Enviar pesquisa

Carregar

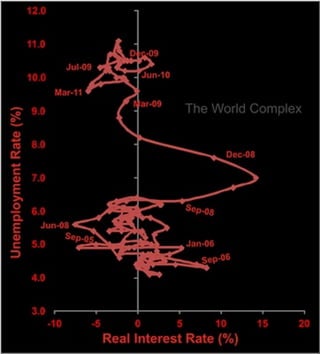

Keynes: Real rate vs Unemployment

•

0 gostou

•

183 visualizações

Fasanara Capital ltd

Seguir

Denunciar

Compartilhar

Denunciar

Compartilhar

1 de 1

Baixar agora

Baixar para ler offline

Recomendados

power

Chichol

Chichol

chichomannas

DIAPOSITIVA DE PRESENTACION AL BLOG

Mi blog

Mi blog

Reyna Mani

Magazine research 2

Magazine research 2

957820

Bibi7

Bibi7

Marc Arazi

Folder elektrisch verwarmende kookketel

Folder elektrisch verwarmende kookketel

Peter_Keunen

El hombre light

El hombre light

romycamposm

xcvbnjm,. http://3cy.us/e28b8f69

cvbnjm

cvbnjm

giannigoodday

Adrian zurita haro

Adrian zurita haro

adrianiguana

Recomendados

power

Chichol

Chichol

chichomannas

DIAPOSITIVA DE PRESENTACION AL BLOG

Mi blog

Mi blog

Reyna Mani

Magazine research 2

Magazine research 2

957820

Bibi7

Bibi7

Marc Arazi

Folder elektrisch verwarmende kookketel

Folder elektrisch verwarmende kookketel

Peter_Keunen

El hombre light

El hombre light

romycamposm

xcvbnjm,. http://3cy.us/e28b8f69

cvbnjm

cvbnjm

giannigoodday

Adrian zurita haro

Adrian zurita haro

adrianiguana

Bibi10

Bibi10

Marc Arazi

3

3

JessGelibert

Presentacion el hombre light

Presentacion el hombre light

guviarorienta

Flyer

Flyer

doublea196

dfd

Use case ex 4

Use case ex 4

sairametikala

Unit 1 vocabulary

Unit 1 vocabulary

home

hhhhhh

Juan 2

Juan 2

juanitorc

_____ _____ ___

_____ _____ ___

weiss2001

Doc1

Doc1

Prabhash Rawat

Biography

Biography

caila-bishop

Bol fracc

Bol fracc

verinlaza

Cajun Chicken Pasta

Cajun Chicken Pasta

Debbie's Mobile Kitchen

Every Drop Counts! ¡Cada gota cuenta!

Every Drop Counts! ¡Cada gota cuenta!

Cachi Chien

Vivekanandhan model.pdf 1

Vivekanandhan model.pdf 1

theniniyazh

Bibi4

Bibi4

Marc Arazi

Sap Business Objects

Sap Business Objects

shanereese49

Fasanara Capital | Investment Outlook 1. Fake Markets: How Artificial Money Flows Kill Data Dependency, Affect Market Functioning and Change the Structure of the Market Hard data ceased to be a driver for markets, valuation metrics for bonds and equities which held valid for over a century are now deemed secondary. Narratives and money flows trump hard data, overwhelmingly. ‘Fake Markets’ are defined as markets where the magnitude and duration of artificial flows from global Central Banks or passive investment vehicles have managed to overwhelm and narcotize data-dependency and macro factors. A stuporous state of durable, un-volatile over-valuation, arrested activity, unconsciousness produced by the influence of artificial money flows. - Passive Flows: The Prehistoric Elephant In The Room - ETFs Are Taking Over Markets - The Impact of Passive Investors on Active Investors: the Induction Trap - How Narratives Evolve To Cover For Fake Markets - Defendit Numerus: There is Safety in Numbers - What Could We Get Wrong 2. Be Short, Be Patient, Be Ready Markets driven by Central Banks, passive investment vehicles and retail investors are unfit to price any premium for any risk. If we are right and this is indeed a bubble (both in equity and in bonds), it will eventually bust; it is only a matter of time. The higher it goes, the higher it can go, as more swathes of private investors are pulled in. The more violently it can subsequently bust. The risk of a combined bust of equity and bonds is a plausible one. It matters all the more as 90%+ of investors still work under the basic framework of a balanced portfolio, exposed in different proportions to equity and bonds, both long. That includes risk parity funds, a leveraged version of balanced portfolio. That includes alternative risk premia funds, a nice commercial disguise for a mostly long-only beta risk, where premia is extracted from record rich markets that made those premia tautologically minuscule.

