Demystifying Flexible Staffing's Role in Today's Labor Market & Economy

•

0 gostou•261 visualizações

Andrew Steinerman, JP Morgan Business & Education Services Mr. Steinerman explored how flexible labor is a concurrent indicator of the economy and a leading read on labor. According to Mr. Steinerman's research and relative to past recoveries, flexible labor has seen a faster lift off the bottom in the current cycle, as companies have recognized the value of labor flexibility in the uncertain economic environment following the great recession. This compelling look into the economies of scale for flexible labor also showed how: The professional segment drives flexible staffing growth and profitability Flexible staffing is still a secular growth industry Global trends in flexible staffing penetration

Recomendados

Mais conteúdo relacionado

Mais procurados

Mais procurados (16)

Destaque

Destaque (6)

Semelhante a Demystifying Flexible Staffing's Role in Today's Labor Market & Economy

Semelhante a Demystifying Flexible Staffing's Role in Today's Labor Market & Economy (20)

Último

Último (20)

Demystifying Flexible Staffing's Role in Today's Labor Market & Economy

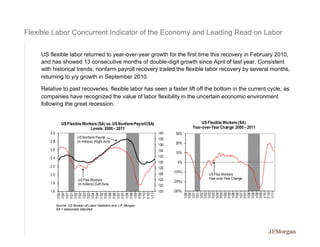

- 1. Flexible Labor Concurrent Indicator of the Economy and Leading Read on Labor US flexible labor returned to year-over-year growth for the first time this recovery in February 2010, and has showed 13 consecutive months of double-digit growth since April of last year. Consistent with historical trends, nonfarm payroll recovery trailed the flexible labor recovery by several months, returning to y/y growth in September 2010. Relative to past recoveries, flexible labor has seen a faster lift off the bottom in the current cycle, as companies have recognized the value of labor flexibility in the uncertain economic environment following the great recession. US Flexible Workers (SA) vs. US Nonfarm Payroll (SA) US Flexible Workers (SA) Levels: 2000 – 2011 Year-over-Year Change: 2000 – 2011 3.0 140 30% US Nonfarm Payroll 138 2.8 (in millions) (Right Axis) 20% 136 2.6 134 10% 2.4 132 130 0% 2.2 128 (10%) 2.0 126 US Flex Workers US Flex Workers 124 Year-over-Year Change 1.8 (20%) (in millions) (Left Axis) 122 1.6 120 (30%) 1/00 1/02 7/02 7/04 1/05 1/07 7/07 1/09 7/09 7/00 1/01 7/01 1/03 7/03 1/04 7/05 1/06 7/06 1/08 7/08 1/10 7/10 1/11 1/00 1/01 7/04 7/05 7/06 7/07 7/08 7/09 7/10 7/00 7/01 1/02 7/02 1/03 7/03 1/04 1/05 1/06 1/07 1/08 1/09 1/10 1/11 Source: US Bureau of Labor Statistics and J.P. Morgan SA = seasonally adjusted

