Recomendados

Recomendados

Mais conteúdo relacionado

Semelhante a Company report venus remedies ltd

Semelhante a Company report venus remedies ltd (20)

Mais de Four-S

Mais de Four-S (20)

Company report venus remedies ltd

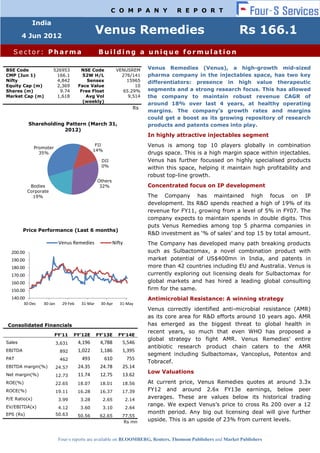

- 1. C O M P A N Y R E P O R T India 4 Jun 2012 Venus Remedies Rs 166.1 Sector: Pharma Building a unique formulation BSE Code 526953 NSE Code VENUSREM Venus Remedies (Venus), a high-growth mid-sized CMP (Jun 1) 166.1 52W H/L 276/141 pharma company in the injectables space, has two key Nifty 4,842 Sensex 15965 differentiators: presence in high value therapeutic Equity Cap (m) 2,369 Face Value 10 Shares (m) 9.74 Free Float 65.29% segments and a strong research focus. This has allowed Market Cap (m) 1,618 Avg Vol 9,514 the company to maintain robust revenue CAGR of (weekly) around 18% over last 4 years, at healthy operating Rs margins. The company’s growth rates and margins could get a boost as its growing repository of research Shareholding Pattern (March 31, products and patents comes into play. 2012) In highly attractive injectables segment Promoter FII Venus is among top 10 players globally in combination 14% 35% drugs space. This is a high margin space within injectables. DII Venus has further focussed on highly specialised products 0% within this space, helping it maintain high profitability and robust top-line growth. Others Bodies 32% Concentrated focus on IP development Corporate 19% The Company has maintained high focus on IP development. Its R&D spends reached a high of 19% of its revenue for FY11, growing from a level of 5% in FY07. The company expects to maintain spends in double digits. This puts Venus Remedies among top 5 pharma companies in Price Performance (Last 6 months) R&D investment as ‘% of sales’ and top 15 by total amount. Venus Remedies Nifty The Company has developed many path breaking products 200.00 such as Sulbactomax, a novel combination product with 190.00 market potential of US$400mn in India, and patents in 180.00 more than 42 countries including EU and Australia. Venus is 170.00 currently exploring out licensing deals for Sulbactomax for 160.00 global markets and has hired a leading global consulting 150.00 firm for the same. 140.00 Antimicrobial Resistance: A winning strategy 30-Dec 30-Jan 29-Feb 31-Mar 30-Apr 31-May Venus correctly identified anti-microbial resistance (AMR) as its core area for R&D efforts around 10 years ago. AMR Consolidated Financials has emerged as the biggest threat to global health in recent years, so much that even WHO has proposed a FY'11 FY'12E FY'13E FY'14E global strategy to fight AMR. Venus Remedies’ entire Sales 3,631 4,196 4,788 5,546 antibiotic research product chain caters to the AMR EBITDA 892 1,022 1,186 1,395 segment including Sulbactomax, Vancoplus, Potentox and PAT 462 493 610 755 Tobracef. EBITDA margin(%) 24.57 24.35 24.78 25.14 Net margin(%) Low Valuations 12.73 11.74 12.75 13.62 ROE(%) 22.65 18.07 18.01 18.56 At current price, Venus Remedies quotes at around 3.3x ROCE(%) 19.11 16.28 16.37 17.39 FY12 and around 2.6x FY13e earnings, below peer P/E Ratio(x) 3.99 3.28 2.65 2.14 averages. These are values below its historical trading EV/EBITDA(x) range. We expect Venus’s price to cross Rs 200 over a 12 4.12 3.60 3.10 2.64 EPS (Rs) 50.63 month period. Any big out licensing deal will give further 50.56 62.65 77.55 Rs mn upside. This is an upside of 23% from current levels. Four-s reports are available on BLOOMBERG, Reuters, Thomson Publishers and Market Publishers

- 2. Company Report: Venus Remedies 4 Jun 2012 Investment Rationale A top player in the attractive injectables space Venus is among top 10 players globally in combination drugs space with the biggest capacity in Asia in manufacturing for injectables. The US$200bn injectable market is higher on margins and faces lower pricing pressure compared to oral pharmaceuticals. A consistent focus on injectables, the highest end of the formulation value chain marked by stringent manufacturing standards, demanding quality parameters and low competition (only 1% of India’s over 10,000 pharmaceutical companies produce injectables) gives Venus a better ability to deliver higher margins. High growth segments Focussed on Venus Remedies has focused on high growth segments like anti- high growth, infective (33% of revenue) and oncology (30.7%) which are high margin considered to be the fastest growing segments and expected to segments within contribute 50 to 60% of product launches globally by 2015. injectables With changing demography and overall changes in lifestyle, anti- infective, oncology, cardiovascular and neurology segments are expected to benefit the most in the coming years, not only in India but globally. Venus has been investing strongly in R&D for all of these segments which will sooner than later start benefiting the company. Venus has already launched products in segments like anti-biotic, oncology, and neurology in last few years. Maintains high margin with highly specialised products Venus Remedies’ reported operating margins are better than the peer set, reflecting its focus on high margin segments within injectables. The company has margins better than all peers except Claris. The reason behind this is Venus Remedies’ conscious strategy to move away from its me-too products to enter high margin specialised segment with the backing of strong R&D process. Better profitability supporting the growth FY11 Margin (%) TTM Margin (%) Company EBIDTA PAT EBIDTA PAT Mid-Cap Peers Ajanta Pharma 19% 10% 21% 12% Indoco 13% 11% 14% 9% Four-S Research 2

