abortion pills in Jeddah Saudi Arabia (+919707899604)cytotec pills in Riyadh

Market Outlook 13th July 2011

1. Market Outlook

India Research

July 13, 2011

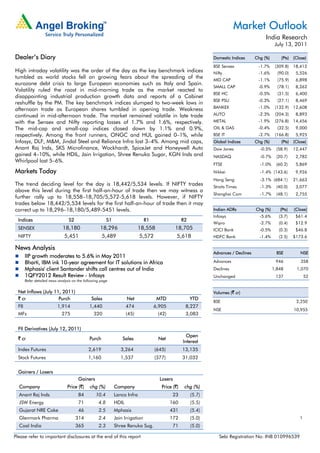

Dealer’s Diary Domestic Indices Chg (%) (Pts) (Close)

BSE Sensex -1.7% (309.8) 18,412

High intraday volatility was the order of the day as the key benchmark indices Nifty -1.6% (90.0) 5,526

tumbled as world stocks fell on growing fears about the spreading of the MID CAP -1.1% (75.9) 6,898

eurozone debt crisis to large European economies such as Italy and Spain.

SMALL CAP -0.9% (78.1) 8,262

Volatility ruled the roost in mid-morning trade as the market reacted to

BSE HC -0.5% (31.5) 6,400

disappointing industrial production growth data and reports of a Cabinet

BSE PSU -0.3% (27.1) 8,469

reshuffle by the PM. The key benchmark indices slumped to two-week lows in

BANKEX -1.0% (132.9) 12,608

afternoon trade as European shares tumbled in opening trade. Weakness

continued in mid-afternoon trade. The market remained volatile in late trade AUTO -2.3% (204.3) 8,893

with the Sensex and Nifty reporting losses of 1.7% and 1.6%, respectively. METAL -1.9% (276.8) 14,456

The mid-cap and small-cap indices closed down by 1.1% and 0.9%, OIL & GAS -0.4% (32.5) 9,000

respectively. Among the front runners, ONGC and HUL gained 0–1%, while BSE IT -2.7% (166.8) 5,925

Infosys, DLF, M&M, Jindal Steel and Reliance Infra lost 3–4%. Among mid caps, Global Indices Chg (%) (Pts) (Close)

Anant Raj Inds, SKS Microfinance, Wockhardt, SpiceJet and Honeywell Auto Dow Jones -0.5% (58.9) 12,447

gained 4–10%, while HDIL, Jain Irrigation, Shree Renuka Sugar, KGN Inds and NASDAQ -0.7% (20.7) 2,782

Whirlpool lost 5–6%.

FTSE -1.0% (60.2) 5,869

Markets Today Nikkei -1.4% (143.6) 9,926

Hang Seng -3.1% (684.1) 21,663

The trend deciding level for the day is 18,442/5,534 levels. If NIFTY trades Straits Times -1.3% (40.0) 3,077

above this level during the first half-an-hour of trade then we may witness a

Shanghai Com -1.7% (48.1) 2,755

further rally up to 18,558–18,705/5,572-5,618 levels. However, if NIFTY

trades below 18,442/5,534 levels for the first half-an-hour of trade then it may

correct up to 18,296–18,180/5,489-5451 levels. Indian ADRs Chg (%) (Pts) (Close)

Infosys -5.6% (3.7) $61.4

Indices S2 S1 R1 R2

Wipro -2.7% (0.4) $12.9

SENSEX 18,180 18,296 18,558 18,705 ICICI Bank -0.5% (0.3) $46.8

NIFTY 5,451 5,489 5,572 5,618 HDFC Bank -1.4% (2.5) $173.6

News Analysis

Advances / Declines BSE NSE

IIP growth moderates to 5.6% in May 2011

Bharti, IBM ink 10-year agreement for IT solutions in Africa Advances 946 358

Mphasis' client Santander shifts call centres out of India Declines 1,848 1,070

1QFY2012 Result Review - Infosys Unchanged 137 52

Refer detailed news analysis on the following page

Net Inflows (July 11, 2011) Volumes (` cr)

` cr Purch Sales Net MTD YTD

BSE 2,250

FII 1,914 1,440 474 6,905 8,227

NSE 10,955

MFs 275 320 (45) (42) 3,083

FII Derivatives (July 12, 2011)