- 2. Professional Segment Drives Flexible Staffing Growth and Profitability Over recent economic cycles, US flexible staffing has been diversifying beyond its traditional commercial staffing base and is gaining further adoption in professional staffing (including accounting/finance and IT) that is key to future secular growth of the broader sector. Light industrial staffing, which led the flex staffing recovery in early 2010 has shown strong growth through the past year, although it has begun to come up against tougher year-over-year comps. IT staffing led the professional staffing segment’s return to year-over-year growth in mid-2010, while non-IT professional staffing (e.g., accounting/finance and legal) returned to growth later in 2010. We believe flexible labor in the professional staffing segment possesses greater opportunities to outpace the growth and profitability of commercial staffing over this economic expansion. US Flexible Staffing Market Growth by Sector Highlights Higher Growth Rates in Professional Staffing: 1996 - 2012F Type of Flexible Staffing 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011F 2012F Office/Clerical 9% 10% 8% 7% 7% (5% ) (5% ) 2% 4% 8% 2% (2% ) (9% ) (24% ) 9% 13% 8% Industrial 7% 10% 6% 7% 7% (12% ) 0% 5% 23% 7% 3% (5% ) (7% ) (25% ) 27% 14% 7% Commercial Staffing 8% 10% 7% 7% 7% (9%) (3%) 4% 14% 7% 3% (4%) (8%) (25%) 19% 14% 7% IT Staffing NA NA 23% 11% 9% (13% ) (21% ) (3% ) 10% 10% 9% 8% (4% ) (20% ) 13% 12% 12% Finance & Accounting 5% 9% 10% 15% 15% 27% 24% (8% ) (3% ) 2% 6% 6% 1% (28% ) (7% ) 4% 9% Technical/Engineering NA NA 21% 24% 26% (9% ) (13% ) 2% 21% 23% 11% 6% (7% ) (29% ) 2% 10% 8% Healthcare 24% 29% 8% 7% 4% 4% (6% ) (3% ) 11% 16% 10% 11% 2% (23% ) 14% 11% 8% Legal NA NA 25% 20% 17% 14% 13% 9% 12% 18% 15% 7% 6% (41% ) 10% 9% 17% Other NA NA 25% 20% 29% 13% (9% ) (1% ) 10% 11% 8% 7% 4% (26% ) 9% 5% 10% Professional Staffing 31% 33% 18% 13% 13% (2%) (7%) (3%) 8% 11% 9% 7% (1%) (25%) 7% 11% 10% Total US Flexible Staffing 16% 19% 12% 10% 10% (5%) (5%) 0% 11% 9% 6% 2% (4%) (25%) 12% 12% 9% Source: Staffing Industry Analysts (SIA), April 2011

- 3. Flexible Staffing Still a Secular Growth Industry Flexible staffing penetration (flexible labor as a % of the total labor market) in the 2002-2007 upcycle peaked at 1.96% in November 2005, slightly below the 2.03% level achieved during the previous expansion. The flexible labor peak of 2005 did not surpass prior peaks because of: 1) a relatively deeper trough following the 2001 recession, 2) a relatively shorter expansionary cycle of 2002-2007, and 3) the IT staffing drag in 2002-2003. We believe flexible labor in the US still has ample secular growth potential, despite not surpassing the prior peak levels in the last economic expansion, as the memory of the great recession continues to spur businesses to look to flex staffing as a source of agility in an uncertain economic environment. Rising Rate of Increase in Flex Penetration Over Economic Cycles, 1972 -2011 2.25% Flex Penetration 2.00% 1.72% in April '11 D 1.75% C E 1.50% 1.25% 1.00% B 0.75% A 0.50% 0.25% 0.00% 1/72 1/74 1/76 1/78 1/80 1/82 1/84 1/86 1/88 1/90 1/92 1/94 1/96 1/98 1/00 1/02 1/04 1/06 1/08 1/10 Source: US Bureau of Labor Statistics, National Bureau of Economic Research, and J.P. Morgan

- 4. Global Trends in Flexible Staffing Penetration The US has long enjoyed liberal labor regulations related to flexible staffing. American companies and workers have both benefited from the flexibility offered by staffing services. The long-term trend is toward global deregulation/adoption of flex staffing due to the benefits of flexible labor, despite the residual opposition from unions and socialist political parties. Flexible staffing offers benefits to companies (by allowing for a more variable cost base and opportunities to preview full-time workers), to workers (by allowing for more flexible work-life arrangements), and to governments/society (by helping to reduce unemployment rates and related costs). 2009 Flexible Staffing Penetration in Key Global Regions 3.6% 2.5% 1.7% 1.7% 1.7% 1.6% 1.3% 0.7% U.K. Netherlands France Belgium Japan Germany U.S. Italy Source: CIETT Economic Report 2011