- 3. Company Report: Venus Remedies 4 Jun 2012 Natco Pharma 19% 12% 23% 12% Nectar 20% 9% 18% 6% Parabolic Drugs 15% 8% 18% 6% Average 17% 10% 19% 9% Injectable Peers Strides Arcolab 21% 7% 21% 32% Ahlcon 16% 6% 16% 7% Parenteral Drugs 10% 1% -2% -20% Claris 31% 19% 32% 17% Kilitch 15% 7% 17% 9% Average 19% 8% 17% 9% Industry Average 18% 9% 18% 9% Venus 25% 13% 22% 13% (Source: Ace Equity, company reports) Profitability set to improve The company is confident that it can improve margins going forward. The key reason behind this is the high revenue flow expected from out-licensing of the already developed technology. This revenue will add to the top-line without putting much strain on cost side of the company’s profit and loss sheet. Creating significant opportunities through R&D Focus on formulation R&D products to beat me-too generic products competition Venus has evolved an innovative approach to its R&D investments to overcome competition in generic drugs. Its R&D is focussed on creating new drug candidates through formulation focused research, where it aims to combine two or more already patented APIs into a Research new formulation or a dosage form. Venus aims to make formulations pipeline based that are more effective than alternatives available in the market. It on novel aims to offer a therapeutic advantage and differ from me-too generic formulations products. This strategy offers a low-risk, low-cost alternative to the traditional pharmaceutical development of new medicines, due to their shorter development timeline. New Chemical Entities (NCEs) take a long time to develop, often at a cost of over US$1bn. Conversely, the development of new therapies through Venus’ method is cheaper and less time consuming, as it has a known mechanism of action and an established safety and efficacy profile. This offers products a less complex clinical development process. It also has a simpler pathway to patent approval that can potentially save pharmaceutical sponsors both time and money. Four-S Research 3

- 4. Company Report: Venus Remedies 4 Jun 2012 Some of its key products like Sulbactomax and Vancoplus are novel formulations of previously approved APIs. Concentrating on future epidemic : Anti-Microbial Resistance Venus has maintained strong focus on Antimicrobial resistance (AMR) while developing research products. Antimicrobial resistance (AMR) is the resistance of a microorganism to an antimicrobial medicine to which it was previously sensitive. These resistant organisms are able to withstand attack by antimicrobial medicines, such as antibiotics, antivirals, and antimalarials, so that standard treatments become ineffective and infections persist and may spread to others. Infections caused by resistant microorganisms often fail to respond to the standard treatment, resulting in prolonged illness and greater risk of death. Once resistance evolves, it can spread very rapidly across borders and around the world. This drug resistance threatens to erase gains made in disease treatment and control in developing countries. Venus Remedies is one of the few R&D led companies which has innovated and developed a comprehensive range of novel antibiotic combinations which not just provide relief from the aggravated problem of antibiotic resistance but also are cost-effective and have reduced side effects. The Company could foresee the potential of antibiotics fading 10 years back and it is the result of its focused approach that today it has some SUPER BUG tackling solutions under patent protection. The entire antibiotic research products of Venus like Vancoplus, Sulbactomax, Potentox, Tobracef and many more cater to the Antimicrobial Resistance segment. Sulbactomax – a key growth driver The biggest product from Venus’s R&D initiative is Sulbactomax, an anti-infective product, used to combat beta-lactamase generated Sulbactomax, a drug resistance, the only product in its category to prevent growth likely winner and spread of bacterial resistance. Sulbactomax is a combination of Ceftriaxone and Sulbactam with VRP1034. Venus’s tests show that Sulbactomax is much more effective than all the existing third generation cephalosporins and their combinations. Research pipeline robust, several launches ahead Research Besides Sulbactomax, Venus’s R&D has come up with several new launches unique formulations like Vancoplus, Potentox, and Tobracef. beginning to hit Achnil, launched in FY11, is a revolutionary once-a-day pain killer, the market given Product of the Year award by Biospectrum Asia for its uniqueness in addressing critical health conditions. Four-S Research 4

- 5. Company Report: Venus Remedies 4 Jun 2012 Many new products like Tumatrek, Trois and Stermex were lauched in FY12 and many more to be launched in coming years. These new products are estimated to generate revenue of 5-10% for the company in the next 2-3 years. Venus Remedies is coming up with constant flow of research products mainly due to its well thought out R&D process which looks for novel solutions that fill the vast gap between challenging ailments and available molecules. Aims to create Sizeable IP wealth by 2015 Venus now has 80+ global patents out of more than 360+ filed for its 13 research products. There is a clear indication that the company has created strong traction in R&D as well as Global presence. Rightly positioned to capitalise IP wealth Licensing Sulbactomax itself is patented in 42 countries including the EU discussions on countries; patents are awaited from 8 more countries including US for Sulbactomax and Japan. Sulbactomax has US$400mn market in India itself, according to Venus. Global potential is indicated by third generation cephalosporins and carbapenems, a close substitute, which have market of around US$2bn globally. Venus Remedies has already out- licensed Sulbactomax successfully to a South Korean pharma company to monetise the South Korean US$585mn market. In a similar way, Venus Remedies is looking to capitalise its IP wealth from its range of research products by striking deals with global pharma companies for specific geographies. Venus Remedies has already shortlisted a number of companies and is very close to finalising the deal with these companies. The company has hired renowned external agencies to make sure these deals are executed in the best interest of Venus Remedies’ stakeholders. Market authorisation in regulated markets Venus Remedies has marketing authorisations for EU markets for multiple products like Meropenem. It is the first Indian company to get GCC market authorisation for its oncology and Carbepenem products. This authorisation will further increase market reach of its products, pushing revenue growth. Vast pool of patented R&D products to capitalise on Since Venus Remedies has reorganized its priorities and started investing in R&D, it has developed respectable IP wealth within a very short period. Venus currently has more than 13 research products in development, with 11 products already under patent protection. 7 of these products are already commercialised not only in India but are also launched in emerging export markets through various alliances, and are selling in 12 countries. Overall, Venus Remedies boasts of 80+ patents out of more than Four-S Research 5

- 6. Company Report: Venus Remedies 4 Jun 2012 360+ filed in over 51 countries. It has 44 product registered in developed countries and has filed 108 CTDs for 7 products. Venus Remedies also has more than 375 market authorizations in semi- regulated market. Strong IP wealth with patented technology and ready to launch products along with EU GMP certified plant will enable Venus Remedies to monetise this wealth in the near future. Traction from research products to grow Revenue from With ever growing investment in R&D by Venus Remedies (from R&D products 14.5% of revenue in 2009 to 19% in 2011) and a strong R&D team could grow 20- of 60 scientists, in-licensing and R&D alliances with many 25% annually international universities, Venus Remedies is on right path to grow its IP wealth. This is also evident from range of their products in phase II & III of research. Research products contributed around 25% of Venus’ total revenue in FY12. Revenue from research products is expected to grow at a rate of 20-25%, higher than the generics in its portfolio. This strong traction is expected in near future because of new research products and established products. Superior operational efficiencies Better working capital management The chart below shows debtor turnover for the latest financial year. Venus Remedies performance here is above peer averages. Debtors Turnover 12.00 10.00 8.00 6.00 4.00 2.00 0.00 Running business with higher capital efficiency Venus remedies is utilizing its capital efficiently, resulting in better profitability ratio and better returns to its stakeholders. It can be seen from Venus remedies having highest ROE and ROCE ratios compared to most of its peers and much higher than industry average. Four-S Research 6

