Gold appears to be nearing the projected top of an Elliott wave triangle pattern near $1,100 based on technical analysis of price movements and contracting waves. Implied volatility in gold has not risen as expected with the recent price increases, suggesting waning speculation, which is a signal that the top may be near. The analysis provides several limited risk trades to profit from a potential price drop to $955 or further increases, including buying puts, a straddle, or calls with risk management protections.

Beginners Guide to TikTok for Search - Rachel Pearson - We are Tilt __ Bright...

Outlook on Gold - Nov. 4, 2009

1. Volatility Research & Trading

Research@vVolatility.com

04 November 2009

Volume 1, Issue 4

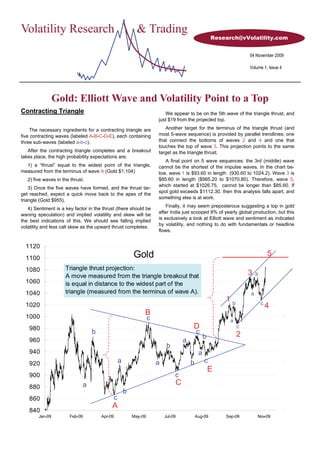

Gold: Elliott Wave and Volatility Point to a Top

Contracting Triangle We appear to be on the 5th wave of the triangle thrust, and

just $19 from the projected top.

The necessary ingredients for a contracting triangle are Another target for the terminus of the triangle thrust (and

five contracting waves (labeled A-B-C-D-E), each containing most 5-wave sequence) is provided by parallel trendlines; one

three sub-waves (labeled a-b-c). that connect the bottoms of waves 2 and 4 and one that

touches the top of wave 3. This projection points to the same

After the contracting triangle completes and a breakout target as the triangle thrust.

takes place, the high probability expectations are;

A final point on 5 wave sequences: the 3rd (middle) wave

1) a “thrust” equal to the widest point of the triangle, cannot be the shortest of the impulse waves. In the chart be-

measured from the terminus of wave A (Gold $1,104) low, wave 1 is $93.60 in length (930.60 to 1024.2). Wave 3 is

2) five waves in the thrust. $85.60 in length ($985.20 to $1070.80). Therefore, wave 5,

which started at $1026.75, cannot be longer than $85.60. If

3) Once the five waves have formed, and the thrust tar-

spot gold exceeds $1112.30, then this analysis falls apart, and

get reached, expect a quick move back to the apex of the

something else is at work.

triangle (Gold $955).

Finally, it may seem preposterous suggesting a top in gold

4) Sentiment is a key factor in the thrust (there should be

after India just scooped 8% of yearly global production, but this

waning speculation) and implied volatility and skew will be

is exclusively a look at Elliott wave and sentiment as indicated

the best indications of this. We should see falling implied

by volatility, and nothing to do with fundamentals or headline

volatility and less call skew as the upward thrust completes.

flows.

1120

1100 Gold 5

1080 Triangle thrust projection: 11

A move measured from the triangle breakout that 3 b

1060 is equal in distance to the widest part of the

1040 triangle (measured from the terminus of wave A). a

1b c

1020 4

1000

B 9

c a

980 D c

b c 2

b

960 a

b

940 a

920 a a b c 7

E

900 c

a C

880

b

860 c

A

840 5

Jan-09 Feb-09 Apr-09 May-09 Jul-09 Aug-09 Sep-09 Nov-09

2. Implied Volatility is unimpressed with higher Gold

The break of the triangle

1120 5 was initially met with excite-

1100 Gold

ment, renewed gold fever and

1080 3 11 a spectacularly fast jump in

b

1060 one-month implied volatility

1040 1 a

from 16% to 26%. Implied

1020 B

b c

4 volatility was cheap and had

1000 c a 9 been relatively motionless for

D c

980 b c 2 the previous two months, so a

b

960 a move of that extent was not

b

940 a entirely unexpected.

920 a a b c 7

E What did seem a bit odd,

900 c

a C was the speed with which 1m

880 b vol fell back to 17% once the

860 c

A spot advance paused.

840 5

Jan-09 Feb-09 Apr-09 May-09 Jul-09 Aug-09 Sep-09 Nov-09 On the next jump in gold

(wave 3 on the top chart), im-

1120 45 plied volatility rose again, but

was unable to surmount the

1100 43 wave 1 high.

1080 41

The current gold rise has

1060 39 produced an even more pa-

1040 37 thetic volatility response. 1m

1020 35 vol is languishing below 19%,

a full 7% less than it attained

1000 33 after the initial triangle break.

1y Implied Vol

980 31

One-year implied vol is also

960 29 unable to exceed recent highs

940 27 as gold propels higher. 1y vol

920 25 has been overvalued by at

least 10% for a long time now,

900 23

1m Implied Vol so the muted vol response is

880 21 less of a surprise than the 1

860 19 month stupor.

840 17 The lower chart shows 1m

820 15 and 1y 25 delta risk reversals

Jan-09 Feb-09 Apr-09 May-09 Jul-09 Aug-09 Sep-09 Nov-09 (25d call vol - 25d put vol). The

1m RR managed to reach

1120 12 3.5% on the wave 1 and 3 ad-

vances, but has dropped below

1100 11 2% on the current gold rise.

1y 25d Risk Reversal

1080 10 This is a clear example of a

lack of participation by the

1060 9 speculative community.