Open

` cr Purch Sales Net

Interest

Index Futures 2,619 3,264 (645) 13,135

Stock Futures 1,160 1,537 (377) 31,032

Gainers / Losers

Gainers Losers

Company Price (`) chg (%) Company Price (`) chg (%)

Anant Raj Inds 84 10.4 Lanco Infra 23 (5.7)

JSW Energy 71 4.8 HDIL 160 (5.5)

Gujarat NRE Coke 46 2.5 Mphasis 431 (5.4)

Glenmark Pharma 314 2.4 Jain Irrigation 172 (5.0) 1

Coal India 365 2.3 Shree Renuka Sug. 71 (5.0)

Please refer to important disclosures at the end of this report Sebi Registration No: INB 010996539

2. Market Outlook | India Research

IIP growth moderates to 5.6% in May 2011

The pace of industrial production moderated further in May 2011, with IIP growth slowing

to 5.6% from a downwardly revised 5.8% in April 2011. The latest IIP print was well below

Bloomberg’s median forecast of 8.5%.

Growth in manufacturing production, which accounts for 80% of the industrial production,

slowed to 5.6% (vs. 6.3% in April 2011 and 8.9% in May 2010). In terms of industries, 14

of the 22 industry groups in the manufacturing sector registered positive growth during

May 2011. Mining production growth was muted at 1.4% (1.3% in April 2011) compared

to strong 7.8% growth in May 2010. Growth in electricity picked up sharply to 10.3% from

6.5% in April 2011 and 6.2% in May 2010.

As per use-based data, basic goods recorded growth of 7.2% compared to 6.1% in May

2010 and 6.9% growth in April 2011. Capital goods’ performance cooled off to 5.9%

compared to 7.3% (revised from 14.5%) growth in April 2011. Consumer durables

continued to report slower growth trend witnessed in April 2011, with growth of 5.2%;

overall consumer goods grew by 5.4% during May 2011.

The moderating growth trend is in-line with the RBI’s target of reducing demand-side

inflationary pressures even if it means sacrificing a bit of short-term growth. Though

elevated inflation numbers may prompt the RBI to persist with one or two more hikes in its

repo rates, overall looking at the signs of cooling global commodity prices, moderating

food inflation, weakening domestic demand, slowing credit off-take and higher deposit

mobilisation, we believe both inflation and interest rates are likely to start cooling off from

2HFY2012.

Bharti, IBM ink 10-year agreement for IT solutions in Africa

Bharti Airtel (Bharti) has signed a 10-year agreement with IBM to provide IT solutions to its

employees across 16 African countries. IBM will provide a standard operating

environment, help desk and desk-side support to enhance employee efficiency and

convenience. The deal size has not been disclosed. This is in addition to a partnership

signed in late 2010 between the two sides to manage the computing technology and

services to power Bharti’s mobile communications network spanning 16 African countries.

As part of the new agreement, IBM will provide end-user services to Bharti’s employees

across Africa, in French and English. The consolidation of Bharti's helpdesks is expected to

bring about greater cost savings and efficiencies through streamlining of the processes for

addressing IT operational issues. We maintain our Neutral rating on the stock.

Mphasis' client Santander shifts call centres out of India

Santander, a UK-based financial services firm, has decided to stop outsourcing services to

Mphasis and shift all its Indian call centres for retail banking customers back home.

Santander announced that it is recalling outsourced work from India back to the UK

following complaints by customers over their frustration in dealing with offshore

employees. Santander has hired an additional 500 UK staff to handle the estimated 1.5mn

calls each month. The new staff is fully trained and is now available to take calls. In total,

Santander's UK call centres employ 2,500 staff. Santander is a wholly owned unit of

Spain's Banco Santander S.A. This client contributes 2–3% to Mphasis’ BPO revenue

(~i.e.US$5mn annually) and is not amongst its top clients. This contract is expected to

cease from August 2011 (i.e. from 4QFY2011).

We expect this to have a marginal impact on the company’s earning’s estimate. The stock

is currently under review.