- 7. Company Report: Venus Remedies 4 Jun 2012 ROE ROCE 30% 25% 25% 20% 20% 15% 15% 10% 10% 5% 5% 0% 0% Indoco Ahlcon Ajanta Pharma Nectar Natco Pharma Industry Average Parenteral Drugs Strides Arcolab Parabolic Claris Venus Kilitch Indoco Ahlcon Ajanta Pharma Nectar Natco Pharma Industry Average Parenteral Drugs Strides Arcolab Parabolic Claris Venus Kilitch Valuations – have trended down in FY12 High discount compared to its peers Valuations Venus is currently traded at discounted valuations as compared to its ignoring steady pharma peers. When we divide peers among injectable segment and growth, and mid-cap segment, within injectable segment, Venus Remedies is at R&D results lowest multiple compare to its all injectable peers. Venus is also at lower range of valuations amongst Pharma companies of similar scale. Currently, Venus is traded at a PE ratio of 3.3 whereas mid-cap Pharma companies are traded at an average of 9.5 and injectables are traded at an average PE of 13.4. Given Venus’ steady growth performance, and reasonable return on capital, this gap will get bridged, at least partially, if not wholly. If it gets revenue from out-licensing, the process of narrowing of the valuation gap could get accelerated, giving a major upside for the stock. Four-S Research 7

- 8. Company Report: Venus Remedies 4 Jun 2012 Peer Benchmarking The peer set: mid-cap pharma companies & injectable players Venus Remedies is among the leading injectable manufacturers in India. We have compared it to its injectable peers, as well as midcap pharma peers. We find its performance is within peer averages, and better on some parameters. The strategy of Venus Remedies to focus on niche injectables segment has benefitted company, which is evident from its growth in last few years and margins it has managed through out. Company Market EV TTM TTM TTM TTM TTM TTM PAT Cap Sales Sales 4- EBITDA EBITDA PAT 4-yr yr CAGR 4-yr CAGR CAGR Mid-Cap Peers Ajanta Pharma 7456 8633 6714 21% 1407 29% 773 37% Indoco 4981 5980 5389 19% 735 15% 460 11% Natco Pharma 11517 13717 4831 10% 1095 20% 602 10% Nectar 4339 12299 13412 15% 2453 18% 804 2% Parabolic 1253 5997 9288 33% 1666 37% 574 18% Average 5909 9325 7927 19% 1471 24% 642 16% Injectable Peers Strides Arcolab 39986 64181 25645 26% 5399 67% 1,689 15% Ahlcon 3089 3341 848 9% 139 1% 43 -2% Parenteral Drugs 1441 7329 3083 10% -52 NA 50 NA Claris 10674 14376 7625 0% 2446 5% 1,414 4% Kilitch 570 1100 1414 5% 235 1% 105 2% Average 11152 18065 7723 10% 1633 19% 660 5% Industry Average 8531 13,695 7825 15% 1552 21% 651 10% Venus 1617 3486 4049 18% 896 15% 493 9% Better P&L Venus Remedies has performed better than its injectable peers in the growth numbers last 4 years as peers’ overall profit declined. Venus managed to than injectables improve PAT at a CAGR of 9%. peer average Peer revenues have grown at an average of 15%, while Venus has delivered growth rates of 18% over last four years. Among the best organic growths Among the companies performing better than Venus on growth, Strides Arcolab revenue was boosted by its acquisitions of Ascent Pharmahealth. Ascent Pharmahealth, one of the biggest branded generic drug manufacturer in Australia, had sales of US$140mn in FY10. Strides recently sold out 94% of its stake in Ascent to refocus Four-S Research 8

- 9. Company Report: Venus Remedies 4 Jun 2012 on speciality injectables. As can be seen in the table below, Venus Remedies is among the outperformers in its peer group on standalone basis as well, signifying success of Venus Remedies to grow organically at very comfortable rate. Venus Remedies has managed to propel its growth organically using its strong product portfolio and strong presence in highly growing injectable space. Company Revenue CAGR (FY08-FY11) Ahlcon Parenterals 11% Ajanta Pharma 17% Claris Lifesciences 4% Indoco Remedies 22% Kilitch Drugs 8% Natco Pharma 16% Nectar Lifesciences 13% Parabolic Drugs 31% Parenteral Drugs 22% Strides Arcolab 9% Industry Avg 15% Venus Remedies 19% Standalone revenues, Rs mn Comparing key P&L items Better profitability parameters Focus on high Venus Remedies has outperformed most of its peers in profitability in margin products midcap as well as injectable peers while generating strong growth has boosted numbers in last few years. margins While injectable peers have EBITDA margins of 17% on average and 9% PAT margins, Venus Remedies has managed to clock 22% EBITDA margin for TTM and 12% PAT TTM margins. Venus Remedies has better margins among its mid-cap peer companies which are averaging 19% EBITDA and 9% PAT margins compared to 22% EBITDA and 12% PAT TTM margins of Venus Remedies. Four-S Research 9

- 10. Company Report: Venus Remedies 4 Jun 2012 FY11 Margin (%) TTM Margin (%) Company EBIDTA PAT EBIDTA PAT Mid-Cap Peers Ajanta Pharma 19% 10% 21% 12% Indoco 13% 11% 14% 9% Natco Pharma 19% 12% 23% 12% Nectar 20% 9% 18% 6% Parabolic Drugs 15% 8% 18% 6% Average 17% 10% 19% 9% Injectable Peers Strides Arcolab 21% 7% 21% 32% Ahlcon 16% 6% 16% 7% Parenteral Drugs 10% 1% -2% -20% Claris 31% 19% 32% 17% Kilitch 15% 7% 17% 9% Average 19% 8% 17% 9% Industry Average 18% 9% 18% 9% Venus 25% 13% 24% 12% Balance sheet ratios Reasonable leverage Debt Equity (x) Interest Coverage (x) Company FY10 FY11 FY10 FY11 Mid-Cap Peers Ajanta Pharma 0.83 0.8 2.87 4.02 Parabolic 2.65 1.25 2.03 2.27 Indoco 0.21 0.29 14.3 21.22 Nectar 0.97 1.1 2.59 2.35 Natco Pharma 0.39 0.62 4.88 4.99 Average 1.01 0.81 5.33 6.97 Injectable Peers Ahlcon 0.29 0.66 7.35 3.17 KIlitch Drugs 0.57 0.63 4.27 4.94 Parenteral Drugs 0.62 0.75 3.17 1.3 Claris 0.39 0.38 4.07 4.07 Strides Arcolab 1.57 1.74 1.79 0.97 Average 0.69 0.83 4.13 2.89 Industry Average 0.85 0.82 4.73 4.93 Venus 0.87 0.79 4.28 3.77 Although Venus Remedies has investing heavily in its R&D and capacity ramp up in last 3-4 years, its debt condition is in line with industry scenario. Its financial position is pretty much on par Four-S Research 10