1040 8 The 1y RR is more reflec-

tive of real (long-term) gold

1020 7

demand, and is at silly levels to

1000 6 begin with. With implied vol

falling as gold rallies, the RR

980 5 should be on a fast track to

960 4 zero.

1m 25d Risk Reversal

940 3 There must be a level

where both specs and long-

920 2 term security seekers re-enter

the market via gold calls, but

900 1

that level is likely significantly

880 0 higher (beyond the triangle

Jan-09 Feb-09 Apr-09 May-09 Jul-09 Aug-09 Sep-09 Nov-09 thrust projection top?).

Volume 1, Issue 4 Page 2

3. One-year Implied Volatility is expensive; One-month vol is fair.

The premium of one-year implied volatility

1120 46

over one-year realized volatility remains

1100

extreme. (realized vol is exponentially 44

1080 weighted using hourly data). 42 1y Implied vol

1060

1040 40 has been consis-

tently overvalued

1020 38 since Dec 08.

1000

36 It fell 20% from

980

the March 09 44%

960 34

top, but has further

940 32 to go.

920

900 Gold 30 Who buys this

stuff at a negative

28

880 edge of 10% to

860 26 15%?

840 24 At some point I

820 1 yr Implied Vol would expect a

22 degree of capitula-

800

10.9% 20 tion from the 1y vol

780

buyers.

760 1 yr Realized Vol 18

740

16

720

700 14

680 12

Oct-08 Dec-08 Jan-09 Mar-09 Apr-09 May-09 Jul-09 Aug-09 Sep-09

While one-year implied vol is extremely expensive, one-month 60 1m Implied vol

implied vol is fairly valued. The recent jumps in 1m vol were displays the volatile

1080 58

unsupported by realized volatility, but any move back to 16-17% nature of specula-

56

1055 tors.

appears to offer reasonably-priced gamma for the next gold move. 54

1030 52 While realized

50 vol was first stead-

1005 ily lower, and then

980

Gold 48

consistently side-

46

ways, the jumpi-

955 44

ness of implied vol

42

930 shows the desire of

40 specs to hop on

905 38 breakouts.

36

880 At these levels,

34

1m vol is a safe buy

855 32

when it trades at or

30

830 below weighted

1m Implied Vol 28

realized vol.

805 26

780 24

22

755 20

730 18

16

705

14

1m Realized Vol

680 12

Oct-08 Dec-08 Jan-09 Mar-09 Apr-09 May-09 Jul-09 Aug-09 Sep-09

Page 3 Volatility Research & Trading

4. Limited Loss Trades to play a

top at $1,100 and a dip to $955

Trade Ideas: affected by skew) costs 10% of payout. Odds are therefore

Implied Vol is reasonable in the front end of the curve and 9:1. For every $10 you bet, $100 is received if $955 touches.

rich in the back end, so any strategy should incorporate either

front end purchases, back end sales, or both. Trade 3: Buy a 1.5 month ATM straddle

Skew is extreme for calls in the one year, so that favours

selling low delta calls and buying low delta puts. But since the

absolute level of 1y vol is high, we are left with just 1y call An idea with much less leverage, but a greater chance of

selling. turning a profit is a simple purchase of an at-the-money

straddle, again for the 18 Dec 09 date. With implied volatility

Skew is moderate for the one-month, so buying puts is at 20.5%, an atm straddle costs $57. Breakeven is $57 either

reasonable (they are cheaper than calls. Avoid selling gamma side of spot, so if our $955 target comes to pass the profit

(Gold calls), since we want to make a bit of money if correct (on expiration) would be 1.55 times premium. If India has

in our analysis, not lose our jobs if wrong. several more tones of gold to buy, or if all fiat currencies sud-

One month is a bit too short, and two months is too long, denly disappear, the topside profit potential could also be

so we’ll settle on 18 Dec (46 days) for option expiries. attractive.

Trade 1: Buy a 1.5 month 30 delta put Trade 4: Buy a 1y Gold call with a $1,300 RKO (for the

With Gold at 1,100, and 46 day 30 delta puts at 20% vol, tempered bulls).

the cost of buying an 18 Dec 09 $1,065 Put would be $14.70.

Our target is $955 (triangle apex), so if correct we would To sell both high 1y skew and high 1y implied volatility, a

make a net gain of $95.30, or 6.5 times premium. If wrong, 1y $1,100 Gold call (off a spot of $1,100) with a reverse

we would lose $14.70. knockout at $1,300 costs a mere $10. The premium rises to

Trade 2: Buy a 1.5 month $955 one-touch $20 if the knockout is pushed higher to $1,400. The risk in

these trades is a Gold rises beyond the topside barrier. You

would lose the premium despite calling the direction cor-

A $955 one-touch (American style—look any time) also rectly.

based off a $1,100 spot and 19.5% vol (lower than the previ-

ous trade because it is a lower delta and is therefore more

Ma

nag

e th

eD

own

sid

e...

Please direct any enquiries or feedback to:

Research@vVolatility.com

Page 4 Volatility Research & Trading

Disclaimer: This document researches assets from primarily a volatility perspective. No forecasts made or implied in this analysis should be used as a basis for

assuming, increasing or reducing risk of any sort. The opinions expressed in this publication are those of the author, and are subject to frequent and dramatic

change as new information is introduced. This document is for entertainment purposes only.