Recomendados

Recomendados

Mais conteúdo relacionado

Destaque

Destaque (15)

Último

Último (20)

Bab 2 bu iin

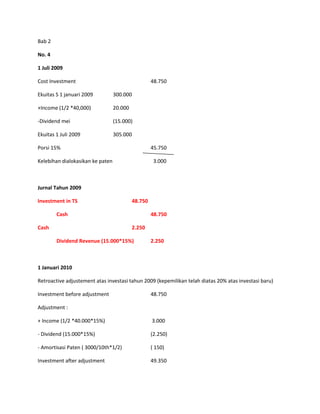

- 1. Bab 2 No. 4 1 Juli 2009 Cost Investment 48.750 Ekuitas S 1 januari 2009 300.000 +Income (1/2 *40,000) 20.000 -Dividend mei (15.000) Ekuitas 1 Juli 2009 305.000 Porsi 15% 45.750 Kelebihan dialokasikan ke paten 3.000 Jurnal Tahun 2009 Investment in TS 48.750 Cash 48.750 Cash 2.250 Dividend Revenue (15.000*15%) 2.250 1 Januari 2010 Retroactive adjustement atas investasi tahun 2009 (kepemilikan telah diatas 20% atas investasi baru) Investment before adjustment 48.750 Adjustment : + Income (1/2 *40.000*15%) 3.000 - Dividend (15.000*15%) (2.250) - Amortisasi Paten ( 3000/10th*1/2) ( 150) Investment after adjustment 49.350

- 2. Total Adjustment 600 (49.350-48.750) Cost Investment (new) 99.000 Ekuitas S 1 januari 2010 = 310.000 Porsi 30% 93.000 Selisih dialokasikan ke paten 6.000 Jurnal Tahun 2010 Investment AFS 147.750 Investment in T/S 48.750 Mencatat Reklasifikasi Investasi Cash 99.000 Investment AFS 600 Retroactive Retained Earning 600 adjustment Cash (30.000*45%) 13.500 Penerimaan Dividen Investment in S 13.500 Mei dan November Investment AFS 27.000 Pengakuan Bagian Laba Income from S (60.000*45%) 27.000 S tahun 2010 Income from S 900 Amortisasi Paten Investment AFS 900 ** atas investasi pertama 3000/10th = 300 ***atas Investasi kedua 6000/10th = 600

- 3. Kesimpulan 2009 Investment in S akhir 48.750 Income from S 2.250 2010 Investment in S akhir 160.950 Income from S 26.100