- 11. Company Report: Venus Remedies 4 Jun 2012 compared to most of its peers as can be seen table above. Liquidity ratios on par Current Ratio (x) Cash Ratio (x) Company FY9 FY10 FY11 FY10 FY11 Mid-Cap Peers Ajanta Pharma 1.62 1.85 1.55 0.16 0.12 Indoco 2.7 2.79 2.63 0.48 0.31 Nectar 1.26 2.11 1.72 0.17 0.13 Natco Pharma 1.27 1.31 1.53 0.08 0.31 Average 1.71 2.02 1.86 0.21 0.2 Injectable Peers Ahlcon 1.11 1.58 1.37 0.36 0.1 KIlitch Drugs 1.68 1.42 1.08 0.17 0.38 Claris 1.54 2.53 3.43 1.08 1.04 Strides Arcolab 1.39 2.12 1.86 0.37 0.19 Average 1.43 1.91 1.94 0.43 0.36 Industry Average 1.57 1.96 1.90 0.32 0.28 Venus 1.65 1.50 1.67 0.11 0.11 Venus Remedies is maintaining liquidity status similar to peers in the industry even though it has under taken high capex in last few years in R&D and capacity up-gradation. In March 2012, ICRA has assigned a BBB- rating to Venus Remedies on its debt facilities, citing comfortable financial risk profile marked by healthy size of net worth. Four-S Research 11

- 12. Company Report: Venus Remedies 4 Jun 2012 Comparing Peer Valuation Dividing peer set into two parts In the table below, as earlier, we have presented two sets of peers: mid-cap pharma companies and companies in injectable space. Valuation* EV/ CAGRs 4 year Ratios EBIDTA Company P/E P/E EV/ EV/ TTM TTM D/E ROCE ROE (TTM) (TTM) EBIDTA TTM Sales NP (FY11) (FY11) Sales Mid-Cap Peers Ajanta Pharma 4.62 9.72 8.96 6.13 1.69 17% 32% 0.80 22% 27% Indoco 10.70 10.84 9.28 8.13 1.24 21% 19% 0.29 14% 15% Natco Pharma 14.48 19.13 15.80 12.52 2.97 11% 10% 0.62 16% 16% Nectar 5.35 5.41 5.58 5.58 1.10 13% 11% 1.10 14% 15% Parabolic 5.00 2.18 5.95 3.60 0.89 31% 21% 1.25 15% 20% Average 8.03 9.45 9.11 7.19 1.58 19% 19% 0.81 16% 19% Injectable Peers Strides Arcolab 9.59 4.85 13.80 11.89 2.53 35% 31% 1.74 12% 17% Ahlcon 10.83 53.63 31.17 24.11 4.98 4% -11% 0.66 17% 12% Parenteral Drugs 88.27 -2.29 14.78 -139.91 1.51 32% -36% 0.75 4% 2% Claris 7.24 7.24 6.07 6.07 1.90 7% 19% 0.38 16% 15% Kilitch 7.48 4.58 4.97 4.69 0.75 8% -3% 0.63 13% 13% Average 24.68 13.60 14.16 11.69 2.33 17% 0% 0.83 12% 12% Industry Average 16.4 11.53 11.6 9.44 1.96 18% 9% 0.82 14% 15% Venus 3.98 3.28 3.91 4.06 0.96 19% 9% 0.79 19% 23% *based on latest financial year, +excluding Parenteral Drugs Venus Remedies is discounted lower compared to all its peers Sharp valuation Venus Remedies is valued at a sharp discount by the market discount to both compared to all of its peers. While Venus Remedies’ PE is ~3x FY12, injectables and industry average is hovering at 8-9x. Amongst the peer set listed pharma peers above, parenteral peers get similar valuation compared to pharma companies, but within the parenteral set as well, Venus is getting a low valuation. On a ttm basis Venus Remedies trades at discount of 70%, with a PE ratio of 3 compared to industry average of 10.63x. Venus Remedies’ EV/EBITDA is at discount of 43% and EV/Sales shows a discount of 38% with respect to industry average. Four-S Research 12

- 13. Company Report: Venus Remedies 4 Jun 2012 Valuation and Price Target Scope for higher valuations Business In terms of business ratios, like growth rates, operating margins, performance balance sheet ratios, Venus is doing as well as its peers. supports better It is likely Venus’ valuations are still suffering from the resettlement valuation of FCCB redemptions in FY10. This FCCB was issued in 2006, and given the bear phase the Indian markets were going through in FY10, the prevailing share price was much lower than the market price. Accordingly, investors wanted redemption. However, ultimately both parties agreed for a settlement at a lower price. Liquidity situation continues to remain reasonable. The company’s current rating is BBB-, as awarded by ICRA in March 2012. Another reason for the low valuation is the high R&D spends, some of which is passed through the balance sheet. Investors may be wanting to see more tangible results from the investment on R&D. We believe this scenario may change going forward as the market begins to see more results from Venus’s R&D pipeline. We also expect bottom-line growth to robust over FY12-14, as the company derives greater share of sales from high margin products. Any significant deal on Sulbactomax can be a further driver of rerating. Price Target 3 year P/E band chart 400 PE 350 7x 300 250 5x 200 150 3x 100 50 0 1-Apr-09 1-Aug-09 1-Apr-10 1-Aug-10 1-Apr-11 1-Aug-11 1-Feb-10 1-Feb-11 1-Feb-12 1-Dec-09 1-Dec-10 1-Dec-11 1-Jun-09 1-Oct-09 1-Jun-10 1-Oct-10 1-Jun-11 1-Oct-11 PE PE PE Even if Venus Venus is currently trading at around 3.3x FY12 eps and 2.6x maintains expected FY13 eps. This is below its historic trading range of the last current ttm 3 years, and around the valuation at the depth of the 2009 bear Four-S Research 13

- 14. Company Report: Venus Remedies 4 Jun 2012 valuations, market. These values are also much below peer levels. Similarly, its Mar’13 price EV/EBITDA for FY13 works out to 3.1x, which is much less than peer could touch levels. around Rs 225 We expect Venus to rerate upwards as market realises the strides it has made it its R&D portfolio. We expect Venus’s price to cross Rs 200 over a 12 month period, implying a rating of 3.3x expected FY13 earnings. This is an upside of 23% from current levels. Four-S Research 14

