Portugal Income Tax - 20% Low Tax Non Habitual Resident Scheme

•

2 gostaram•2,639 visualizações

Portugal -20% Low Tax Income Scheme & Tax Exemptions for Non Habitual Residents. How to achieve Portugal's reduced tax rates.

Recomendados

Recomendados

Mais conteúdo relacionado

Mais de Acumum - Legal & Advisory

Mais de Acumum - Legal & Advisory (17)

Último

Último (20)

Portugal Income Tax - 20% Low Tax Non Habitual Resident Scheme

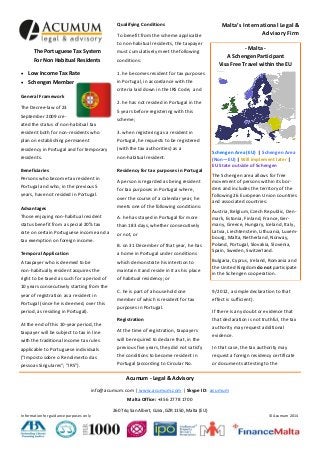

- 1. Qualifying Conditions To benefit from the scheme applicable to non-habitual residents, the taxpayer The Portuguese Tax System must cumulatively meet the following For Non Habitual Residents conditions: Low Income Tax Rate - Malta A Schengen Participant Visa Free Travel within the EU 1. he becomes resident for tax purposes Schengen Member Malta’s International Legal & Advisory Firm in Portugal, in accordance with the criteria laid down in the IRS Code; and General Framework 2. he has not resided in Portugal in the The Decree-law of 23 5 years before registering with this September 2009 created the status of non-habitual tax scheme; resident both for non-residents who 3. when registering as a resident in plan on establishing permanent Portugal, he requests to be registered residency in Portugal and for temporary (with the tax authorities) as a residents. non-habitual resident. Beneficiaries Residency for tax purposes in Portugal Persons who become tax resident in Portugal and who, in the previous 5 years, have not resided in Portugal. A person is regarded as being resident for tax purposes in Portugal where, over the course of a calendar year, he Advantages meets one of the following conditions: Those enjoying non-habitual resident A. he has stayed in Portugal for more status benefit from a special 20% tax than 183 days, whether consecutively rate on certain Portuguese income and a or not, or tax exemption on foreign income. B. on 31 December of that year, he has Temporal Application a home in Portugal under conditions A taxpayer who is deemed to be which demonstrate his intention to non-habitually resident acquires the maintain it and reside in it as his place right to be taxed as such for a period of of habitual residency; or 10 years consecutively starting from the year of registration as a resident in Portugal (since he is deemed, over this period, as residing in Portugal). At the end of this 10-year period, the Schengen Area (EU) | Schengen Area (Non—EU) | Will implement later | EU State outside of Schengen The Schengen area allows for free movement of persons within its borders and includes the territory of the following 26 European Union countries and associated countries: Austria, Belgium, Czech Republic, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Iceland, Italy, Latvia, Liechtenstein, Lithuania, Luxembourg, Malta, Netherland, Norway, Poland, Portugal, Slovakia, Slovenia, Spain, Sweden, Switzerland. Bulgaria, Cyprus, Ireland, Romania and the United Kingdom do not participate in the Schengen cooperation. C. he is part of a household one 9/2012, a simple declaration to that member of which is resident for tax effect is sufficient). purposes in Portugal. Registration If there is any doubt or evidence that that declaration is not truthful, the tax authority may request additional taxpayer will be subject to tax in line At the time of registration, taxpayers with the traditional income tax rules will be required to declare that, in the applicable to Portuguese individuals previous five years, they did not satisfy In that case, the tax authority may ("Imposto sobre o Rendimento das the conditions to become resident in request a foreign residency certificate pessoas Singulares"; "IRS"). Portugal (according to Circular No. or documents attesting to the evidence. Acumum - Legal & Advisory info@acumum.com | www.acumum.com | Skype ID: acumum Malta Office: +356 2778 1700 260 Triq San Albert, Gzira, GZR 1150, Malta (EU) Information for guidance purposes only © Acumum 2014