Fasanara Capital | Investment Outlook | May 3rd 2017

Fasanara Capital | Investment Outlook | May 3rd 2017

Fasanara Capital ltd

Fasanara Capital | Investment Outlook 1. The Future Is Wide Open: Avoid The ‘Illusion Of Knowledge’ Trap The single most dangerous thinking trap / optical illusion for investors today is to look at Trump, Brexit and Italy Referendum as non-events, buried in the past. We believe that 2017 may likely be driven by the same factors that failed to shape 2016. The non-events of 2016 are likely to be the drivers of 2017. Finally, we will get to find out if Brexit means Brexit, if Trump means Trump, if a failed Italian referendum means early elections and a membership of the EMU in jeopardy down the line. 2. Structural Shift: These Are Transformational Times The macro outlook of the next years will be influenced the most by these structural trends: › Protectionism, De-Globalization & De-Dollarization. In Pursuit of Inclusive Growth › End of ‘Pax Americana’. The ascent of China. Geopolitical risks on the rise › End of ‘Pax QE’. Markets without steroids, but still delusional. › 4th Industrial Revolution: labor participation rate falling from 63% to 40% in 10 years? 3. Our Baseline Scenario: Bubble Unwind, Equities and Bonds Down Starting this 2017, our major macro convictions are as follows: › Global Tapering to progress › US Dollar to keep grinding higher › European Political Instability to worsen › US Equities to weaken

Fasanara Capital | Investment Outlook | January 17th 2017

Fasanara Capital | Investment Outlook | January 17th 2017

Fasanara Capital ltd

1. Reflation Phase To Be Temporary, More Downside Ahead Earlier on in 2016, ‘random and violent markets’ went off to panic mode out of (i) fears over China’s messy stock market and devaluing currency, (ii) plummeting oil price, (iii) strong US Dollar. Today, we believe complacent markets are similarly illogical and over-shooting, this time on the way up. As we re-assess the validity of the underlying risks, we expect a shift in narrative in the few months ahead and a sizeable sell-off for risk assets. 2. Four Key Conviction Ideas We analyze below our key ideas for the next 12 months: Short Chinese Renminbi Thesis. In Q1, China only managed to keep GDP in shape by means of graciously expanding credit by a monumental 1 trn $. Unsurprisingly, at 250% total debt on GDP, you cannot borrow 10% of GDP per quarter for long, without a currency adjustment, whether desired or not. Short Oil Thesis. Long-term, we believe Oil will follow a volatile path around a declining trend-line, which will take it one day to sub-10$. Within 2016, we expect global aggregate demand to stay anemic and supply to surprise on the upside, inventories to grow, primarily due to the accelerating speed of technological progress. Short S&P Thesis. To us, the S&P is priced to perfection, despite a most cloudy environment for growth and risk assets, thus representing a good value short, for limited upside is combined with the risk of a sizeable sell-off in the months ahead. Short European Banks Thesis. We believe that micro policies at the local level, while valid, are impotent against heavy structural macro headwinds, and only the macro environment can save the banking sector in its current form in the longer-term. Macro structural headwinds for banks these days are too heavy a burden (negative sloped interest rate curves, deeply negative interest rates, deflationary economy, depressed GDP growth, over-regulation, Fintech), and will likely push valuations to new lows in the months/years ahead.

Fasanara Capital | Investment Outlook | May 3rd 2016

Fasanara Capital | Investment Outlook | May 3rd 2016

Fasanara Capital ltd

‘Deflationary Boom Markets’ ‘Deflationary Boom Markets’ is the name of the game. Deflation forces Central Banks into action. Central banks to push Bonds and Equities higher, inflating the bubble some more, although on a rougher path and with higher volatility than we got accustomed to in recent years.