July 13, 2011 2

3. Market Outlook | India Research

1QFY2012 Result Review

Infosys

For 1QFY2012, Infosys reported revenue of US$1,671mn, up 4.3% qoq, primarily on the

back of decent 4.0% qoq volume growth. The 4.0% qoq volume growth was mainly driven

by 6.8% qoq growth in onsite volumes; offshore volumes grew by 2.7% qoq. Pricing

remained stable during the quarter. The cross-currency movement benefited USD revenue

by 1.2% qoq. In INR terms, revenue came in at `7,485cr, registering 3.2% qoq growth.

The company’s EBITDA and EBIT margins declined by 298bp and 291bp qoq to 29.1%

and 26.1%, respectively, due to wage hikes given in 1QFY2012 (10–12% for offshore

employees and 2–3% for onsite employees) effective from April 1, 2011. Also, EBIT margin

got negatively impacted by 40bp qoq due to INR appreciation against USD. PAT stood at

`1,722cr, down 5.4% qoq.

The FY2012 USD revenue growth guidance was left unchanged at 18–20% yoy to

US$7.13bn–7.25bn. For 2QFY2012, Infosys has guided for 3.5–5.0% qoq growth in USD

revenue to US$1.730bn–1.755bn, which is lower than our expectations. EPS guidance for

FY2012 increased to US$2.88–2.92, 10.0–11.5% yoy growth vs. the previous guidance of

8–10% yoy growth. We recommend Accumulate rating on the stock with target price of

`3,200.

Economic and Political News

Borrowing in FY2012 not to exceed `4.17lakh crores: Finance Minister

PM axes seven ministers, inducts eight new faces in minor cabinet reshuffle

Finance Ministry okays 6 PPP road projects worth `9,774cr

NHAI seeks to bypass green nod for land

Corporate News

HCL may buy out DLF stake in Insurance JV

M&M plans to enter non-life insurance space

Lavasa not ready to accept MoEF pre-conditions for hill city

Source: Economic Times, Business Standard, Business Line, Financial Express, Mint

Events for the day

Bajaj Finserv Results

Bajaj Finance Results

MPS Results

July 13, 2011 3

4. Market Outlook | India Research

Research Team Tel: 022-3935 7800 E-mail: research@angelbroking.com Website: www.angelbroking.com

DISCLAIMER

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Angel Broking Limited, its affiliates, directors, its proprietary trading and investment businesses may, from time to time, make investment

decisions that are inconsistent with or contradictory to the recommendations expressed herein. The views contained in this document are

those of the analyst, and the company may or may not subscribe to all the views expressed within.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable sources

believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this document is for

general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way responsible for any loss or

damage that may arise to any person from any inadvertent error in the information contained in this report. Angel Broking Limited has

not independently verified all the information contained within this document. Accordingly, we cannot testify, nor make any representation

or warranty, express or implied, to the accuracy, contents or data contained within this document. While Angel Broking Limited

endeavours to update on a reasonable basis the information discussed in this material, there may be regulatory, compliance, or other

reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Angel Broking Limited and its affiliates may seek to provide or have engaged in providing corporate finance, investment banking or other

advisory services in a merger or specific transaction to the companies referred to in this report, as on the date of this report or in the past.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Note: Please refer to the important ‘Stock Holding Disclosure' report on the Angel website (Research Section). Also, please refer to the

latest update on respective stocks for the disclosure status in respect of those stocks. Angel Broking Limited and its affiliates may have

investment positions in the stocks recommended in this report.

Ratings (Returns): Buy (> 15%) Accumulate (5% to 15%) Neutral (-5 to 5%)

Reduce (-5% to 15%) Sell (< -15%)

Address: 6th Floor, Ackruti Star, Central Road, MIDC, Andheri (E), Mumbai - 400 093.

Tel: (022) 3935 7800

Angel Broking Ltd: BSE Sebi Regn No : INB 010996539 / CDSL Regn No: IN - DP - CDSL - 234 - 2004 / PMS Regn Code: PM/INP000001546

Angel Capital & Debt Market Ltd: INB 231279838 / NSE FNO: INF 231279838 / NSE Member code -12798 Angel Commodities Broking (P) Ltd: MCX Member ID: 12685 / FMC Regn No: MCX / TCM /

CORP / 0037 NCDEX : Member ID 00220 / FMC Regn No: NCDEX / TCM / CORP / 0302

July 13, 2011 4