- 2. income earned in Portugal which does not qualify for the special 20% rate in Malta’s International Legal & Advisory Firm order to determine which of the pro- The Portuguese Tax System For Non Habitual Residents gressive tax rates applies to the total Conditions income). governing the Circular No. 2/2010 provides that Low Income Tax Rate income in categories A and B earned Schengen Member abroad, to which the exemption existence of close personal and method does not apply (because they economic ties to another state. do not meet the qualifying conditions) are to be taxed at the special rate of Taxation 20% where this income is derived from Income earned in Portugal a high added value activity. Income in Category A (income from application of the exemption in respect of category B, E, F or G income, (professional income, entrepreneurial income, income from land, capital income & capital gains) It is sufficient that one of the following conditions is met: employment) and B (income from Conditions governing the exemption entrepreneurial and professional work) in respect of Category A income (paid 1. such income is liable to be taxed in of the IRS are subject to a special tax work) another Contracting State in rate of 20%, provided that it comes It is sufficient that one of the following from high added value activities - avoidance of double taxation entered conditions is met: into by Portugal with that state; or 1. such income is, in effect, subject to 2. where no such convention exists, it is tax in the other Contracting State in liable to be taxed in the other country, Other Income accordance with the Convention for territory or region, according to the Included in other categories of the IRS, the elimination of double taxation OECD Model Tax Convention on are subject to tax in accordance with entered into by Portugal with that Income and on Capital, provided that the general taxation rules applicable to state, or such income does not come from a 2. where no such convention exists, territory classified as a tax haven by the income is, in effect, taxed in the Portugal and is not considered as other country, territory or region, having been earned in Portugal. provided it is not considered as having It is not necessary, in this scenario, that being earned in Portugal such income is actually subject to tax supplementary tax of 2.5% will be If such income is not taxed in the abroad, but they could potentially be. imposed). source State, it will benefit from the Where income is not taxed by the preferential 20% tax rate. source State, it will be able, however, Note: a non-habitual resident can al- to benefit from the preferential tax ways opt for the tax credit method to rate of 20%. be applied, in which case he is obliged Conditions governing the application to include his income for tax purposes. of the exemption in respect of cate- activities which are defined in Order No. 12/2010 of 7 January (see Annex). habitual residents and, therefore, subject to the progressive tax rates applicable to Portuguese income (up to a maximum rate of 46.5%, in addition to which, on any taxable income exceeding €153,300, a Income earned abroad Elimination of international double taxation through the application of the exemption method: if certain conditions are met, income earned accordance with the Convention for the gory H income (pensions): the special abroad will not be taxed in Portugal, it case of foreign retirees will however be counted for accounting purposes together with Acumum - Legal & Advisory info@acumum.com | www.acumum.com | Skype ID: acumum Malta Office: +356 2778 1700 260 Triq San Albert, Gzira, GZR 1150, Malta (EU) Information for guidance purposes only © Acumum 2014

- 3. It is sufficient that one of the following conditions is met: 408 – Medical physiotherapists; 409 – Gastroenterologists; 410 – Ophthalmologists; 411 – Orthopaedists; 412 – Otolaryngologists (ENT); 413 – Paediatricians; 414 – Radiologists; 415 – Doctors - other specialised 5 – Teachers:501 – University professors. 6 – Psychologists: 601 – Psychologists. 7 – Liberal, technical & related professions: 701 – Archaeologists; 702 – Biologists and experts in life sciences; 703 – Computer programmers; 704 – Computer consultancy and programming activities related to information and computer technology; 705 – Computer programming activities; 706 – Information technology consultancy; 707 – Management and operation of computer hardware; 708 – Information services activities; 710 – Data processing, hosting & elated activities; 711 – Other information service activities; 712 – Media activities; 713 – Other information service activities; 714 – Scientific research and development; 715 – Research and development related to natural and physical sciences; 716 – Biotechnology research and development; 717 – Designers. 8 – Investors, Managers and Administrators: 801 – Investors, administrators and managers who foster productive investment if attached to projects which are eligible and employed under contracts which confer tax benefits entered into in accordance with the General Tax Code, approved by Decree-Law No. 249/2009 of 23 September; 802 – Senior business executives. public pensions are, in principle, subject to tax exclusively in the state of 1. such income is taxed in the other the paying agency. Contracting State in accordance with the Example: The tax convention between Convention for the avoidance of double France and Portugal grants the taxation entered into by Portugal with exclusive right to tax private pensions that state, or to the state of residency. Persons 2. it is not considered as having been earned in Portugal. resident for more than 183 days in Portugal who were not resident for tax purposes in Portugal in the previous 5 IMPORTANT: This scheme is very attrac- years may therefore benefit from tive for foreign retirees whose pensions being non-habitual resident in are from States which, under the Con- Portugal. In these circumstances, vention for the avoidance of double private pensions from France will not taxation entered into between Portugal be subject to tax in France and will, and the state, grant the exclusive right moreover, be exempt from taxation in to tax pensions to the state in which the Portugal. pension recipient resides (e.g. United ANNEX—Order No. 12/2010 high States, Switzerland, Luxembourg, Malta, added value activities 1 - Architects, engineers and similar technicians 101 – Architects; 102 – Engineers; 103 – Geologists. 2 – Artists, actors and musicians: 201 – Theatre, ballet, cinema, radio and television performers; 202 – Singers; 203 – Sculptors; 204 – Musicians; 205 – Painters. 301 – Auditors; 302 – Tax Consultants. 4 - Doctors and dentists: 401 – Dentists; 402 – Analysts; 403 – Surgeons; 404 – Ship's doctors; 405 – GPs; 406 – Dentists; 407 – Stomatologists; Spain, etc.) double non-taxation, namely, the income is not subject to tax in the source state and is exempt in the state of residency. In practice, this device can often result in the income not being subject to tax in either the source state or Portugal, since the majority of tax treaties entered into by Portugal, based on the OECD model, provide that, in respect of private pensions, the taxpayer may be subject to tax only in the state where he resides. Only Acumum - Legal & Advisory ‘Uniquely local - Uniquely International’ Located in the EU tax efficient jurisdiction of Malta, Acumum Legal & Advisory employs Maltese, UK, & international lawyers & tax accountants - with extensive on-location & off-shore international experience - providing appropriate, bespoke solutions. Taxation Corporate & Company Formation Financial Services Licenses Gaming Aviation Insurance Licenses Intellectual Property Trusts & Foundations Maritime & Yachts Telco, Tech, Media Estate & Wealth Management Arbitration & Litigation Immigration & Residency Divisions Compliance Accounting, Tax & Back Office Outsourcing info@acumum.com | www.acumum.com | Skype ID: acumum Malta Office: +356 2778 1700 260 Triq San Albert, Gzira, GZR 1150, Malta (EU) Information for guidance purposes only © Acumum 2014