Fasanara Capital | Investment Outlook | October 26th 2015

Fasanara Capital | Investment Outlook | October 26th 2015

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital ltd

Fasanara Capital Investment Outlook | February 1st 2015 1. Seismic Activity On The Rise 2. No Volatility No Gain 3. The Role Of Optionality 4. Crystal Ball 5. Deflation Is A Multi-Year Process 6. Three Big Trades for 2015

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital ltd

Mais conteúdo relacionado

Destaque

Bibi10

Bibi10

Marc Arazi

3

3

JessGelibert

Presentacion el hombre light

Presentacion el hombre light

guviarorienta

Flyer

Flyer

doublea196

dfd

Use case ex 4

Use case ex 4

sairametikala

Unit 1 vocabulary

Unit 1 vocabulary

home

hhhhhh

Juan 2

Juan 2

juanitorc

_____ _____ ___

_____ _____ ___

weiss2001

Doc1

Doc1

Prabhash Rawat

Biography

Biography

caila-bishop

Bol fracc

Bol fracc

verinlaza

Cajun Chicken Pasta

Cajun Chicken Pasta

Debbie's Mobile Kitchen

Every Drop Counts! ¡Cada gota cuenta!

Every Drop Counts! ¡Cada gota cuenta!

Cachi Chien

Vivekanandhan model.pdf 1

Vivekanandhan model.pdf 1

theniniyazh

Bibi4

Bibi4

Marc Arazi

Sap Business Objects

Sap Business Objects

shanereese49

Destaque

(16)

Bibi10

Bibi10

3

3

Presentacion el hombre light

Presentacion el hombre light

Flyer

Flyer

Use case ex 4

Use case ex 4

Unit 1 vocabulary

Unit 1 vocabulary

Juan 2

Juan 2

_____ _____ ___

_____ _____ ___

Doc1

Doc1

Biography

Biography

Bol fracc

Bol fracc

Cajun Chicken Pasta

Cajun Chicken Pasta

Every Drop Counts! ¡Cada gota cuenta!

Every Drop Counts! ¡Cada gota cuenta!

Vivekanandhan model.pdf 1

Vivekanandhan model.pdf 1

Bibi4

Bibi4

Sap Business Objects

Sap Business Objects

Mais de Fasanara Capital ltd

Fasanara Capital | Investment Outlook 1. Fake Markets: How Artificial Money Flows Kill Data Dependency, Affect Market Functioning and Change the Structure of the Market Hard data ceased to be a driver for markets, valuation metrics for bonds and equities which held valid for over a century are now deemed secondary. Narratives and money flows trump hard data, overwhelmingly. ‘Fake Markets’ are defined as markets where the magnitude and duration of artificial flows from global Central Banks or passive investment vehicles have managed to overwhelm and narcotize data-dependency and macro factors. A stuporous state of durable, un-volatile over-valuation, arrested activity, unconsciousness produced by the influence of artificial money flows. - Passive Flows: The Prehistoric Elephant In The Room - ETFs Are Taking Over Markets - The Impact of Passive Investors on Active Investors: the Induction Trap - How Narratives Evolve To Cover For Fake Markets - Defendit Numerus: There is Safety in Numbers - What Could We Get Wrong 2. Be Short, Be Patient, Be Ready Markets driven by Central Banks, passive investment vehicles and retail investors are unfit to price any premium for any risk. If we are right and this is indeed a bubble (both in equity and in bonds), it will eventually bust; it is only a matter of time. The higher it goes, the higher it can go, as more swathes of private investors are pulled in. The more violently it can subsequently bust. The risk of a combined bust of equity and bonds is a plausible one. It matters all the more as 90%+ of investors still work under the basic framework of a balanced portfolio, exposed in different proportions to equity and bonds, both long. That includes risk parity funds, a leveraged version of balanced portfolio. That includes alternative risk premia funds, a nice commercial disguise for a mostly long-only beta risk, where premia is extracted from record rich markets that made those premia tautologically minuscule.