- 15. Company Report: Venus Remedies 4 Jun 2012 Venus Remedies’ Business As we noted in the valuation section, the low valuation given to Venus could partly derive from a lack of understanding of its business model. Its research model is quite unique compared to most Indian pharma companies. Second, inventors might not be giving much weight to its research capability, and assigning much value to its research pipeline. All of the above could arise because while Venus Remedies’ focus on R&D has resulted in significant investments, strong returns are yet to flow in. As a result, the company has not come close to generating free cash flows in recent years. These issues are discussed in detail below. A vision to break-out from me-too companies R&D push from Till year 2000, Venus Remedies was part of the cluttered generic 2006 injectables products segment. At the time, Venus Remedies was involved in generics injectables only. Realising generic products would have a limited scope in the future with patent regime coming into place in India from 2005; Venus Remedies changed its strategy and decided to focus on innovation to drive its growth. Venus Remedies started investing in R&D from year 2001. In a short time of 4 years, they filed for their first patent for Sulbactomax. The R&D effort is beginning to show steady results since then. Understanding Venus’ R&D R&D spends Venus Remedies is ranked 3rd among all Indian listed above peer pharmaceutical companies in terms of R&D spends as a share of levels revenues. It is ranked among the top 15 R&D spenders in absolute terms. Rank Companies R&D Spend (FY11) 1 Dr Reddy’s Laboratories 8464 2 Sun Pharmaceutical Inds. 2860 3 Matrix Laboratories 2820 4 Cadila Healthcare 2686 5 Cipla 2598 6 Biocon 1725 7 Ranbaxy Laboratories 1670 8 Torrent Pharmaceuticals 1527 9 Lupin 1268 10 Glenmark Pharmaceuticals 983 11 Aurobindo Pharma 815 Four-S Research 15

- 16. Company Report: Venus Remedies 4 Jun 2012 12 Panacea Biotec 772 13 Piramal Healthcare 716 14 Venus Remedies 696 15 Jupiter Bioscience 567 (Rs mn) Rank Companies % of revenue 1 Vivo Bio Tech 49 2 Suven Life Sciences 22 3 Venus Remedies 19 4 Jupiter Bioscience 17 5 KDL Biotech 16 Sun Pharma Advanced Research 6 Company 14 7 Zenotech Laboratories 12 8 Dr Reddys Laboratories 11 9 Auromed 11 Venus Remedies has invested more than Rs 1.5bn in the last 3 years, which is around 16.5% of its revenue in this period. For last three years, all the capex is done is also mainly in R&D, up-gradation and modernisation. R&D capability of Venus Remedies A multi-pronged The Company has proven its R&D capability with the gradual approach increase of revenue from the research products and 80+ patents in hand from over 51 countries. Venus has, in all, 11 testing labs working together to develop first-of-its kind product through highly sophisticated technology. It has developed 13 research products in short span of 9-10 years. At any time, R&D has a pipeline of 20+ products. On average, the Company comes out with 1-2 new developed products every year. In FY10, Venus Remedies launched Mebatic, an infusion therapy and Ampucare, a wound healing therapy, a first of its kind product in India. In FY12 Venus Remedies launched Achnil, a once-a-day painkiller. Venus has a well developed R&D centre with high tech capabilities at par with stringent cGLP standards. Its R&D centre has a strong 60 member scientist team; 70% of them are PhDs and post graduates. In licensed The Company also benefits from in-licensing alliances with various tumour innovative companies and university. It has in-licensed solid tumour detection detection technology for early detection from University of Illinois. technology from Such alliances have enhanced company’s R&D capabilities and have University of helped to improvise its R&D process. Illinois As of now, Venus is preparing to file more than 100 CTDs and ACTDs Four-S Research 16

- 17. Company Report: Venus Remedies 4 Jun 2012 each in the coming 3 years to take its present count of 600 ACTDs to 700 and 108 CTDs to 200 by 2015. Key Research areas Nano-tech Novel Drug Delivery System (NDDS): Venus has achieved success in based sustained development of nanotechnology-based, sustained release and release targeted delivery formulations with NDDS. This has resulted in formulations developing formulations with reduced adverse drug reaction and side effects in therapeutics areas of oncology, NSAID, neuroscience, arthritic disorders, stress and lifestyle-related diseases, immune chemistry, infectious diseases and wound healing. NDDS is advance drug delivery system which improves drug potency, control drug release to give a sustained therapeutic effect and provide greater safety. It is used to target a drug specifically to a desired tissue. Non-infringing Formulation Development: Venus is building its IP through formulations developing non-infringing formulations. Company is developing various formulations to revitalise established brands, fill product pipeline gaps and enhance patient compliance. With the help of strong regulatory team, Venus has managed to gain early mover advantage in many leading generic markets. Research Capabilities: Process developme nt and technology transfer Analytical Clinical research research division services (ARD) Research Capabilities Office of Chemical research and support stability (ORS) testing Pre- Natural clinical product division research (PCD) Process development and technology transfer: Ability to transfer technology from laboratory to pilot and to manufacturing scale. This is vital in technology transfer required to scale a Four-S Research 17

- 18. Company Report: Venus Remedies 4 Jun 2012 successful molecule and technology transfer in out-licensing deals. Analytical research division: Capable in developing novel formulations, analytical development and drug design support. Chemical and stability testing division: Capability to perform stability tests as per ICH guidelines provides analytical services to research dept and meets international quality and regulatory standards. Pre-clinical division: Performs pre-clinical trials and oxicological studies under GLP environment. Natural product research: screens natural products and drug development as per pharmacopial and medicine standards. Office of research support: Bridges the gap between research and marketing through interactions with the field force, training marketing teams, addressing queries raised by the PMT team and designing experiments for research value-addition. Clinical research services: Division involved in Phase-I, II, III, IV and BA/ BE clinical studies monitoring, as per GCP, for its research products to accelerated the delivery of safe and effective therapeutics. Key Initiatives in R&D Cell Culture Molecular Biology (CCMB) laboratory Working on a Venus has setup CCMB laboratory in affiliation with some other novel cancer pharma companies to fasten the cancer drugs testing. The company treatment has 4-5 such products which are expected launched in next 4-5 years. Company is also working on novel cancer drug for target- specific treatment (90% of the drug will go to the affected area against the present 10%). This will reduce the side effects of these drugs and also brings down the costs. Tie-ups with renowned research institutes A typhoid Company has tie-ups with IMTECH, a renowned research center of testing kit CSIR and Punjab University. Through this alliance, company is through a developing a typhoid diagnostic kit. This kit will reduce detection research tie-up time from 48 hrs to few minutes. Company has the authorisation to market this kit worldwide. Products conforming to ASEAN CTD Venus has upgraded its entire product pipeline of 75 products to ASEAN CTD preparing the entire portfolio for international. Four-S Research 18

