OTN - Trade Brief on CARICOM-Canada Investment

•

0 gostou•138 visualizações

Recomendados

Recomendados

Mais conteúdo relacionado

Semelhante a OTN - Trade Brief on CARICOM-Canada Investment

Semelhante a OTN - Trade Brief on CARICOM-Canada Investment (13)

Mais de Office of Trade Negotiations (OTN), CARICOM Secretariat

Mais de Office of Trade Negotiations (OTN), CARICOM Secretariat (20)

OTN - Trade Brief on CARICOM-Canada Investment

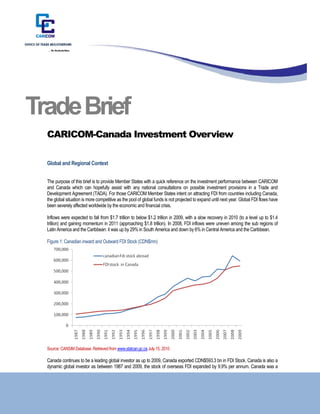

- 1. OTN BARBADOS OFFICE 1st Floor, Speeedbird House, Bridgetown BB11121, n Ref: R 31000.3/6-2 2010-07-18 6) BARBADOS Tel: (246 430‐1670 Fax: (246) 228 8‐9528 Emai barbados.office@crnm. il: .org OTN JAMAICA OFFICE 2ND Floor, PCJ Building, Kingsto 5, on JAMAICA Tel: (876 908‐4242 Fax: (876) 754 6) 4‐2998 Ema jamaica.office@crnm.o ail: org Trad B ef T de Brie CA ARICOM M-Cana Inve ada estmen Over nt rview Globa and Regional Context al l The purpose of this brie is to provide Me ef ember States with a quick referenc on the investm performance between CARIC h ce ment e COM and Ca anada which can hopefully assis with any natio consultations on possible in n st onal s nvestment provisions in a Trade and Development Agreemen (TADA). For those CARICOM M nt Member States in on attracting FDI from countr including Can ntent g ries nada, the glob situation is mo competitive as the pool of glob funds is not pro bal ore s bal ojected to expand until next year. G d Global FDI flows have been seeverely affected worldwide by the e w economic and financial crisis. Inflows were expected to fall from $1.7 t t trillion to below $ trillion in 200 with a slow re $1.2 09, ecovery in 2010 (to a level up to $1.4 trillion) and gaining mom mentum in 2011 (approaching $1. trillion). In 2008, FDI inflows we uneven amon the sub region of .8 ere ng ns Latin America and the Caribbean: it was u by 29% in Sou America and d C up uth entral America an the Caribbean. down by 6% in Ce nd Figure 1: Canadian inwa and Outward FDI Stock (CDN$ ard $mn) Source: CANSIM Database Retrieved from w e. www.statcan.gc.ca J 15, 2010 July Canada continues to be a leading global investor as up to 2009, Canada e a e o exported CDN$59 bn in FDI Sto Canada is also a 93.3 ock. dynamiic global investor as between 198 and 2009, the stock of oversea FDI expanded by 9.9% per an r 87 e as d nnum. Canada w a was CA ARICOM M-Canada Trade and Dev a velopme Agree ent ement

