may interact with trading desk personnel, sales personnel and other parties for the purpose of gathering, applying and interpreting information. Our research professionals are paid on the profitability of MOSt which may include earnings from investment banking and other business. MOSt generally prohibits its analysts, persons reporting to analysts, and members of their households from maintaining a financial interest in the securities or derivatives of any companies that the analysts cover. Additionally, MOSt generally prohibits its analysts and persons reporting to analysts from serving as an officer, director, or advisory board member of any companies that the analysts cover. Our salespeople, traders, and other professionals or affiliates may provide oral or written market commentary or trading strategies to our clients that reflect opinions that are contrary to the opinions expressed herein, and our proprietary trading and investing businesses may make investment decisions that are inconsistent with the recommendations expressed herein. In reviewing these materials, you should be aware that any or all of the foregoing among other things, may give rise to real or potential conflicts of interest. MOSt and its affiliated company(ies), their directors and employees and their relatives may; (a) from time to time, have a long or short position in, act as principal in, and buy or sell the securities or derivatives thereof of companies mentioned herein. (b) be engaged in any other transaction involving such securities and earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions.; however the same shall have no bearing whatsoever on the specific recommendations made by the analyst(s), as the recommendations made by the analyst(s) are completely independent of the views of the affiliates of MOSt even though there might exist an inherent conflict of interest in some of the stocks mentioned in the research report Reports based on technical and derivative analysis center on studying charts company's price movement, outstanding positions and trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's fundamental analysis. In addition MOST has different business segments / Divisions with independent research separated by Chinese walls catering to different set of customers having various objectives, risk profiles, investment horizon, etc, and therefore may at times have different contrary views on stocks sectors and markets. Unauthorized disclosure, use, dissemination or copying (either whole or partial) of this information, is prohibited. The person accessing this information specifically agrees to exempt MOSt or any of its affiliates or employees from, any and all responsibility/liability arising from such misuse and agrees not to hold MOSt or any of its affiliates or employees responsible for any such misuse and further agrees to hold MOSt or any of its affiliates or employees free and harmless from all losses, costs, damages, expenses that may be suffered by the person accessing this information due to any errors and delays. The information contained herein is based on publicly available data or other sources believed to be reliable. Any statements contained in this report attributed to a third party represent MOSt’s interpretation of the data, information and/or opinions provided by that third party either publicly or through a subscription service, and such use and interpretation have not been reviewed by the third party. This Report is not intended to be a complete statement or summary of the securities, markets or developments referred to in the document. While we would endeavor to update the information herein on reasonable basis, MOSt and/or its affiliates are under no obligation to update the information. Also there may be regulatory, compliance, or other reasons that may prevent MOSt and/or its affiliates from doing so. MOSt or any of its affiliates or employees shall not be in any way responsible and liable for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report. MOSt or any of its affiliates or employees do not provide, at any time, any express or implied warranty of any kind, regarding any matter pertaining to this report, including without limitation the implied warranties of merchantability, fitness for a particular purpose, and non-infringement. The recipients of this report should rely on their own investigations. This report is intended for distribution to institutional investors. Recipients who are not institutional investors should seek advice of their independent financial advisor prior to taking any investment decision based on this report or for any necessary explanation of its contents. Most and it’s associates may have managed or co-managed public offering of securities, may have received compensation for investment banking or merchant banking or brokerage services, may have received any compensation for products or services other than investment banking or merchant banking or brokerage services from the subject company in the past 12 months. Most and it’s associates have not received any compensation or other benefits from the subject company or third party in connection with the research report. Subject Company may have been