- 19. Company Report: Venus Remedies 4 Jun 2012 Capitalising the IP Seeking out Venus Remedies understands that it is not easy to capitalise the IP licensing deals wealth they are creating in the huge global market. So to maximise to monetise IP the potential of this IP development, it has a clear strategy in place. Venus Remedies has appointed a leading consulting firm to seek tie- ups with international pharma companies for Sulbactomax. Venus Remedies plans to out-license the patented products to multi- national and regional companies with specific geographical interest considered. This will help Venus Remedies to garner the benefits from market across the globe without having to invest in market development. Venus Remedies has already closed an out-licensing alliance with a major South-Korean Pharma company for Sulbactomax. For FY12, Venus Remedies expects to get 25% of its revenue from its own research products. Venus Remedies’ Manufacturing excellence Among global leaders in fixed dosage injectable manufacturing Venus Remedies is among world’s top 10 injectable manufacturers and has the largest super specialty injectable manufacturing capacity in Asia. Venus has strong presence in relatively uncluttered, specialised, higher margin fixed dosage injectable space. Global injectable market is pegged at US$200bn in 2010 with generic market contributing US$20bn of it. There are limited numbers of players in the injectable space and high investment is required in setting up the complex plants. This will keep margins in this segment high with lesser competition to face in the market. Prominent Products 15% of FY11 Sulbactomax: It is the top product in Venus Remedies kitty with revenue 15% revenue contribution in FY12. The company holds patents for Sulbactomax in South Africa, India, 37 countries of the European Union, Russia, Ukraine, Mexico, Australia and New Zealand while patent is still awaited in six countries including US and Brazil. Sulbactomax is the only product in its category to prevent bacterial resistance. Sulbactomax is a formulation of ceftriaxone and sulbactam with VRP1034. The global injectable antibiotic market is US$200bn of which Ceftriaxone alone accounts around US$1.2bn. Sulbactomax aims to target a significant share of this market because of the growing bacterial resistance. Venus is currently marketing this product in India and seven other countries. Potentox: It is ranked second in Venus Remedies with respect to Four-S Research 19

- 20. Company Report: Venus Remedies 4 Jun 2012 revenue contribution (4.6% in FY12). Company has patents in South Africa, New Zealand, South Korea, Australia, Ukraine and India. 4.2% of FY11 Patents awaited from 44 other countries including EU and US. revenue Potentox, a research-based super-specialty product is used for treating hospital and community acquired pneumonia and febrile neutropenia. It reduces pneumonia treatment time from 21-30 days to 7-10 days and reduces drug and disease-induced toxicities. This is the only solution to growing flouroquinolene and aminoglycoside resistance. 3% of FY11 Vancoplus: It is third biggest product of Venus with 3% of revenue revenue in FY11. The company holds patent in US, Japan, Australia, South Africa, New Zealand and Ukraine. Patents awaited from 44 other countries including EU and Brazil. It is the only remedy after vaccination to treat superbug like MSRA, VRSA, VRE and multi-drug-resistant microbes causing meningitis. The product effectively stops the spread of resistance by preventing bacterial conjugation. 2% of FY11 Tobracef: Tobracef contributed 2% of revenue in FY11. It’s a revenue research-based anti-infective product catering to Pseudomonal infections caused in Cystic Fibrosis and HAP with patents in South Africa and patents awaited from other countries. Once company get patents and authorisation in major regulated market, this could also turn out to be major blockbuster project for Venus Remedies. Neurotol: Neurotol is an innovative product which contains mannitol and glycerine. Neurotol is used in the management of raised intracranial pressure and brain oedema associated with cerebral infraction, intracerebral hemorrhage, head injury, subdural hematoma, brain tumour, encephalitis and toxemia. Neurotol is widely accepted by medical fraternity like neurosurgeons and neurophysicians. The synergy of mannitol and glycerin in Neurotol prevents the chances of rebound oedema. Mannitol is known to provide immediate effect while glycerin is helpful for sustained effect. Venus is the first company to introduce this product. Neurotol offers improved patient compliance with no side-effects when compared with plain generic mannitol. Achnil: Achnil is an NDDS based controlled and sustained release NSAID (non steroidal anti-inflammatory drug) injection. It is the Launched in FY11 world’s first once-a-day pain killer injection which replaces the three injections per day therapy. It has already got patent application in EU and India while patent in US in under process. Achnil was launched in FY11 in the domestic market. The product prevents post surgical adhesion and has high levels of safety. Venus Research Product portfolio Four-S Research 20

- 21. Company Report: Venus Remedies 4 Jun 2012 Products Therapy Nature Sulbactomax Caters to ESBL, NMD-1, Penem Resistance Injection Vancoplus Caters to MRSA, VRSA & VRE Injection Potentox Caters to HAP, Febrile Neutropenia Injection Tobracef Developed for Cystic fibrosis Injection Zydotum For Pseudomonas Infections In Burns Injection Supime Intra-abdominal infections caused by various pathogens and post- Injection operative infections Pirotum Treatment of peritonitis and complicated intra-abdominal infections, Injection pirotum is indicated. continuous ambulatory pulmonary dialysis, management of lower respiratory tract infections and febrile neutropenia Neurotol For raised intracranial pressure and brain oedema associated with Infusion cerebral infraction, intracerebral hemorrhage, head injury, subdural hematoma, brain tumour, encephalitis and toxemia. Mebatic For pre and post surgical procedures, pelvic infections, urinary tract Infusion infections, urogenital tract infections, typhoid and prevention of ICU infections due to anaerobes. AMR compatible research products AMR has rapidly Antibiotic Resistance is spreading faster than expected throughout emerged as a world and the poor R&D pipeline for new antibiotics is further adding big global up this menace. Recently, World Health Organisation (WHO) has also health threat taken this issue with vigour by making this as main theme for World Health Day. According to WHO, AMR results in prolonged illness and greater risk of death. AMR not only increase overall health cost bur WHO feels world may end up in pre anti-biotic era. AMR has become serious problem for treatment for many major diseases like HIV, tuberculosis, malaria, gonorrhoea and many more. Risk factor involved in the infectious diseases has grown much more than it even existed and if it would keep on growing at the same pace, the world will soon reach the pre-antibiotic era again. The situation has deteriorated to an extent that even a mild infection can be deadly in today's world. The rising misuse and under usage has made the life saving antibiotics ineffective against the microbes. Reports say that US households lost approximately US$35bn in 2000 to antibiotic resistant infections including lost wages, extended hospital stays and premature deaths. The annual cost to the US health care system of antibiotic resistant infections is US$21bn to US$34bn and more than 8mn additional hospital days. In 29 countries of European union, an estimated 25,000 people die every year because of the infections related to antibiotics resistance. The medical cost per patient suffering from an antibiotic resistance (ABR) infections ranges from US$18,588 to US$ 29,069. According to the BCC Research report, the global market for infectious disease treatments was valued at $90.4 billion in 2009. This market is expected to increase at a compound annual growth rate (CAGR) of Four-S Research 21