- 2. Pa 2 age www.crnm.or w rg major gglobal recipient of FDI attracting CDN$549.4 bn FD stock as at 200 Canada was also a dynamic g f DI 09. global recipient of FDI f with the inward stock of FDI increasing by 7.7% annually b e y between 1987 and 2009 (see figure 1). d e CARIC COM-Canada In nvestment Perf rformance CARICOM continues to be an important destination for Ca anadian FDI stoc attracting almo 10% of Canad total outward FDI ck, ost da’s d stock a at 2009. Howev this outturn w not reciproca as CARICOM Investors found a home in Canada for CDN$470 m of as ver, was al, a mn FDI sto up to 2009 which represente the lowest out ocks w ed tturn since 2003 (see figure 2). Th signals that C his CARICOM Investm ment strategy may not be ad y dequately success in presenting the region as a springboard into Canada for ext sful g o ternal parties, utillising strategiic locational adva antages including market access and investor pro g otection. This investment performance with CARIC COM being a net importer of capital in a comp c petitive global env vironment sets the context for neg e gotiations of a Tra and Developm ade ment Agreem between CA ment ARICOM and Can nada. Figure 2: CARICOM-Ca anada Investmen Performance (CDN$mn) nt Source: CANSIM Database Retrieved from w e. www.statcan.gc.ca J 15, 2010 July As at th end of 2009, th Member States attracting new in he he s nvestment (FDI s stock) from Canad were: da • The Bahamas (CDN$ 11.7bn); • Barbados (CDDN$40.8bn); and • Trinidad & Tob bago (CDN$2.3bbn). Howeve cumulatively, between 1987 and 2009, the Me er, ember States attra acting FDI stock included the thre aforementione as ee ed well as Jamaica and Guyana. Two of th leading host countries in CAR s G he RICOM for Canad investment are those with w dian which Canada has negotiate Bilateral Inves a ed stment Treaties(BITS), specifically, Trinidad and Tobago and Ba arbados. Addition nally, Canada has negotiated double taxation a a avoidance treaties with Barbados (1980), Jamaica (1978) and Trinida & Tobago (199 s ad 95). The Ca anadian statistica authority (STAT al TCAN) does not have a record b between 1987 an 2009 of FDI s nd stocks in Antigua and a Barbud St. Kitts and Nevis; Dominica Haiti; Grenada Belize and Su da; a; a; uriname. Therefo CARICOM L ore, LDCs may be ha aving difficulty attracting Cana y adian investments and the negotiiations of the TA could provide a timely opport s, ADA e tunity for the LDC to Cs signal t capacity to attract Canadian iinvestment. Addit their a tionally, Canada m be investing in CARICOM ind may g directly, through o other third coountries, and as such, the data may reflect the cou s untry of origin of the investment fu unds, rather than the nationality o the n of investor. Member States are invited to su s ubmit any more ddetailed data they may have at the disposal on Ca y eir anadian investme in ent their terrritories. The Mem States that w more dynam at attracting F from Canada were again The B mber were mic FDI Bahamas (9% gr rowth per ann between 198 and 2009); Bar num 87 rbados (22% grow per annum) a Trinidad and T wth and Tobago (18% gro p.a.). owth CARICOM C M-Canada Trade and Dev a velopme Agreement ent

- 3. Page 3 www.crnm.org Interestingly, the Region’s private sector can seek to utilise the provisions of the TADA strategically in two ways: firstly hosting Canadian investors interested in Joint ventures, or acquiring highly leveraged assets in sectors such as those listed in the following section; and secondly, attracting export-oriented investments from Europe and Latin America. Canada Sectoral Investment Performance Up to 2009, over 40% of Canada’s Outward FDI stock was invested in the finance and insurance sector. Other dominant sectors include Mining and Oils and Gas extraction (15% of Outward FDI stock), and Management of companies and enterprises (10.3% of outward FDI stocks). Interestingly however, the fastest sectors for Canadian outward FDI stock included many sectors of interest to CARICOM, and these sectors could be liberalised within the TADA framework. Between 1999 and 2009, the most dynamic sectors for Canadian Outward FDI included: • Furniture and related product manufacturing (29% growth in outward FDI per annum); • Utilities (23.3% growth p.a.); • Support activities for mining and oil and gas extraction (20.2% growth p.a.); • Agriculture, forestry, fishing and hunting (17.6% growth p.a.); • Clothing manufacturing (23.5% growth p.a.); • Food manufacturing (8.2% growth p.a.); and • Chemical manufacturing (11% growth p.a.). Up to 2009, the major sectors in which Canada has been hosting FDI included: Oil and gas extraction; primary metals production; wholesale trade; finance and insurance; petroleum and coal products manufacturing; management of companies and enterprises; and chemical manufacturing. Sectors that Canada has been contracting its FDI stock between 1999 and 2009 included textile product mills; paper manufacturing; computer and electronics manufacturing; and real estate. These areas could prove to be difficult for CARICOM investors to penetrate in the Canadian market. This examination of the sectors in which Canada is investing internationally is important to inform the sector interests in the negotiation of the CARICOM-Canada TADA. For example, CARICOM Member States could seek to encourage investments in the furniture industry by liberalising that industry to Canadian investors in the negotiations of the TADA. Canada is retreating from international investment in sectors including construction; plastics and rubber products manufacturing; and Information and communication technologies (ICT), as there was significant contraction in outward FDI stock between 1999 and 2009. Based on the foregoing, these sectors may prove difficult to attract investors from Canada into the region. CARICOM-Canada Trade and Development Agreement