a client of Most or its associates during twelve months preceding the date of distribution of the research report MOSt and/or its affiliates and/or employees may have interests/positions, financial or otherwise of over 1 % at the end of the month immediately preceding the date of publication of the research in the securities mentioned in this report. To enhance transparency, MOSt has incorporated a Disclosure of Interest Statement in this document. This should, however, not be treated as endorsement of the views expressed in the report. Motilal Oswal Securities Limited is under the process of seeking registration under SEBI (Research Analyst) Regulations, 2014. There are no material disciplinary action that been taken by any regulatory authority impacting equity research analysis activities Analyst Certification The views expressed in this research report accurately reflect the personal views of the analyst(s) about the subject securities or issues, and no part of the compensation of the research analyst(s) was, is, or will be directly or indirectly related to the specific recommendations and views expressed by research analyst(s) in this report. The research analysts, strategists, or research associates principally responsible for preparation of MOSt research receive compensation based upon various factors, including quality of research, investor client feedback, stock picking, competitive factors and firm revenues Disclosure of Interest Statement CROMPTON GREAVES § Analyst ownership of the stock No § Served as an officer, director or employee No Regional Disclosures (outside India) This report is not directed or intended for distribution to or use by any person or entity resident in a state, country or any jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject MOSt & its group companies to registration or licensing requirements within such jurisdictions. For U.S. Motilal Oswal Securities Limited (MOSL) is not a registered broker - dealer under the U.S. Securities Exchange Act of 1934, as amended (the"1934 act") and under applicable state laws in the United States. In addition MOSL is not a registered investment adviser under the U.S. Investment Advisers Act of 1940, as amended (the "Advisers Act" and together with the 1934 Act, the "Acts), and under applicable state laws in the United States. Accordingly, in the absence of specific exemption under the Acts, any brokerage and investment services provided by MOSL, including the products and services described herein are not available to or intended for U.S. persons. This report is intended for distribution only to "Major Institutional Investors" as defined by Rule 15a-6(b)(4) of the Exchange Act and interpretations thereof by SEC (henceforth referred to as "major institutional investors"). This document must not be acted on or relied on by persons who are not major institutional investors. Any investment or investment activity to which this document relates is only available to major institutional investors and will be engaged in only with major institutional investors. In reliance on the exemption from registration provided by Rule 15a-6 of the U.S. Securities Exchange Act of 1934, as amended (the "Exchange Act") and interpretations thereof by the U.S. Securities and Exchange Commission ("SEC") in order to conduct business with Institutional Investors based in the U.S., MOSL has entered into a chaperoning agreement with a U.S. registered broker-dealer, Motilal Oswal Securities International Private Limited. ("MOSIPL"). Any business interaction pursuant to this report will have to be executed within the provisions of this chaperoning agreement. The Research Analysts contributing to the report may not be registered /qualified as research analyst with FINRA. Such research analyst may not be associated persons of the U.S. registered broker-dealer, MOSIPL, and therefore, may not be subject to NASD rule 2711 and NYSE Rule 472 restrictions on communication with a subject company, public appearances and trading securities held by a research analyst account. For Singapore Motilal Oswal Capital Markets Singapore Pte Limited is acting as an exempt financial advisor under section 23(1)(f) of the Financial Advisers Act(FAA) read with regulation 17(1)(d) of the Financial Advisors Regulations and is a subsidiary of Motilal Oswal Securities Limited in India. This research is distributed in Singapore by Motilal Oswal Capital Markets Singapore Pte Limited and it is only directed in Singapore to accredited investors, as defined in the Financial Advisers Regulations and the Securities and Futures Act (Chapter 289), as amended from time to time. In respect of any matter arising from or in connection with the research you could contact the following representatives of Motilal Oswal Capital Markets Singapore Pte Limited: Anosh Koppikar Kadambari Balachandran Email : anosh.Koppikar@motilaloswal.com Email : kadambari.balachandran@motilaloswal.com Contact : (+65)68189232 Contact : (+65) 68189233 / 65249115 Office Address : 21 (Suite 31),16 Collyer Quay,Singapore 04931 Motilal Oswal Securities Ltd Motilal Oswal Tower, Level 9, Sayani Road, Prabhadevi, Mumbai 400 025 Phone: +91 22 3982 5500 E-mail: reports@motilaloswal.com