Fasanara Capital | Investment Outlook | May 3rd 2017

Fasanara Capital | Investment Outlook | May 3rd 2017

Fasanara Capital ltd

Fasanara Capital | Investment Outlook 1. The Future Is Wide Open: Avoid The ‘Illusion Of Knowledge’ Trap The single most dangerous thinking trap / optical illusion for investors today is to look at Trump, Brexit and Italy Referendum as non-events, buried in the past. We believe that 2017 may likely be driven by the same factors that failed to shape 2016. The non-events of 2016 are likely to be the drivers of 2017. Finally, we will get to find out if Brexit means Brexit, if Trump means Trump, if a failed Italian referendum means early elections and a membership of the EMU in jeopardy down the line. 2. Structural Shift: These Are Transformational Times The macro outlook of the next years will be influenced the most by these structural trends: › Protectionism, De-Globalization & De-Dollarization. In Pursuit of Inclusive Growth › End of ‘Pax Americana’. The ascent of China. Geopolitical risks on the rise › End of ‘Pax QE’. Markets without steroids, but still delusional. › 4th Industrial Revolution: labor participation rate falling from 63% to 40% in 10 years? 3. Our Baseline Scenario: Bubble Unwind, Equities and Bonds Down Starting this 2017, our major macro convictions are as follows: › Global Tapering to progress › US Dollar to keep grinding higher › European Political Instability to worsen › US Equities to weaken

Fasanara Capital | Investment Outlook | January 17th 2017

Fasanara Capital | Investment Outlook | January 17th 2017

Fasanara Capital ltd

1. Reflation Phase To Be Temporary, More Downside Ahead Earlier on in 2016, ‘random and violent markets’ went off to panic mode out of (i) fears over China’s messy stock market and devaluing currency, (ii) plummeting oil price, (iii) strong US Dollar. Today, we believe complacent markets are similarly illogical and over-shooting, this time on the way up. As we re-assess the validity of the underlying risks, we expect a shift in narrative in the few months ahead and a sizeable sell-off for risk assets. 2. Four Key Conviction Ideas We analyze below our key ideas for the next 12 months: Short Chinese Renminbi Thesis. In Q1, China only managed to keep GDP in shape by means of graciously expanding credit by a monumental 1 trn $. Unsurprisingly, at 250% total debt on GDP, you cannot borrow 10% of GDP per quarter for long, without a currency adjustment, whether desired or not. Short Oil Thesis. Long-term, we believe Oil will follow a volatile path around a declining trend-line, which will take it one day to sub-10$. Within 2016, we expect global aggregate demand to stay anemic and supply to surprise on the upside, inventories to grow, primarily due to the accelerating speed of technological progress. Short S&P Thesis. To us, the S&P is priced to perfection, despite a most cloudy environment for growth and risk assets, thus representing a good value short, for limited upside is combined with the risk of a sizeable sell-off in the months ahead. Short European Banks Thesis. We believe that micro policies at the local level, while valid, are impotent against heavy structural macro headwinds, and only the macro environment can save the banking sector in its current form in the longer-term. Macro structural headwinds for banks these days are too heavy a burden (negative sloped interest rate curves, deeply negative interest rates, deflationary economy, depressed GDP growth, over-regulation, Fintech), and will likely push valuations to new lows in the months/years ahead.

Fasanara Capital | Investment Outlook | May 3rd 2016

Fasanara Capital | Investment Outlook | May 3rd 2016

Fasanara Capital ltd

‘Deflationary Boom Markets’ ‘Deflationary Boom Markets’ is the name of the game. Deflation forces Central Banks into action. Central banks to push Bonds and Equities higher, inflating the bubble some more, although on a rougher path and with higher volatility than we got accustomed to in recent years.

Fasanara Capital | Investment Outlook | October 26th 2015

Fasanara Capital | Investment Outlook | October 26th 2015

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital ltd

Fasanara Capital Investment Outlook | February 1st 2015 1. Seismic Activity On The Rise 2. No Volatility No Gain 3. The Role Of Optionality 4. Crystal Ball 5. Deflation Is A Multi-Year Process 6. Three Big Trades for 2015

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital ltd

Abstract from MARCH 2012 fasanara 'fat tail risk hedging programs' FTRHPs

Abstract from MARCH 2012 fasanara 'fat tail risk hedging programs' FTRHPs

Abstract from MARCH 2012 fasanara 'fat tail risk hedging programs' FTRHPs

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | December 1st 2014

Fasanara Capital | Investment Outlook | December 1st 2014

Fasanara Capital ltd

Fasanara Capital Investment Outlook | September 1st 2014

Fasanara Capital Investment Outlook | September 1st 2014

Fasanara Capital ltd

Fasanara Capital I Investment Outlook I April 1st 2014

Fasanara Capital I Investment Outlook I April 1st 2014

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | December 16th 2013

Fasanara Capital | Investment Outlook | December 16th 2013

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | October 7th 2013

Fasanara Capital | Investment Outlook | October 7th 2013

Fasanara Capital ltd

Artificial Markets are Structurally Fragile… Stay Hedged!