- 22. Company Report: Venus Remedies 4 Jun 2012 8.8% to reach US$138bn in 2014. The antibiotics market generated sales of US$42bn in 2009 globally, representing 46 percent of sales of anti-infective agents (which also include antiviral drugs and vaccines) and five percent of the global pharma market. Inception of new antibiotics is getting difficult because of the present drug development scenario which is fraught with financial, regulatory, ethical and scientific bottlenecks. Due to huge investment in R&D and less output (financially) out of the product dejects the pharmaceutical companies to invest in it. Today, Venus Remedies is one of the few R&D led companies to have innovated and developed a comprehensive range of novel antibiotic combinations which not just provide relief from the aggravated problem of antibiotic resistance but also are cost-effective and have reduced side effects. All products which came out of Venus research efforts do cater to antimicrobial resistance. Products Category Dose Indications Sulbactomax Antibiotic Once daily IM/ IV injection in Infections caused by ESBL resistant mild to moderate infections and pathogens: twice daily in severe infections Lower respiratory tract infection Urinary tract infection Skin infections Surgical prophylaxis Bone and Joint infections Acute bacterial septicemia Acute Otitis media Potentox Antibiotic Twice Daily Multi-drug resistance of: Nosocomial Pneumonia Febrile Neutropenia Other severe hospital acquired infections Vancoplus Antibiotic Twice Daily IV injection in mild to Infections caused by resistant pathogens moderate infections and thrice such as MRSA: daily in severe infections. Meningitis Septicemia Skin and skin structure infections Bone and joint infections Post operative infections Tobracef Antibiotic Twice Daily injection Acute pulmonary exacerbations due to: Cystis fibrosis Pneumonia COPD Presence in highly specialised generics Within generics, which were around 75% of revenue in FY11, Venus has shifted focus to high margin products. Currently, Venus sells around 75+ products, with around 20+ products under development Four-S Research 22

- 23. Company Report: Venus Remedies 4 Jun 2012 phase at any point of time. Carbapenams, a Meropenem is one such generic product (carbapenem injection). key part of Venus Remedies has received market authorisation for Meropenem generics folio in EU. This represents a €150mn market opportunity, putting Venus among the top 3 EU-GMP manufacturers globally of carbapenem antibiotics. The Company has also received market authorisation for Imipenem+Cilastatin, Docitaxel and Irinotecan in the European Union. Similarly Venus also has market authorisation in for Gemcitabine for U.K., Germany, Poland Slovania, Portugal and Macedonia. Venus also has strong presence in oncology segment with 21 Oncology injectables in its portfolio. Oncology segment contributed more than generics are 30% to FY11 revenues, with extremely good margins. These are about 29% of much specialised products and high technology is required in revenue manufacturing these products. A key oncology product for Venus Remedies is Gemcitabine, for which it has marketing authorisation for in EU and UK. Gemcitabine is established as a gold standard therapy in treating pancreatic cancer. Venus understands the importance of this highly specialised, high technology, high margin oncology business. Hence, the Company has setup a dedicated sub-business unit for oncology business covering almost all cancer types just to further strengthen the focus on it. Oncology segment is likely to remain high growth has patents of oncology injectables, currently worth US$8.3bn, are set to expire by FY2015. Products kitty As can be seen, Venus has a strong kitty of 8 R&D products marketed in 12 nations. In the high margin oncology segment, it has 19 products with presence in 23 nations. Carbapenem and Cephalosporin has 20 products, with Carbapenem products sold in 23 nations. Category No. of products Presence R&D products 8 products 12 nations Oncology liquid 10 products (in various dosage 19 nations forms) Oncology lyphilised 9 products 23 nations Carbapenem 3 products 23 nations Cephalosporin and other 17 products 18 nations injectables PFS and infusions 5 products 11 nations Four-S Research 23

- 24. Company Report: Venus Remedies 4 Jun 2012 Bigger the pipeline, greater the in-flow in future Venus Remedies has strong R&D product pipeline as of now with more than 10 products at various stages of research. This comprises of products from therapeutic segments such as oncology, anti- infection and neuro. Typhoid and Some of the products close to commercialisation include a Typhoid tumour detection kit. With 17mn patients every year for typhoid, this detection kits detection kit has the potential to be a key revenue generator for part of IP Venus Remedies in future. The kit reduces the time taken for a pipeline typhoid test sharply, from 48 hours to few minutes. Similarly Venus has Tumatrek, an early tumour detection test in phase III and DPPC, a novel triple conjugate for targeted delivery of anticancer drug in preclinical phase. Venus also has products on oral, breast and ovarian cancer under pre-clinical tests. This strong pipeline creates strong prospects for Venus Remedies to drive the growth with its research products. Accolades & Awards showcasing research efforts Venus has received number of awards and accolades in last few years affirming the efforts and path chosen by the company. Venus has won awards for its research products and patents filed by company and as emerging company & manufacturing excellence. List of awards won by Venus Remedies: BioSpectrum Product of the Year 2012 award for its novel research product 'ACHNIL', a once-a-day painkiller. Gold Patent award 2011 for the novel research drugs presented by Pharmexcil. The Bizz- Business Excellence Award 2011 received in US. 'Silver Certificate of Merit' in the Economic Times' India Manufacturing Excellence Awards (IMEA), 2011 held in Mumbai. 'Emerging Company of the Year 2011' award in the 4th annual Pharmaceutical Leadership Summit & Award 2011. Best SMB Award 2008 Emerging India Award 2007 presented by Dr. Manmohan Singh Prime Minister of India. Ampucare Gold Medal 2010 'India Innovation Program- 2010' organized by Lockheed Martin (USA), FICCI and DST (India) . Trois: Gold Medal 2011 'India Innovation Programme - 2011' organized by Lockheed Martin (USA), FICCI. Quality Award 2011 in Gold category from BID International convention at Geneva. 2011 Spotlight award for the Annual Report in the LACP's (League of American Communications Professionals) Global Communication Competition In Bronze category in San Diego, USA. Marketing & Distribution Four-S Research 24

