Scizophrenic market

•Transferir como DOCX, PDF•

1 gostou•410 visualizações

Market commentary focusing on technical analysis of major asset classes and the economic fundamentals behind market movements.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (19)

Destaque

Destaque (10)

Semelhante a Scizophrenic market

Semelhante a Scizophrenic market (20)

Último

Último (20)

Scizophrenic market

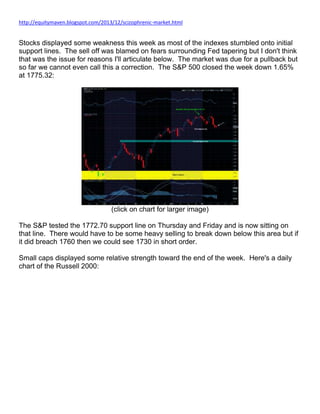

- 1. http://equitymaven.blogspot.com/2013/12/scizophrenic-market.html Stocks displayed some weakness this week as most of the indexes stumbled onto initial support lines. The sell off was blamed on fears surrounding Fed tapering but I don't think that was the issue for reasons I'll articulate below. The market was due for a pullback but so far we cannot even call this a correction. The S&P 500 closed the week down 1.65% at 1775.32: (click on chart for larger image) The S&P tested the 1772.70 support line on Thursday and Friday and is now sitting on that line. There would have to be some heavy selling to break down below this area but if it did breach 1760 then we could see 1730 in short order. Small caps displayed some relative strength toward the end of the week. Here's a daily chart of the Russell 2000:

- 2. (click on chart for larger image) The Russell also flirted with a break down under initial support (white dashed line) but managed to finish the week just above it. On the whole, stocks are no worse for the wear after a down week and I'm mildly encouraged that the two indexes above held on to initial support. I expect more volatility going into next week as we near the FOMC meeting on Tuesday and Wednesday. More on this below. Treasury yields continue their systematic move higher with the Ten Year Treasury yield closing the week at 2.868%: (click on chart for larger image) There has been concern over the impact of higher interest rates on the economy and the stock market. As we take a look at the Ten Year yield from a weekly perspective we see that it is testing Fibonacci resistance for the second time since September:

- 3. (click on chart for larger image) I read an article this week that highlighted Japanese investors who have been gobbling up long term US Treasury paper as they see these yields as quite attractive. They quoted fund manager Yusuke Ito of Mizuho Asset Management, “There’s tremendous deflationary pressure in the U.S. For bonds, the longer the maturity, the better." As U.S. investors exit duration (longer term treasuries) in the domestic bond market, Japanese investors, to whom the U.S. 10-year yield of 2.868% looks positively towering, are snapping the paper up. The country's holdings of U.S. debt rose $98.2 billion in the third quarter, the second largest increase since the data started becoming public 13 years ago. “The Japanese have experience with 15 years of disinflation,” says Hideo Shimomura, chief fund investor at Mitsubishi UFJ. “Now it is spreading to the U.S. It’s worthwhile to take long-end risk in portfolios.” Clearly, Japanese investors, after a two decade losing battle with deflation, have a very different perspective on where global interest rates are going. And they're dumping their money into the safest debt market on the planet. More on this below. On a week where stocks manifested the most weakness since September I was encouraged that commodities, especially industrial commodities, actually penetrated some significant resistance. Copper has broken out above multi year resistance:

- 4. (click on chart for larger image) Below is a weekly chart of the Dow Jones UBS Industrial Metals Index: (click on chart for larger image) Admittedly, commodities are nowhere out of the woods yet but the fact that they displayed this kind of strength during a week of stock market weakness debunks the thesis that stocks were foretelling economic weakness from mounting deflationary forces as a result of Fed tapering. And gold also held it's own this week. I'm not going to show the chart because it basically went nowhere. But the fact that it didn't continue to fall out of bed lent another encouraging tidbit to the commodity story. Another continuing positive development is that the Baltic Dry Index which measures changes in the cost to transport raw materials such as metals, grains and fossil fuels by sea broke through Fibonacci resistance and is at the highest level since October, 2011:

- 5. (click on chart for larger image) Considered a leading indicator of global economic growth the Baltic is forecasting better times ahead for the global economy. Hopefully this trend will continue and the next target for the Baltic is the 4700 area (it closed on Friday at 2330.00). Analysis The market seemed to be telling us that it was no longer afraid of Fed tapering on 12/6 when it rallied on a better than expected monthly employment report. But this week, so the financial press would tell us, everyone was once again scared of an imminent Fed tapering. Aside from the fact I'm fairly certain that the Fed won't begin tapering next week for a number of good reasons which I'll outline below, I don't think the market weakness had anything to do with whether the Fed will taper or not but was simply a matter of a market in need of a much needed breather after an incredible run up. In my opinion, the fact that we saw relative strength in commodities in the face of the sell off in stocks this week validates my position. If my thesis is right, the rally will resume on Wednesday afternoon when the Fed announces it is leaving intact (for now) it's bond buying program. Historically speaking, the Christmas rally normally takes place in the last two weeks of December and has been preceded the majority of times by market weakness the prior two weeks. The Fed will not commence tapering after the December meeting for the following reasons: 1. Inflation is just too low for the Fed to risk a reduction of liquidity, even if they believe the economy is growing. Friday morning's release of the November PPI (Producer Price index) shows producer prices fell 0.1 percent in November fir the third straight month. Economists had expected headline producer prices to be flat in November, compared to a 0.2 percent decline in the prior month. I submit to my readers that, assuming the economy continues to improve, disinflationary concerns will be the paramount consideration going forward on whether/when the Fed begins to taper its asset purchases. 2. Along with inflation being too low, the Fed has to worry about how higher interest rates are going to effect the economy. The Fed has publicly committed to anchoring the short

- 6. end of the yield curve (short term interest rates) with ZIRP (Zero Interest Rate Policy); basically keeping the Fed Funds rate between 0 and 25 basis points (0% - .25%). But as they reduce their asset purchases there will be inevitable pressure on long term interest rates. The first victim of higher long term interest rates will be the housing market. And the home builders will be the first sector to take higher interest rates "on the chin". Here's a chart I haven't posted in awhile of the iShares Dow Jones Home Construction ETF (ITB): (click on chart for larger image) I've outlined the two key events on the chart which impacted home builders in 2013 and they have yet to recover from those two events. The specter of higher interest (read mortgage) rates and the threat of the reduction in Fed asset purchases has kept a lid on home builder stock prices. We need to see a decisive break out in this ETF above the green resistance line for the chart to tell us that higher long term interest rates will not negatively effect this vital part of the US economy. The positive we can glean from the chart is that since September the ETF has experienced a series of higher lows (blue dashed line) which is potentially a bullish development moving forward. 3. Janet Yellen has not taken over the Federal Reserve yet and Bernanke will be loathe to start the process before she's at the helm. 4. The FOMC is in a transition with at least two seats changing hands over the next two months. Once again, the FOMC will await a consensus among the newly constituted FOMC before moving forward with such a crucial decision. Summing up, I'm still looking for 1860 on the S&P although admittedly it is a tall order

- 7. given the setback we've had this week. However, I do expect the rally to resume after the FOMC meeting on Wednesday and with the band aid that politicians put on our burgeoning debt problem this week, the stage is set for a strong month for stocks in January unless the global deflationary juggernaut that have Japanese investors clamoring for our long term debt, takes hold of the global economy. Have a great week! www.equitymaven.blogspot.com