Fasanara Outlook Sept Investors Presentation 2013 | Artificial Markets are St...

Fasanara Outlook Sept Investors Presentation 2013 | Artificial Markets are St...

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | June 28th 2013

Fasanara Capital | Investment Outlook | June 28th 2013

Fasanara Capital ltd

Fasanara Capital | Investment Outlook - June 28th 2013

Fasanara Capital | Investment Outlook - June 28th 2013

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | May 3rd 2013

Fasanara Capital | Investment Outlook | May 3rd 2013

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | April 5th 2013

Fasanara Capital | Investment Outlook | April 5th 2013

Fasanara Capital ltd

Fasanara Capital | Appendix | Portfolio Buckets

Fasanara Capital | Appendix | Portfolio Buckets

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | March 1st 2013

Fasanara Capital | Investment Outlook | March 1st 2013

Fasanara Capital ltd

Fasanara Capital | Investment Outlook | February 1st 2013

Fasanara Capital | Investment Outlook | February 1st 2013

Fasanara Capital ltd

Mais de Fasanara Capital ltd

(20)

Fasanara Capital | Investment Outlook | May 3rd 2017

Fasanara Capital | Investment Outlook | May 3rd 2017

Fasanara Capital | Investment Outlook | January 17th 2017

Fasanara Capital | Investment Outlook | January 17th 2017

Fasanara Capital | Investment Outlook | May 3rd 2016

Fasanara Capital | Investment Outlook | May 3rd 2016

Fasanara Capital | Investment Outlook | October 26th 2015

Fasanara Capital | Investment Outlook | October 26th 2015

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital | Investment Outlook | June 1st 2015

Fasanara Capital Investment Outlook | February 1st 2015

Fasanara Capital Investment Outlook | February 1st 2015

Abstract from MARCH 2012 fasanara 'fat tail risk hedging programs' FTRHPs

Abstract from MARCH 2012 fasanara 'fat tail risk hedging programs' FTRHPs

Fasanara Capital | Investment Outlook | December 1st 2014

Fasanara Capital | Investment Outlook | December 1st 2014

Fasanara Capital Investment Outlook | September 1st 2014

Fasanara Capital Investment Outlook | September 1st 2014

Fasanara Capital I Investment Outlook I April 1st 2014

Fasanara Capital I Investment Outlook I April 1st 2014

Fasanara Capital | Investment Outlook | December 16th 2013

Fasanara Capital | Investment Outlook | December 16th 2013

Fasanara Capital | Investment Outlook | October 7th 2013

Fasanara Capital | Investment Outlook | October 7th 2013

Fasanara Outlook Sept Investors Presentation 2013 | Artificial Markets are St...

Fasanara Outlook Sept Investors Presentation 2013 | Artificial Markets are St...

Fasanara Capital | Investment Outlook | June 28th 2013

Fasanara Capital | Investment Outlook | June 28th 2013

Fasanara Capital | Investment Outlook - June 28th 2013

Fasanara Capital | Investment Outlook - June 28th 2013

Fasanara Capital | Investment Outlook | May 3rd 2013

Fasanara Capital | Investment Outlook | May 3rd 2013

Fasanara Capital | Investment Outlook | April 5th 2013

Fasanara Capital | Investment Outlook | April 5th 2013

Fasanara Capital | Appendix | Portfolio Buckets

Fasanara Capital | Appendix | Portfolio Buckets

Fasanara Capital | Investment Outlook | March 1st 2013

Fasanara Capital | Investment Outlook | March 1st 2013

Fasanara Capital | Investment Outlook | February 1st 2013

Fasanara Capital | Investment Outlook | February 1st 2013

Baixar agora