- 25. Company Report: Venus Remedies 4 Jun 2012 Pan India Venus has established a pan-India marketing presence covering 24 distribution States and two Union Territories, supported by over 700 marketing reach professionals. Venus Remedies has reach of 2,000 stockists and 40 distributors across India for the domestic market. These help target over 40,000 Pharmacies and 120,000 medical practitioners. The company has strong emphasis is on developing network of medical practitioners in critical care segment to address their specialised product market. Marketing Alliances to expand the reach Enhanced by To improve the reach within the domestic market, Venus Remedies tie-ups with has entered into tie-ups with many renowned Indian Pharma other pharma companies like Abbot, IPCA, Glenmark, Lupin, Elder, etc. To target companies the international markets in a better way, Venus Remedies has 11 overseas offices to cover 60 countries. Venus Remedies sells 44 products internationally with 3 research products launched till now. Similar to its domestic market strategy, Venus Remedies has made 20+ international alliances for its international market. Global Presence Direct overseas To capitalise on its IP pipeline, Venus Remedies has developed multi- presence in 11 regional presence across the globe. Venus has setup 11 overseas countries marketing offices covering 60 countries up from 19 countries in FY08. The 22 member team promotes 52 products across the globe. It has export presence in 25 countries with the help of these offices. World Class manufacturing capacities 3 manufacturing Venus Remedies has state of the art manufacturing facilities with the plants, 2 in latest technology. The company has invested more than Rs 2bn for a India, one in 100mn units injectable manufacturing facility at its unit in Baddi, Germany Himachal Pradesh. This has resulted in more than 20 international GMP certifications from more than 50 countries. This facility manufactures in all 75+ super specialty products. In all, Venus Remedies has 3 manufacturing locations: Baddi, Panchkula (India) and one in Germany. All are with EU-GMP and WHO-GMP certification along with other certifications. Its Panchkula site has 7.5mn units capacity for large volume parenterals accredited with WHO-GMP. Products manufactured at this facility include Mebatic, Calridol, Moximicin, Neurotol, Glutapep, among others. The Baddi campus has eight small volume parenteral facilities. It manufactures oncology injections, oncology lyophilised, lyophilised injections, pre-filled syringes and cephalosphorins. It has been accredited with more than 20GMPs. Recently; its Baddi plant has received GCC certification for oncology and carbepenem products, the first in India. Four-S Research 25

- 26. Company Report: Venus Remedies 4 Jun 2012 Venus Pharma GmbH (Germany) With the goal in mind to be a true global Pharma company, Venus acquired the German Pharma company in 2006. It’s strategically located in the second largest Pharma market and largest in Europe, Germany. This acts as an entry vehicle for Venus Remedies products in European market. Venus Pharma GmbH helps Venus Remedies to generate export orders for its products, executes site transfer projects and supports in CTDs filing. Revenue distribution Dry powder and Venus Remedies has a strong existence in dry powder segment oncology are constituting 33% of revenue in FY11. Cehpalosporin and penem the two key products constitute this dry powder segment. Venus Remedies has segments strong presence in this segment in both generic products and also in research products. With multiple countries GMP certification for its manufacturing plant, the export market may grow at very good rate for this segment. Revenue Distribution 24% Anti-cancer 31% Cephalosporin (Inc Carbapenem) Infusions 12% SVP & Others 33% With many products still new in the market and in the process of developing its market, high growth in all the segments especially in oncology, dry powder is very much visible in the coming few years Four-S Research 26

- 27. Company Report: Venus Remedies 4 Jun 2012 Focus on higher margin products Dry Powder Revenues 1,350 60% 1,300 50% 1,250 40% 1,200 30% INR mn 1,150 20% 1,100 1,050 10% 1,000 0% FY08 FY09 FY10 FY11 FY12E Dry Powder % of Total Revenues Dry power share In line with focus on high margin products, share of revenue of dry coming down powder products is coming down. Increasing higher margin oncology segment Oncology biz growth 1,400 35% Oncology Segment % of Revenue 1,200 30% 1,000 25% 800 20% 600 15% 400 10% 200 5% 0 0% FY08 FY09 FY10 FY11 FY12E Oncology is a Oncology segment contributes almost 31% of overall revenue of focus segment Venus Remedies. Due to complex products, critical nature and for Venus sophisticated technology involved in this segment, margins are better here. Venus Remedies has successfully managed to improve oncology contribution. Oncology segment has grown CAGR of 30% in last 4 years. With more than 300 market authorisations from 25 countries, Four-S Research 27

- 28. Company Report: Venus Remedies 4 Jun 2012 the company should be able to maintain this thrust. Risk Factors Venus Remedies has the policy of capitalising major portion of its R&D expenditure. In FY11, Venus Remedies capitalised Rs 557mn of R&D expenditure out of its Rs 686mn R&D expenditure. R&D expenditure capitalisation is not new for pharma companies as most of Indian pharma companies do capitalise part of their R&D expenditure. Yet amount of R&D expenditure capitalised is much higher compared to many other major pharma companies. The Company attributes this to expenditure on research which is yet to be commercialised; around 360 patent applications are still pending. The Company is capitalising expenditure on R&D, IPR, CTD /ACTD and other product registration expenses, R&D activities like clinical trials, process development & technology transfer, in licensing and formulation development from in-licensed technology, expenses on analytical & chemical research on products under commercialization, etc. This R&D expenditure capitalisation is also reflected in cash flow. Though Venus has good positive operation cash flow, company is suffering from negative free cash flow. Four-S Research 28

- 29. Company Report: Venus Remedies 4 Jun 2012 Financial Analysis and Growth Outlook 15% CAGR for revenue expected during FY’12-14 The Company’s net revenues have grown at a CAGR of 18% over FY’08-’12E (for FY12 only stand alone results declared so far, consolidated are our estimates) to Rs 4.78bn from Rs 2.15bn in FY08. Revenue Growth 4,500 4,000 4 year revenue 3,500 CAGR is 18%, 3 3,000 year growth is 12% 2,500 2,000 1,500 1,000 500 - FY'08 FY'09 FY'10 FY'11 FY'12E (Rs mn) The top line of Venus is expected to grow at CAGR of 15% over FY11- 14. Revenue Growth Expected 6,000 Growth to be 5,500 driven by newly 5,000 launched products and 4,500 expansion in 4,000 regional 3,500 presence 3,000 2,500 2,000 1,500 FY'11 FY'12E FY'13E FY'14E Four-S Research 29